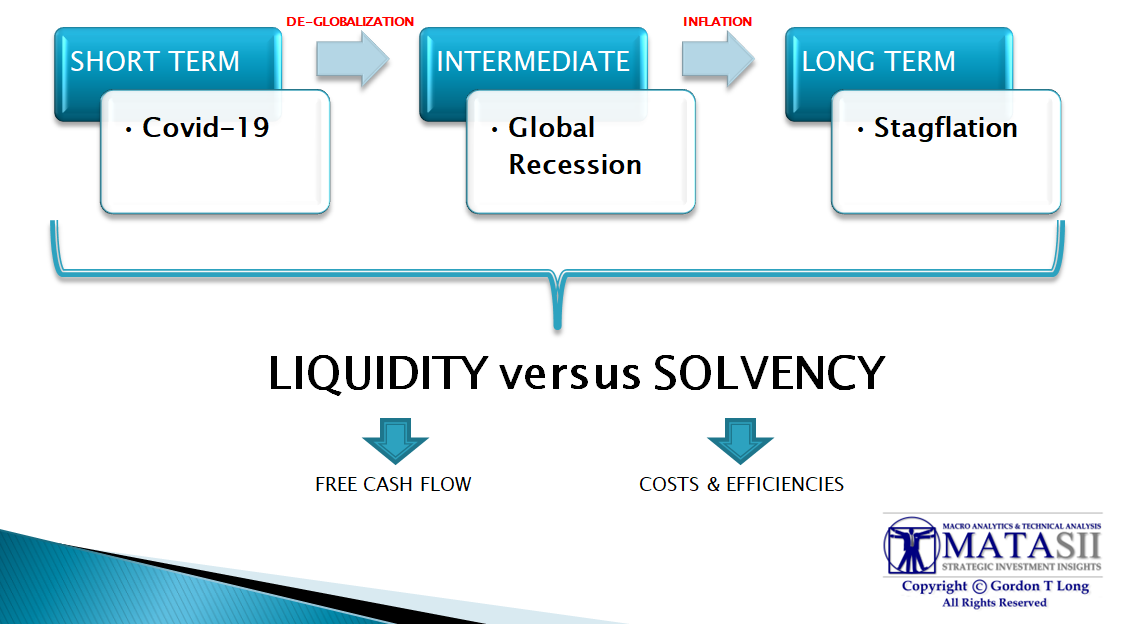

THE "AGE OF DISORDER" WILL BE GOOD FOR HARD ASSETS

We have seen five distinct global economic eras since 1860, and are now entering a sixth, which Deutsche Bank labels the "Age of Disorder". We most likely looking forward to a period that combines elements of the Bretton Woods era (when equities had average performance while bonds did terribly), and the messed-up decade of the 1970s between Bretton Woods and Volcker (when stocks and bonds both did badly). Commodities did well in both eras.

For those who think longer-term, the latest Long-Term Asset Return Study by Deutsche Bank AG's veteran financial historian Jim Reid should be examined. I highlight below some of the key charts and thoughts from his work:

Reid suggests we have seen five distinct global economic eras since 1860, and are now entering a sixth, which he labels the "Age of Disorder":

1. The first Era of Globalization (1860-1914)

2. The Great Wars and the Depression (1914-1945)

3. Bretton Woods and the return to a gold-based monetary system (1945-

1971)

4. The start of fiat money and the high-inflation era of the 1970s (1971-1980)

5. The second Era of Globalization (1980-2020?)

6. The Age of Disorder (2020?-????)

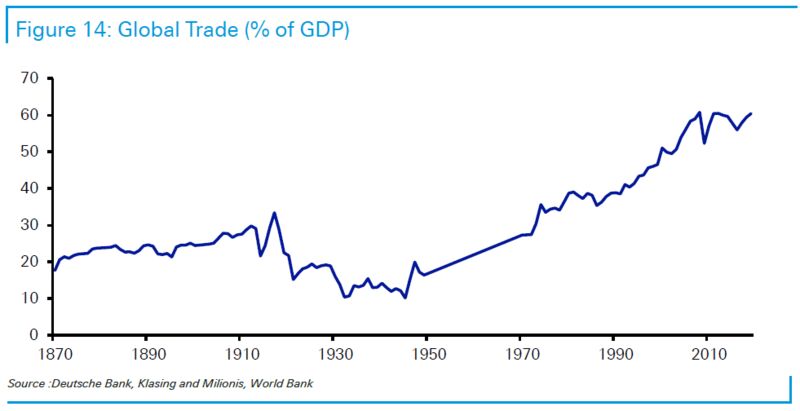

The two eras of globalization stand out in the following chart from Reid, which tracks trade as a share of GDP.

