|

Gordon T Long Research exclusively distributed at MATASII.com

Subscribe to Gordon T Long Research - $35 / Month - LINK

Complete MATASII.com Offerings - $55/Month - LINK

SEND YOUR INSIGHTFUL COMMENTS - WE READ THEM ALL - lcmgroupe2@comcast.net

| |

|

UnderTheLens - OCTOBER 2024

Macro Analytics - 09/30/24

| |

CHINA VERY NEAR A "WHATEVER IT TAKES" MOMENT!

OBSERVATIONS: FED RATES CUTS ARE BEING DONE DIFFERENTLY. SILENTLY, WE ARE NOW FOOTING THE BILL!

It appears that few people fully understand how the Fed actually reduces the Fed Funds Rate nowadays. The Fed is doing it differently behind the scenes than most imagine. The method the Fed uses to control the Federal Funds Rate is very different from the method it used before it launched Quantitative Easing in late 2008. Interest rates today would be much lower than they are – despite the government’s very large budget deficits – if the Fed were not intervening to keep them high. That is because the Fed now actually pays the banks substantial fees for their Bank Reserves and Reverse Repurchase Agreements. How did this happen? Let me explain how you are being handed the bill.

When the Fed launched Quantitative Easing at the end of 2008, it did so by buying Government Bonds and Mortgage-Backed Securities. This caused its Total Assets to surge. The Fed paid for those assets by creating and depositing Bank Reserves into the Reserve Accounts that commercial banks hold at the Fed. Before 2008, there were almost no Bank Reserves. Now there are $3.2 trillion.

- The Federal Funds Rate is the interest rate at which commercial banks lend Bank Reserves to one another.

- Normally, all the other interest rates throughout the economy, such as bond yields, mortgage rates, credit card rates, etc., follow the Federal Funds Rate up and down.

- Before 2008, the very low amount of Bank Reserves made it easy for the Fed to control the Federal Funds Rate.

PRE-2008

If the Fed wanted to cool the economy down to slow the rate of inflation, it could sell to commercial banks a few government bonds that it had bought in the past. When the commercial banks bought those bonds, the Fed would take payment by debiting the Reserve Accounts belonging to the banks that had bought the bonds. Taking Bank Reserves out of those accounts lowered the level of Bank Reserves in the banking system. As Bank Reserves became scarcer, the cost of borrowing those Reserves, the Federal Funds Rate would rise.

Conversely, when the Fed wished to stimulate the economy, it would buy some government bonds from commercial banks, paying for them by depositing Bank Reserves into the Reserve Accounts of the commercial banks from which it had bought the bonds. That would make Bank Reserves more plentiful throughout the banking system, and that would drive down the cost of borrowing Bank Reserves, i.e. it would drive down the Federal Funds Rate. As the Federal Funds Rate fell, so would all the other interest rates and lower rates would stimulate economic growth.

POST-2008

However, once the Fed had created trillions of dollars of Bank Reserves through QE, it was no longer possible for the Fed to control the Federal Funds Rate by making relatively small changes to the quantity of Bank Reserves using the method used priorly. Post-QE, Bank Reserves were far too plentiful for that. So the Fed had to find a new way to control the Federal Funds Rate, which it did. It now controls the Federal Funds Rate by paying the commercial banks interest on their Bank Reserves, something that was not legally permitted until 2008.

The Fed pays an interest rate to the commercial banks for the Bank Reserves they own. This is officially called the Interest Rate On Reserve Balances (IORB). When the Fed pays 5.4% interest on Bank Reserves, as it was doing up until it cut rates Sept 18th, that ensures that the commercial banks won’t lend to anyone at less than 5.4%. Why would they when they can earn 5.4% from the Fed?

When inflation spiked following Covid, the Fed began increasing the Federal Funds Rate by paying a higher and higher rate of interest to the commercial banks on their Bank Reserves. The rate paid by the Fed peaked near 5.4%. This is how the Fed kept the Federal Funds Rate in a range between 5.25% and 5.5% from August 2023 until last week. ===>

| |

|

VIDEO PREVIEW (click image)

Pay-Per-View Page Link

|  | |

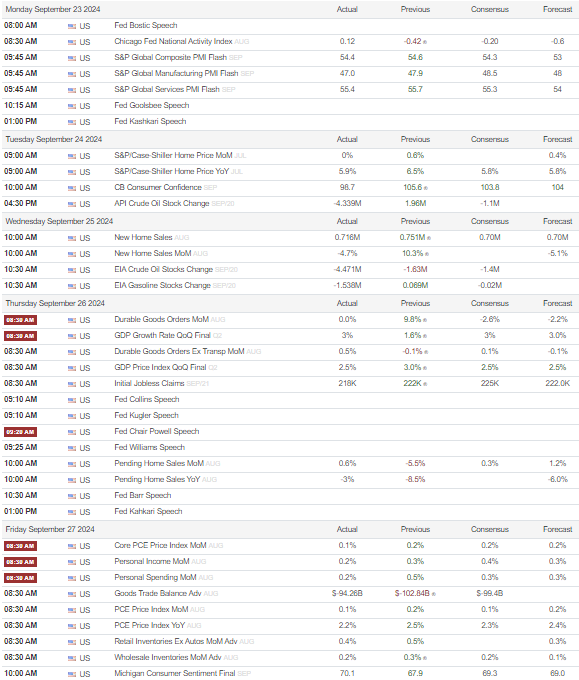

THIS WEEK WE SAW

Exp=Expectations, Rev=Revision, Prev=Previous

US

US New Home Sales Change MM (Aug) -4.7% (Prev. 10.6%)

US Building Permits R Change MM (Aug) 4.6% (Prev. 4.9%)

US GDP Final (Q2) 3.0% vs. Exp. 3.0% (Prev. 3.0%)

US Pending Sales Change MM (Aug) 0.6% vs. Exp. 1.0% (Prev. -5.5%)

===> Now, however, the Fed believes it’s time to reduce interest rates. So, as of last week, the Fed began paying 50 basis points less on Bank Reserves. Now, the Fed’s only paying 4.9% on Bank Reserves. Since the Fed is only willing to pay 4.9% to the commercial banks, those banks will now be willing to lend out money at 4.95%, for instance, whereas before they wouldn’t lend for less than 5.4%.

The Fed is expected to continue lowering the FFR. At its FOMC meeting two weeks ago, the Fed published the projections of the FOMC members showing that, on average, they expect the FFR to fall to 4.4% by the end of this year, to 3.4% next year, and to 2.9% in 2026. That suggests the Fed will cut the FFR by another 200-basis point over the next two and a quarter years. It will do that by paying less and less interest on Bank Reserves.

There are so many Bank Reserves washing around the banking system that the Fed has to pay interest on them to keep interest rates as high as they are now. As the Fed pays less on those Bank Reserves during the months ahead, the Federal Funds Rate will fall and so will most other interest rates throughout the economy – regardless of how much money the government borrows to finance its very large budget deficits.

That’s because the government borrowing doesn’t change the level of Bank Reserves, so long as the government spends the money it borrows. When the government spends, the money it borrowed gets re-injected back into the economy and the amount of Bank Reserves remains unchanged. When we add Bank Reserves and Reverse Repos together this amounts to $3.9 trillion of excess Liquidity that the Fed must pay interest on to prevent interest rates from falling. $3.9 trillion is a lot of Liquidity, but not as much as before. The peak was $6.2 trillion in Dec. 2021. This excess Liquidity is currently shrinking now due to QT.

BOTTOM LINE

Who cares about all this? You should because the Fed is losing significant money this way. This reduces the money it was returning to the US Treasury. Basically the money is coming out of our pockets in taxes and into the banks' pockets. They are getting richer while we wonder why we are getting poorer? QE was an expensive "Kick-the-Can".

| |

========================= | |

|

WHAT YOU NEED TO KNOW!

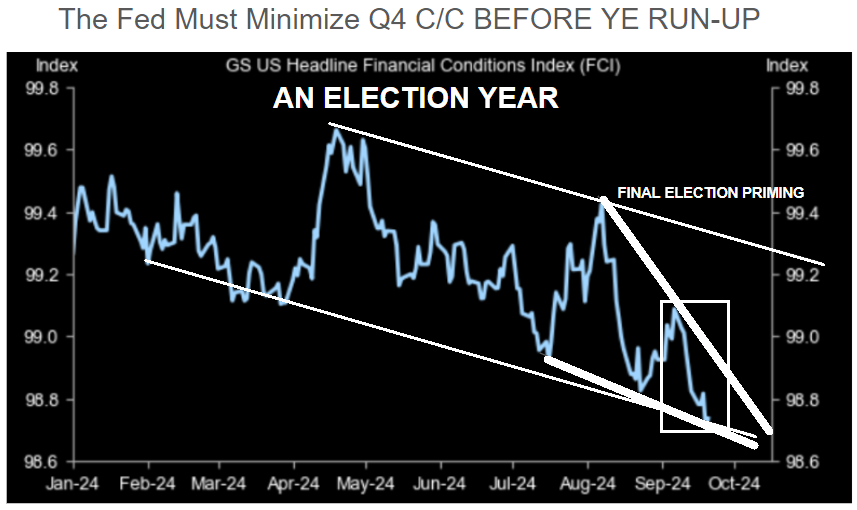

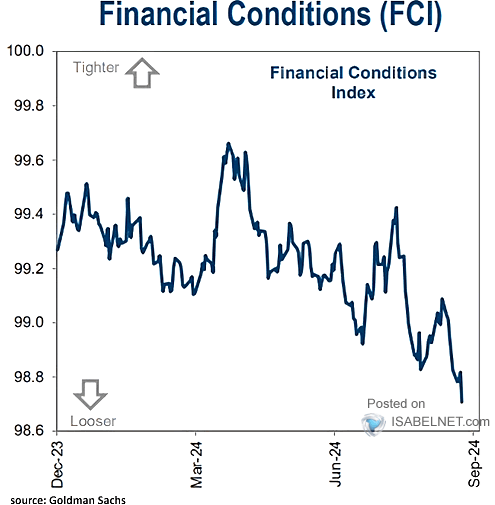

FINANCIAL CONDITIONS LOOSENED EVEN FURTHER?

If the Fed isn't "political", then why is Financial Conditions (as Measured by the Financial Conditions Index - FCI) loosening EVEN FURTHER - as we close into the November 5th US Election?

The rates have been loosened all year, but recently have taken yet another nosedive lower! With China launching major reflation efforts, excess liquidity can be expected to increase further (as well as Inflation Pressures).

| |

|

RESEARCH

1- CHINA NEARS THE "WHATEVER IT TAKES" MOMENT!

US LOOSENING INTO ALREADY EXTREMELY LOOSE FINANCIAL CONDITIONS

+ CHINA NOW REFLATING

+ EXTREME LIQUIDITY (Last Week's Detail)

= INFLATION RE-IGNITED

- THURSDAY ANNOUNCEMENT - From the Politburo: Significant Fiscal Policy Support (Details in Research)

- TUESDAY ANNOUNCEMENT- From the PBOC: Important Monetary Policy support (Details in Research)

- SIGNALLING TO COME: Social Support (Lift Home Purchase Curbs)

- HSTECH is up some 30% over the past week. This is no small cap, this is China's Tech Index!

- CSI 300 - Best Week since 2008

2- IGNORE PUTIN AT OUR PERIL!

- The narrative from mainstream media is that Russia President Vladimir Putin is attempting to "blackmail" the US and NATO regarding the use of Nuclear Weapons.

- I don't buy into this White House summation of Putin's strategic shift.

- The truth is no matter what Putin says the Biden Administration is not listening. There is no diplomacy occurring, which only leads to mis-calculated mistakes and worse. Like the Cuban Missile Crisis it is time for Leadership. The White House is playing with matches here and no one seems to be at the helm and in charge.

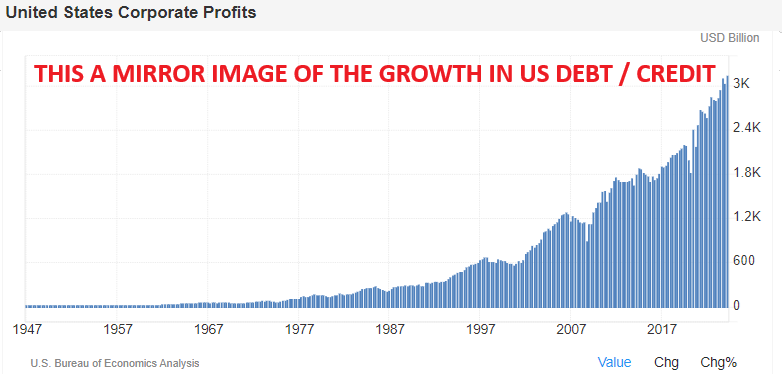

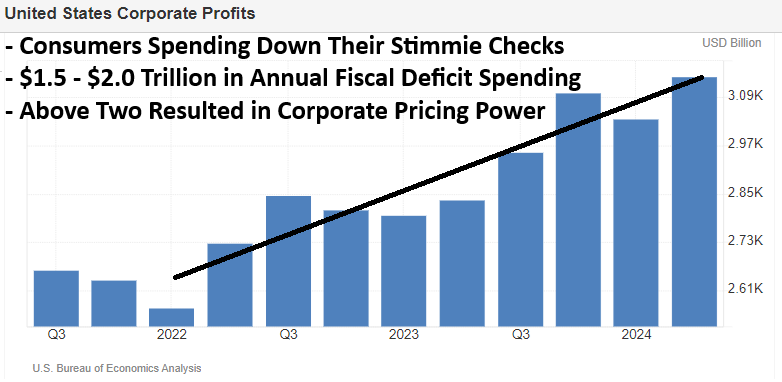

3- A STEADILY RISING CORPORATE PROFITS DANCE?

-

QUESTION: Why Are US Corporate Profits Rising So Quickly?

-

ANSWER: Debt/Credit Growth =~GDP Growth =~ Nominal Profit Growth.

-

PUBLIC NARRATIVE: We show how Microsoft's AI Bot "Copilot" answered the question. Quite entertaining, but missing the essence of the question in delivering what the public might believe.

| |

|

DEVELOPMENTS TO WATCH

REDFIELD LABELS IT AS "AGENCY CAPTURE"

(Further support of this month's UnderTheLens Video)

-

Former CDC Director Robert Redfield wrote an editorial in Newsweek on Tuesday explaining the causes for this obesity crisis are primarily due to:

"Special interest and corporate influences on our federal agencies."

Kennedy is right: All three of the principal health agencies suffer from agency capture. A large portion of the FDA's budget is provided by pharmaceutical companies. NIH is cozy with biomedical and pharmaceutical companies and its scientists are allowed to collect royalties on drugs NIH licenses to pharma. And as the former director of the Centers for Disease Control and Prevention (CDC), I know the agency can be influenced by special interest groups.

