|

UnderTheLens - JUNE 2024

Macro Analytics - 05/27/24

| |

THE US CONSUMER IS SLOWLY BREAKING

OBSERVATIONS: I'M AN IMMIGRANT & DON'T LIKE WHAT IS HAPPENING TO NEW IMMIGRANTS!

I am an immigrant to the US! I immigrated to the US over 35 years ago and I can tell you it wasn't easy. I strongly believe that it shouldn't be. Here is why...

I HAD TO PROVE MY WORTH

Being allowed into the US was an arduous process for me where I continually had to prove my worth. It was grueling as I went through: the Visa process (B1, H1) to be able to work, the Green Card authorizing permanent residency and planning a future, and finally the Citizenship process to vote and continue working. Each stage was a joyous occasion celebrating an achievement. Sneaking into the country in darkness of night is to completely rob your dignity and the great honor that becoming an American can eventually bestow on you!

I HAD TO PROVE MY DESIRE

During the process I could have no criminal convictions or would face immediate deportation with the humiliation and disruption. I had to study for and take an oral examination to prove that I understood what America stood for, how it was governed, what it believed in and what were the laws that bound "US" together. Our mass immigrant "paroles" are not educated on any of this and are being treated exactly as US criminal "paroles" are treated! They have been lied to about what awaits them if they simply "get in" by paying the cartels.

I HAD TO ESTABLISH MY LIFE ON MY OWN

It was certainly a challenge to get credit, banking, driver's license, mortgage, social security, medical coverage, etc., but I did it. I did it with confidence that I was building a future on rock and not sand of false expectations of government handouts. Our hopeful new citizens are left not knowing if they will be allowed to stay without a lifetime of "hiding". They are marooned in the hands of completely unfunded and ill equipped state and local services for handouts as they are caged in "shelters", gymnasiums and even former condemned prisons. Forsaken at the mercy of government bureaucrats, Washington politics with no direction on how to get on with building a life. They are left feeling as useful pawns within a senseless and confusing US political game. They must feel similar to those Americans that arrived on "slaver ships", but only with a different type of master. They must feel anything but free, instead feeling like captives of political masters versus the slave owners of old!

We are robbing and abusing them.

There is little doubt that out of every hundred there are minimally 5% that are bad people. In fact, large numbers have been directly released from hash prison. This is the type of raft they are forced to be exposed to. Unfortunately, they are also held accountable and tarnished by the US public for any heinous crimes that the five precent commit. Many are young and are being forced into crime by the 5% to survive in America.

I ALWAYS FELT THE OPPORTUNITIES IN AMERICA WERE INFINITE

Our new guests are being left to feel helpless, ill equipped and likely over time hopeless, since they have: ===>

| |

| |

THIS WEEK WE SAW

Exp=Expectations, Rev=Revision, Prev=Previous

US

US Philadelphia Fed Non-Manufacturing Activity May: -0.6 (prev. -12.4)

US S&P Global Manufacturing PMI Flash (May) 50.9 vs. Exp. 50.0 (Prev. 50.0)

US S&P Global Services PMI Flash (May) 54.8 vs. Exp. 51.3 (Prev. 51.3)

US S&P Global Composite Flash PMI (May) 54.4 vs. Exp. 51.1 (Prev. 51.3)

US New Home Sales-Units (Apr) 0.634M vs. Exp. 0.679M (Prev. 0.693M, Rev. 0.665M)

US Initial Jobless Claims 215k vs. Exp. 220k (Prev. 222k, Rev. 223k)

US Continued Jobless Claims 1.794M vs. Exp. 1.794M (Prev. 1.794M, Rev. 1.786M)

US KC Fed Manufacturing (May) -1.0 (Prev. -13.0)

US KC Fed Composite Index (May) -2.0 (Prev. -8.0)

===>

- No Skills

- Can't Speak the language

- Work is only what Americans can't live on and refuse to do!

- Minimum labor and minimum everything

- Seen to be an "election" party pawn by the powerful

- Treated like second class citizens

- Dumped in transient "compounds" and "shelters"

- Left in limbo, "unknowing" for potentially years?

- Forced to be a ward of the state

What are we as a nation doing about any of this? Where is the funding, the plan, the training and the process for citizenship? Even "Banana" Republics would have a publicly understood & supported plan?

WHAT KIND OF COUNTRY WOULD DO THIS???

What I see is not the America I know and came to love. None of this reflects our values. I find myself continuously wondering what the millions of new immigrants are feeling tonight??

How long will it be before they hate America .... and hate me?

| |

========================= | |

|

WHAT YOU NEED TO KNOW!

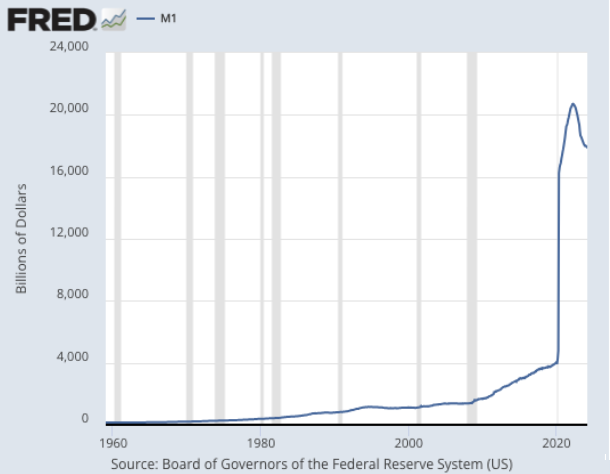

THE FACE OF MODERN MONETARY THEORY

"The chart to the right is the face of modern monetary theory and the ease in which governments can steal your wealth while it sits in the bank from unsound money. It is the face of an unfolding currency and financial system extinction event as people WAKE UP!

M1 is circulating supply and the fed and treasury increased it by 400% in Biden’s first year! The enormity can be seen in the timeline back to 1960. In that perspective it is a nuclear mushroom cloud. It most certainly is not prudence and good management by our banking masters. The financial system is now the face of a Potemkin village to the REAL economy which is shrinking rapidly. This is the fuel for GDP (aka government spending) which produces no wealth and is actually DEBT in Disguise. Producing nothing but a GDP print that creates endless malinvestments with no return".

Ty Andros, Today's Foremost Austrian Economist!

RESEARCH

- THE WHITE HOUSE DOESN'T UNDERSTAND THE "AVERAGE" US CONSUMER

- US consumer consumption was based on a strong & expanding middle class. That has also changed as we are now a country of "haves" and "have nots".

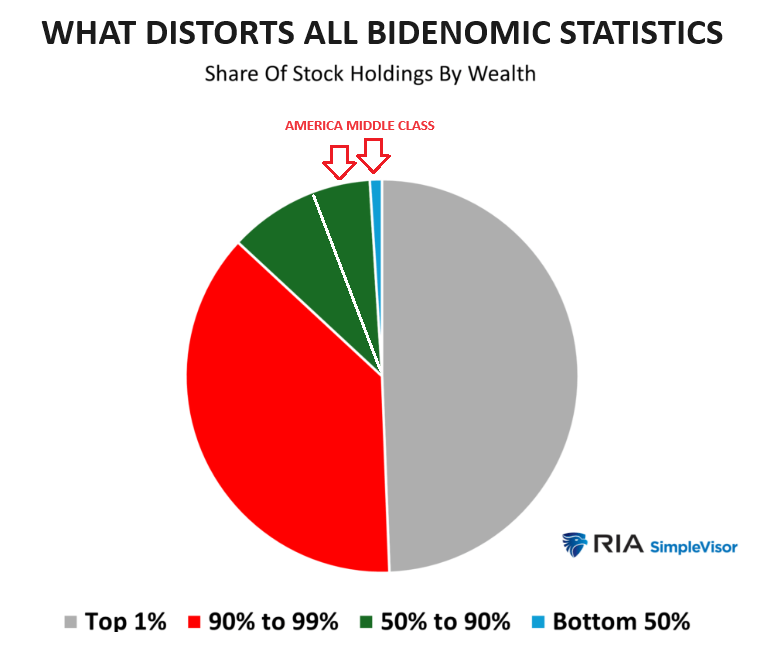

- The US Consumer is finally in trouble or more correctly has fractured. Fractured into "strata" or what could best be simplified as a "two tier economy", which Bidenomic statistics currently hides through the "great distorter".

- Most people are substantially below average because the wealthy have become so wealthy that the statistics don't reflect any reality of being mathematically average!, That is the Great Distorter of Bidenomics that the White House seems not to understand.

- INFLATION IS CRIPPLING THE GLOBALLY POWERFUL US CONSUMER

- According to a recent independent study (which I encourage you to read), a family of four in the US now needs to make over $$177,798 annually to live comfortably.

- Most Americans do not make enough money to “live comfortably” in the highly inflationary environment that we find ourselves in today.

- The study reveals the incomes needed for families to live comfortably across the United States and the stark contrast in the cost of living between states.

- The study reveals that in the most expensive states, families need nearly $300,000 to simply live ‘comfortably.’

- The least expensive state requires about half that salary – still over $100,000.

- Meanwhile, the average annual salary in the US is $59,428, or $28.34 per hour, as of May 2024.

- THE LOW END US CONSUMER IS NOW IN SERIOUS TROUBLE!

- It is Inflation and the rising cost of living which is now in the forefront of Americans' mind.

- Though every American is feeling this, it is the low-End US Consumer who is in serious trouble.

- You only have to go to your local Wal-Mart, Target or Dollar Store to visibly see what is happening in America.

- Mall Shopping and big "Anchor Stores" are long ago dead because it is simply no longer affordable to most.

- What Amazon or Temu can't cheaply and readily deliver you must try and hopefully find at Wal-Mart, Target or Dollar Tree.

- If you listened to these corporations recent quarterly earnings conference calls (as we did) the message is undeniable!

| |

|

DEVELOPMENTS TO WATCH

EV BLUNDER - GREEN HYBRID HYDROGEN SHIFT

- The forced EV adoption and mandated timeline for no fossil fuel vehicles on US roads was a major US Policy mistake.

- Competitive technology advancement is what delivers cost effective choices for the consumer. It can never be mandated by the political class.

- The market is rejecting EV for Hybrids and specifically Green Hydrogen Hybrids at the expensive tremendous amounts of wasted tax payer money.

RUSSIA RETALIATES BY SEIZING US & EU BANKS ASSETS

- We strongly warned in our March 11th Newsletter that it was a serious policy blunder for the US Asset Seizure of Russian Funds. It was both illegal and the consequences were financial suicide for the US International Banks forced into the scheme.

- The International court has ruled against it and thereby allowed Russia to reclaim its assets by seizure of US and EU banking assets.

- RESULT:

- Russia Seizes $440 Million From JPMorgan (FT).

- Russia Confiscates €800 Million From Deutsche Bank, Unicredit And Commerzbank (FT).

