|

Gordon T Long Research exclusively distributed at MATASII.com

Subscribe to Gordon T Long Research - $35 / Month - LINK

Complete MATASII.com Offerings - $55/Month - LINK

SEND YOUR INSIGHTFUL COMMENTS - WE READ THEM ALL - lcmgroupe2@comcast.net

| |

|

LONGWave - JULY 2024

Technical Analysis - 08/05/24

| |

A LOOMING JAPANESE FIRESALE OF US TREASURIES?

Profligate government spending has institutionalized multitrillion-dollar annual deficits, which have driven up interest rates and left Treasury markets teetering on the edge. Now Japan is on the verge of a $400 billion fire sale of U.S. debt. This could break the back of the Treasury market and devastate Americans’ finances.

The source of Japan’s sudden need for liquidity is the state-owned Government Pension Investment Fund, which holds the social security reserves of nearly every Japanese worker.

Because the government wants to prop up the plunging yen, it intends to sell the American assets and buy Japanese ones.

The amounts here aren’t trivial: the fund is more than $1.5 trillion, of which $400 billion is U.S. Treasuries. This conversion from dollar-denominated assets to yen-denominated ones means dumping a quantity of Treasuries on the market equal to about 20% of the federal government’s net annual borrowing.

A 20% increase in the supply of Treasuries is huge when yields are already around 5% and poised to go higher. Higher yields increase how much interest must be paid to service our $35 trillion federal debt.

Last month, the Treasury Department spent a record $140 billion just on interest to keep its debt scheme going. For perspective, that amounts to more than three-quarters of personal income tax revenue collected in June - for interest alone.

If Japan starts unloading its U.S. Treasuries, that exacerbates the problem: increasing the supply of Treasuries makes it harder for the U.S. government to sell new ones and finance the massive budget deficit. The only way to entice more people to buy Treasuries will be to offer higher interest rates, which will cause the interest on the debt to climb even faster, heading to $2 trillion annually and beyond.

Many countries, such as Russia, have already sold off all their Treasuries. China, the second-largest foreign holder of U.S. debt, is selling them hand-over-fist, having sold one-third in the past five years. If the largest holder, Japan, has a fire sale in this environment, it would be the equivalent of a margin call on the U.S. Treasury Department—the moment the bank tells you to cough up more cash or they cut you off.

People the world over are losing confidence in the federal government’s ability to repay its debts and no longer see the dollar as a secure asset. In just 3½ years, the dollar has lost one-fifth of its value, wiping out trillions of dollars of bondholders’ wealth around the world.

This kind of backdoor default is why some Japanese banks have already begun liquidating their Treasury holdings, including the country’s fifth-largest bank, Norinchukin, selling $63 billion in Treasuries. ===>

| |

|

VIDEO PREVIEW (click image)

Pay-Per-View Page Link

|  | |

THIS WEEK WE SAW

Exp=Expectations, Rev=Revision, Prev=Previous

US

US Dallas Fed Manufacturing Business Index (Jul) -17.5 (Prev. -15.1)

US ADP National Employment (Jul) 122.0k vs. Exp. 150.0k (Prev. 150.0k, Rev. 155k)

US Pending Sales Change MM (Jun) 4.8% vs. Exp. 1.5% (Prev. -2.1%, Rev. -1.9%)

US Chicago PMI (Jul) 45.3 vs. Exp. 45.0 (Prev. 47.4)

===> The even larger Japan Post Bank has more than $550 billion, mostly U.S. bonds, which could also soon head to the auction block.

The fire sale doesn’t end there. Because Japan’s Government Pension Investment Fund influences all other pensions in Japan, another $800 billion in U.S. assets also might be looking for a new financial home.

Even as almost every Treasury buyer is selling, including the Federal Reserve, the federal government is ramping up borrowing to cover ballooning deficits. Financial markets are staring down the barrel of soaring interest rates and a massive liquidity drain.

If the Treasury gets backed into this corner and is forced to pony up higher yields, then things will unravel fast. We’ll look back fondly at 8% mortgage rates and the limited bank failures of spring 2023, because things will be much worse than that.

Of course, the government could short-circuit this entire collapse by simply cutting spending and getting on a path to fiscal sustainability. After all, margin calls don’t happen if investors believe the investments are still good.

Unfortunately, there’s no sign of such fiscal responsibility in our government.

h/t AJ ANTONI / PS ONGE

| |

========================= | |

|

WHAT YOU NEED TO KNOW!