-

Redfield acknowledges that agency capture is a serious issue, highlighting that federal agencies responsible for regulating food and medicine are possibly compromised by the food industrial complex and big pharma.

FOOD IS THE ULTIMATE WEAPON OF CONTROL

- We face a near-term future in which the control mechanisms will be all-pervasive.

-

Elites have known for millennia, it is food that is the ultimate weapon of control.

- As former US Secretary of State articulated in 1973: ‘Who controls the food supply controls the people’.

-

Professor George Kent eloquently explained in 2008, it is in the interest of the Elite that people are hungry. See ‘The Benefits of World Hunger’.

- So any critical analysis of what is being imposed on humanity must take careful account of how food – and the farming of it – is being utterly transformed.

| |

|

GLOBAL ECONOMIC REPORTING

US PERSONAL CONSUMPTION EXPENDITURE (PCE)

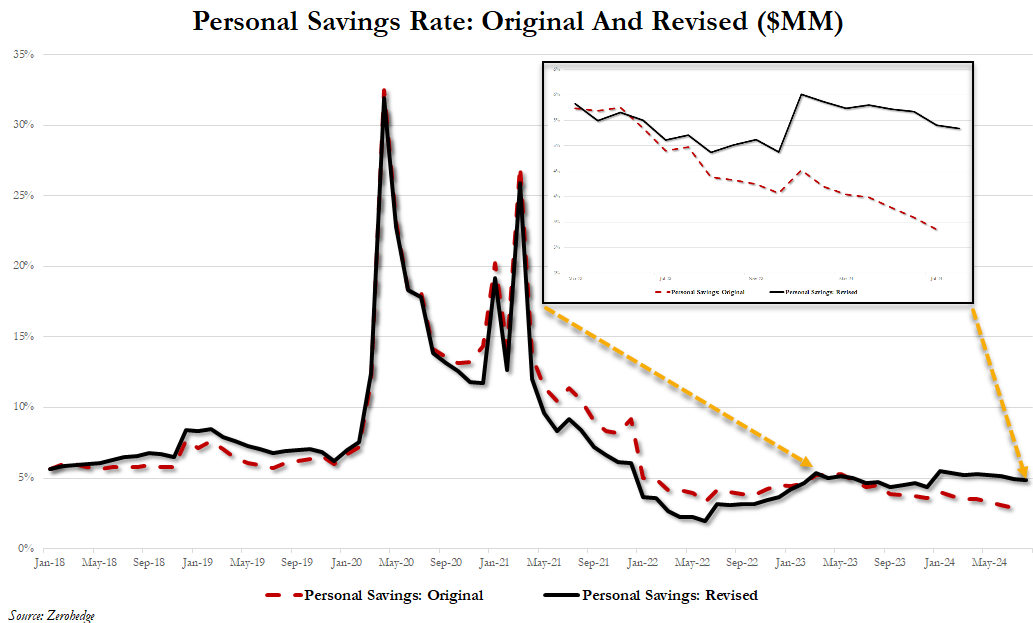

- A 2 percentage point revision higher for the savings rate?? Every effort is being pursued to mislead the consumer to feel richer than they are.

-

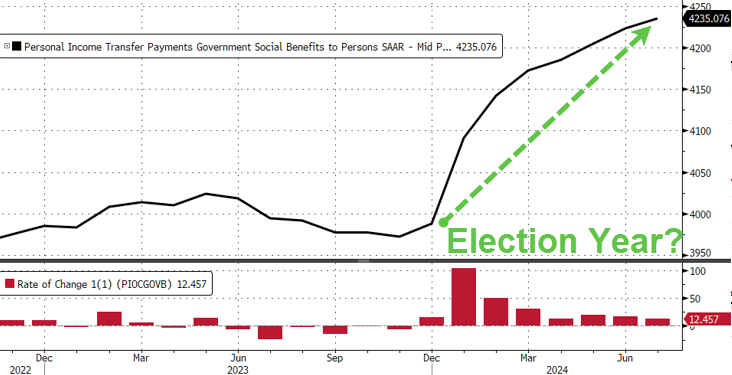

PERSONAL INCOME GOVERNMENT TRANSFER PAYMENTS: Imagine how bad things would be if the government wasn't sending billions to 'we, the people' all of a sudden. In other words, the consumer is now wiped out and yet key inflation measures refuse to drop materially. So yes, the Fed will continue to cut (election year after all) and then we can finally unleash the second coming of the Arthur Burns (1970s) hyperinflation Fed.

US Q2 GDP - FINAL ESTIMATE 3.0%

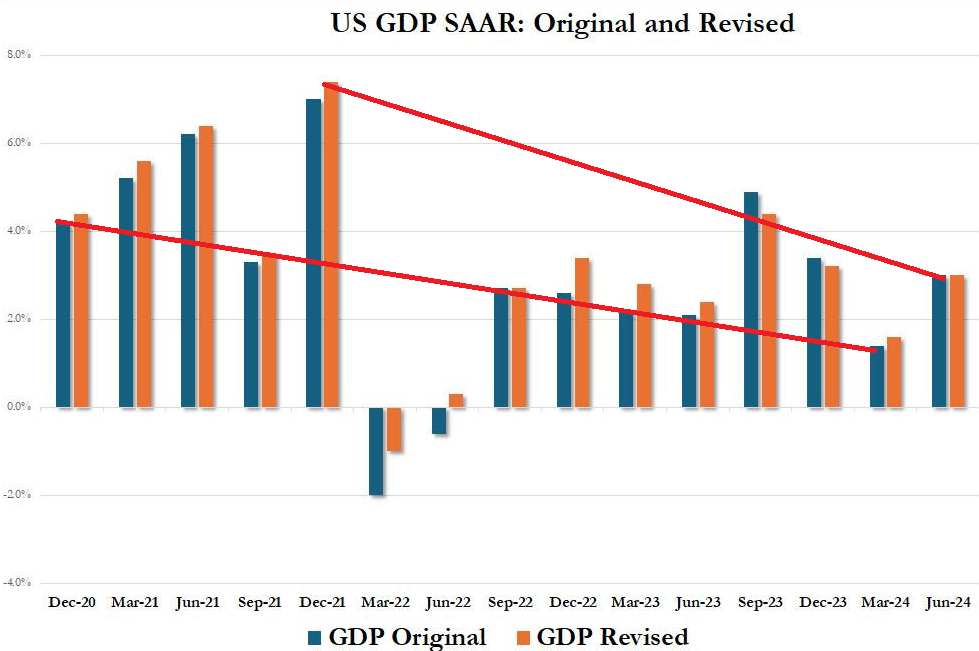

- What was amusing, is that the BEA decided to revise the Q2 2022 GDP print from negative (-0.6%) to positive (0.3%), effectively voiding the technical recession that took place in the first half of the year when GDP contracted for two consecutive quarters.

- GDP remains quite meaningless as an indicator. How could it be otherwise, when the Fed just started its most aggressive easing cycle after a quarter in which the US economy allegedly grew 3%?

| |

|

In this week's "Current Market Perspectives", we focus on the signals that Sentiment, Fundamentals and various market Segments (Credit, Bond and Equity) are currently giving us.

=========

| |

|

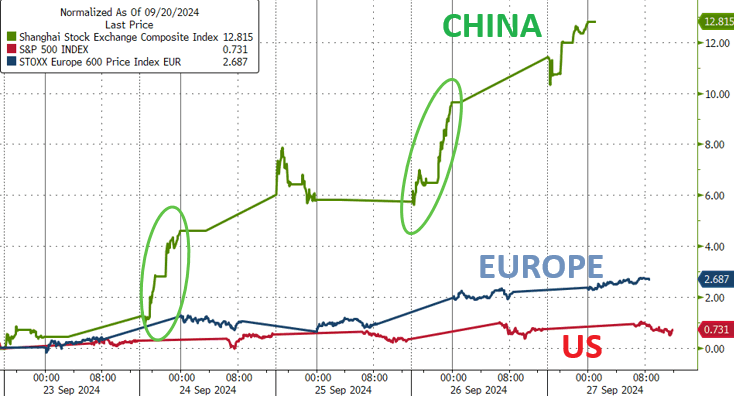

1- CHINA NEARS THE "WHATEVER IT TAKES" MOMENT!

Best week for China markets since 2008!

A CHINA SHOCKER: Chinese equities suddenly are the most overbought in "modern history". The China squeeze has been much more violent than the melt up we saw earlier this year. The index is up 17% since October 2019. ChiNext is the home to the most speculative stuff when it comes to Chinese equities trading. This index is having the biggest up day overnight, +8.2% as of writing. Time to likely Book any gains and take a well deserved weekend. RSI at 83. (Chart Right)

- RSI at 88.

- KWEB is up another few percent in pre market.

- The call spreads (and rolling into higher strikes dynamically) has been the index trade of the year.

- If you haven't, I hope you squared out those before the weekend.

CHART BELOW: HSTECH is up some 30% over the past week. This is no small cap - this is China's tech index.

|  | CHART BELOW: The most recent China squeeze has been much more violent than the melt up we saw earlier this year. The CSI300 index is up 17% since Oct 2019 | |

|

WHY DID THIS HAPPEN?

-

SIGNALLING TO COME: SOCIAL SUPPORT (Lift Home Purchase Curbs)

-

THURSDAY - From the POLITBURO: Significant Fiscal Policy Support

-

TUESDAY - From the PBOC: Important Monetary Policy support

The Chinese Politburo Thursday followed up the PBOC’s performance of Tuesday by announcing new fiscal stimulus measures aimed at supporting China’s ailing real estate sector. The Politburo offered few specifics beyond a commitment to halt the sharp slide in residential real estate prices, but reports suggest that policy measures will include approximately 2 trillion Yuan of new bond issuance this year to support consumption and alleviate debt burdens at the local government level. Cynics will say that the numbers announced are inadequate to the challenge (and they are probably right), but the material point is that the central government is now sending a clear signal that this is their “whatever it takes” moment.

| |

|

Despite the Politburo’s announced intention to place strict limits on new development the market latched onto the broad state support theme to bid up construction-adjacent commodities like iron ore, copper and steel futures. SGX iron closed up more than 2% and has rallied past through the $100/mt level.

WHAT THIS REALLY MEANS

China has just fired the stimulus bazooka 5 minutes after the Fed kicked off its easing cycle with a supersized rate cut. Suddenly we are watching a rally in commodity markets, (the Bloomberg Commodity Index has closed higher in 12 of the last 15 sessions), right at the moment that the Fed declared “Mission Accomplished” in the inflation fight and turned its attention instead to a softening labor market.

US LOOSENING INTO ALREADY EXTREMELY LOOSE FINANCIAL CONDITIONS (CHART RIGHT)

+ EXTREME LIQUIDITY (LAST NEWSLETTER DETAIL)

+ CHINA NOW REFLATING

==============================

= INFLATION RE-IGNITED!

WHAT A BAZOOKA LOOKS LIKE (IMHO)

- A policy shift to a balanced Mercantilism Strategy with a dramatically Increased Domestic Consumption Strategy

- A viable "Social Net" that includes retirement and health programs (to allow higher consumption spending versus excess savings)

NOW SIGNALLING - YET ANOTHER RIFLE SHOT - STILL NO BAZOOKA!

- Shanghai and Shenzhen to lift key remaining home purchases curbs to boost market; to remove curbs on non-local residents from buying homes; to scrap limits on number of homes Chinese can buy, via Reuters citing sources. Expected to announce the changes in the coming weeks. Capital Beijing considers limiting similar restrictions, expect in key districts.

- China's PBoC said the impact of the recently announced incremental interest rate policy on banks' net interest margins remains neutral overall.

- PBoC announced its 50bps RRR cut took effect from today and said the weighted average RRR for financial institutions was now at 6.6% after the new cut, while it set the 7-day reverse repo rate at 1.50% vs prev. 1.70%, as previously guided earlier this week, and injected CNY 278bln via 14-day reverse repos with the rate lowered to 1.65% from 1.85%.

THURSDAY ANNOUNCEMENT - A RIFLE SHOT BUT NO BAZOOKA!

- China is to issue USD 284bln of sovereign debt as part of fresh fiscal stimulus in which some of the fiscal support measures could be unveiled as early as this week, according to Reuters sources.

- Half of the stimulus package was said to be designed to stimulate consumption and the other half is to help local governments tackle local debt problems, while funds are to provide a monthly allowance of around CNY 800 per child to all households with two or more children, excluding the first child.

- China's securities regulator said public funds will have access to a wider variety of investible asset categories and it will continuously increase the scale and proportion of equity funds.

- PBoC vowed quick action and a special team to help boost the economy, while it also vowed to accelerate the adoption of financial boost policies, according to Bloomberg.

TUESDAY ANNOUNCEMENT - A PISTOL SHOT BUT NO BAZOOKA!

The PBOC, NDRC & CSRC announced a series of coordinated policy easing, including:

1. Cutting RRR by 0.5%

2. Cutting the 7D policy rate by 0.2%

3. Lowering the interest rate on outstanding mortgages

4. Easing down payment requirements for 2nd homes, and

5. Establishing a “stock stabilization fund” where the PBOC will provide Rmb500bn of liquidity to funds, brokers or insurers to buy stocks. (JPM market intelligence) Their conclusion on trading: "So enough to cause a short-squeeze, but in itself arguably not enough to convince LO money to add, unless there are more announcements to follow."

PBoC cut the RRR and 7-day reverse repo rate, whilst also announcing measures for the property sector and stock market.

- PBoC Governor Pan announced to cut RRR by 50bps which will provide CNY 1tln worth of long-term capital and cut the 7-day reverse repo rate by 20bps to 1.50%, while he said they will guide LPRs lower and reduce the mortgage rate for existing mortgages in which the average reduction in the interest rate of existing mortgages will be about 0.5 percentage points. PBoC also lowered down payments for second homes to 15% from 25% and will no longer distinguish between down payments for first and second homes which will be unified at 15%. Pan said they must support the steady recovery of prices in the economy and must coordinate monetary policy and fiscal policy, while he added the financial weighted reserve ratio for large banks will be reduced to 8% after the RRR cut and they might further cut RRR by year-end. Furthermore, he stated the MLF rate will be lowered by 0.3ppts and LPR will be lowered by 0.2-0.25ppts.

- China Securities Regulatory Commission Chairman said they will issue guidance for medium-term and long-term funds to enter the market and will issue measures to promote mergers, acquisitions and reorganisations. China will also release six new measures to support M&A soon and allow funds and brokers to tap PBoC funds to buy stock, while China reportedly plans at least CNY 500bln of liquidity to support stocks and is studying setting up a stock stabilisation plan.

- China NFRA head said China is to increase core tier-1 capital of the country's six largest commercial banks and will broaden the amount and proportion of equity investment restrictions, as well as establish a mechanism for coordinating financing of micro and small enterprises.

| |

2- WE ARE IGNORING PUTIN AT OUR PERIL - When Diplomacy Stops, Wars Happen!