- Putin Decree Allows Seizure Of US Property & Assets If Russian Funds Taken By West (SOURCE)

| |

|

GLOBAL ECONOMIC REPORTING

1- ELECTION YEAR ECONOMICS

- The election year assignment given to Julie Su (Acting Labor Secretary controlling the BEA) is to ensure unfolding softer US employment data to keep Fed easing bets alive and a market that is forced to price this in, even though Inflation persists.

- The trick she must deliver is to balance the decay in a controlled and gradual fashion, like "boiling a frog" so Powell has more time to keep the expected "PIVOT" alive. ... ah .. the twisted web they weave!

2- WEEKLY JOBLESS CLAIMS

- BEA reported 215,000 Americans filed for jobless benefits for the first time last week. This was down from the prior week's 223,000.

- However, WARNs and job cut announcements (not provided by the government) are notably elevated?

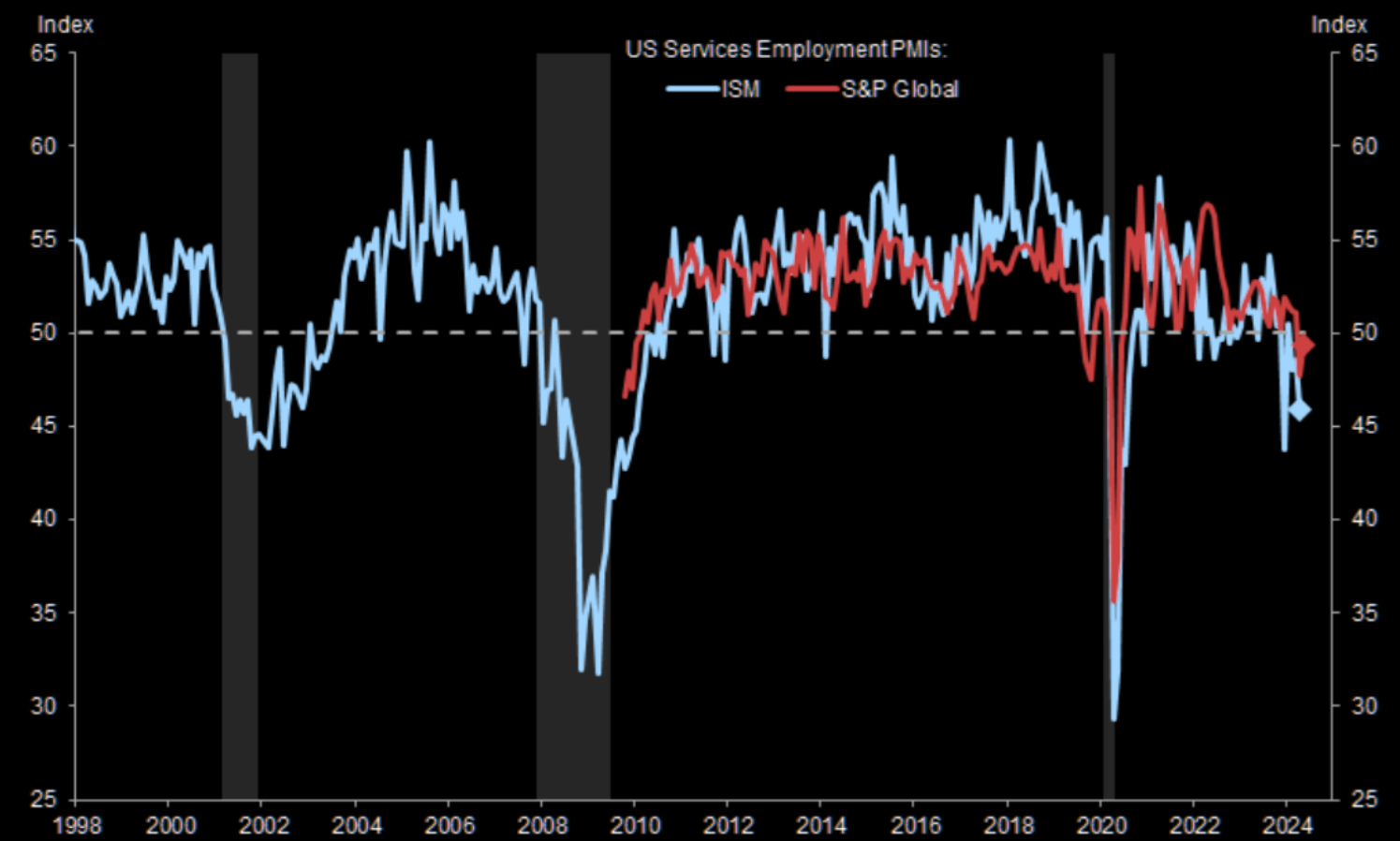

3- S&P GLOBAL PMI - Inflation Still A Problem!

- Flash US Services Business Activity Index at 54.8 (April: 51.3). 12-month high

- Flash US Manufacturing PMI at 50.9 (April: 50.0). 2-month high

- Selling price inflation has meanwhile ticked higher and continues to signal modestly above-target inflation.

- Factory input prices advanced at the fastest rate since November 2022.

| |

|

In this week's "Current Market Perspectives", we focus on the signals that sentiment, fundamentals and various markets (Credit, Bond and Equity) are currently giving us.

=========

| |

|

THE WHITE HOUSE DOESN'T UNDERSTAND THE "AVERAGE" US CONSUMER

I have found that the working stages of my life have been bound inextricably by a commonality, intriguingly illustrated by the chart to the right.

I grew up listening to my grandfather and father lamenting surviving the "Dirty Thirties". Well rooted in those stories, I began my working career in the early 70's and faced daily the struggles of client corporations installing our IBM mainframe computers to fight inflation and control costs. Subsequently as a professional investor navigating the Dotcom Bubble implosion through to the Financial Crisis, I found myself fighting turbulent and chaotic financial markets. Somehow, as challenging as all these periods in my life prosperity ensued, standards of living increased and the America Dream continued to shine brightly.

The more that I contemplated why the continuous advancement didn't faulter, the more I realized I appreciated it was because I had been blessed to have lived through an era of ever increasing consumption with seemingly no limits.

My financial success was to a large degree rooted in this appreciation as I capitalized on the US Economy becoming an economy driven on a foundation of a world leading 70 consumption engine. Over-stored, over-malled with more retail space per capita than anywhere in the known world.

| |

For years investors marveled at how powerful and robust the US consumer was. There seemed like there was nothing that could stop it - Recessions, Wars, Interest Rates, Inflation .. Investors who bet against it always lost and in the 90's finally labelled any such misplaced investment as a "Widow Maker"!

Investment success always meant NEVER betting against the US consumer's penchant to consume.

That has now changed!

The US Consumer is finally in trouble or more correctly has fractured.

Fractured into "strata" or what could best be simplified as a "two tier economy", which Bidenomic statistics currently hides through the "great distorter" shown to the right.

THE GREAT DISTORTER

According to the published statistics, the average pensioner has income of $70,000. These numbers make no sense to most people because NO ONE IS ACTUALLY AVERAGE! Most people are substantially below average because the wealthy have become so wealthy that the statistics don't reflect any reality of being mathematically average!

US consumer consumption was based on a strong & expanding middle class. That has also changed as we are now a country of "haves" and "have nots".

| |

Current statistics suggest the average retiree has an income of $70-$80K. Do you know anyone with this income? I know retired Doctors, Lawyers and Dentists who do not have this level of income!

This is why Bidenomics is a joke to the vast numbers of Americans. Yet to the "HAVES" in the White House and the Washington political class, they just think most Americans are "deplorables" or as Nancy Pelosi argued recently are lost in the right's populist democracy of "God, Gays & Guns". Those are how they describe their fellow Americas who are the "HAVE NOTS"!

| |

INFLATION IS CRIPPLING THE GLOBALLY POWERFUL US CONSUMER

According to a recent independent study (which I encourage you to read), a family of four in the US now needs to make over $$177,798 annually to live comfortably.

Most Americans do not make enough money to “live comfortably” in the highly inflationary environment that we find ourselves in today…

- The study reveals the incomes needed for families to live comfortably across the United States and the stark contrast in the cost of living between states.

- The study reveals that in the most expensive states, families need nearly $300,000 to simply live ‘comfortably.’

- The least expensive state requires about half that salary – still over $100,000.

- Meanwhile, the average annual salary in the US is $59,428, or $28.34 per hour, as of May 2024.

The study determined that Massachusetts is the most expensive state - it takes a whopping $301,184 a year for a family of four to “live comfortably” there.

If these numbers make no sense to you it is because once again they are "Averages" and the Great Distorter is doing its misleading game. It actually fosters inflation because it arms unions and labor with the ammunition to confront management with further wage demands. Once this genie is out of the bottle there is no putting it back in.

These numbers make no sense to most people because NO ONE IS ACTUALLY AVERAGE! Most people are substantially below average, because the wealthy have become so wealthy that the statistics don't reflect any reality of being mathematically average!

|  | |

THE LOW END US CONSUMER IS NOW IN SERIOUS TROUBLE!

As the chart to the right illustrates, it is Inflation and the rising cost of living which is now in the forefront of Americans' mind.

Though every American is feeling this, it is the low-End US Consumer who is in serious trouble.

LOW END RETAIL

You only have to go to your local Wal-Mart, Target or Dollar Store to visibly see what is happening in America.

Mall Shopping and big "Anchor Stores" are long ago dead because it is simply no longer affordable to most.

What Amazon or Temu can't cheaply and readily deliver you must try and hopefully find at Wal-Mart, Target or Dollar Tree.

If you listened to these corporations recent quarterly earnings conference calls the message is undeniable!

| |

WHAT THEY ARE OBSERVING:

WAL-MART

-

Walmart executives must be paying attention to Gen Z consumers bitching on TikTok and X about the failures of Bidenomics, as many of them have to work multiple jobs and still can't afford to put food on the table, pay shelter costs and buy gasoline at the pump. That's why America's largest retailer is launching a new line of cheap store-brand groceries for consumers, more importantly, targeting lost and hopeless youngsters. (READ)

- With prices soaring, consumers have been prioritizing staples over larger, discretionary purchases: this has dented sales of competitors such as Home Depot and Target. But as higher-income consumers trade down or search for deals, Walmart is benefiting from a decision to roll out more discounts and new products and revamp stores.

- Lower-income consumers are buying in similar patterns at Walmart, purchasing more groceries and other necessities than general merchandise.(READ)

TARGET

- Target Chief Executive Brian Cornell told reporters that high prices are hurting the wallets of customers.

- "We remain cautious in our near-term growth outlook," Christina Hennington, the company's chief growth officer, said.

- Hennington said discretionary spending would be under pressure in the coming months, adding demand for appliances and home products languishes. However, she noted apparel demand is improving.

- To mitigate further sales declines, Target is following Walmart's lead by lowering prices for cash-strapped consumers. The company said earlier this week that it would reduce prices on thousands of products this summer.

- It's not just Target and Walmart slashing prices. McDonald's recently entertained the idea of returning $5 meal deals again because low-income people are broke. (READ)

DOLLAR TREE

- Dollar Tree's CEO pointed out that the company's fastest-growing demographic is consumers making around $125k a year. This comes as Bidenomics fails what's left of the middle class. There really is something amiss with the economy when budget retailers can no longer supply customers with low-cost items.

