WILL 2021 BE THE YEAR OF HARD ASSETS?

INFLATION: We expect to see Inflation in the short to intermediate term impacting disposable income in the form of;

- Increased taxes at all levels of government,

- Covid-19 retail and services 'surcharges',

- Rising interest rates,

- Higher import costs &

- Higher food costs.

DEFLATION: On the other hand we expect to see increased deflation during the same period due to

- A decreased wealth effect, A

- A temporary slowing rate of government liquidity injections and

- Weak consumer demand due to unemployment and rising bankruptcies.

All of this will be negative for precious metals in the immediate near term but will set the stage for the next major leg up for Precious Metals in the first half of 2021..

IS THE QUANTITY OF MONEY FORMULA OBSOLETE OR TELLING US ALL WE NEED TO KNOW?

The following formula's were developed when:

- Money was not Fiat and backed by gold (making "M" now obsolete),

- Economies were dominantly domestic with exports playing a relatively minor role, (Making "T" now obsolete),

- Government Debt and Stimulus Deficit Spending were minor (Distorting the whole GDP formula by Transfer Payments to "C" and foreign financing impacting "I").

MV = PT

Where: "M" is Quantity of Money, "V" is Velocity of Money, "P" is Cumulative Average Price and "T" is volume of Goods and Services.

GDP = C + G + I +X(e-i)

Where: "C" is Consumption, "G" is Government, "I" is Investment and "X" is net of Exports and Imports.

Nevertheless, knowing GDP = MV = PT gives us some very useful information. If we include both Money and Credit in "M", and "T" to include net exports then we can see that M & T today are heavily influenced by the financing burden of the twin deficits. Also knowing that the US economy approximates a 70% consumption economy through the creation of debt (Government, Consumer and Corporate debt) then we can see that the financing rate of the debt is of paramount importance. Obviously this is the real reason why the Federal Reserve MUST keep rates near the zero bound to enable the financing of the ever increasing US debt.

Unfortunately, the US has reached the point where financing for the US debt must come increasingly from monetization or foreigners who must receive attractive rates and the security of a currency that won't devalue. The US$ as the global reserve currency and US Treasury debt as the benchmark for Risk Free, both of these long established cornerstones are now in serious question as well as EuroDollar financing.

What this means is that financial pressures for global financial stability are building that will require the US$ to be higher and UST real rates to also be higher or the global economy will suffer an immense shock. The long standing solution of "Kicking the Can Down the Road" suggests the powers to be can be fully expected to make this happen in whatever fashion it might take to avoid the shock.

It is our view therefore that higher US real rates in 2021 are likely to take Precious Metals higher, even with contrarily a stronger US$