The narrative from mainstream media is that Russia President Vladimir Putin is attempting to "blackmail" the US and NATO regarding the use of Nuclear Weapons. I don't buy into this White House summation of Putin's strategic shift. There is no diplomacy occurring which only leads to mis-calculated mistakes and worse. Like the Cuban Missile Crisis it is time for Leadership. The White House is playing with matches here and no one seems to be at the helm and in charge.

|  | |

At a moment the West - especially the US and UK - are still mulling whether to allow Ukraine forces to attack Russian territory using NATO-provided long-range missiles, President Vladimir Putin has just issued a hugely significant statement regarding his country's nuclear doctrine.

Putin on Wednesday very clearly lowered the threshold regarding Russian strategic forces' use of nukes. He in a televised address to Russia’s Security Council said nuclear doctrine has been effectively revised in light of the "emergence of new sources of military threats and risks for Russia and our allies." This is clearly in response to the latest series of escalated cross-border attacks from Ukraine deep into Russian territory. Some of these have threatened to hit Moscow.

He went on to describe that in the event Western powers assist another nation in a major attack on Russian soil, those same Western powers will also be held responsible. This can trigger Russian nuclear launch, according to the new doctrine. This lowers the bar for what can be considered an 'existential threat' against the Russian homeland and its population.

The timing of this dramatic and serious alteration in nuclear policy is without doubt aimed at Zelensky's visit to the United States, where he is presenting Ukraine's 'victory plan' separately to President Biden, VP Harris, as well as Donald Trump.

A NEW MILITARY NUCLEAR DOCTRINE

PUTIN: "WE RESERVE THE RIGHT TO USE NUCLEAR WEAPONS IN CASE OF AGGRESSION AGAINST RUSSIA AND BELARUS."

Russian President Vladimir Putin proposed significant updates to Russia’s nuclear strategy, citing the rapidly evolving global military-political situation. These changes reflect the Kremlin's concerns about increasing tensions and shifting alliances in international security.

Putin emphasized the need to adapt Russia’s nuclear strategy to current conditions, stating:

"The current military-political situation is changing dynamically in the world, and we must take this into account."

His comments signal a potential recalibration of Russia’s approach to nuclear deterrence.

A key component of the proposed updates includes redefining the conditions under which Russia might resort to using nuclear weapons. According to Putin:

"A number of clarifications have been proposed regarding the conditions under which nuclear weapons may be used."

This suggests that the Russian military may be considering a broader range of scenarios where nuclear options could be on the table.

Putin outlined a new provision that would expand the definition of aggression against Russia. He stated:

"Aggression against Russia by any non-nuclear state, with the participation or support of a nuclear state,

is proposed to be considered as a joint attack on the Russian Federation."

This shift implies that any non-nuclear nation involved in hostilities with Russia, backed by a nuclear-armed country, could trigger a nuclear response from Moscow.

Furthermore, Putin reiterated that Russia reserves the right to use nuclear weapons in defense of not only its own territory but also that of Belarus, a close ally.

"We reserve the right to use nuclear weapons in the event of aggression against Russia and Belarus,"

Putin declared, underscoring the deepening military ties between the two nations.

The proposed changes highlight Russia’s growing concern over the security threats posed by NATO and other Western-aligned countries, as well as potential regional conflicts that could involve nuclear powers.

| |

|

A STEADILY RISING CORPORATE PROFITS DANCE?

QUESTION: Why Are US Corporate Profits Rising So Quickly?

CHART TO THE RIGHT: The answer to the question is shown here. Debt/Credit Growth =~ GDP Growth =~ Nominal Profit Growth.

NARRATIVE BELOW: This is how Microsoft's AI Bot "Copilot" answered the question. Quite entertaining, but misses the mark!

Ah, the ever-elusive dance of corporate profits! Let’s unravel this financial tango, shall we?

**1. ** Economic Growth and Revisions:

-

First off, it’s important to note that the U.S. economy has been doing a little shimmy behind the scenes. According to revised data from the Commerce Department’s Bureau of Economic Analysis (BEA), the U.S. economy grew faster in 2023 than initially thought. Surprise upgrades to business investment and consumer spending played a part, even though the Federal Reserve was doing its interest rate cha-cha.

- Gross domestic product (GDP) for 2023 got a makeover—it strutted from an estimated 2.5% growth to a more impressive 2.9%. Not bad, right? And guess what? Residential investment (that’s fancy talk for home building) also got a makeover, contributing to the upward revision. So, houses were basically voguing their way into the stats.

**2. ** Corporate Profits: Cha-Ching!

-

Now, let’s talk about those corporate profits. Picture this: companies flexing their financial biceps. In 2023, corporate profits did a dramatic hair flip — they were sharply revised up by a whopping $288.5 billion, or 8.9%1. Why? Well, a few things:

-

Pricing Power: Companies suddenly had more swagger when it came to pricing. Rising inflation gave them a boost — like finding a hidden stash of glitter in their balance sheets.

-

Net Interest: Higher interest rates (thanks, Fed) also played a role. Imagine interest rates doing the samba and corporate profits following suit.

-

Proprietors’ Income: This category got a little love too. It’s like the side hustle of corporate income — think dividends, rents, and all that jazz.

-

Wages and Salaries: Okay, here’s the twist — wages and salaries didn’t party as hard. They got a downgrade. Maybe they were too busy practicing their moonwalk.

**3. ** Inflation and the Affordability Tango:

- But wait, there’s more! Inflation waltzed into the scene. As corporations lamented supply chain woes and higher labor costs, their profits skyrocketed. And guess what? This fueled inflation. It’s like a high-stakes game of Monopoly where everyone’s buying hotels on Boardwalk.

-

Oh, and here’s a plot twist: Americans were feeling flush (thanks to pandemic stimulus payments), so they could handle the higher prices. No wonder companies didn’t feel the need to lower them. It’s like saying, “Sure, I’ll pay extra for that avocado toast. I’ve got stimulus vibes.”

**4. ** The Global Groove:

So, my friend, corporate profits are doing the hustle, inflation’s doing the twist, and the economy’s throwing a surprise party. Keep an eye on those balance sheets — they might just break into a full-on conga line next!

| |

|

DEVELOPMENTS TO WATCH

REDFIELD LABELS IT AS "AGENCY CAPTURE"

(Further support of this month's UnderTheLens Video)

NEWSWEEK ARTICLE LINK

Former CDC Director Robert Redfield wrote an editorial in Newsweek praising President Trump's decision to join forces with Robert Kennedy Jr. to "make America healthy again."

Redfield wrote in the op-ed published on Tuesday:

"We know chronic disease is more than 75 percent of the country's $4 trillion annual health care expenditure. Unfortunately, we have become a sick nation. We're paying too much for chronic disease, and this must change. It's time to make America healthy again,"

After more than four decades in public health, Redfield believes the former president "chose the right man [RFK Jr.] for the job" to combat the processed foods industrial complex, which has ignited an obesity crisis across the Heartland.

"For instance, obesity in American children has increased dramatically since John F. Kennedy's presidency, from around 4 percent in the 1960s to almost 20 percent in 2024.The causes of childhood obesity are complex, but a primary origin is clearly the modern American diet of highly processed foods."

He explained the causes for this obesity crisis are primarily due to

"Special interest and corporate influences on our federal agencies."

Redfield pointed out that "Kennedy is right" about the corporate capture problem of federal agencies.

Kennedy is right: All three of the principal health agencies suffer from agency capture. A large portion of the FDA's budget is provided by pharmaceutical companies. NIH is cozy with biomedical and pharmaceutical companies and its scientists are allowed to collect royalties on drugs NIH licenses to pharma. And as the former director of the Centers for Disease Control and Prevention (CDC), I know the agency can be influenced by special interest groups.

Redfield acknowledges that agency capture is a serious issue, highlighting that federal agencies responsible for regulating food and medicine are possibly compromised by the food industrial complex and big pharma.

Maybe it was a warning sign when big pharma and the feds pushed Ozempic as the 'wonder shot' to end the obesity crisis instead of promoting 1) Exercise and 2) Safe & Clean Food.

| |

|

FOOD IS THE ULTIMATE WEAPON OF CONTROL

We face a near-term future in which the control mechanisms will be all-pervasive.

- Elites have known for millennia, it is food that is the ultimate weapon of control.

- As former US Secretary of State articulated in 1973: ‘Who controls the food supply controls the people’.

-

Professor George Kent eloquently explained in 2008 - it is in the interest of the Elite that people are hungry. See ‘The Benefits of World Hunger’.

So any critical analysis of what is being imposed on humanity must take careful account of how food – and the farming of it – is being utterly transformed.

In essence, the Elite plan is:

- To feed us genetically mutilated, synthesized and poisoned trash and insects

- Profit from our ill-health

- Force small farmers off their land

- Undermine rural communities and

- Utterly transform the ancient practice of farming into a corporate, technocratic operation.

If you want some of the details, there are excellent sources that highlight the importance of buying organic/biodynamic food while organizing to grow your own and making sure that your local trading community can defend your food sources against the advancing technocracy.

| |

A DESTABILIZING FOOD SHOCK - PREVIEW VIDEO | |

|

GLOBAL ECONOMIC INDICATORS:

What This Week's Key Global Economic Releases Tell Us

| |

|

PERSONAL CONSUMPTION EXPENDITURE (PCE)

The Fed's favorite inflation indicator, the Core PCE, rose less than expected on a MoM basis (+0.1% vs +0.2% exp), but on a YoY basis, Core PCE rose from 2.6% to 2.7% (in line with exp) - the highest since April.

- The headline PCE fell to +2.2% YoY - the lowest since March 2021...

- The o-called SuperCore PCE re-accelerated in August to +3.29% Y-o-Y.

- Both income and spending rose less than expected in August (income smallest MoM rise since July 2023 and spending equal lowest since Jan 2024)...

- On a Y-o-Y basis, both spending and income growth slowed...

- Thanks to massive revisions, the savings rate comps are a mess. We note that at 4.8% of disposable income, it is at its lowest since Dec 2023. For comparison, the savings rate (pre-revision) in July was 2.9%.

- Personal income was revised dramatically higher.

- Spending was also revised higher, (but less so).

- A 2 percentage point revision higher for the savings rate. Every effort is being made to make the consumer appear richer than they are. (Chart Above Right)

CHART BELOW:

PERSONAL INCOME GOVERNMENT TRANSFER PAYMENTS: Imagine how bad things would be if the government wasn't sending billions to 'we, the people' all of a sudden. In other words, the consumer is now wiped out and yet key inflation measures refuse to drop materially. So yes, the Fed will continue to cut (election year after all) and then we can finally unleash the second coming of the Arthur Burns (1970s) hyperinflation Fed.

|  | |

|

US Q2 GDP - FINAL ESTIMATE 3.0%

In summary, the print was a "nothingburger".

What was more important was the data revisions to historical prints, starting in Q1 2019 and going through Q4 2023 and which, according to Goldman, would wipe out as much as 0.4% to GDP. So what did the data show?

Well, as shown in the pre/post revisions (chart to the right), there was certainly notable revisions to GDP prints, especially in the second half of 2023, where Q3 GDP was cut from 4.9% to 4.4%, and Q4 was trimmed from 3.4% to 3.2%. Yet previous quarters were unexpectedly revised higher, starting with Q4 2022 and through Q2 2023. Also notable is that much of 2020 and 2021 were revised higher as the BEA now sees a stronger rebound from the covid shock.

OFFICIAL MAINSTREAM ANNOUNCEMENT DETAILS

Q2 US GDP (FINAL EST.): The final GDP estimate for Q2 was unrevised at 3.0%, in line with expectations, and accelerating from the 1.6% growth seen in Q1.

- The BEA highlights that, in the final estimate, upward revisions to private inventory investment and federal government spending were offset by downward revisions to nonresidential fixed investment, exports, consumer spending, and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, also increased.

- The GDP sales number was revised down to 1.9% from 2.2%, while consumer spending was revised down to 2.8% from 2.9%.

- The deflator was unrevised as expected at 2.5%.

- On prices, Core PCE was unrevised at 2.89%, with the headline unrevised at 2.5%.

- The supercore metrics, saw PCE Ex food, energy and housing unrevised at 2.3%, while PCE services ex-energy and gooding was revised to 3.0% from 3.1%.

- The report is a welcome one but is deemed stale, given it covers Apr-June, but nonetheless shows the progress made on inflation whilst maintaining a robust economy in Q2.

- Note, the Atlanta Fed Q3 GDP tracker currently is tracking growth at 2.9%, suggesting economic momentum has continued into Q3.

- Analysts at Oxford Economics note that "The revisions only strengthen our conviction that the US economy will continue to expand at a decent pace over the coming year, which suggests labor market conditions are unlikely to deteriorate markedly from here. We think that will push Fed officials toward a more gradual series of interest rate cuts in the quarters ahead.

| |

|

CORPORATE PROFITS

Corporate profits in the United States rose by 3.5% from the previous period to $ 3.142 trillion in the second quarter of 2024, above preliminary estimates of a 1.7% increase and recovering from a downwardly revised 2.1% drop in Q1.

Undistributed profits soared by 10%, (vs -8.8% in Q1), and net cash flow with inventory valuation adjustment rose by 4.8% (vs -2.8%).

Net dividends showed no growth, after a 1.8% increase in the previous period. Compared to the corresponding period of the previous year, corporate profits rose by 10.8%.

| |

|

GLOBAL

WHAT DOES YOUR SCAN OF THE DATA BELOW TELL YOU? - THE MEDIA AVOIDS BAD NEWS!

We present the data in a way you can quickly see what is happening.