- Hundreds of 99 Cents Only stores abruptly closed, and the company was forced into liquidation due to "rising levels of shrink, persistent inflationary pressures and other macroeconomic headwinds." (READ)

MACDONALDS & BURGER KING

- First McDonald's, Now Burger King Admits Consumers are Broke With Planned Reintroduction of $5 Meal Deal.

- The bigger story is that mega-corporations are cutting prices and offering deals because, as Goldman has shown, working-poor consumers have hit a proverbial brick wall. (READ)

NOTE: THURSDAY EARNINGS ANNOUNCEMENT: PDD (PDD) +1.1%: EPS and revenue surpassed expectations - powered by strong adoption of its international shopping site, Temu, and as it attracted more price-conscious customers.

| |

THE OVERALL CONSUMER IS LIKELY TO SURVIVE UNTIL THE ELECTION - BUT 2025 WILL BE DEVASTATING FOR CONSUMPTION

NOTE: If you find the above caption "over-the-top", I encourage you to listen to our current video for the reality of what election economic damage is being done in advance of 2025.

COVER BY RETAIL ANALYSTS

- The XLY consumer discretionary ETF down about 4% since our April 8 note, but it is also down roughly the same for the year, even as the broader S&P plows higher, and is now some 11% higher.

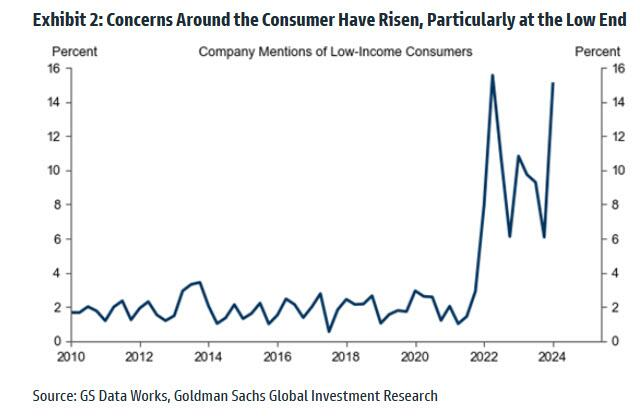

- Low Income Concern

- Overall strong spending growth could mask substantial weakness under the surface, especially since "companies increasingly called out a weaker lower-end consumer in Q1 earnings calls", or in other words, mentions of low-income consumers are at record levels, and matching the post-covid crash.

- That many companies suggested that higher rates and price levels have "forced consumers in lower income strata to make increasingly difficult trade-offs that could eventually lead to a pullback in spending" - view validated by the weak April retail sales report, and signs of a slowing labor market.

- Growing concern about the bottom 50 percentile of US consumers

- Goldman: "we anticipate underperformance for lower-income households due to weaker growth in transfer income, (largely reflecting a post-pandemic normalization in Medicaid enrollment) and outperformance for higher-income households due to outsized gains in interest income on the back of higher rates."

- Negative sentiment around consumer spending, particularly at the end of Q1 and start of Q2.

- First, tax withholdings—which are based on tax brackets that reset to realized inflation with a lag—increased by more than expected at the start of 2024. The effective tax rate (tax payments divided by personal income) rose by 0.6pp relative to end-2023 through March, effectively lowering real disposable personal income (DPI) growth by 2.4pp on a quarter-on-quarter annualized basis in Q1.

- Second, capital gains tax payments (proxied by non-withheld tax receipts) increased by more than expected this spring and is currently tracking more than $60bn above 2023 levels in real terms, thereby creating a headwind to spending around the April tax deadline. This increase in tax payments, as well as a hit from a moratorium on employee retention tax credit (ERTC) claims, can explain some (but not all) of a decline in real average tax refunds in 2024 relative to prior years.

- Third, upside inflation surprises in Q1 likely weighed on consumer spending for two reasons. First, larger-than-expected price increases eroded nominal income gains and household spending power. Second, consumer sentiment is highly correlated with inflation, implying that the Q1 inflation surge likely lowered households’ assessment of the overall economic outlook, particularly for lower-income households who remain most exposed to price increases.

We would agree with the optimistic view, at least until the elections, after which the fiscal stimulus will fall off a cliff and with it the spending power of US consumers.

"Risks around our spending growth forecast as asymmetrically skewed to the downside, mostly because the saving rate,

is already low and there is no clear catalyst for an acceleration in spending going forward."

| |

|

DEVELOPMENTS TO WATCH

EV BLUNDER - THE GREEN HYBRID HYDROGEN SHIFT

- The forced EV adoption and mandated timeline for no fossil fuel vehicles on US roads was a major US Policy mistake.

- Competitive technology advancement is what delivers cost effective choices for the consumer. It can never be mandated by the political class.

- The market is rejecting EV for Hybrids and specifically Green Hydrogen Hybrids at the expensive tremendous amounts of wasted tax payer money.

THE PROBLEM WITH EV

- Batteries are the critical flaw with EV. The porblem isn't electric, but the forced limited storage of electricity.

- Batteries must be recharged which takes time, tremendously impacting usability, convenience and requiring vast supporting charging infrastructure.

- Batteries are heavy which impacts Heavy Freight hauling road restrictions and regulations.

- Batteries as built into EVs are tremendously expensive to replace or repair. It is so serious that residual values have forced fleets such as Hertz to sell their cars to stave off bankrupting the corporations.

- Batteries come with an element of fire risk which has proven to be a real world problem.

- Batteries suffer limitations in extreme cold and heat environments.

- Charging Stations are not convenient and a long ways from making "road trips" with EV extremely limiting, impossible or prohibitive.

- EVs are more expensive regarding Insurance for damage (battery replacements and electronics required) as well as home insurance if charging from home (mandatory for public useability).

WHY HYBRIDS

- Removal of the storage requirement of electricity through batteries

- More convenient and builds upon modifications of the existing national refueling infrastructure (faster implementation)

- Time and cost to market to meet current government mandates

- Proving to be less expensive because of the exploding cost and availability of Lithium, Nickle and Zinc

The best current Hybrid choice is a Clean Hydrogen Fuel Cell (Avoid Battery Storage) to Generate

an Electric Powered Drive Train.

| |

|

RUSSIA RETALIATES BY SEIZING US BANKING ASSETS

We strongly warned in our March 11th Newsletter that it was a serious policy blunder for the US Asset Seizure of Russian Funds. It was both illegal and the consequences were financial suicide for the US International Banks forced into the scheme.

The International court has ruled against it and thereby allowed Russia to reclaim its assets by seizure of US and EU banking assets.

- Russia Seizes $440 Million From JPMorgan (FT)

- Russia Confiscates €800 Million From Deutsche Bank, Unicredit And Commerzbank (FT)

- Putin Decree Allows Seizure Of US Property & Assets If Russian Funds Taken By West (SOURCE)

It has only begun! The US government gave the money to Ukraine. Who is going to now make the international banks whole? THESE ARE MASSIVE BOTTOM LINE LOSSES that will force major reassessment of these banks lending capabilities. Can anyone hear "Liquidity Bleed"?

| |

|

GLOBAL ECONOMIC INDICATORS:

What This Week's Key Global Economic Releases Tell Us

ELECTION YEAR ECONOMICS

The election year assignment given to Julie Su (Acting Labor Secretary(directing the BEA) is to ensure unfolding softer US employment data to keep Fed easing bets alive and a market that is forced to price this, though Inflation persists.

The trick she must deliver is to balance the decay in a controlled and gradual fashion like "boiling a frog" so Powell has more time to keep the expected "PIVOT" alive. ... ah .. the twisted web they weave!

| |

|

WEEKLY JOBLESS CLAIMS

BEA reported 215,000 Americans filed for jobless benefits for the first time last week. This was down from the prior week's 223,000.

However, WARNs and job cut announcements (not provided by the government) are notably elevated (red line in chart on the right).

Meanwhile Initial Jobless claims are lower and appear so small as to almost not budge (green line at the bottom of the chart)?

| |

S&P GLOBAL PMI

INFLATION IS NOT YET UNDER CONTROL!

-

Flash US Services Business Activity Index at 54.8 (April: 51.3). 12-month high

-

Flash US Manufacturing PMI at 50.9 (April: 50.0). 2-month high

S&P Global US business activity accelerated in early May at the fastest pace in two years, largely reflecting stronger growth for service providers and the accompanied pickup in inflation.

The S&P Global flash May composite purchasing managers index advanced by more than 3 points to 54.4, the highest since April 2022.

- Selling price inflation has meanwhile ticked higher and continues to signal modestly above-target inflation.

- Factory input prices advanced at the fastest rate since November 2022.

| |

|

GLOBAL MACRO

WHAT DOES YOUR SCAN OF THE DATA BELOW TELL YOU? - THE MEDIA AVOIDS BAD NEWS!

We present the data in a way you can quickly see what is happening.

THIS WEEK WE SAW

Exp=Expectations, Rev=Revision, Prev=Previous

| |

|

UNITED STATES

- US Philadelphia Fed Non-Manufacturing Activity May: -0.6 (prev. -12.4)

- US S&P Global Manufacturing PMI Flash (May) 50.9 vs. Exp. 50.0 (Prev. 50.0)

- US S&P Global Services PMI Flash (May) 54.8 vs. Exp. 51.3 (Prev. 51.3)

- US S&P Global Composite Flash PMI (May) 54.4 vs. Exp. 51.1 (Prev. 51.3)

- US New Home Sales-Units (Apr) 0.634M vs. Exp. 0.679M (Prev. 0.693M, Rev. 0.665M)

- US Initial Jobless Claims 215k vs. Exp. 220k (Prev. 222k, Rev. 223k)

- US Continued Jobless Claims 1.794M vs. Exp. 1.794M (Prev. 1.794M, Rev. 1.786M)

- US KC Fed Manufacturing (May) -1.0 (Prev. -13.0)

- US KC Fed Composite Index (May) -2.0 (Prev. -8.0)

JAPAN

- Japanese Trade Balance (JPY)(Apr) -462.5B vs. Exp. -339.5B (Prev. 387.0B)

- Japanese Exports YY (Apr) 8.3% vs. Exp. 11.1% (Prev. 7.3%)

- Japanese Imports YY (Apr) 8.3% vs. Exp. 9.0% (Prev. -5.1%)

- Japanese Machinery Orders MM (Mar) 2.9% vs. Exp. -2.2% (Prev. 7.7%)

- Japanese Machinery Orders YY (Mar) 2.7% vs. Exp. 2.3% (Prev. -1.8%)

- Japanese JibunBK Manufacturing PMI Flash SA (May) 50.5 (Prev. 49.6)

- Japanese JibunBK Services PMI Flash SA (May) 53.6 (Prev. 54.3)

- Japanese National CPI YY (Apr) 2.5% vs. Exp. 2.4% (Prev. 2.7%)

- Japanese National CPI Ex. Fresh Food YY (Apr) 2.2% vs. Exp. 2.2% (Prev. 2.6%)