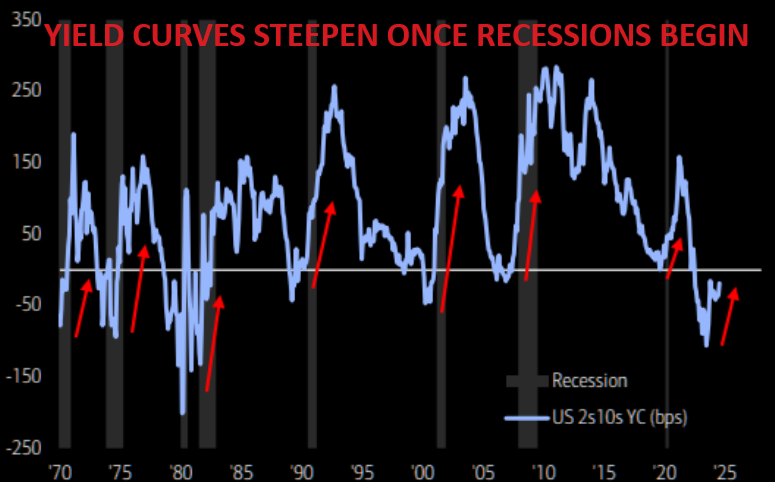

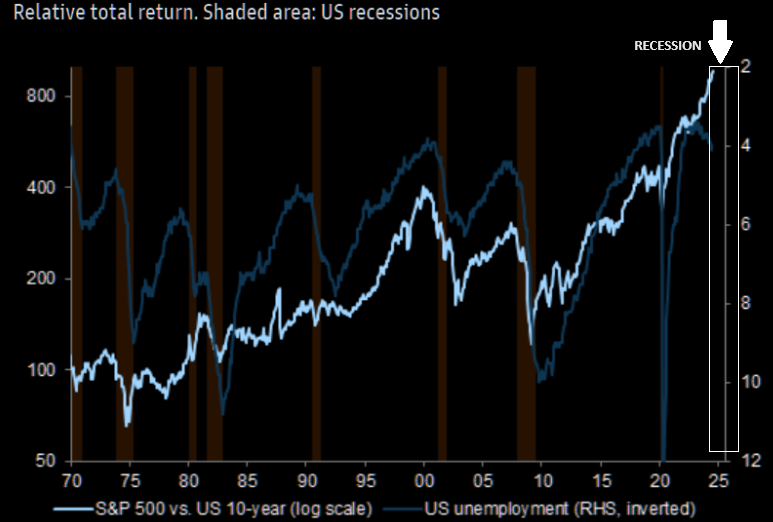

STEEPENING YIELD CURVES DON'T LIE!

Yield Curves don't lie nor are false indicators of pending recessions when they steepen - especially from current low levels and having been inverted this long!! (Red arrows shown on the chart to the right.)

Stock market selling however historically begins when the inversion actually goes positive and the Fed has initiated their first rate cut. Markets historically have risen in anticipation of rate cuts but sell on the fact, because the Fed only cuts on clearly evident deteriorating economic forces it to react. Falling PE begin to be priced in with earnings soon falling.

RESEARCH

1- 2024 Q2 EARNINGS

- When expectations are too high, then investors tend to over-react to any concerns. This is what we continue to see in this earning season. It has become a "Sell" the news.

- Major players announced operating concerns of various degrees. Investors however are immediately reacting by reducing their exposure.