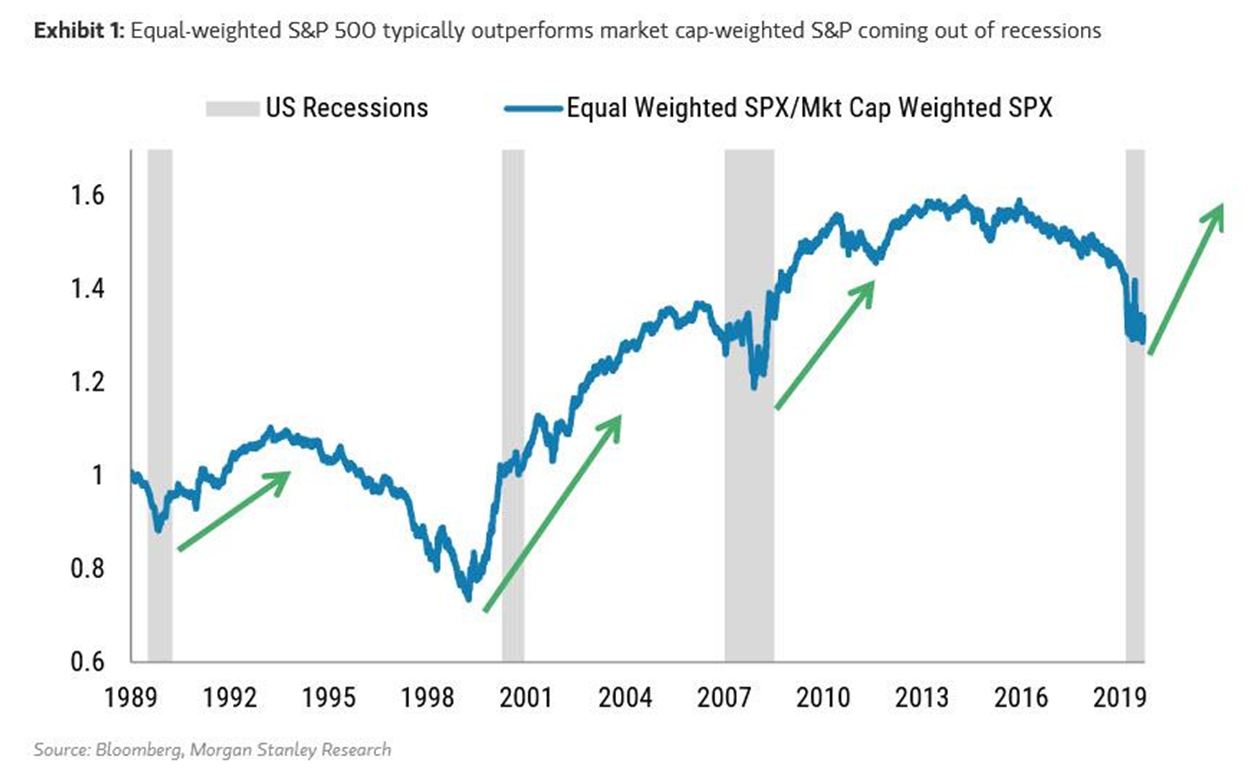

WILL INFLATION PLUS DEFLATION MEAN A ROTATION TO "VALUE"

Rising Inflation pressures (see below) as well as Deflationary pressures (see below) will force investors towards Value plays.

One way we see this occurring is a shift of the Equal Weight to Market Cap ratio (see below). This will be a rotation from the major market cap stocks within the market indices to the broader market which has not performed as well in during the pandemic rebound and currently offer better value.

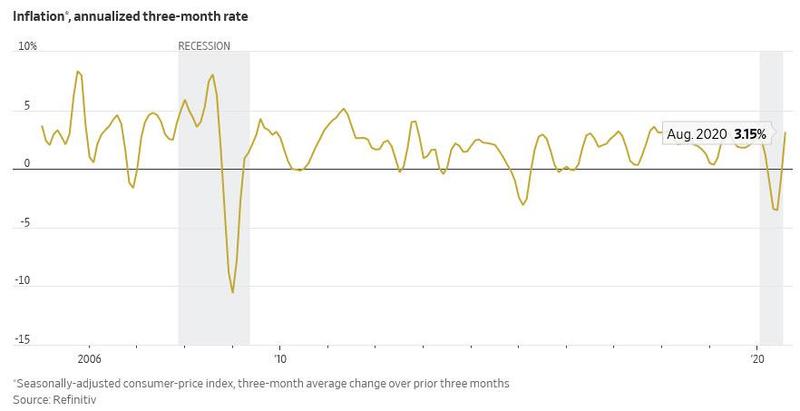

The gap between everyday experience and the yearly inflation rate of 1.3% in August is massive. The price of the stuff we're buying is rising much faster, while the stuff we're no longer buying has been falling, but still counts for the figures... the cost of food at home, where so many of us have been spending our time, was up 4.6% in August compared with a year earlier, the biggest rise in almost a decade. In deserted workplace and school cafeterias, food is 3% cheaper.

AUGUST UnderTheLens Video

- VIDEO: 18 Minutes with 49 Supporting Slides Inflation PLUS Deflation?

|

|

|

ADDENDUM TO THE OCTOBER UnderTheLens VIDEO

1- BOTH DEFLATION PLUS INFLATION

If the US$ is to weaken significantly over the next 12-18 months, then investment strategies are highly likely to change to reflect the following:

GOOD FOR:

- Investment Grade Bonds,

- Dividend Paying Stocks,

- Consumer Staples

GOOD FOR:

- Precious Metals,

- Commodities

2- INFLATION IS OCCURRING IN WHAT YOU ARE ACTUALLY BUYING

Inflation hasn't even picked up yet. Meanwhile, the chart of the gold price adjusted for CPI since the 70s looks like one of the largest and longest cup & handle charts we have ever seen. In other words, both the nominal and the real price of gold could be poised for a breakout.