- Japanese National CPI Ex. Fresh Food & Energy YY (Apr) 2.4% vs. Exp. 2.5% (Prev. 2.9%)

UK

- UK Rightmove House Price Index MM 0.8% (Prev. 1.1%)

- UK CPI MM (Apr) 0.3% vs. Exp. 0.2% (Prev. 0.6%)

- UK CPI YY (Apr) 2.3% vs. Exp. 2.1% (Prev. 3.2%)

- UK Core CPI MM (Apr) 0.9% vs. Exp. 0.7% (Prev. 0.6%)

- UK Core CPI YY (Apr) 3.9% vs. Exp. 3.6% (Prev. 4.2%)

- UK CPI Services MM (Apr) 1.50% vs. Exp. 1.10% (Prev. 0.60%)

- UK CPI Services YY (Apr) 5.90% vs. Exp. 5.50% (Prev. 6.00%)

- UK Flash Manufacturing PMI (May) 51.3 vs. Exp. 49.5 (Prev. 49.1)

- UK Flash Services PMI (May) 52.9 vs. Exp. 54.7 (Prev. 55.0)

- UK Flash Composite PMI (May) 52.8 vs. Exp. 54.0 (Prev. 54.1)

- UK GfK Consumer Confidence (May) -17.0 vs. Exp. -18.0 (Prev. -19.0)

| |  |

|

EU

- Eurozone Labor Costs Prelim Y/Y (Q1) 4.9% (Prev. 3.4%)

- EU HCOB Manufacturing Flash PMI (May) 47.4 vs. Exp. 46.2 (Prev. 45.7)

- EU HCOB Services Flash PMI (May) 53.3 vs. Exp. 53.5 (Prev. 53.3)

- EU HCOB Composite Flash PMI (May) 52.3 vs. Exp. 52.0 (Prev. 51.7)

- EU Consumer Confidence Flash (May) -14.3 vs. Exp. -14.2 (Prev. -14.7)

- EZ Negotiated Wages (Q1) 4.69% vs. Exp. 4.3% (Prev. 4.45%)

GERMANY

- German Producer Prices MM (Apr) 0.2% vs. Exp. 0.3% (Prev. 0.2%)

- German Producer Prices YY (Apr) -3.3% vs. Exp. -3.1% (Prev. -2.9%)

- German HCOB Manufacturing Flash PMI (May) 45.4 vs. Exp. 43.1 (Prev. 42.5)

- German HCOB Services Flash PMI (May) 53.9 vs. Exp. 53.5 (Prev. 53.2)

- German HCOB Composite Flash PMI (May) 52.2 vs. Exp. 51.0 (Prev. 50.6)

SOUTH AFRICA

- South African CPI MM (Apr) 0.3% vs. Exp. 0.4% (Prev. 0.8%); YY (Apr) 5.2% vs. Exp. 5.3% (Prev. 5.3%)

SWEDEN

- Swedish Unemployment Rate (Apr) 8.9% (Prev. 9.2%)

SINGAPORE

- Singapore GDP QQ (Q1 F) 0.1% vs Exp. 0.1% (prev. 1.2%)

- Singapore GDP YY (Q1 F) 2.7% vs Exp. 2.5% (prev. 2.7%)

AUSTRALIA

- Australian Consumer Sentiment MM (May) -0.3% (Prev. -2.4%)

- Australian Westpac Consumer Sentiment Index (May) 82.2 (Prev. 82.4)

- Australian Judo Bank Manufacturing PMI Flash (May) 49.6 (Prev. 49.6)

- Australian Judo Bank Services PMI Flash (May) 53.1 (Prev. 53.6)

NEW ZEALAND

- New Zealand Retail Sales Volumes QQ (Q1) 0.5% vs. Exp. -0.3% (Prev. -1.9%)

- New Zealand Core Retail Sales QQ (Q1) 0.4% vs Exp. 0.0% (Prev. -1.7%)

| |

CURRENT MARKET PERSPECTIVE | |

|

NVIDA SIGNALS MARKET DIRECTION

A STALLING TRADING RANGE

Click All Charts to Enlarge

| |

A RED DOW - Every single stock in the Dow Jones was red Thursday after the Nvidia earnings release. It has been a long time since this last happened. The first time this has happened in 2024. Nvidia is single handedly responsible for just under half of the +6% SPX earnings growth seen this quarter. How perfectly fitting then that NVDA all by itself held up the stock market Thursday. | |

1 - SITUATIONAL ANALYSIS | |

|

ENTERING A RANGE BOUND MARKET?

Positioning might not be a major tailwind going forward, but it also isn’t necessarily a big headwind.

There are two key reasons for this:

1. We’ve yet to see a broad-based chase or reaching for risk. Example, the 1wk or 4wk change z-scores have yet to tick up to more extended levels.

Additionally, there’s been little sustained short covering among Hedge Funds.

2. High levels of positioning on their own aren’t necessarily followed by market weakness. Example, for most of 1Q24, positioning was around where it is today and the market rallied. Same thing was true for most of 2021.

CONCLUSION: Expect a trading range bound market within moderately higher highs and lows bound by rising 50 and 100 DMAs.

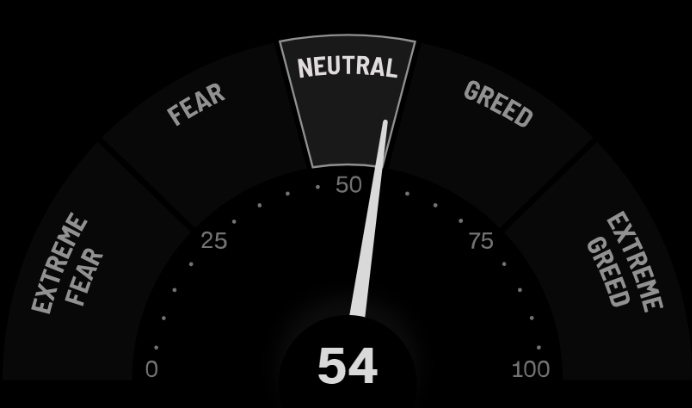

CHART RIGHT TOP: Greed-Fear Index gradually moving higher.

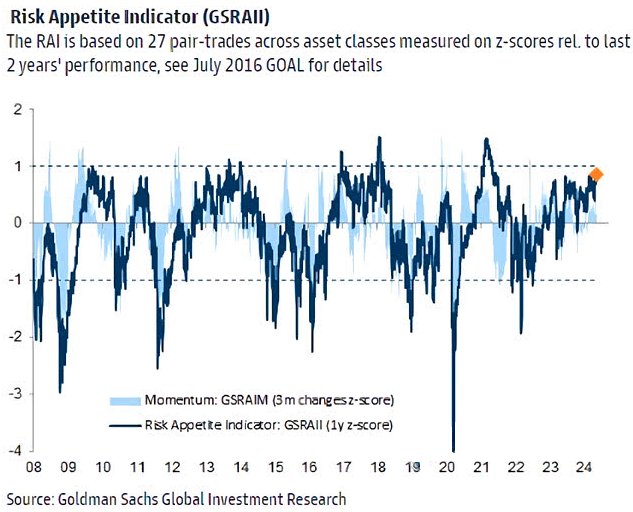

CHART RIGHT BOTTOM:

Goldman Sachs' Risk Appetite Indicator (GSRAII Index) is back to elevated levels.

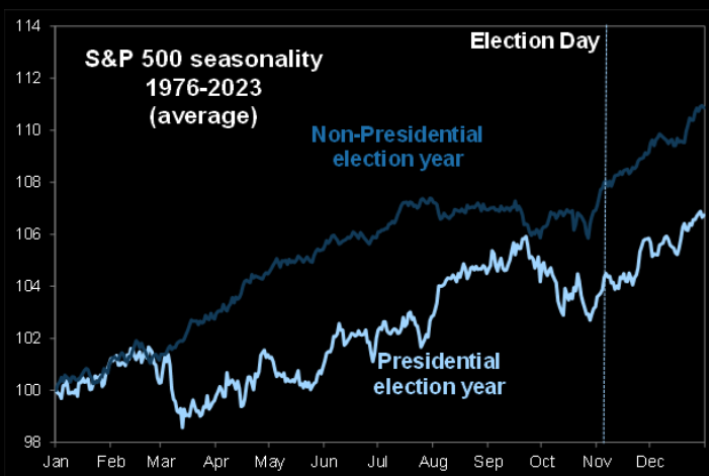

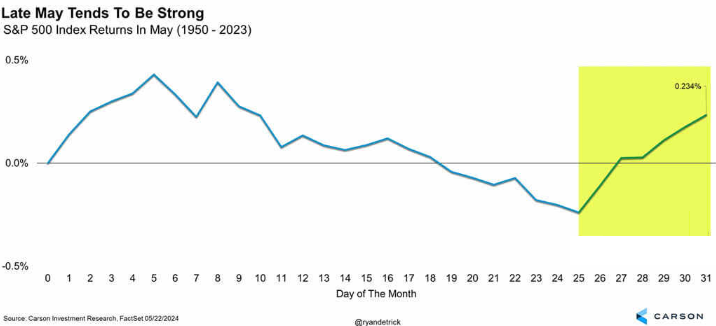

CHARTS BELOW: Election Year & MAY Seasonality.

| | |

| |

|

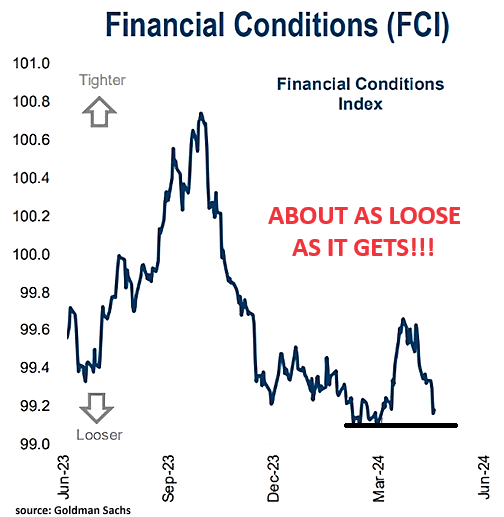

FINANCIAL CONDITIONS ARE FULL THROTTLE OPEN!

CHART RIGHT: Financial Conditions, as reported by Goldman Sachs over the last year, show already Loose Financial Conditions are again being loosened to as low a level as it gets - Must be an Election Year?

The FOMC Minutes on Wednesday showed some Fed members feared that despite a 'restrictive' monetary policy, financial conditions were too easy.

| |

|

|

"AS GO THE BANKS, SO GO THE MARKETS"

MATASII BANKING STOCK INDEX

- Bank stocks retreated on NVDA Earnings finding initial support at the prior Double Top.