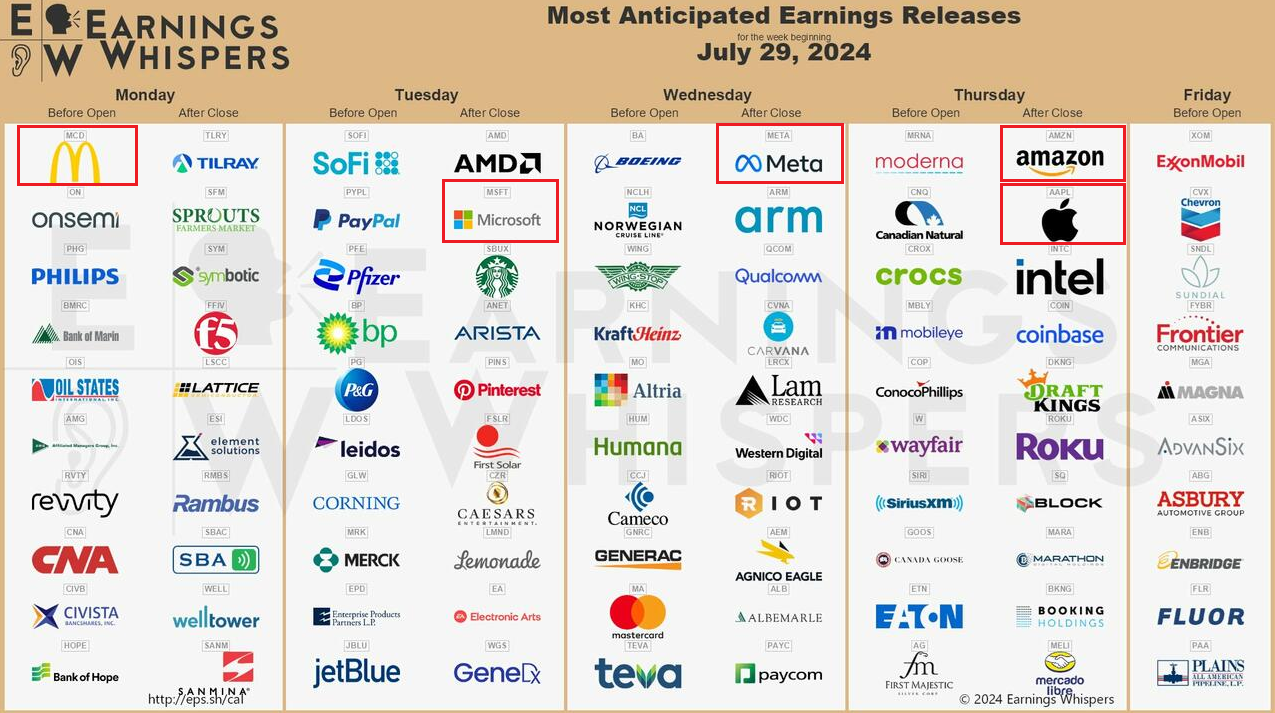

- We examine a few of the major players who have announced their Q2 earnings: McDonalds (Fast Foods), Microsoft (PS Software), Meta (Social Media), Amazon (Online Retail) and Apple (Consumer Electronics).

2- BOJ RAISES RATES & REDUCES JGB BUYING

- BoJ raised its short-term interest rate to 0.25% (prev. 0.00-0.10%).

- BoJ is to reduce scheduled monthly bond buying by around JPY 400bln each quarter and with bond purchases to be JPY 3tln a month as of Q1 2026.

- US rate cuts will shrink rate spread which, along with a strengthening Yen, will place pressures on the viability of the $3.5T Japanese Carry Trade to continue to finance US & EU debt and fiscal deficits.

| |

|

DEVELOPMENTS TO WATCH

US TREASURY: QUARTERLY REFUNDING ANNOUNCEMENT

- Q3 funding needs were revised lower to $740 billion from $847 billion projected last quarter. According to the Treasury, the borrowing estimate was $106 billion lower than announced in April 2024, largely due to lower Federal Reserve System Open Market Account (SOMA) redemptions and a higher beginning-of-quarter cash balance.

- Q4 funding needs are estimated at $565 billion, $115 billion above estimates of $450 billion, which is quite a bit higher than expected, but is also due in part to the higher TGA estimate of $700 billion.

- The Treasury expects to borrow just over $1.3 trillion by year-end.

FOMC - JULY MEETING

- Federal Open Market Committee votes unanimously to leave benchmark rate unchanged in target range of 5.25%-5.5%, a more than two-decade high, for the eighth straight meeting

- Fed also tweaks language to say price pressures remain “somewhat” elevated, and acknowledge “some further progress” toward inflation goal, from “modest further progress” in previous statement

- Officials also adjust their assessment of the labor market, saying job gains “have moderated” and the jobless rate “has moved up but remains low”

| |

|

GLOBAL ECONOMIC REPORTING

JUNE LABOR REPORT - NFP

- The US added just 114K payrolls, a huge miss to expectations of 175K and also a huge drop from the downward revised June print of 206K, now (as always ) revised to just 179K.

- This was the lowest print since December 2020, (at least prior to even more revisions), and a 3 sigma miss to the median estimate of 175K.

- SAHM RULE TRIGGERED = RECESSION

JOLTS, QUITS & HIRES

- While private jobs saw another broad drop in openings across private sectors, this was almost fully offset by the relentless surge in government job openings.

- Private sector job openings plunged to a level seen back in late 2018. Government job openings are just shy of a record high!

CONSUMER CONFIDENCE - Expectations

- The overall trend in the labor market indicator remains weaker.

- Purchase plans for homes, cars, and appliances have all plunged.

| |

|

In this week's "Current Market Perspectives", we focus on the signals that Sentiment, Fundamentals and various markets Segments (Credit, Bond and Equity) are currently giving us.

=========

| |

|

1- Q2 EARNINGS

KEY METRICS

-

Earnings Scorecard: For Q2 2024, (with 75% of S&P 500 companies reporting actual results), 78% of S&P 500 companies have reported a positive EPS surprise and 59% of S&P 500 companies have reported a positive revenue surprise.

-

Earnings Growth: For Q2 2024, the blended (year-over-year) earnings growth rate for the S&P 500 is 11.5%. If 11.5% is the actual growth rate for the quarter, it will mark the highest year-over-year earnings growth rate reported by the index since Q4 2021 (31.4%).