- At the point when President Nixon ended the Bretton Woods tie to gold, 50 years ago, trade was no greater as a proportion of the world economy than it had been on the eve of the First World War. It now makes up roughly double that share.

- The collapse of the Berlin Wall and then China's entry to the World Trade Organization really made a difference.

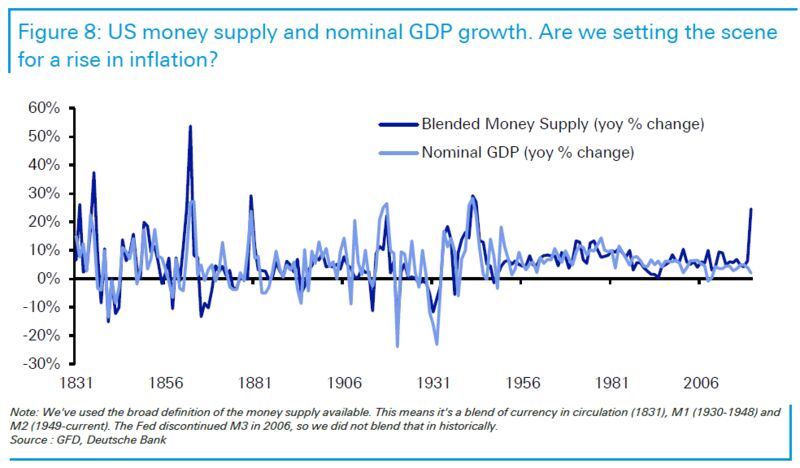

The problem, as Reid makes clear, is that for the last two decades, the current order has required ever greater reliance on debt. If you want to include the Covid impact, then debt as a proportion of GDP would move to levels only previously seen to fight the Second World War.

Covid-19 is catalyzing a breakdown in confidence in the existing order. Critically, the pandemic forced governments across the world into expansive fiscal policy to match the expansive monetary policy that has lasted a decade. If we combine that spending with a huge increase in the money supply, inflation may at last be ready to take off:

Reid isn't the first to point out that inequality is reaching politically intolerable levels, but he illustrates the phenomenon well. Wealth has become far more concentrated in the U.S. since Volcker and Reagan. And lenient taxation of companies is common to all major developed economies. That means labor has lost out to capital to an ever greater extent. Now, the power of capital may have been taken too far.

We can likely expect democratically elected governments to enact policies that favor labor at the expense of capital. Meanwhile, the fissure between the U.S. and China promises a retreat for globalization. That implies greater power for workers, as they no longer have to compete with cheaper labor overseas, and a return to inflation. The move toward a bipolar rather than a globalized world seems inexorable.

What does all this imply for asset returns?