- Momentum (bottom pane) also fell off with firmer support slightly lower.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

2 - FUNDAMENTAL ANALYSIS

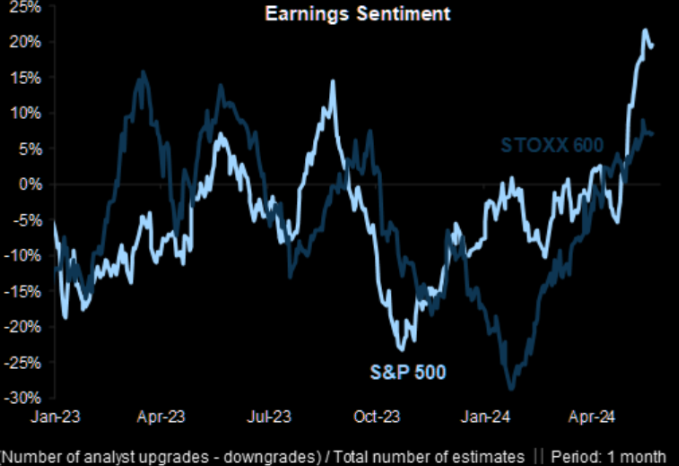

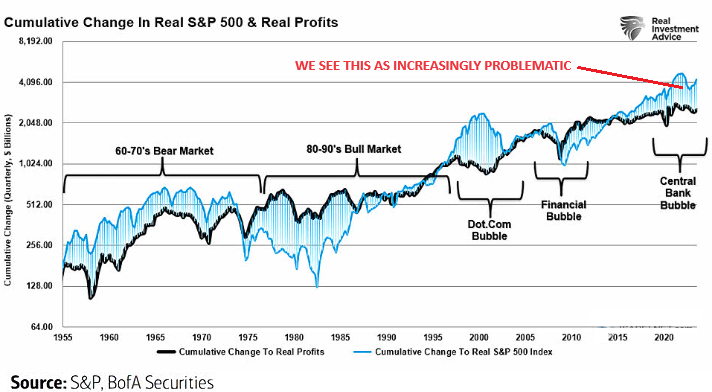

This earnings revisions metrics for S&P500 looks very strong (chart right).

Global EPS revisions have improved over the past couple of months, recording fewer EPS downgrades. The 3-month net revisions sit at -4.5%, up from -8.2% at the end of Q1.

The recent improvement in earnings seems to be driven by a sharp rise in sales expectations. A rising top line is the key to maintaining the uptrend in the profit cycle.

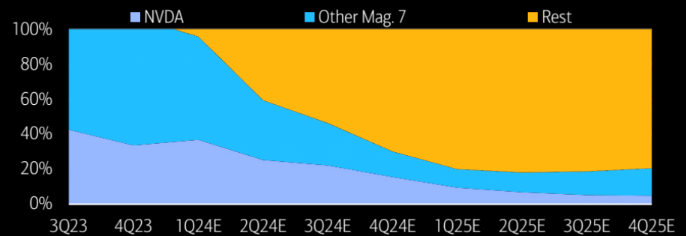

GROWTH IS BROADENING OUT - The chart below shows % contribution of S&P 500 earnings growth Y-o-Y (3Q23 - 4Q25E). This was Nasdaq's best week relative to Russell 2000 since Nov 2023.

| |

|

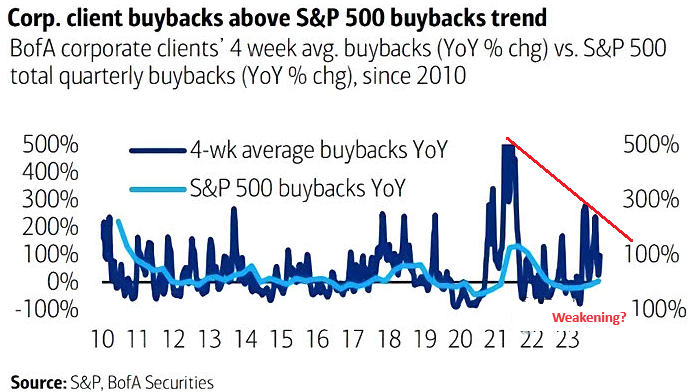

CORPORATE STOCK BUYBACKS

Jamie Dimon, CEO of JPMorgan Chase advised the markets that JPM stock was too expensive at this time and therefore JPM would refrain from further Buybacks until a better price was available. I am sure he is not the only CEO making the same decision?

Corporate Buybacks & Nvidia have been the drivers of the markets and both are showing the possibilities of slowing.

| |

|

MARKET DRIVERS

GLOBAL MARKETS HAVE FALLEN ON NVDA'S BLOWOUT EARNINGS BEAT

As goes NVDA, so goes the MAG-7 - As Goes Mag-7 so goes The Market

| |

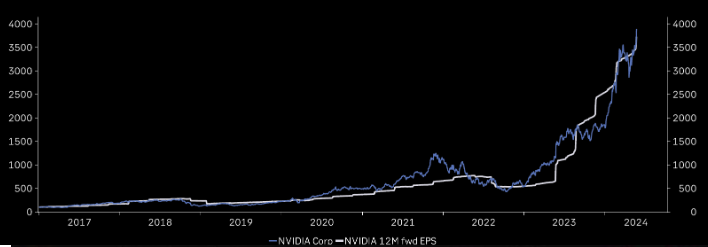

NVDA - Daily

CHART RIGHT: "NVIDIALANDIA" - Where Price and EPS are the two best friends.

MARK-TO MARKET AT ITS FINEST!

To generate 80% gross margins on 75% market share is awe inspiring. Just consider this the ultimate example of mark-to-market. When NVDA made a cycle low in October of 2022, the company had $280bn of market cap and a forward P/E of 25; today, it has $2.5tr of market cap and a forward P/E of 31. Along that 18- month path, their earnings (and free cash flow) grew roughly 10-fold.

The magnitude of all this invites a fair question of sustainability, I haven't seen anything like it even during the Dotcom Bubble!.

DOES THE MARKET NOW FINALLY BELIEVE NVIDIA HAS GONE TOO FAR, TOO FAST???

- 5 years ago, Nvidia had a market cap of just $100 billion. It is now the 3rd largest public company in the world and 17% away from being larger than Apple.

- Nvidia is now larger than Tesla and Amazon combined

- Nvidia is now larger than the entire German stock market.

- At $2.6 trillion, Nvidia's market cap is now $890 billion higher than all of the companies in the S&P 500 Energy sector combined. The total net income of the Energy sector is $128 billion vs. $43 billion for Nvidia.

- Nvidia's share of the Data Center Compute market has grown from ~15% five years ago to ~80% today.

- NVDA has opened up yet another Unfilled Earnings Gap higher.

- At some point the major unfilled gaps must be filled. NVDA therefore may no longer be a long term hold put rather a position trading stock as others entering the space and force margins to contract.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

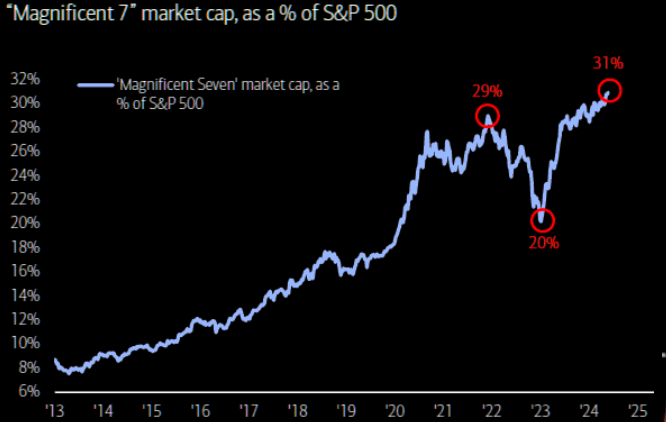

MAGNIFICENT 7

Magnificent 7 is up a magnificent 24% YTD (chart right), contributing >50% of SPX return (NVDA alone = 25%) as monopolistic mega tech monopolizes performance..

Total CAPEX + R&D for the Magnificent Seven this year is expected to total $348bn, (think about that for a second).

Here’s another way to frame it: the Magnificent 7 is reinvesting 61% of their operating free cash flow back into

CAPEX + R&D!

- The basket of 'Magnificent 7' stocks rallied for the fifth straight week to a new record high (obviously helped generously by NVDA).

- We are concerned about the momentum Divergence (bottom pane). When momentum potentially reaches the overhead momentum (slightly higher) a significant drop often follows. Caution advised.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

"CURRENCY" MARKET (Currency, Gold, Black Gold (Oil) & Bitcoin) | |

|

10Y REAL YIELD RATE (TIPS)

Real Rates reached our initial overhead resistance level of 2.25% before falling off hard (Chart Right).

TRADING RANGE: Equity markets reacted

to labor market pressures associated with a weakening Jobs Report (last Friday).

We expected yields & rates to test the lower trend line (chart above right) as we wait on NVDA Earnings potentially changing equity risk premiums.

CONTROL PACKAGE

There are TEN charts we have outlined in prior chart packages, which we will continue to watch closely as a CURRENT Control Set:

-

US DOLLAR -DXY - MONTHLY (CHART LINK)

-

US DOLLAR - DXY - DAILY (CHART LINK)

-

GOLD - DAILY (CHART LINK)

-

GOLD cfd's - DAILY (CHART LINK)

-

GOLD - Integrated - Barrick Gold (CHART LINK)

-

SILVER - DAILY (CHART LINK)

-

OIL - XLE - MONTHLY (CHART LINK)

-

OIL - WTIC - MONTHLY - (CHART LINK)

-

BITCOIN - BTCUSD - WEEKLY (CHART LINK)

-

10y TIPS - Real Rates - Daily (CHART LINK)

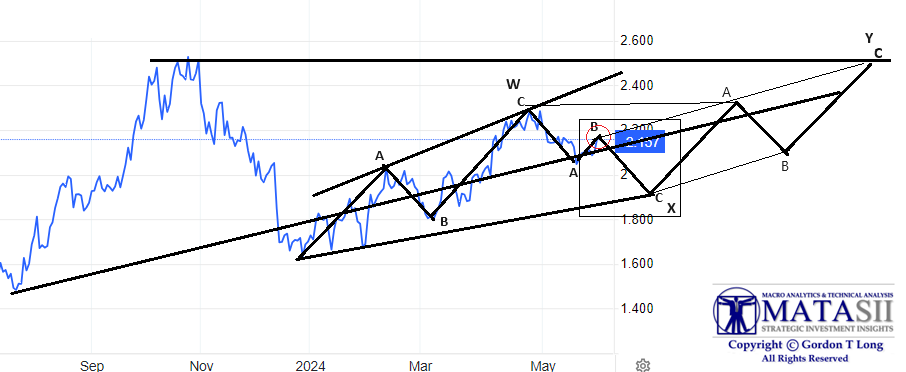

GOLD - cfd - DAILY

- Gold Bullion's worst week in 8 months (since Sept 2023)

- The Gold cfd has fallen further since the NVDA earnings release.