EXPECTED PATTERN FORMATION

As the WSJ's James Mackintosh writes, "if it feels like the price of everything you buy has been soaring, that's because it has-even as central bankers everywhere worry about the danger of deflation." He then points out to the "massive gap" between everyday experience and the annual inflation rate of 1.3%, and notes that "the price of the stuff we're buying is rising much faster, while the stuff we're no longer buying has been falling, but still counts for the figures."

Which makes sense, of course: after all with more demand for a given good or service, the price will jump and vice versa. And as the data reveals, in this post-covid, "work-from-home" age, annual inflation for certain products is now solidly overshooting the Fed's targets:

Start with the cost of food at home, where so many Americans have been spending their time, and which was up 4.6% in August compared with a year earlier, the biggest rise in almost a decade. In deserted workplace and school cafeterias, food is 3% cheaper.

While food prices are traditionally volatile, the same pattern emerges for many things sensitive to us sitting at home on Zoom. Few home workers need a new suit or dress (down 17%), makeup (down 3%), hotel room (down 13%) or air ticket (down 23%). At the same, the following activities have led to sharp price increases: sitting at home in your pajamas (men's nightwear is up 4%), cycling (bikes up 6%), reading for pleasure (books up 4%, newspapers up 5%) and making things (sewing machines and fabric up 9%, cameras up 4%). Medical care is in demand (up 5%), while higher education is much less attractive (tuition fees up 1.3%, the lowest since data started in the late 1970s).

INFLATION & WAGES (FOR SKILLED/HIGHLY QUALIFIED EMPLOYEES) ARE RISING.

3- FOOD SHORTAGES AHEAD & WITH IT FOOD INFLATION

"We have witnessed farms dumping thousands of gallons of milk down the drain, meat producers slaughtering animals and burying them, and farmers destroying crops all over the country and the world. The reason for this is two-fold. First, many major producers would not want a glut of their product on the market and see their prices dropdown. Second, with the totalitarian measures forcing the shut down of restaurants across the country, many farms and producers lost a massive part of their market, thus destroying it.

- The head of the UN World Food Program repeatedly warned us that we would soon be facing "famines of biblical proportions", and his predictions are now starting to become a reality.

- We have already seen food riots in some parts of Africa, and it isn't too much of a surprise that certain portions of Asia are really hurting right now.

- The UN World Food Program is projecting that the number of people facing "severe food insecurity" in Latin American and Caribbean nations will rise by a whopping 270 percent in the months ahead.

- Historic flooding has been going on in China for months that is wiping out crops on a massive scale... Experts from the global financial services group Nomura said that although the flooding is among the worst that China has experienced since 1998, it could still get worse in the weeks to come, with the nation poised to lose $1.7 billion in agricultural production. However, since the start of the monsoon season, the area of flooded croplands have almost doubled. Nomura's estimates also do not include the potential loss of wheat, corn and other major crops. Therefore, China could be facing a far greater economic loss than current projections.

PANDEMIC'S SECOND WAVE: GROCERY STORES ARE PREPARING:

US FARMERS ARE IN TROUBLE!

- U.S. farmers have been going bankrupt in staggering numbers during this downturn, and the federal assistance that was supposed to help them survive has mostly gone to "large, industrialized farms"...

- U.S. farm bankruptcies hit an eight-year high last year, and they are on pace to go even higher this year.

|

EXPECT VOLATILITY BEFORE WE BEGIN SHIFTING TO "VALUE" FROM "GROWTH"

Rising Inflation pressures (see below) as well as Deflationary pressures (see below) will force investors towards Value plays. One way we see this occurring is a shift the Equal Weight to Market Cap ration (see below). This will be a rotation from the major market cap stocks within the market indices to the broader market which has not performed as well and offer better value.

EQUAL WEIGHTED VERSUS MARKET CAP

Between now and the election we can expect higher volatility and difficult trading environment. After the election either side will initiate Fiscal Stimulus which will assist with some degree of Economic recovery.

This would suggest consumer cyclicals/services, materials, industrials and financials. Moving down the capitalization curve makes sense. Perhaps the best way to express such a view is to look at the equal-weighted S&P 500 versus the market cap-weighted version.