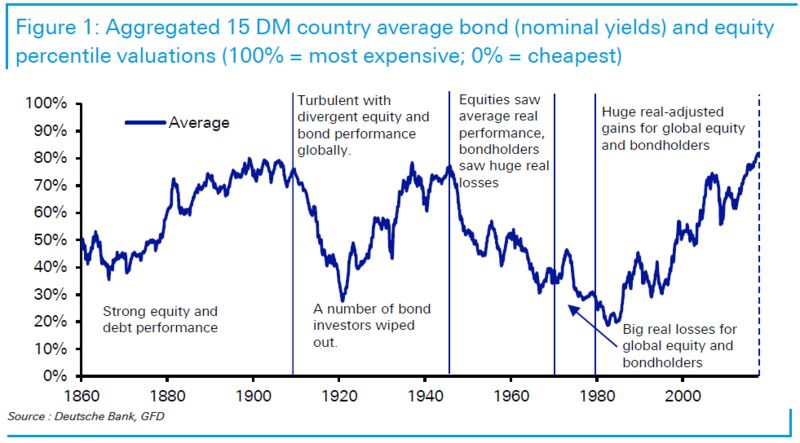

This chart smooshes together equity and bond returns for 15 developed markets since 1860. We most likely have to look forward to a period that combines elements of the Bretton Woods era (when equities had average performance while bonds did terribly), and the messed-up decade of the 1970s between Bretton Woods and Volcker (when stocks and bonds both did badly):

CONCLUSIONS

This isn't appealing.

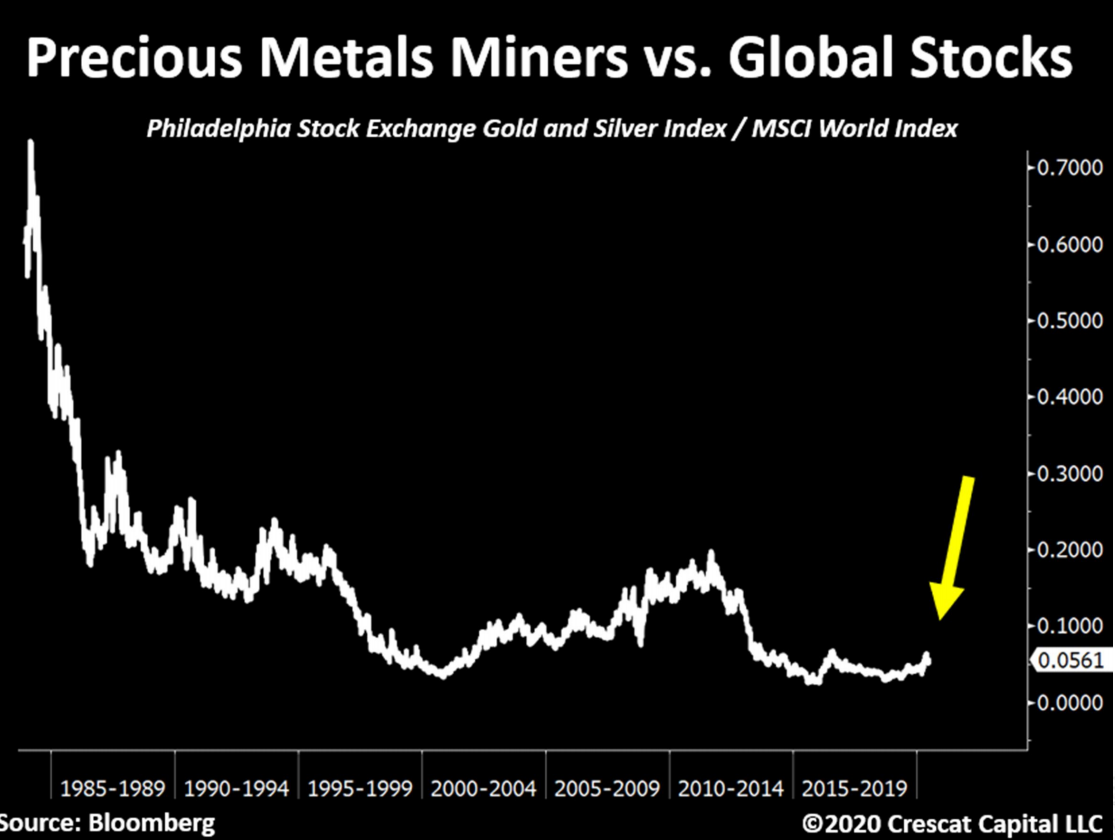

Betting on a return to inflation might be a good idea since the only period in which commodities outperformed was the Stagflationary 1970s. As commodities (excluding precious metals) have been mired in a bear market for more than a decade, and have a historical tendency to move in long waves, maybe that is one asset class to look at.

Many trends of the last decade seem to have been taken as far as they can go, if not too far. Extrapolating them further into the future would be a bad idea.