- The Elliott Wave count suggests a minimum 23.6& retracement with the likelihood retracement of 38.2% and support at the 100 DMA.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

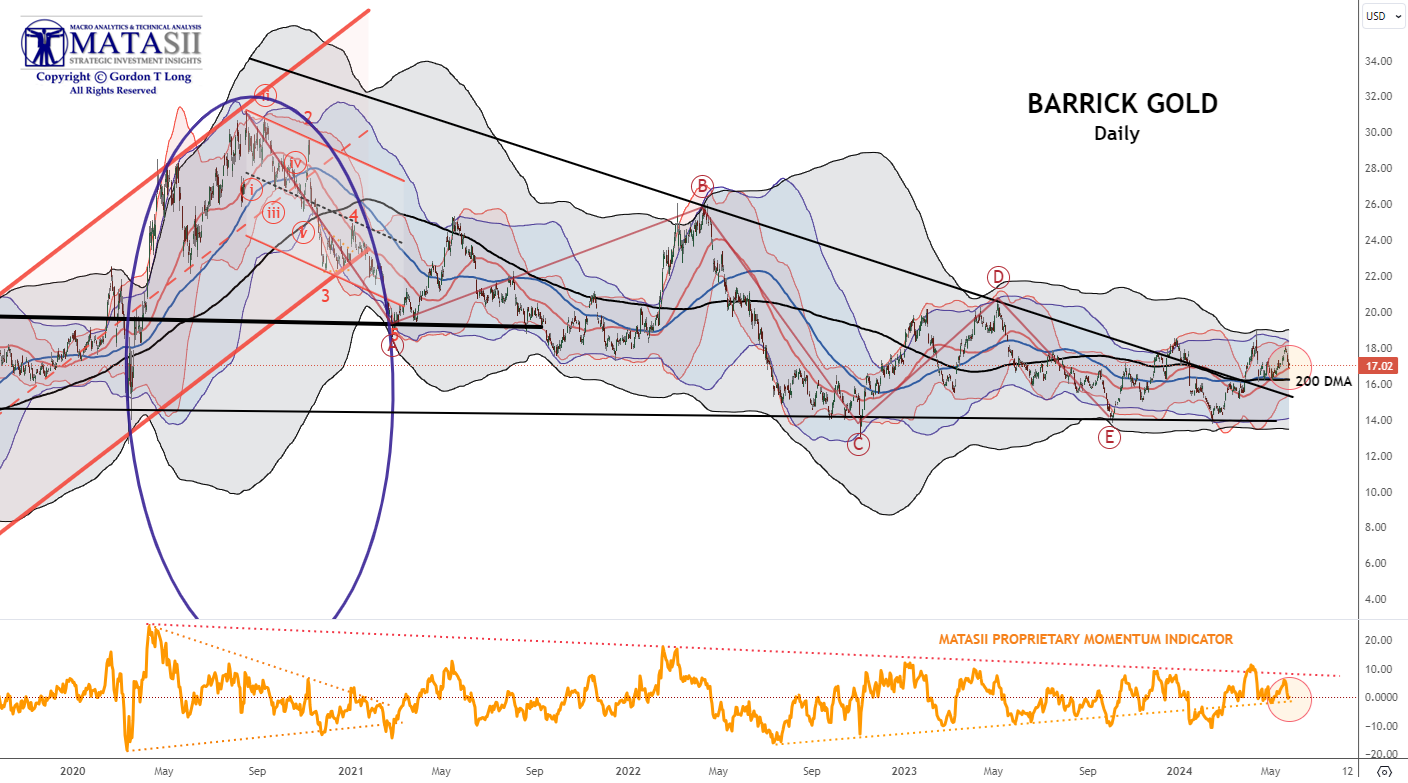

GOLD - INTEGRATED MINERS

Barrick Gold - Daily

Gold stocks have abnormally lagged the gold price - normally gold stocks have a beta of 2X to the gold price. This implies gold miners could be up 45% from current prices. The chase may soon be on?

- Barrick Gold has fallen since the NVDA earnings release finding support at the 50 DMA.

- Barrick Gold also found support at it support trend line (lower pane).

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

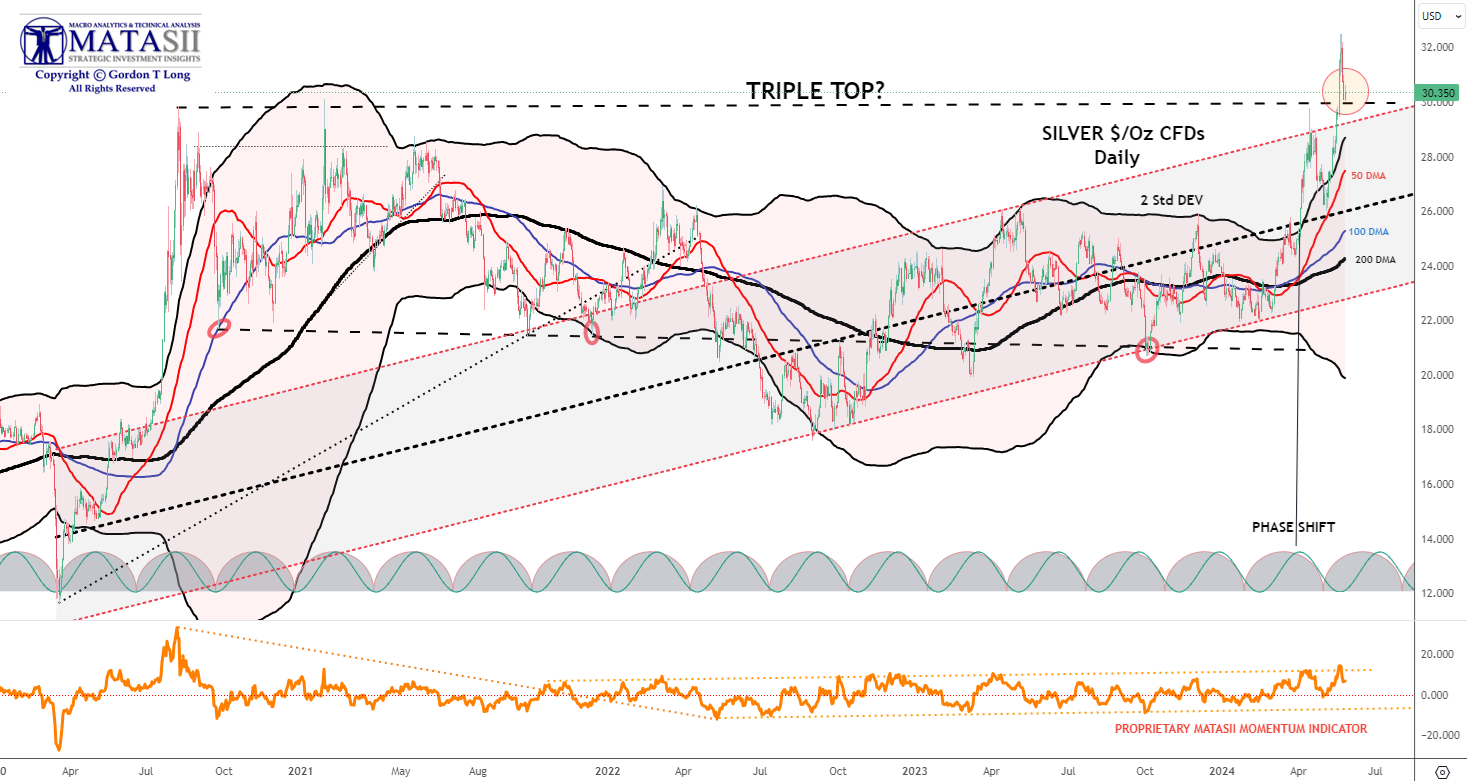

SILVER - Daily

- Silver was down on the week but outperformed gold, holding above $30.

-

Silver has fallen since the NVDA earnings release finding support at its prior Triple Top.

- Silver found overhead resistance at its longer term momentum trend line (lower pane).

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

CHART RIGHT: We have seen bears throw in the towel lately, but what if this is just another overshoot? We have seen similar setups play out before. Believe it or not, but this is the biggest down candle for the SPX since April 30th.

CONTROL PACKAGE

There are FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set":

-

The S&P 500 (CHART LINK)

-

The DJIA (CHART LINK)

-

The Russell 2000 through the IWM ETF (CHART LINK),

-

The MAGNIFICENT SEVEN (CHART ABOVE WITH MATASII CROSS - LINK)

-

Nvidia (NVDA) (CHART LINK)

| |

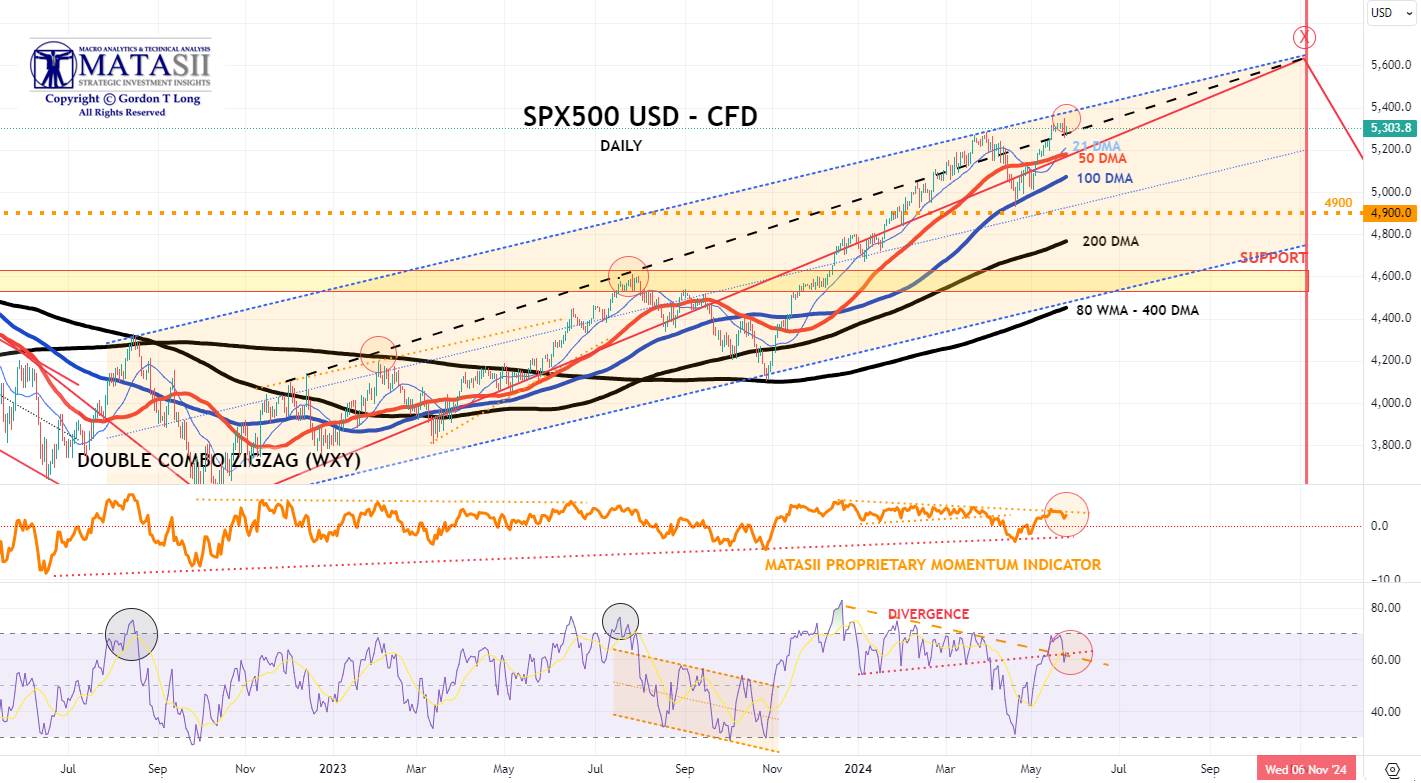

S&P 500 CFD

- The S&P 500 cfd has barely moved all week holding tight to a rising trend line (dashed black line) and putting in a new high.