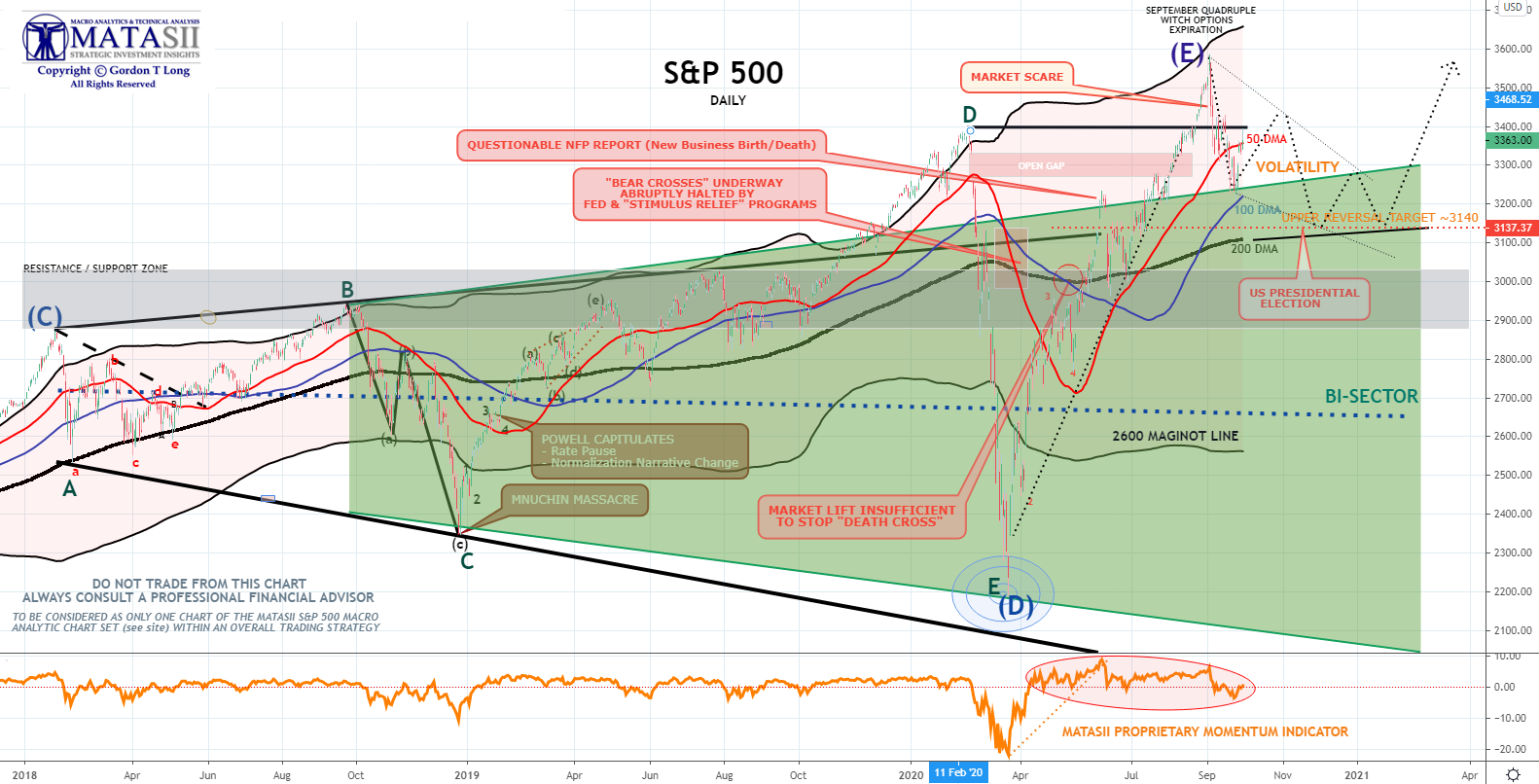

MATASII'S STRATEGIC INVESTMENT INSIGHTS

S&P 500

We have targeted the 200-day moving averages for the S&P 500 and Nasdaq 100 as good levels to think about, which are approximately 6% and 14% lower, respectively

Your LIVE DESK TOP / TABLET / PHONE

MACRO ANALYTIC Video Chart Link: SUBSCRIBER LINK

NOTE: Any Problems with this Chart: E-Mail lcmgroupe2@comcast.net

|

UnderTheLens - OCTOBER 2020

MACRO PERSPECTIVE:

VIDEO: 16 Minutes with 40 supporting slides.

NOTE: VIDEO IS CURRENTLY ONLY AVAILBALE TO SUSBCRIBERS

FULL TRANSCRIPTION: SUBSCRIBER LINK

|

|

|

|

|

|