THIS WEEK WE SAW

Exp. =Expectations, Prev. =Previous

| |

|

UNITED STATES

- US S&P Global Manufacturing PMI Flash (Sep) 47.0 (Prev. 47.9)

- US S&P Global Services PMI Flash (Sep) 55.4 (Prev. 55.7)

- US S&P Global Composite Flash PMI (Sep) 54.4 (Prev. 54.6)

- US Consumer Confidence (Sep) 98.7 vs. Exp. 104.0 (Prev. 103.3, Rev. 105.6)

- US Richmond Fed Composite Index (Sep) -21.0 (Prev. -19.0)

- US Richmond Fed Mfg Shipments (Sep) -18.0 (Prev. -15.0)

- US Richmond Fed Services Index (Sep) -1.0 (Prev. -11.0)

- US Monthly Home Price MM (Jul) 0.1% (Prev. -0.1%)

- US Monthly Home Price YY (Jul) 4.5% (Prev. 5.1%, Rev. 5.3%)

- US CaseShiller 20 MM SA (Jul) 0.3% vs. Exp. 0.4% (Prev. 0.4%, Rev. 0.47%)

- US CaseShiller 20 YY NSA (Jul) 5.9% vs. Exp. 5.9% (Prev. 6.5%, Rev. 6.5%)

- US New Home Sales-Units (Aug) 0.716M vs. Exp. 0.7M (Prev. 0.739M)

- US New Home Sales Change MM (Aug) -4.7% (Prev. 10.6%)

- US Building Permits R Number (Aug) 1.47M (Prev. 1.475M)

- US Building Permits R Change MM (Aug) 4.6% (Prev. 4.9%)

- US GDP Final (Q2) 3.0% vs. Exp. 3.0% (Prev. 3.0%)

- US Core PCE Prices Final (Q2) 2.8% vs. Exp. 2.8% (Prev. 2.8%)

- US Durable Goods (Aug) 0.0% vs. Exp. -2.6% (Prev. 9.8%)

- US Durables Ex-Transport (Aug) 0.5% vs. Exp. 0.1% (Prev. -0.2%, Rev. -0.1%)

- US Pending Sales Change MM (Aug) 0.6% vs. Exp. 1.0% (Prev. -5.5%)

- US Initial Jobless Claims w/e 218.0k vs. Exp. 225.0k (Prev. 219.0k, Rev. 222k)

- US Continued Jobless Claims w/e 1.834M vs. Exp. 1.838M (Prev. 1.829M, Rev. 1.821M)

- US KC Fed Manufacturing (Sep) -18.0 (Prev. 6.0)

- US KC Fed Composite Index (Sep) -8.0 (Prev. -3.0)

CHINA

- Chinese Industrial Profit YTD YY (Aug) 0.5% (Prev. 3.6%)

- Chinese Industrial Profits YY (Aug) -17.8% Y/Y (prev. 4.1%)

JAPAN

- Japanese Services PPI (Aug) 2.70% vs. Exp. 2.60% (Prev. 2.80%)

- Tokyo CPI YY (Sep) 2.2% vs. Exp. 2.2% (Prev. 2.6%)

- Tokyo CPI Ex. Fresh Food YY (Sep) 2.0% vs. Exp. 2.0% (Prev. 2.4%)

- Tokyo CPI Ex. Fresh Food & Energy YY (Sep) 1.6% vs. Exp. 1.6% (Prev. 1.6%)

AUSTRALIA

- Australian Judo Bank Manufacturing PMI Flash (Sep) 46.7 (Prev. 48.5)

- Australian Judo Bank Services PMI Flash (Sep) 50.6 (Prev. 52.5)

- Australian Judo Bank Composite PMI Flash (Sep) 49.8 (Prev. 51.7)

- Australian Weighted CPI YY (Aug) 2.7% vs. Exp. 2.7% (Prev. 3.5%)

- Australian Trimmed Mean CPI YY (Aug) 3.40% (Prev. 3.80%)

NEW ZEALAND

- New Zealand Trade Balance (Aug) -2203.0M (Prev. -963.0M, Rev. -1016M)

- New Zealand Annual Trade Balance (Aug) -9.29B (Prev. -9.29B, Rev. -9.35B)

- New Zealand Exports (Aug) 4.97B (Prev. 6.15B, Rev. 6.09B)

- New Zealand Imports (Aug) 7.17B (Prev. 7.11B, Rev. 7.10B)

SWEDEN

- Swedish Overall Sentiment (Sep) 94.9 (Prev. 94.7); Manufacturing Confidence (Sep) 94.2 (Prev. 97.1); Total Industry Sentiment (Sep) 96.5 (Prev. 95.0); Consumer Confidence SA (Sep) 99.5 (Prev. 96.3)

| |  |

|

EU

- EU HCOB Manufacturing Flash PMI (Sep) 44.8 vs. Exp. 45.5 (Prev. 45.8)

- EU HCOB Services Flash PMI (Sep) 50.5 vs. Exp. 52.3 (Prev. 52.9)

- EU HCOB Composite Flash PMI (Sep) 48.9 vs. Exp. 50.5 (Prev. 51.0)

- EU Money-M3 Annual Grwth (Aug) 2.9% vs. Exp. 2.6% (Prev. 2.3%); Loans to Non-Fin (Aug) 0.8% (Prev. 0.6%); Loans to Households (Aug) 0.6% (Prev. 0.5%)

- EU Industrial Sentiment (Sep) -10.9 vs. Exp. -9.9 (Prev. -9.7, Rev. -9.9); Services Sentiment (Sep) 6.7 vs. Exp. 5.9 (Prev. 6.3, Rev. 6.4); Economic Sentiment (Sep) 96.2 vs. Exp. 96.5 (Prev. 96.6, Rev. 96.5); Selling Price Expec (Sep) 6.2 (Prev. 6.1, Rev. 6.2); Cons Infl Expec (Sep) 10.9 (Prev. 11.3)

GERMANY

- German HCOB Manufacturing Flash PMI (Sep) 40.3 vs. Exp. 42.3 (Prev. 42.4)

- German HCOB Services Flash PMI (Sep) 50.6 vs. Exp. 51.0 (Prev. 51.2)

- German HCOB Composite Flash PMI (Sep) 47.2 vs. Exp. 48.2 (Prev. 48.4)

- German Ifo Expectations New (Sep) 86.3 vs. Exp. 86.3 (Prev. 86.8)

- German Ifo Business Climate New (Sep) 85.4 vs. Exp. 86.0 (Prev. 86.6)

- German Ifo Current Conditions New (Sep) 84.4 vs. Exp. 86.1 (Prev. 86.5, Rev. 86.4)

- German Unemployment Rate SA (Sep) 6.0% vs. Exp. 6.0% (Prev. 6.0%); Unemployment Chg SA (Sep) 17.0k vs. Exp. 12.0k (Prev. 2.0k); Unemployment Total SA (Sep) 2.823M (Prev. 2.801M); Unemployment Total NSA (Sep) 2.806M (Prev. 2.872M).

FRANCE

- French HCOB Manufacturing Flash PMI (Sep) 44.0 vs. Exp. 44.3 (Prev. 43.9)

- French HCOB Services Flash PMI (Sep) 48.3 vs. Exp. 52.5 (Prev. 55)

- French HCOB Composite Flash PMI (Sep) 47.4 vs. Exp. 50.6 (Prev. 53.1)

- French Consumer Confidence (Sep) 95.0 vs. Exp. 92.0 (Prev. 92.0, Rev. 93)

- French CPI Prelim MM NSA (Sep) -1.2% vs. Exp. -0.70% (Prev. 0.50%); CPI Prelim YY NSA (Sep) 1.2% vs. Exp. 1.60% (Prev. 1.80%); Producer Prices YY (Aug) -6.3% (Prev. -5.40%) Consumer Spending MM (Aug) 0.2% vs. Exp. -0.10% (Prev. 0.30%) CPI (EU Norm) Prelim YY (Sep) 1.5% vs. Exp. 2.0% (Prev. 2.2%) Consumer Spending MM (Aug) 0.2% vs. Exp. -0.1% (Prev. 0.3%, Rev. 0.2%) Producer Prices MM (Aug) 0.2% (Prev. 0.2%, Rev. 0.3%).

SPAIN

- Spanish Retail Sales YY (Aug) 2.3% (Prev. 1.0%, Rev. 1.1%)

- Spanish HICP Flash MM (Sep) -0.10% vs. Exp. 0.00% (Prev. 0.00%); CPI MM Flash NSA (Sep) -0.60% vs. Exp. -0.10% (Prev. 0.00%); CPI YY Flash NSA (Sep) 1.50% vs. Exp. 1.90% (Prev. 2.30%); core 2.40% vs. Exp. 2.80% (Prev. 2.70%); HICP Flash YY (Sep) 1.7% vs. Exp. 1.9% (Prev. 2.4%); Spanish GDP Final QQ (Q2) 0.8% vs. Exp. 0.8% (Prev. 0.8%); GDP YY (Q2) 3.1% vs. Exp. 2.9% (Prev. 2.9%); GDP Final QQ (Q2) 0.8% vs. Exp. 0.8% (Prev. 0.8%).

ITALY

- Italian Consumer Confidence (Sep) 98.3 vs. Exp. 97.0 (Prev. 96.1); Mfg Business Confidence (Sep) 86.7 vs. Exp. 87.1 (Prev. 87.1, Rev. 87.0)

- Italian Industrial Sales YY WDA (Jul) -4.7% (Prev. -3.7%); Industrial Sales MM SA (Jul) -0.4% (Prev. 0.1%)

UK

- UK Flash Manufacturing PMI (Sep) 51.5 vs. Exp. 52.5 (Prev. 52.5)

- UK Flash Services PMI (Sep) 52.8 vs. Exp. 53.5 (Prev. 53.7)

- UK Flash Composite PMI (Sep) 52.9 vs. Exp. 53.5 (Prev. 53.8)

- UK car manufacturing output fell 8.4% Y/Y to 41,271 units in August, according to SMMT.

SWEDEN

- Swedish Overall Sentiment (Sep) 94.9 (Prev. 94.7); Manufacturing Confidence (Sep) 94.2 (Prev. 97.1); Total Industry Sentiment (Sep) 96.5 (Prev. 95.0); Consumer Confidence SA (Sep) 99.5 (Prev. 96.3)

| |

CURRENT MARKET PERSPECTIVE | |

|

CHINA, GOLD & CRYPTO SURGE

MARKETS WAITING ON CLEARER DIRECTION

Click All Charts to Enlarge

| S&P 500 CUP AND HANDLE: Recent upside breakouts in S&P 500 cumulative net up volume (lower panel) ,along with a MODIFIED Cup & Handle formation (upper panel), suggest that the S&P 500 may be nearing a near term corrective / consolidation. Note: The vertical black bars measure a completed C&H pattern. | |

|

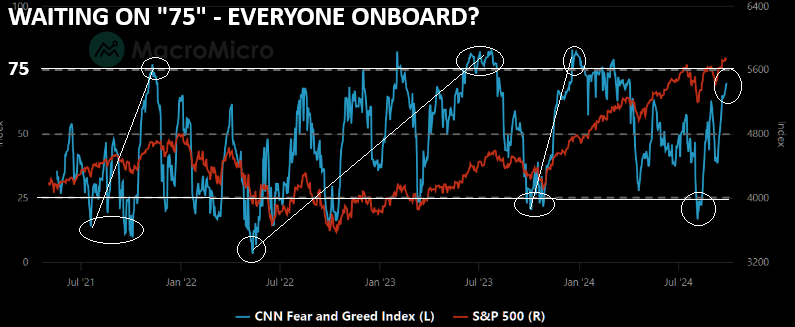

SENTIMENT - A CORRECTIVE / CONSOLIDATION BEFORE THE YEAR-END RUN-UP

MARKETS WAITING ON "75", EVERYONE ONBOARD CLOSING BUYBACK WINDOW

1- WAITING ON "75" - PUBLIC ON BOARD YET?

SPX vs CNN's Greed/Fear Index (Charts Right):

We have not seen this much greed in a while. Traders are waiting for extreme greed territory (FLIPS AT 75), before they start looking at shorts. Currently they are building protection (SKEWS).

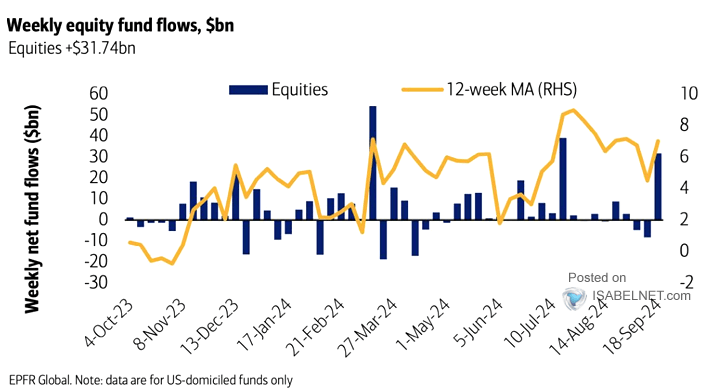

2- PUBLIC CLAMORING TO GET ONBOARD

U.S. equity funds have seen substantial inflows amounting to $31.74 billion, reflecting a strong positive sentiment among investors, particularly following the Fed’s decision to cut interest rates last week.

However, in the US, Hedge Funds remained net sellers (-1.3z in past 5 days), as selling/de-grossing prior to the Fed was not reversed on Wed/Thurs. HF turnover also remained pretty low for most days recently and quite low relative to VIX levels.

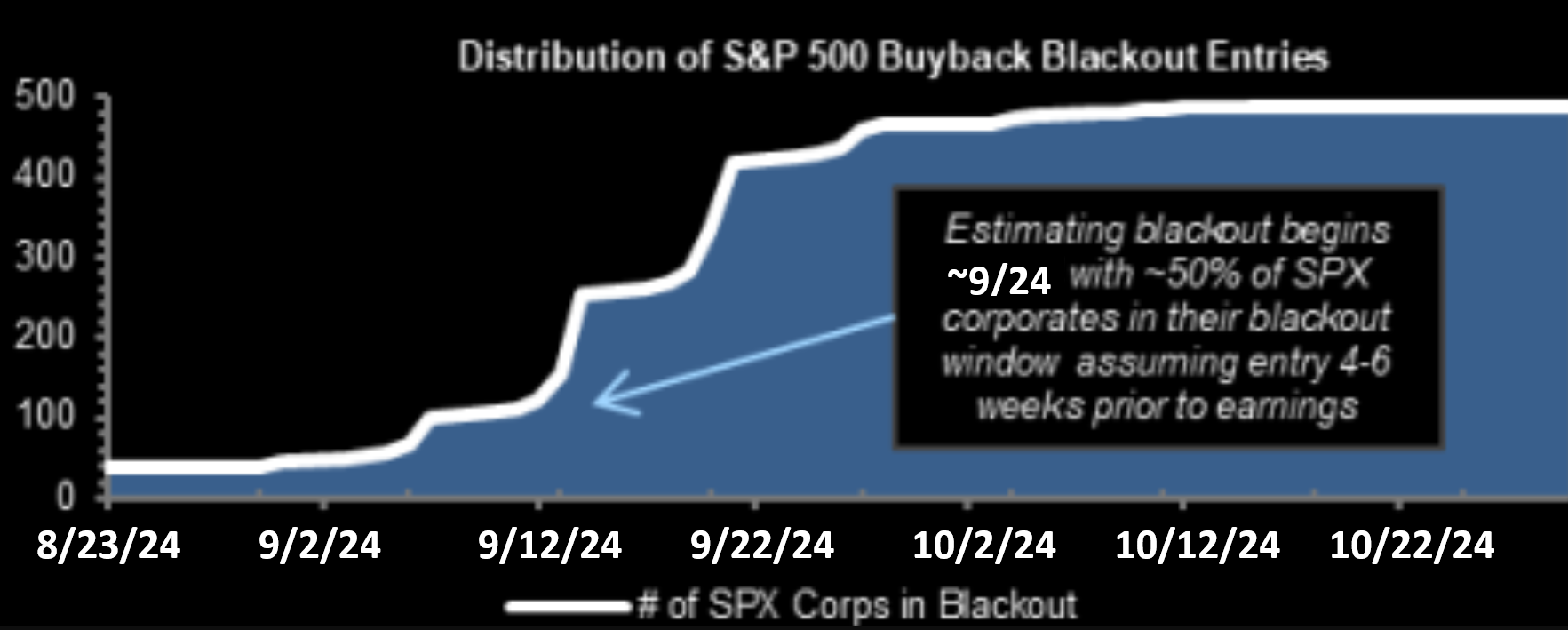

3- CLOSING BUYBACK WINDOW

On ~9/24 approximately 50% of corporations had already entered their Stock BuyBack Q3 Earnings Window.