- The S&P 500 cfd to however see weakness in its RSI level (lower pane). We have been concerned about the Divergence for some time and this is likely to be the beginning of further weakness to lower levels on the RSI.

- MATASII Proprietary Momentum Indicator (middle pane) appears to be showing signs of weakening.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

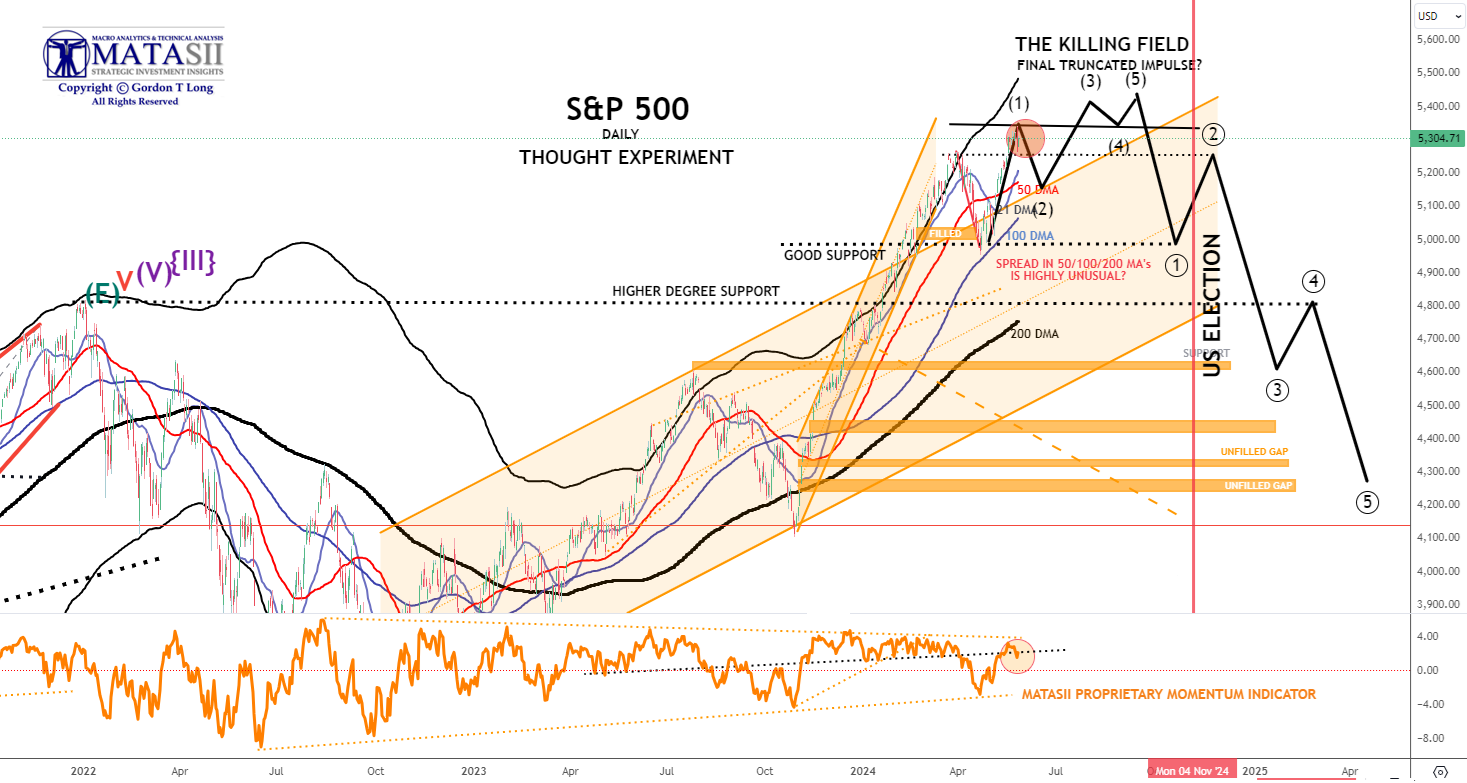

S&P 500 - Daily - Our Thought Experiment

Our Thought Experiment, which we have discussed many times previously in the way of a projection, suggests we have put in a near term top and will now consolidate before possibly completing one final small impulse higher OR put in a final Wave 5 of a higher degree.

NOTE: To reiterate what I previously wrote - "the black labeled activity shown below, between now and July, looks like a "Killing Field" where the algos take Day Traders, "Dip Buyers", the "Gamma Guys" and FOMO's all out on stretchers!"

- Like the S&P 500 cfd, the S&P 500 has barely moved all week but did put in a new top.

- MATASII Proprietary Momentum Indicator appears to be showing signs of weakening (lower pane).

OUR CURRENT ASSESSMENT IS THAT THE INTERMEDIATE TERM IS LIKELY TO LOOK LIKE THE FOLLOWING: (NOTE - The black projection has not been changed since prior posts so as to serve as a reference.)

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

STOCK MONITOR: What We Spotted

MONDAY

- Markets have been choppy to start the week, albeit in very thin news flow, as participants await the key risk events such as FOMC Minutes, Nvidia (NVDA) earnings, and UK inflation data on Wednesday followed by US PMIs on Thursday.

- US indices ended the day mixed (SPX flat, RUT +0.4%, DJIA -0.5%) with the Nasdaq 100 (+0.7%) outperforming and seeing tailwinds from Nvidia (+2.5%) ahead of earnings on Wednesday, whereby it had a couple of PT raises at different brokerages.

- Sectors are mixed – Tech is outperforming and Financials are the laggard, weighed on by JPMorgan (JPM) (-4.5%) after CEO Dimon said the bank is not going to engage in buybacks at these prices, and also noted the succession timetable is no longer five years anymore, indicating it could be less.

- The Dollar is flat and within tight parameters as Antipodeans and the Yen lag, with the latter's cross hitting a peak of 156.30.

- The crude complex was choppy, but settled lower amid no geopolitical escalation and no indication of any foul play in Iranian President death.

- Spot gold and copper hit ATHs, although now sit of best levels.

- Treasuries were lower and curve steepened in catalyst light trade ahead of the week’s aforementioned major risk event.

INFLATION BREAKEVENS: 5yr BEI +0.7bps at 2.343%, 10yr BEI +0.7bps at 2.341%, 30yr BEI +1.0bps at 2.346%.

REAL RATES: 10Y -- 2.135%

STOCK SPECIFIC

- JPMorgan (JPM) -4.5%: Pared all pre-market gains as ahead of its investor day, it lifted FY NII guidance; CEO Dimon said they're not going to engage in buybacks at these prices and noted the succession timetable is not five years anymore, indicating it could be less.

- Apple (AAPL) +0.5%: Reportedly slashed iPhone prices in China amid Huawei competition.

- Nvidia (NVDA) +2.5%: Ahead of earnings on Wednesday, Baird, Barclays, and Stifel raised PT of the Co.

- Microsoft (MSFT) +1%: Announced new category of AI-focused computers; CEO said it has introduced copilot plus PCs.

- Paramount (PARA) flat: Sony and Apollo have taken a key step in bid for Paramount’s assets, according to NY Times. Two Cos. have signed NDA with Paramount, allowing them to look at Paramount’s nonpublic financial information.

- Li Auto (LI) -13%: Revenue and vehicle deliveries missed, with Q2 guidance light.

- Target (TGT) -2%: Will lower prices on approx. 5,000 frequently shopped items.

- Johnson Controls (JCI) +2.5%: Activist investor Elliott has built a position with the stake worth more than USD 1bln.

- Micron (MU) +3%: Upgraded at Morgan Stanley; said it overestimated how much significant 2023 losses would weigh on the stock's valuation, and underestimated both the economic and narrative elements of AI memory.

- Norwegian Cruise Line (NCLH) +7.5%: Boosts FY adj. EPS guidance on strong demand and bookings.

- Hims & Hers (HIMS) +27.5%: Announced the addition of GLP-1 injections to its comprehensive weight loss portfolio, giving customers an affordable way to consistently access safe, high-quality weight loss treatment.

TUESDAY

- US indices were little changed on Tuesday (SPX +0.2%, NDX +0.1%, DJIA +0.2%, RUT -0.2%) with sectors mixed; Nvidia (NVDA) (+0.4%) saw marginal upside ahead of earnings of Wednesday.

- In FX, the Dollar Index was flat and within very tight ranges as CAD and NZD underperforming, with the former after cooler-than-expected inflation data, with the latter awaiting RBNZ overnight.

- The crude complex was slightly lower, albeit off session lows, amid little geopolitical escalation and ahead of private inventory data after-hours. Treasuries were slightly firmer in choppy trade, as initially saw some spillover strength from Canadian CPI, before two-way action on Fed’s Waller.

- Waller stuck to his line from March that "several more months of good inflation data" is still needed to support an easing in policy despite the recent CPI data, while he noted a further increases in policy rate probably unnecessary.

- While markets have been treading water in the first couple of days this week, the risk events come thick and fast on

- Wednesday, beginning with UK inflation and concluding with Nvidia earnings, with FOMC Minutes and US 20yr auction sandwiched in the middle.

INFLATION BREAKEVENS: 5yr BEI -0.5bps at 2.344%, 10yr BEI -0.2bps at 2.341%, 30yr BEI -0.6bps at 2.341%.

REAL RATES: 10Y -- 2.157%

STOCK SPECIFIC

- Zoom (ZM) -0.4%: Next quarter profit guidance was light.

- Keysight Technologies (KEYS) -8.4%: Next quarter outlook disappointed.

- Lam Research (LRCX) +2.4%: Announced 10-for-1 stock split and a USD 10bln share repurchase plan.

- Xpeng (XPEV) +5.9%: Shallower loss per share and revenue beat; sees next quarter deliveries rising 25-37.9% Y/Y.

- JD.Com (JD) -4.2%: Announced proposed offering of USD 1.5bln convertible senior notes.

- Macy’s (M) +5.1%: Profit beat, with outlook for both Q2 and FY impressing. Revenue missed and SSS surprisingly declined.

- AutoZone (AZO) -3.6%: Revenue and comp. sales fell short.

- Nordson (NDSN) -8.4%: Disappointing next quarter outlook and cut FY24 profit view.

- Micron (MU) -1.2%: Raised FY24 CapEx view to around USD 8bln from 7bln.