NOTE:

- Dealers continue to choke on massive long gamma (paying fat theta checks).

- This is changing soon. McElligott on gamma going forward "....set to MASSIVELY “unclench” us after the expiration / re-strike on September 30th".

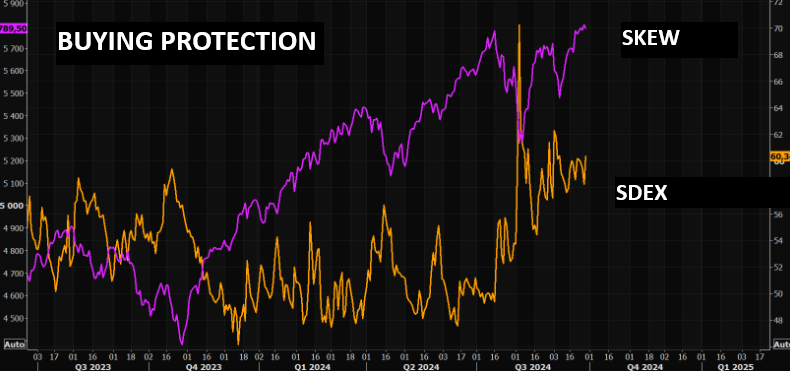

4- PROFESSIONALS FOCUSED ON PROTECTION (SKEWS)

The bid for downside protection continues to be very strong. We saw the SDEX index move higher Friday again, despite equities trading relatively boring.

The crowd is long and in need of downside protection.

NOTE:

- It was not your normal Friday VIX. VIX rounded off the week rather stressed. 2 day 5 min chart showing "dislocation" clearly. Need to watch the VVIX closely here, especially when it moves like it did on a Friday!

- Buy protection when you can, not when you must. The crowd absolutely hates puts again. You know what that means.

- Index downside protection relatively attractively priced, at least looking at put spreads, (due to low volatility and still elevated skew). Traders look for this as an opportunity.

| |

1- WAITING ON "75" - PUBLIC ON BOARD YET? | 2- PUBLIC CLAMORING TO GET ONBOARD | PROFESSIONALS FOCUSED ON PROTECTION (SKEWS) | |

|

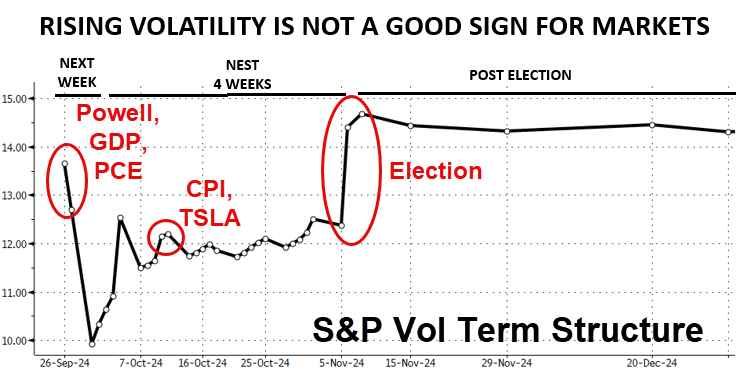

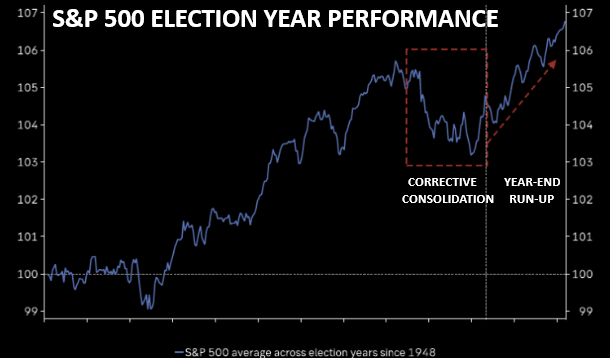

THE ELECTION YEAR CYCLE

CHART RIGHT: The historical election performance suggests our expected near term corrective / consolidation is likely with a follow on Year End stock run-up.

RISING VOLATILITY

| |

|

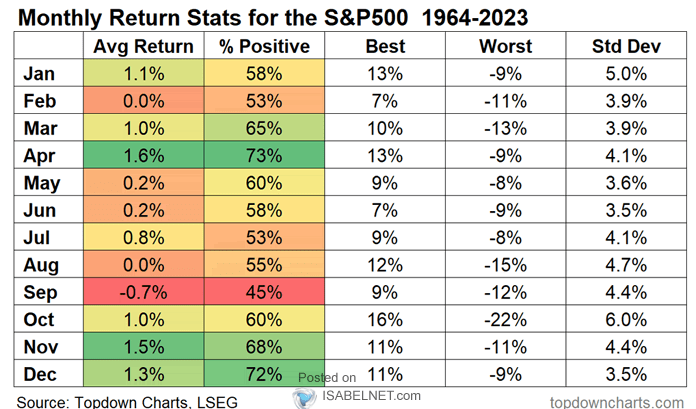

TABLE BELOW: The last two weeks of September are historically the weakest of the year. | |

|

Stocks have NEVER been more expensive relative to the economy.

Total US market cap back up to 200% of GDP.

"43% of S&P 500 market cap now under FTC/DoJ antitrust investigation".

| |

|

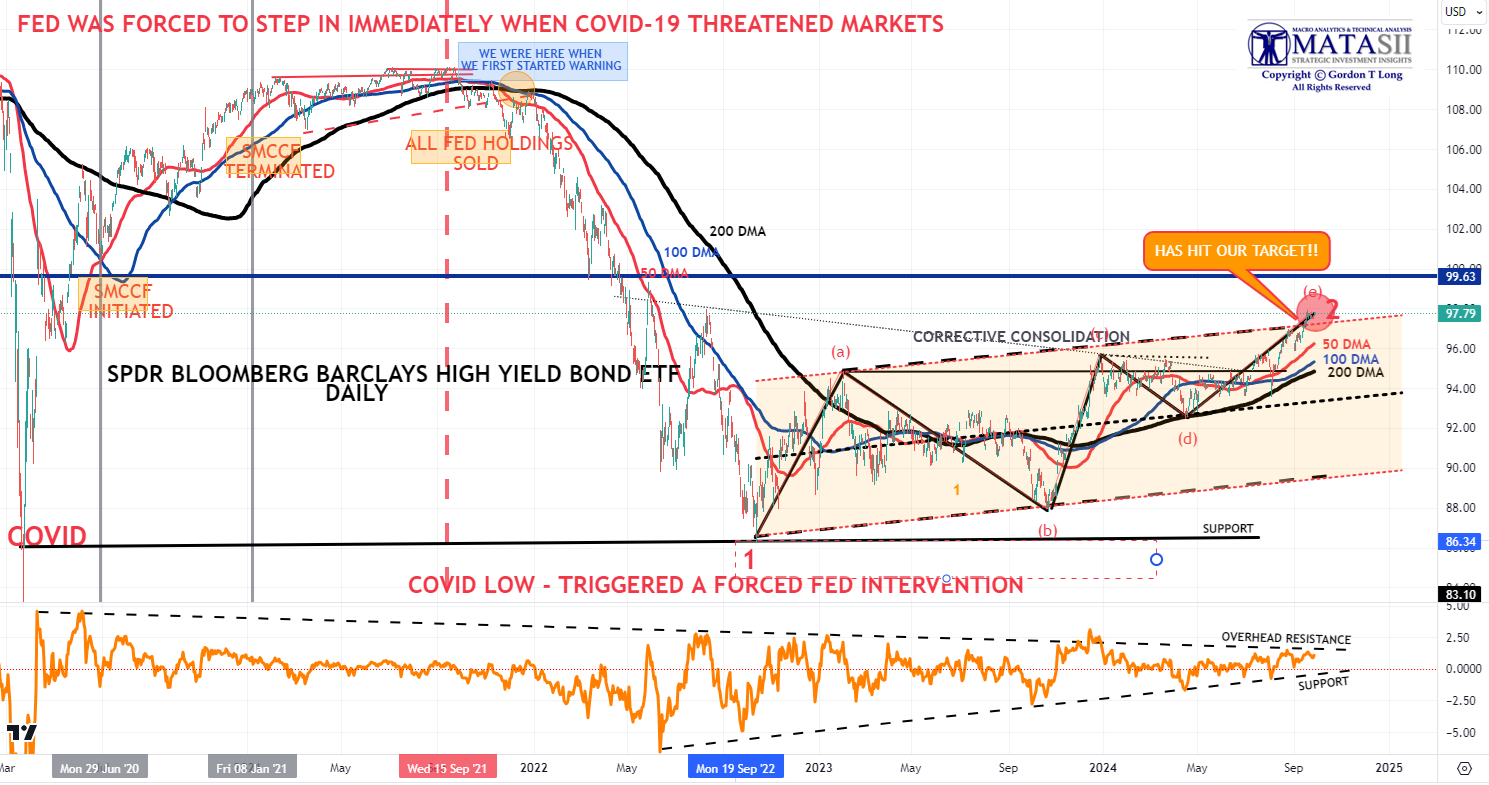

CREDIT ALWAYS LEADS! - We Have Our Target Met

HY Credit, as represented by the Bloombergs High Yield Bond ETF (JNK), has reached our target. All indications are that the corrective consolidation wave since Covid (and the buying at the time of Corporate Bonds by the Fed) has now ended.

With the Fed initiating the process of lowering the Fed Funds Rate, we should expect HY spreads to begin widening to reflect the reason the Fed is lowering rates - a concern for slowing economic growth, potential increasing unemployment levels and the longer term impact of elevated rates hitting!, All this leads credence to a Recession being ahead of whatever degree (soft or hard?).

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

2 - TECHNICAL ANALYSIS.

WE ARE VERY CLOSE TO A POTENTIAL CORRECTIVE / CONSOLIDATION

BEFORE A YEAR-END STOCK RUN-UP

| |

|

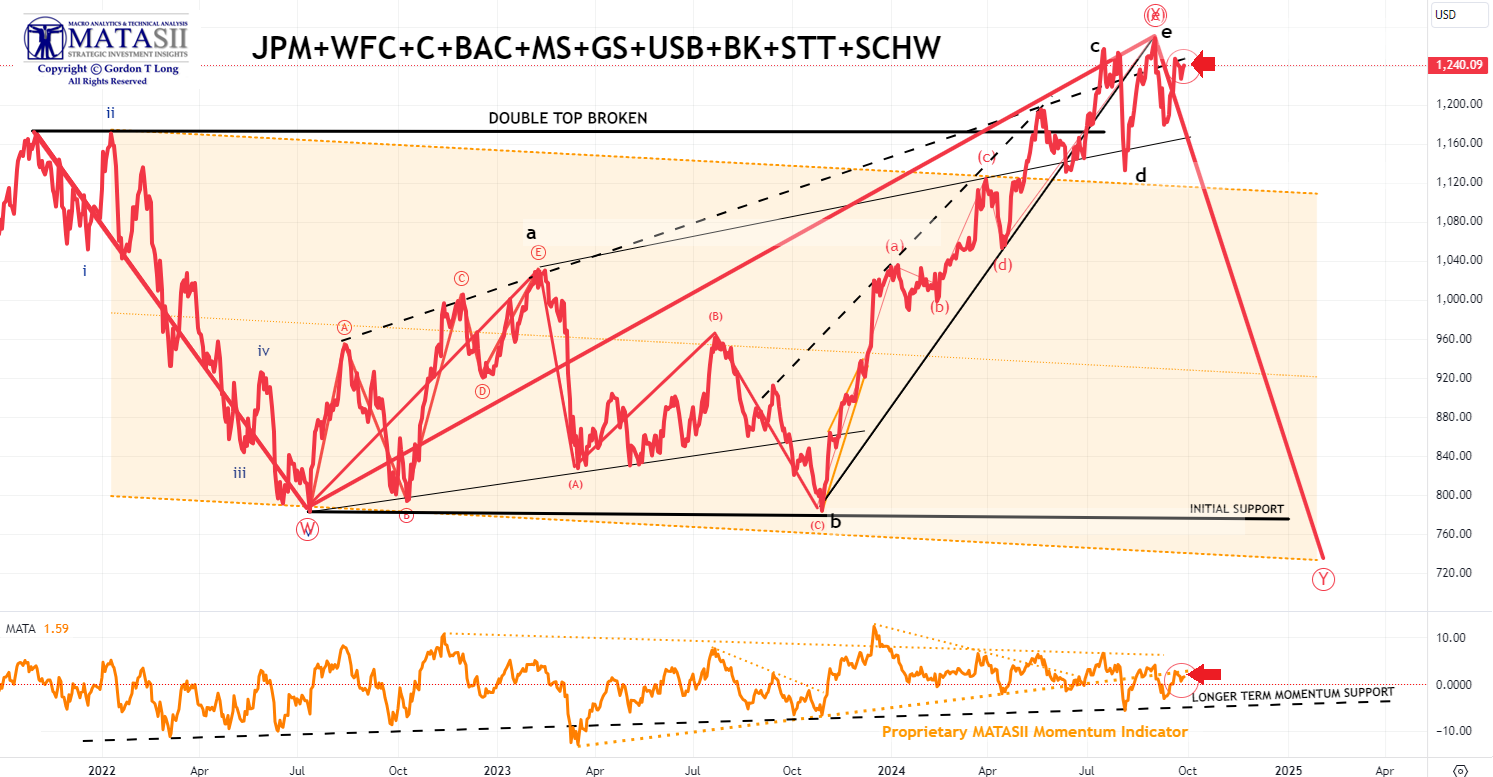

THE MATASII FINANCIAL INDEX

- The MATASII Financial Index appears to have possibly put in an important top with the FOMC 50 bps cut announcement.

- The MATASII Proprietary Momentum Indicator, after reaching an initial overhead resistance trend line, has shown weakness.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

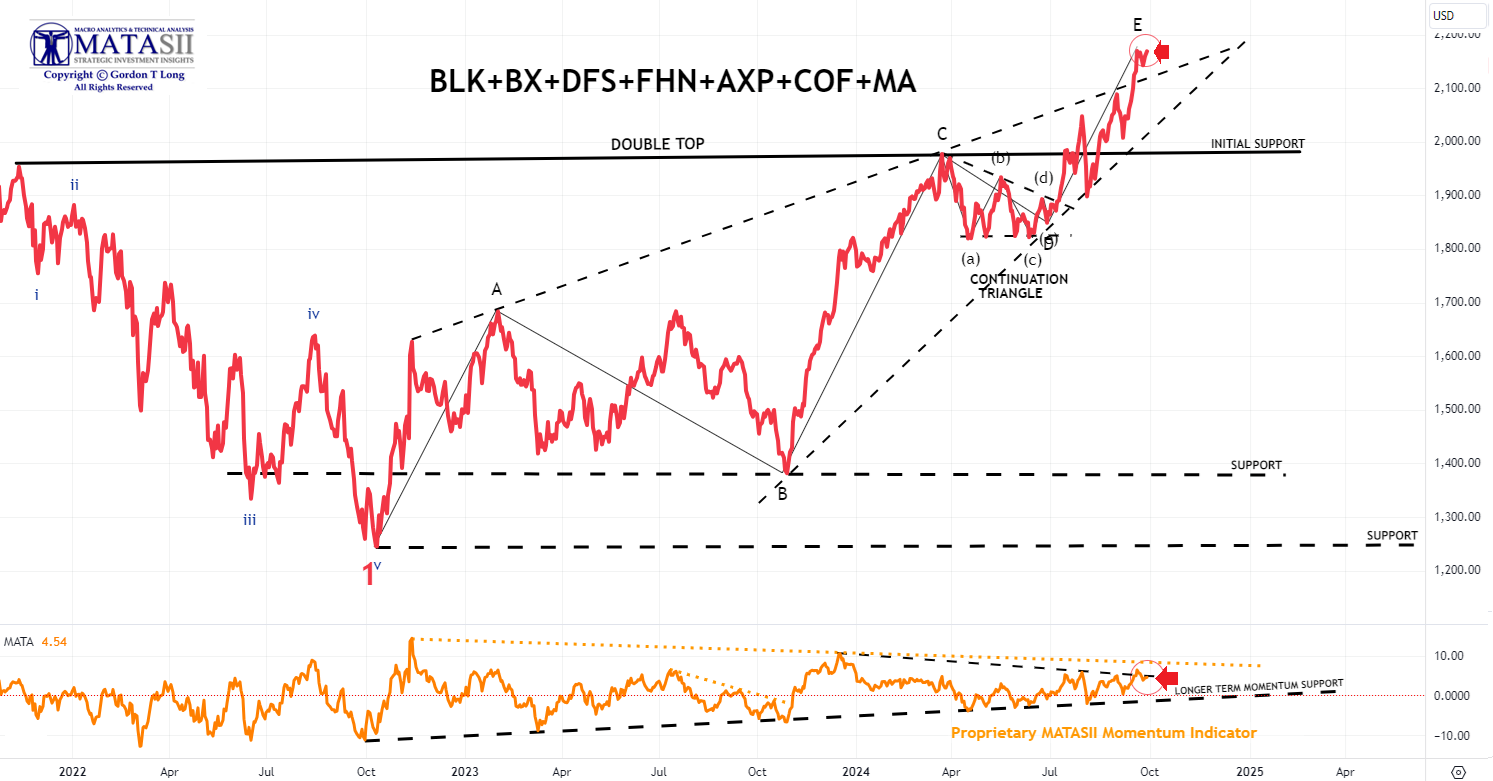

THE MATASII BANK INDEX

- The MATASII Bank Index appears to be completing a possible Dome Top or Head & Shoulders pattern.

- The MATASII Proprietary Momentum Indicator, after reaching an initial overhead resistance trend line, has shown weakness.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

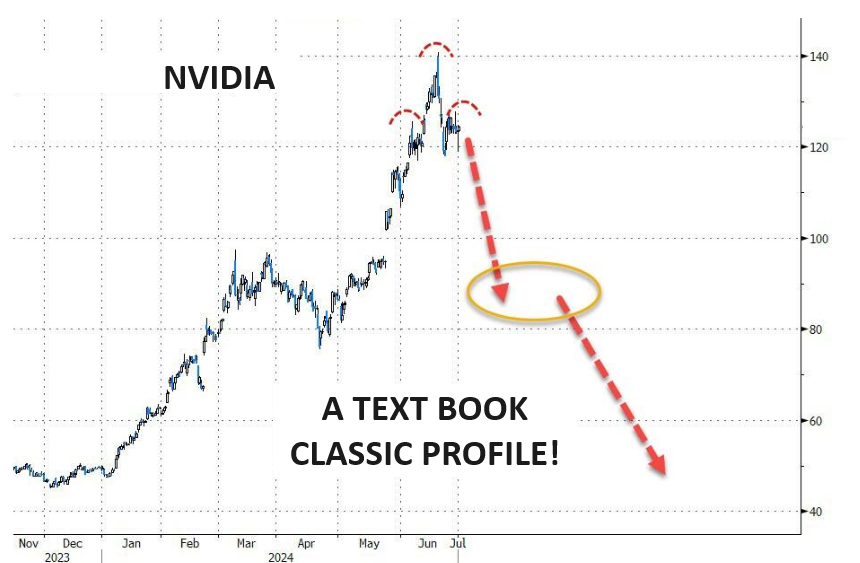

CHART RIGHT: NVDA v the dominant darling CSCO of the Dotcom Bubble (for those who recall). | | |

| |

|

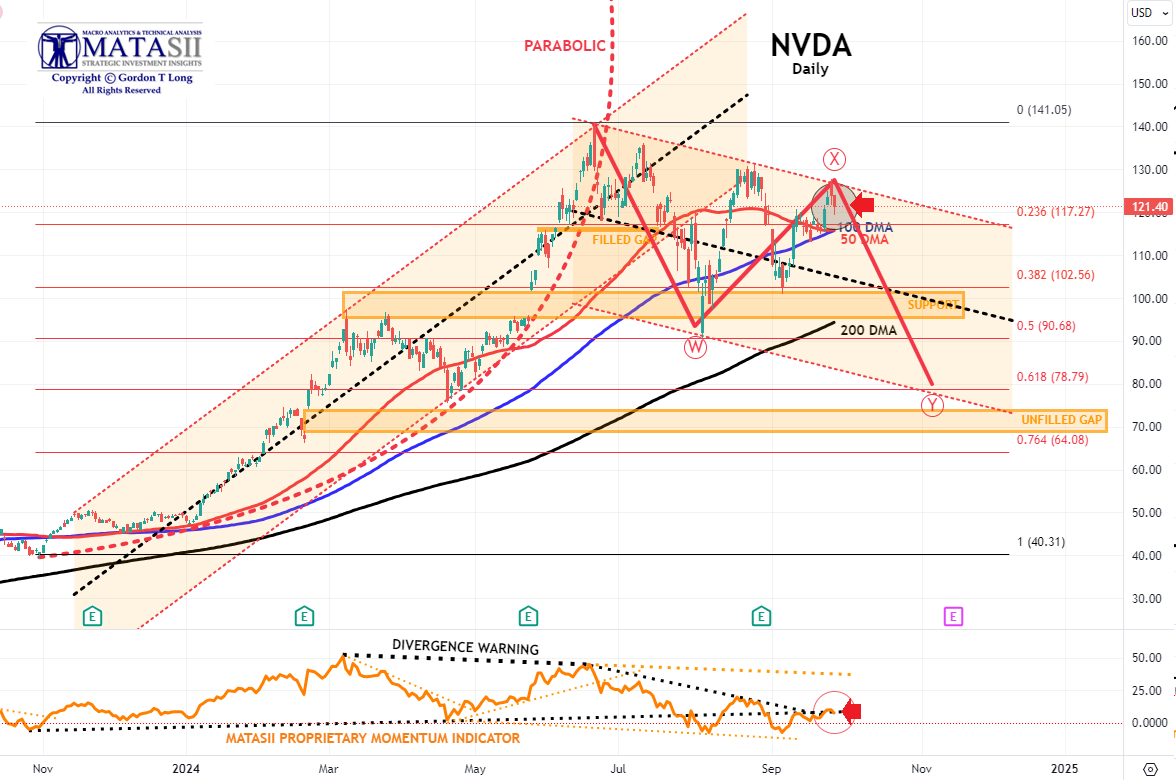

CHART RIGHT: NVDA has entered bear territory (-23% from intraday high on June 20th, 2024). Ominously, Nvidia's market cap recently fell $279 billion IN ONE DAY, the largest single-day decline for any company in history. That's bigger than the market cap of 474 companies in the S&P 500.

- NVDA surged higher this week reaching its upper trend channel before pulling back.

- Meanwhile the MATASII Proprietary Momentum Indicator (lower pane) has again rebounded back to two major overhead resistance levels (dotted black lines).

- The MATASII Proprietary Momentum Indicator (lower pane below) has been signaling that this sell-down was coming for some time now.

- Divergence is normally seen as a warning to the downside and is still ahead if the Divergence isn't removed by a movement higher in Momentum.

- At some point, the major unfilled gaps (at much lower levels) must be filled. We anticipate a likely test of the 200 DMA in Q4.

- NVDA therefore may no longer become a Short to Intermediate Long Term hold, but rather a position trading stock, as other competitors enter the space, force margins and the earnings growth rate contracts.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

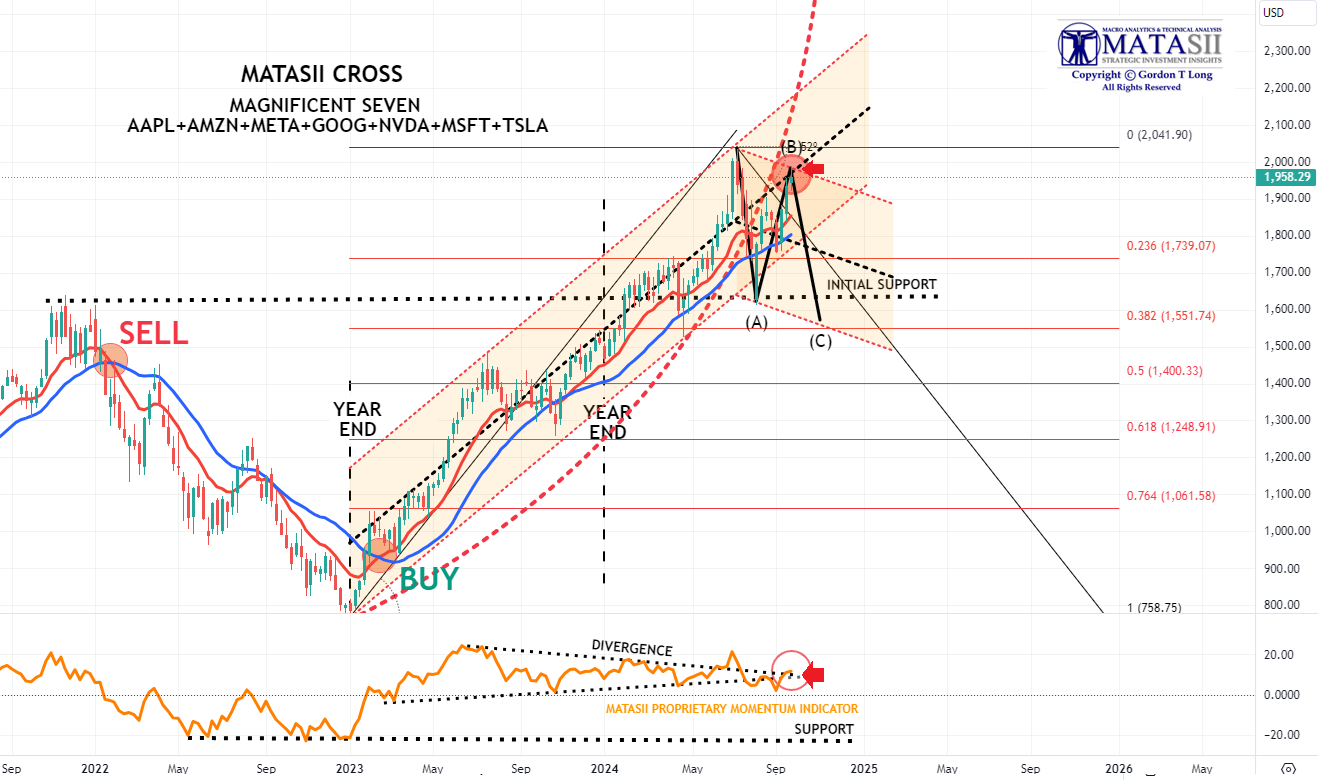

AS GOES NVDA SO GOES THE MAG-7

AS GOES THE MAG-7 SO GOES THE MARKET!

MAGNIFICENT 7

CONTROL PACKAGE

- APPLE - AAPL - DAILY (CHART LINK)

- AMAZON - AMZN - DAILY (CHART LINK)

- META - META - DAILY (CHART LINK)

- GOOGLE - GOOG - DAILY (CHART LINK)

- NVIDIA - NVDA - DAILY (CHART LINK)

- MICROSOFT - MSFT - DAILY (CHART LINK)

- TESLA - TSLA - DAILY (CHART LINK)

- The Magnificent Seven has counter rallied strongly back to the mid-point of its rising upper trend channel, (now an overhead resistance level), and above our long term expected 52 degree rate decay line.

- Meanwhile the MATASII Proprietary Momentum Indicator (lower pane) has once again also rebounded back to two major overhead resistance levels (dotted black lines).

- As we said in former reports: "A brief counter rally may ensue next week, but it is highly likely that Longer term Momentum Support (lower pane black dashed line) will soon be tested".