- Eli Lilly (LLY) +2.6%: Positive Crohn’s disease data and China approved its GLP-1 drug to treat diabetes.

- Amazon (AMZN) -0.2%, Nvidia (NVDA) +0.6%: AMZN halted orders of NVDA ‘superchip’ to await updated model, according to the FT. NVDA’s earnings are to be released after close on Wednesday.

- Intel (INTC) -1.1%: In collaboration with Microsoft (MSFT) to enable several PHI-3 models across its data center platforms and its AI PCs and edge solutions

- GE Aerospace (GE) +1.1%: Announced it will hire 900 engineers this year.

WEDNESDAY

- US indices were lower on Thursday, with underperformance in the small-cap Russell 2000 as traders await the pivotal Nvidia earnings after-hours.

- The Dollar was flat for the majority of the session, but saw gains into the close to print a high of 104.970, which saw most G10 peers see losses vs. the Buck and resulted in the NZD wiping out all of its post-RBNZ gains.

- As a brief recap, it was a hawkish RBNZ hold, as it kept the OCR unchanged at 5.50%, as expected, but noted that monetary policy needs to be restricted, raised OCR projections, and the Minutes revealed the committee discussed the possibility of increasing the OCR at this meeting.

- UK CPI was hotter-than-expected and has pushed out the first fully priced cut to November (vs. Sept. pre-release). Treasuries saw weakness on account of the aforementioned UK inflation metrics, albeit not as large as European peers, and the US 20yr auction had little sway.

- The dated FOMC Minutes added little new, and largely echoed what Fed officials have recently said with attention now turning to Flash PMIs (Thurs), Prelim UoM (Fri), ahead of Core PCE on May 31st.

- The crude complex saw further weakness with a continuation of the recent trend, amid a lack of notable geopolitical developments, as gains in wake of the not as large as expected crude EIA build swiftly pared. Lastly, copper and spot gold gave back some of the gains from recent ATHs

INFLATION BREAKEVENS: 5yr BEI -0.4bps at 2.340%, 10yr BEI -0.1bps at 2.339%, 30yr BEI -0.3bps at 2.339%.

REAL RATES: 10Y -- 2.144%

STOCK SPECIFIC

- Target (TGT) -8%: Earnings missed as it was driven by a Y/Y sales decline of about 3% as consumers bought fewer discretionary items.

- Analog Devices (ADI) +10.9%: Top and bottom-line beat, alongside better-than-expected next quarter.

- Amazon (AMZN) flat: AWS is to invest EUR 15.7bln in data centers in Spain.

- Lululemon (LULU) -7.2%: Will implement a new integrated design structure and announced the departure of its chief product officer.

- PDD (PDD) +1.1%: EPS and revenue surpassed expectations - powered by strong adoption of its international shopping site, Temu, and as it attracted more price-conscious customers.

- TJX Companies (TJX) +3.5%: EPS topped alongside raising FY25 outlook for pre-tax profit margin and profit.

- Shopify (SHOP) +3%: Upgraded at GS; said its shares are at an attractive entry point following a rough year to date.

- Sysco (SYY) -3.4%: Missed on long term EPS growth

- Boeing (BA) +0.1%: Saw weakness after Reuters sources reported that its planes deliveries to China have been delayed in recent weeks.

THURSDAY

- The morning upside in equity futures had completely faded, and more, by the time of market close with upside in yields seen in wake of the hot services PMI data supporting the Dollar and hitting stocks.

- The selling pressure in equities accelerated once Europe had packed up for the day with little fresh fundamentals driving the move lower. However, it is worth noting we are heading into a long weekend and month-end next week given the US and UK market holiday on the 27th May, which perhaps could see some early month-end rebalancing after the pronounced May upside so far.

- The only sector to close in the green on Thursday was tech, largely buoyed by Nvidia (NVDA) which closed +9% after a strong earnings report Wednesday night, which initially boosted other semis but by the close the SOXX ETF closed in the red.

- Note, the equal weighted SPX (RSP) closed lower by 1.4%. T-Notes bear flattened after the hot US PMI data which was buoyed by the stellar Services PMI, which came in above all analyst forecasts.

- The data also gave a helping hand to the Dollar from lows seen in the morning after strong German and EZ PMI data.

- Elsewhere on US data, jobless claims fell by more than expected but did little to change the narrative, while New Home Sales disappointed, but also sparked little reaction.

- Oil prices also gave up their gains after the US PMIs, with a firmer Dollar and downbeat risk tone weighing. Gold prices also slumped throughout the session.

- There was little fresh on Fed speak other than Fed's Bostic who reiterated familiar language with attention turning to UoM Final data in May after the prelim survey saw upside moves in the inflation expectations.

- US Durable Goods are also released on Friday, with commentary from Fed's Waller the Fed speak highlight. Elsewhere, Japan's CPI overnight and UK Retail Sales in the morning will be of note.

INFLATION BREAKEVENS: 5yr BEI -1.7bps at 2.329%, 10yr BEI -2.0bps at 2.326%, 30yr BEI -2.0bps at 2.322%.

REAL RATES: 10Y -- 2.171%

STOCK SPECIFIC

- Nvidia (NVDA) +9%: EPS and revenue beat w/ strong data center revenue. Announced a 10-for-1 stock split, raised cash dividend 150%, and impressive commentary surrounding the Hopper-Blackwell transition.

- VF Corp (VFC) -3%: Posted a surprise loss per share and top line missed, alongside noting revenue will remain challenged in the near term.

- DuPont (DD) +0.5%: Will divide into three separate businesses; CEO plans to step down to become executive chair of the board on June 1st.

- Live Nation (LYV) -8%: US DoJ is to seek a breakup of Live Nation-Ticketmaster.

- TSMC (TSM) +0.6%: Sees more than 10% semiconductor industry growth this year excluding memory chips, and foundry business growing 15-20%.

- GlobalFoundries (GFS) -8.5%: Announced pricing of USD 950mln secondary offering of ordinary shares at USD 50.75/shr. Note, closed Wednesday at USD 55.21/shr

- News Corp (NWSA) flat: Signs a landmark multi-year global partnership with OpenAI.

- E.l.f. Beauty (ELF) +19%: Top and bottom line surpassed expectations.

- Cytokinetics (CYTK) -17%: Announced a USD 500mln common stock offering.

- Morgan Stanley (MS) -1.8%: Gorman will step down as chairman on Dec 31st, according to Bloomberg.

- Boeing (BA) -7.5%: CFO confirmed Reuters reports on delayed plane deliveries to China due to Chinese regulatory reviews. Boeing (BA) now expects negative free cash flow in 2024, vs March estimate for the low single-digit billions.

- Comerica (CMA) -5.5%: The OCC announces enforcement action against Comerica; said it has found unsafe or unsound practices, including those relating to the bank's risk governance framework and internal controls.

FRIDAY

- Stocks closed green on Friday with outperformance in the Nasdaq with sectoral gains most seen in Communication and Tech names although most sectors closed green (ex health care) with broad-based gains (equal-weighted SPX +0.7%).

- Stocks generally were bid throughout the US afternoon with a rally ensuing from the better-than-expected UoM data which saw inflation expectations ease from the sharp gains seen in the prelim survey.

- Elsewhere, T-Notes were flat across the curve but with a slightly flatter bias.

- Note that Fed Governor Waller spoke on R*, noting he has not changed his view that the neutral rate is relatively low.

- The Dollar was lower in wake of the UoM data while the stronger-than-expected Durable Goods data ultimately had little impact.

- The Yen was flat vs the softer Dollar following mixed inflation data overnight and fresh jawboning from officials after USD/JPY rose above 157.00 on Thursday.

- The CAD outperformed on the weaker Buck, risk environment and higher oil prices, despite weak retail sales data.

- The upside in crude prices was buoyed by the aforementioned Greenback selling but it was not enough to pare the crude weakness seen throughout the week.

- Note that next week, US and UK markets are shut on Monday on account of Memorial Day in the US and Spring Bank holiday in the UK.

- However, it is an action packed week with focus on the US Core PCE data, the 2nd estimate of US GDP, and a plethora of Fed speak.

INFLATION BREAKEVENS: 5yr BEI +0.6bps at 2.337%, 10yr BEI +0.4bps at 2.330%, 30yr BEI +0.2bps at 2.324%

REAL RATES: 10Y -- 2.155%

STOCK SPECIFIC

- Nvidia (NVDA) +2.5%: Cuts China prices as it competes with Huawei.

- Intuit (INTU) -8.5%: Next quarter profit guidance was light. Although, earnings beat, with FY outlook surpassing expectations.

- Workday (WDAY) -15.5%: Cut FY25 subscription revenue outlook.

- Tesla (TSLA) +3%: To cut Model Y output at Shanghai plant by at least 20% during March-June 2024, according to Reuters citing sources.

- Eli Lilly (LLY) flat: Is to spend USD 5.3bln to make more Mounjaro and Zepbound, according to WSJ; sees new site to start making medicines near end 2026. CEO says they are delaying ex- US GLP1 drugs until supply improves.

- Ross Stores (ROST) +8%: Top and bottom line beat alongside raising FY profit view.

- Deckers Outdoors (DECK) +14%: EPS and revenue surpassed expectations.

- Guardant Health (GH) +13.5%: Resumed trading after the stock was halted since close on 22nd May. This morning, FDA AdCom recommends approval of Guardant Health's Shield blood test.

- Stericycle (SRCL) +15.5%: Reportedly weighing sale after getting takeover interest, according to Bloomberg.

| |

CONTROL PACKAGE

There have FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set":

- The 10Y TREASURY NOTE YIELD - TNX - HOURLY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - DAILY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - WEEKLY (CHART LINK)

- The 30Y TREASURY BOND YIELD - TNX - WEEKLY (CHART LINK)

- REAL RATES (CHART LINK)

FISHER'S EQUATION = 10Y Yield = 10Y INFLATION BE% +REAL % = 2.33% + 2.155% = 4.488%

10Y UST - TNX - DAILY

- The TNX rose this week to above its descending 144 EMA.

- It appears to have found potential near term overhead resistance offered by a long term falling trend channel.

- We see more weakness as the 10 Year Real Rate falls further even if inflation break-evens were to rise.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

10Y UST - TNX - WEEKLY

- The TNX (NASDAQ) rose this week to its descending 144 EMA.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond ‘fair use’, you must obtain permission from the copyright owner.

========

| |

MATASII'S STRATEGIC INVESTMENT INSIGHTS | |

2020 VIDEOS OUTLINING THE COMING RISE IN INFLATION, STAGLFLATION & COMMODITY PRICES | |

|

THE REGULATORY STATE

RELEASED - 01-17-24 --- 212 Page Paper

FULL 212 PAGE PDF DOWNLOAD

| |

IDENTIFICATION OF HIGH PROBABILITY TARGET ZONES | |

Learn the HPTZ Methodology!

Identify areas of High Probability for market movements

Set up your charts with accurate Market Road Maps

Available at Amazon.com

| |

The Most Insightful Macro Analytics On The Web | | | | |