- Continued caution is advised since major global "Dark Pools" have been identified as presently operating behind the scenes on the Mag-7.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

"CURRENCY" MARKET (Currency, Gold, Black Gold (Oil) & Bitcoin) | |

|

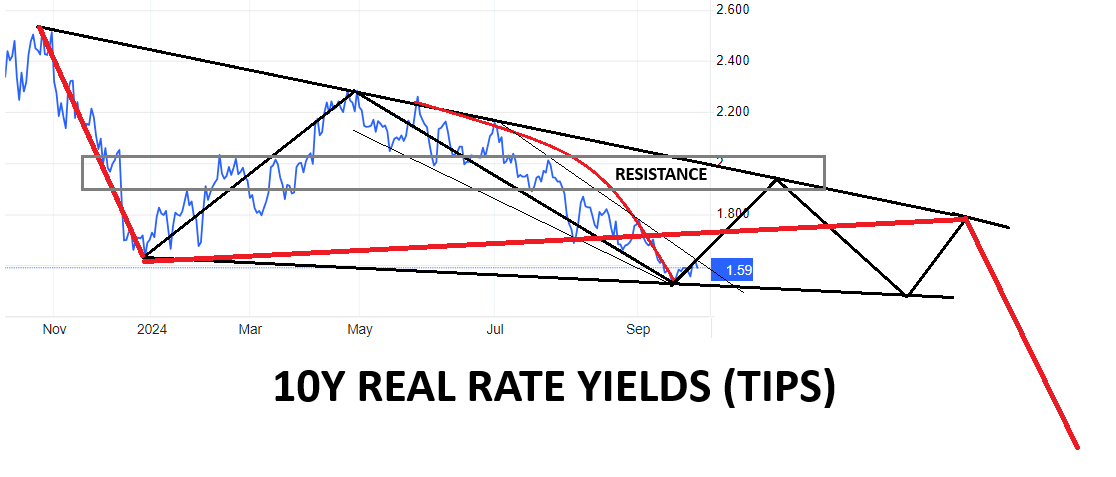

10Y REAL YIELD RATE (TIPS)

Real Rates continue to fall and begin to suggest an ending diagonal pattern is emerging, (shown in the chart to the right - as of close week ending 09/27/24). (LATEST)

NOTE: Gold is suggesting it will be resolved by the red line (chart right) with a fall in real rates (chart lower right) and rising Gold prices.

| |

CONTROL PACKAGE

There are TEN charts we have outlined in prior chart packages, which we will continue to watch closely as a CURRENT Control Set:

-

US DOLLAR -DXY - MONTHLY (CHART LINK)

-

US DOLLAR - DXY - DAILY (CHART LINK)

-

GOLD - DAILY (CHART LINK)

-

GOLD cfd's - DAILY (CHART LINK)

-

GOLD - Integrated - Barrick Gold (CHART LINK)

- SILVER - DAILY (CHART LINK)

-

OIL - XLE - MONTHLY (CHART LINK)

-

OIL - WTIC - MONTHLY - (CHART LINK)

-

BITCOIN - BTCUSD -WEEKLY (CHART LINK)

-

10y TIPS - Real Rates - Daily (CHART LINK)

| |

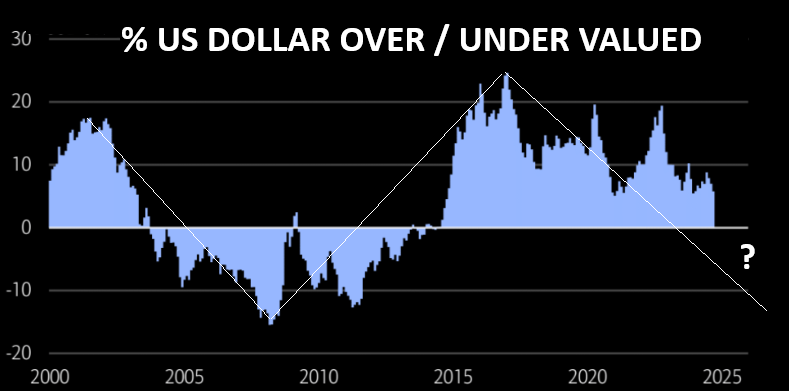

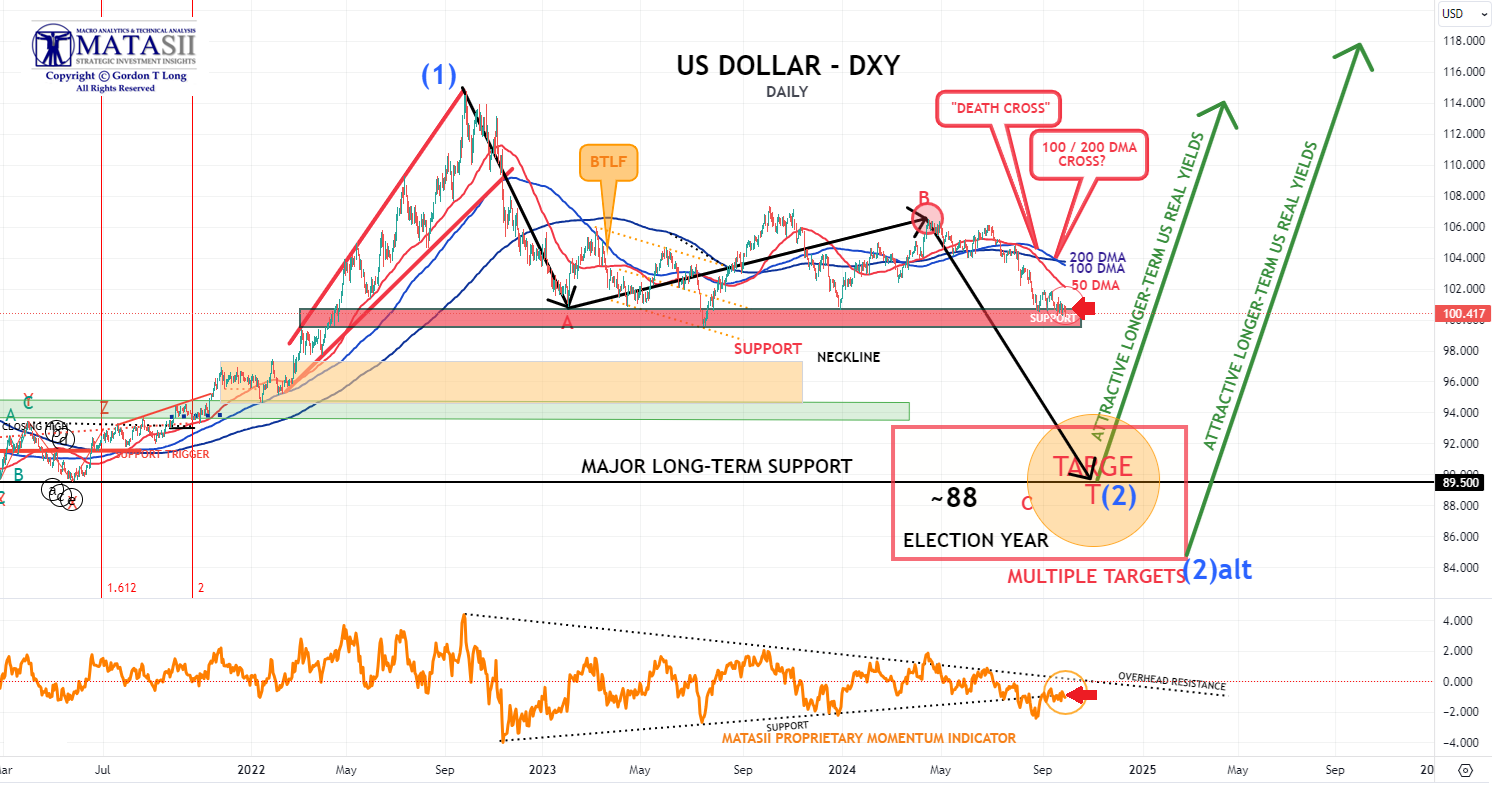

US DOLLAR - DXY - DAILY

CHART RIGHT:

Trading mean reversion often involves pain. The dollar continues trading close to range lows. It looks like it is going to "give in", but the DXY still manages holding these supports. Likely get a pop higher (max pain trade)?

CHART BELOW:

The US real effective exchange rate relative to moving average over past ten years.

This historically has been a mean reverting oscillator.

| |

MATASII CHART BELOW

- We have a Death Cross on the DXY, (the 50 DMA crosses the 200 DMA to the downside).

- We also have the 100 DMA in the process of crossing the 200 DMA to the downside.

- We would expect the Dollar to soon break its long held support level (red band below) - likely soon after the Fed cutting the Fed Funds Rate.

- The MATASII Proprietary Momentum Indicator (lower pane) appears ready to break its longer term support level (dotted black trend line).

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

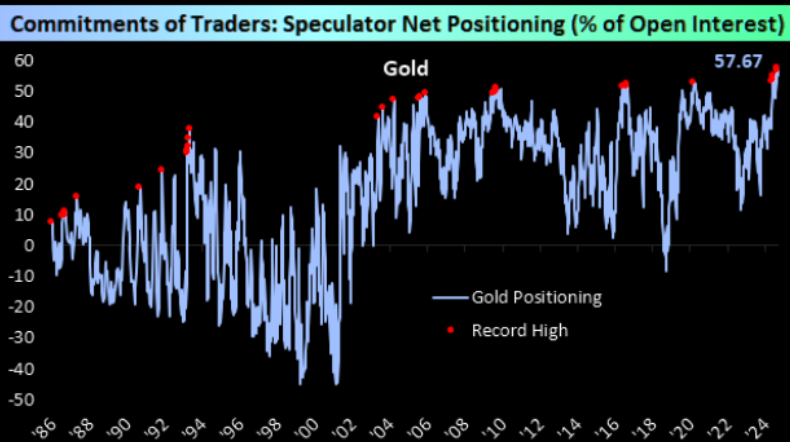

GOLD

CHART RIGHT:

It appears everyone is now chasing gold up here!

CHART BELOW:

Gold reversing in the upper part of the trend channel. The run up to channel highs has been impressive, but even great things "come to an end", or at least take a pause.

NOTE: The US 10Y Real Yield Rate (chart) is showing indications of a short term lift. Gold moves inversely to the Real Rate.

| |

CHART BELOW

- Gold continues to surge higher without the support of a falling dollar or further weakening in Real Rates.

- However, continue to watch Real Rates closely for a potential corrective / consolidation retreat. (see chart).

- The Macro continues to suggest higher prices with the dollar falling and Real Rates weakening.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

CONTROL PACKAGE

There are FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set":

- The S&P 500 (CHART LINK)

- The DJIA (CHART LINK)

- The Russell 2000 through the IWM ETF (CHART LINK)

- The MAGNIFICENT SEVEN (CHART ABOVE WITH MATASII CROSS - LINK)

- Nvidia (NVDA) (CHART LINK)

S&P 500 CFD

- The S&P 500 cfd decisively broke the previous Triple Top with the FOMC Rate announcement and continues to rise to new highs with weakening rate of rise.

- The MATASII Proprietary Momentum Indicator (middle panel) has found resistance at its overhead resistance "Divergence" level, (as part of a large wedge that appears soon to end).

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

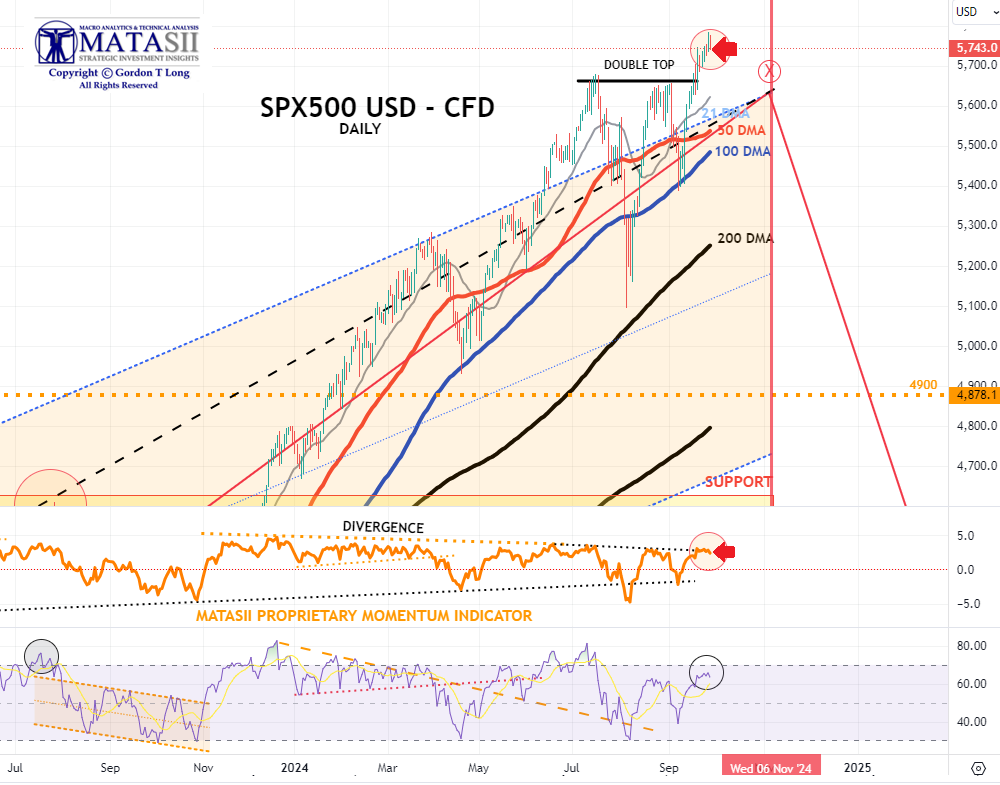

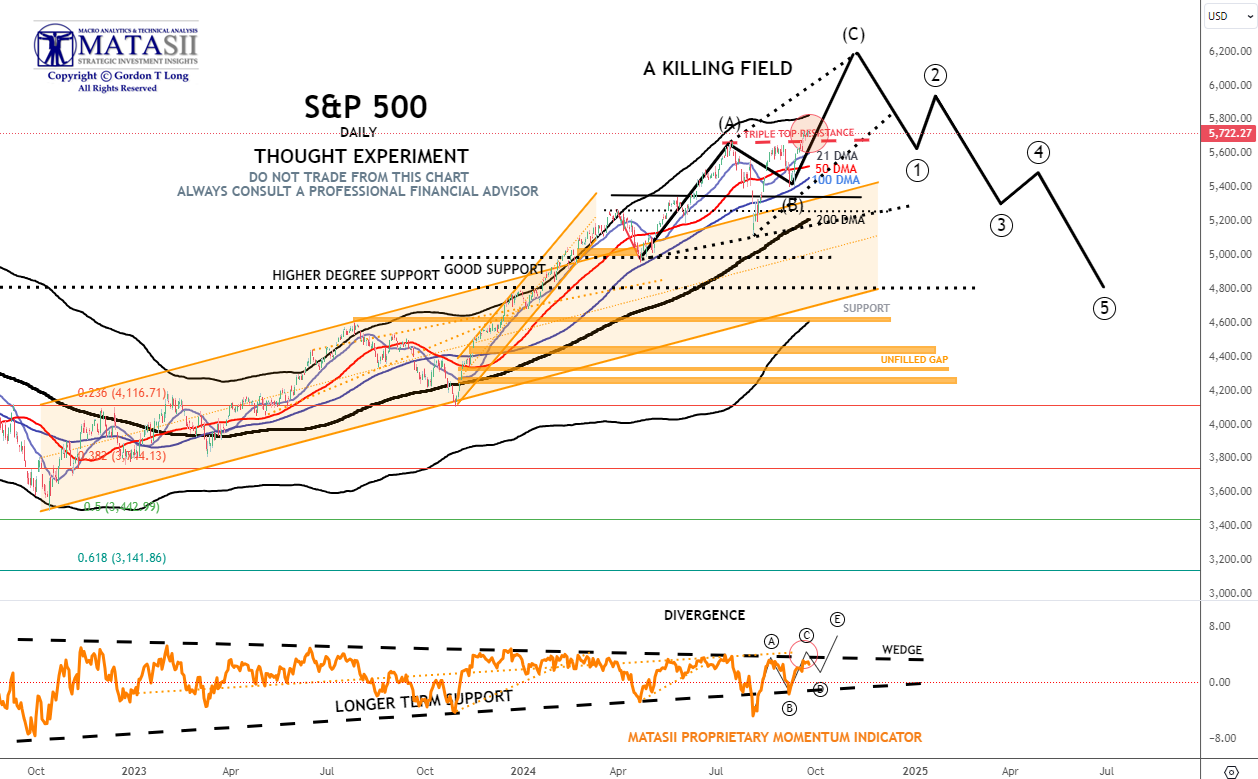

S&P 500 - Daily Our Thought Experiment

OUR CURRENT ASSESSMENT IS THAT THE INTERMEDIATE TERM IS LIKELY TO LOOK LIKE THE FOLLOWING:

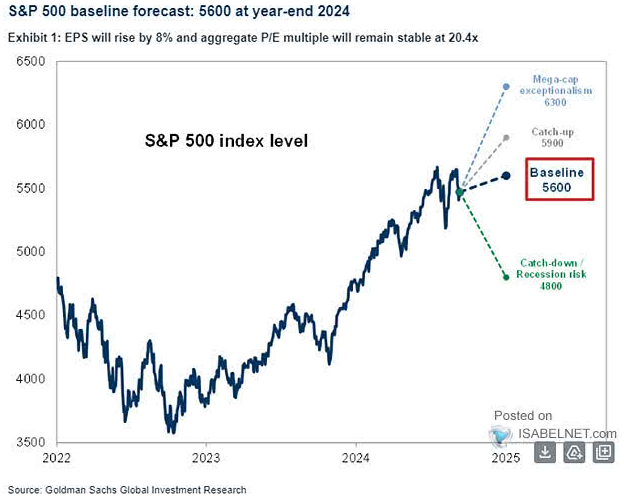

CHART RIGHT: In its base case scenario, Goldman Sachs projects a year-end 2024 price target of 5,600 for the S&P 500 index, supported by robust earnings growth and a stable price-to-earnings ratio.

NOTE: To reiterate - "the black labeled activity shown below, between now and September, looks like a "Killing Field", where the algos take Day Traders, "Dip Buyers", the "Gamma Guys" and FOMO's all out on stretchers!"

- We have a Triple Top ... and marginally broke it.

- The S&P 500 has broke higher since the FOMC Rate announcement and continues to rise to new highs.

- HOWEVER, The MATASII Proprietary Momentum Indicator (middle pane) has found resistance at its overhead resistance "Divergence" level, (as part of a large wedge that appears soon to end).

- The longer term Momentum Indicator wedge (dashed black lines) is narrowing. It appears the S&P 500 may now be looking to test lower support level before advancing further.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

STOCK MONITOR: What We Spotted

|  | |

LOWER BOND YIELDS CORRECTLY SPOT A WEAKER MACRO

CONTROL PACKAGE

There are FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set":

- The 10Y TREASURY NOTE YIELD - TNX - HOURLY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - DAILY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - WEEKLY (CHART LINK)

- The 30Y TREASURY BOND YIELD - TNX - WEEKLY (CHART LINK)

- REAL RATES (CHART LINK)

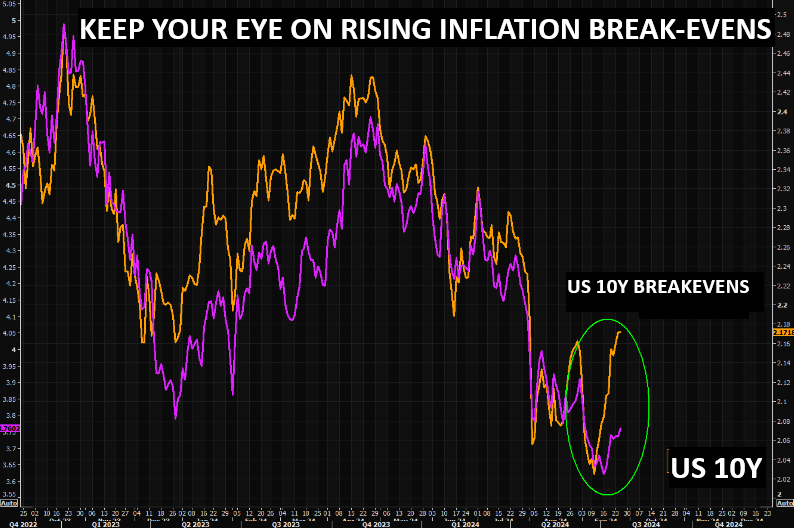

FISHER'S EQUATION = 10Y Yield = 10Y INFLATION BE% + REAL % = 2.148% + 1.59% = 3.738%

2YR AUCTION: Overall it was a mixed 2yr auction, as it came in on-the-screws against the prior 0.6bps stop-through and the six-auction average of a 0.3bps stop-through. Bid-to-cover was 2.59x, shy of the both the previous, 2.68x, and the average, 2.66x. Regarding the breakdown, dealers took 12.8% of the auction (prev. 11.9%, avg. 13.2%), while directs and indirects took 19.6% (prev. 19.1%, avg. 19.9%) and 67.6% (prev. 69.0%, avg. 66.8%), respectively. Overall, it was a very weak US 20yr auction whereby the High Yield tailed the WI by 2bps in contrast to the prior auction stopping through 0.1bps, and the six-auction average a stop through of 1.3bps. Bid-to-Cover was 2.51, also less than the prior, 2.54x, and the average, 2.68x. Looking at the takedown, Dealers, the forced buyers, took 18.6% much greater than the prior and avg. of 9.7% and 8.7%, respectively. Directs took 18.3% (prev. 19.3%, avg. 17.1%) while Indirects took 65.1% (prev. 71.0%, avg. 74.2%).

5YR AUCTION: The 5yr supply overall was mixed although the high yield of 3.519% came in on the screws with the WI at 3.519%, vs the prior and six auction average for a 0.3bps tail. The bid-to-cover of 2.38x was slightly below the prior but in line with the average. The breakdown saw primary dealers take just 11.5% of the auction, beneath the prior 13.2% and the average of 14.6%, thanks to a pick up in direct demand to 18.2% from 16.3%, which was also above the average. Indirect demand was more-or-less unchanged at 70.3%, holding above the six-auction average of 68%.

7YR AUCTION: Overall a strong 7yr auction, the high yield of 3.668% stopped through the when issued by 0.7bps, the largest stop through in the 7yr since March, a stronger sign of demand than the prior 0.9bp tail and six auction average for a tail of 0.1bps. The Bid-to-Cover of 2.63x was above the prior 2.5x and average 2.54x, while the breakdown was also encouraging with a notable pick up in direct demand. Direct bidders took 20.3% of the supply, rising from the prior 11.2% and average of 16.8%. Indirect demand declined to 70.8% from 75.1%, but still remained above the average 70.1%.

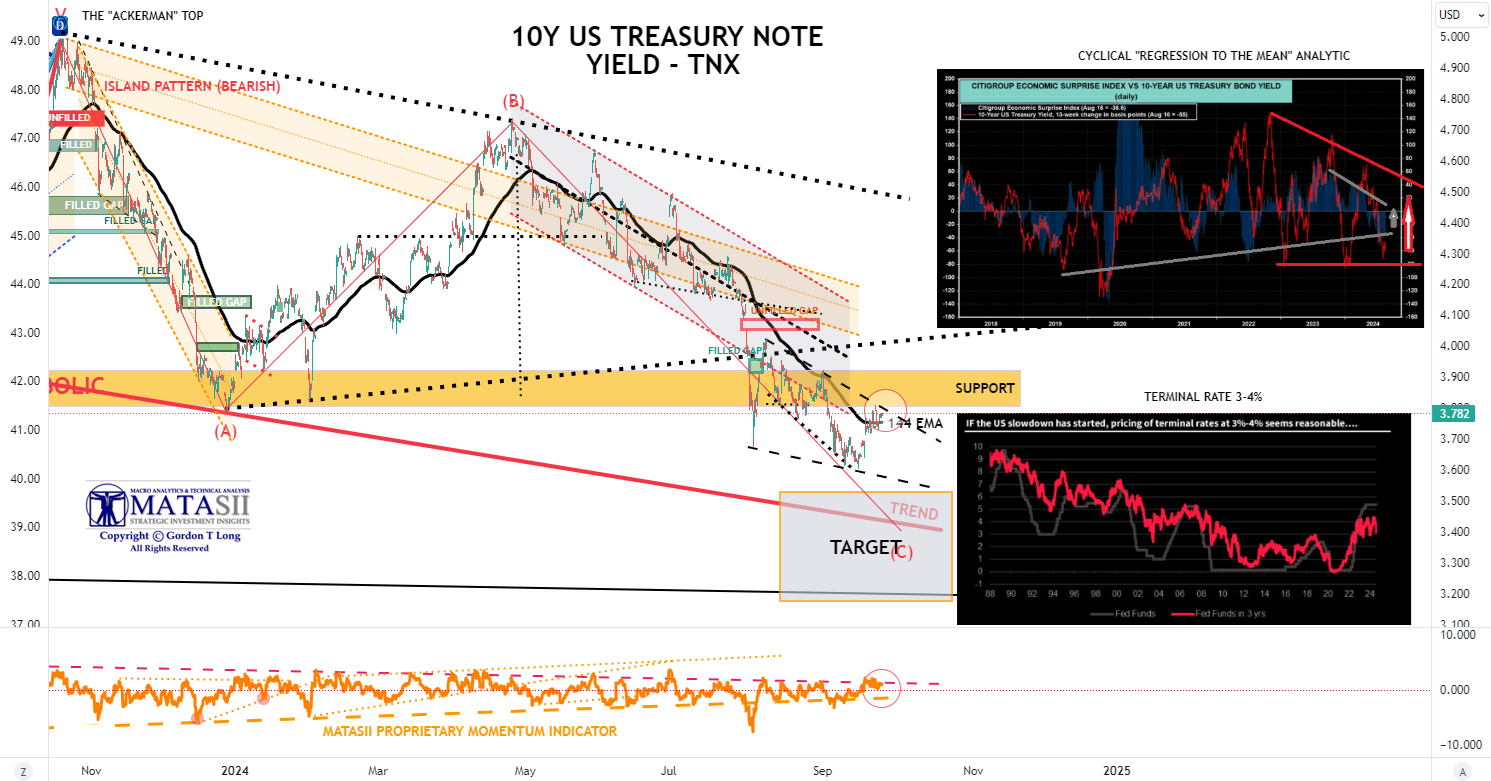

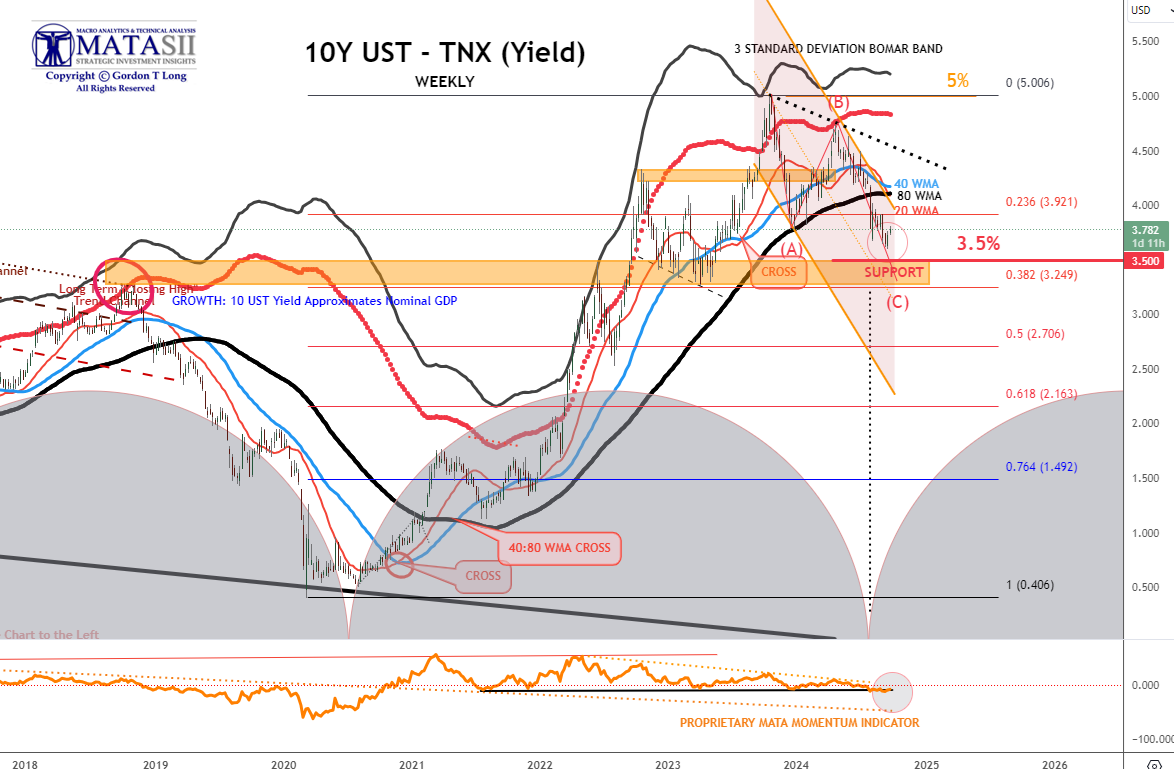

10Y UST - TNX - WEEKLY

- The 20 WMA has crossed the 80 WMA - this is normally quite Bearish for Yields!

- However, the distance of yields below the WMAs suggest a retracement towards the bands should be expected before heading lower.

- The Proprietary MATASII Momentum Indicator (lower pane) is also showing a test of its support trend level.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

10Y UST - TNX - HOURLY

- The TNX yields actually rose from the FOMC announcement of lower rates to the 144 EMA Resistance level.

- The Momentum Indicator (lower pane) is also showing a test of its overhead resistance level.

- The Bond Vigilante's continue to send a clear message to the Fed that they are behind the curve and yields should be taken lower.

- However, the Fed is signalling they will be taken lower but at a slower rate than the market is currently pricing in.

- Current rising Yields are likely reflective of pricing in the Fed's guidance.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond ‘fair use’, you must obtain permission from the copyright owner.

========

| |

MATASII'S STRATEGIC INVESTMENT INSIGHTS | |

2020 VIDEOS OUTLINING THE COMING RISE IN INFLATION, STAGLFLATION & COMMODITY PRICES | |

IDENTIFICATION OF HIGH PROBABILITY TARGET ZONES | |

Learn the HPTZ Methodology!

Identify areas of High Probability for market movements

Set up your charts with accurate Market Road Maps

Available at Amazon.com

| |

The Most Insightful Macro Analytics On The Web | | | | |