-

Earnings Revisions: On June 30, the estimated (year-over-year) earnings growth rate for the S&P 500 for Q2 2024 was 8.9%. Nine sectors are reporting higher earnings today, (compared to June 30), due to upward revisions to EPS estimates and positive EPS surprises.

-

Earnings Guidance: For Q3 2024, 39 S&P 500 companies have issued negative EPS guidance and 35 S&P 500 companies have issued positive EPS guidance.

-

Valuation: The forward 12-month P/E ratio for the S&P 500 is 20.7. This P/E ratio is above the 5-year average (19.3) and above the 10-year average (17.9).

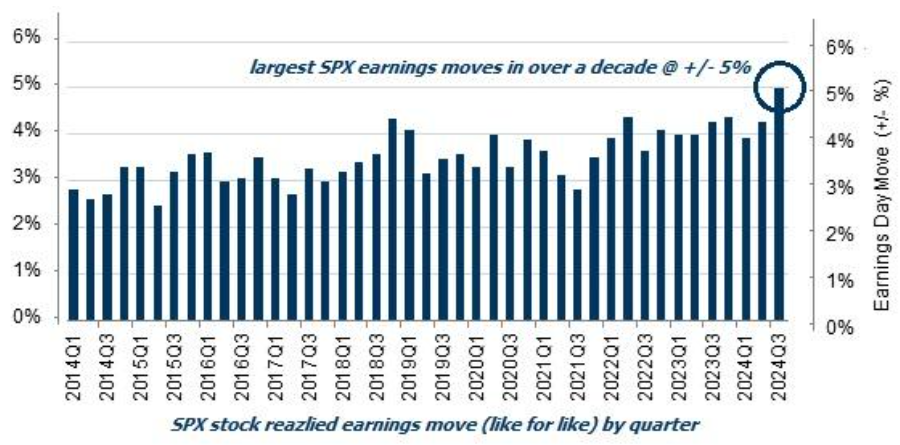

CHART BELOW: Goldman Sachs noted "This has been the most volatile earnings season since the financial crisis!"

| |

|

EVERYONE BEGGING FOR LOWER RATES

CHART RIGHT: Data shows corporate America's interest in the highly anticipated rate-cut cycle has surged to new record highs in earnings calls. From S&P 500 and Stoxx 600 companies, management teams mentioning the words "Federal Reserve" on earnings calls hit a new high on data going back to 2001 this earnings season.

The Fed's interest rate hiking campaign over the last 2.5 years has dented consumer spending and corporate profits, with borrowing costs slowing down the overall economy to tame inflation. While the first rate cut won't meaningfully make a difference for consumers, it will lower borrowing costs for companies big and small.

| |

BANK STOCKS OFTEN SIGNAL WHAT LIES AHEAD! | |

WE HAVE HEARD THE SPIN - NOW "WHERE'S THE MEAT!" | THE SPIN TO SUPPORT HIGH EXPECTATIONS CAN'T HIDE THE PROBLEMS | |

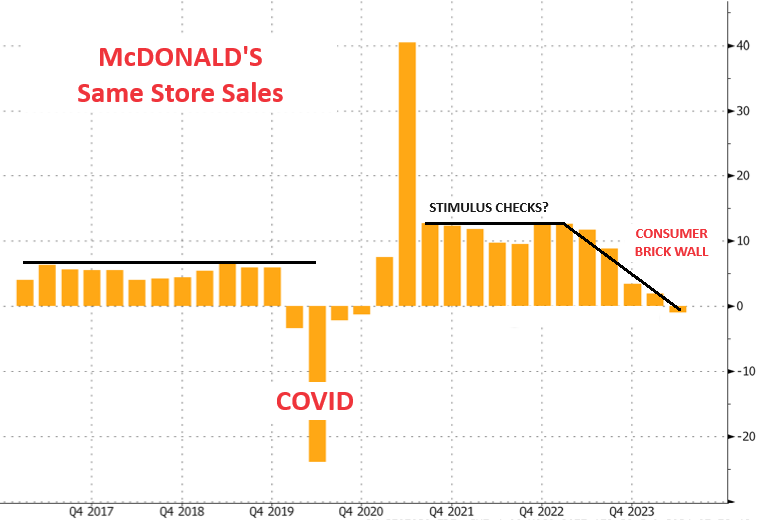

McDONALD'S (Fast Food)

McDonald's reported disappointing Q2 results, missing both the average earnings and revenue expectations tracked by FactSet.

- The largest fast-food chain in the country reported the first quarterly decline in same-store sales since Q4 2020, as sliding Big Mac demand is evident of low and mid-tier consumers being squeezed by elevated inflation and sky-high interest rates produced by failed Bidenomics.

- McDonald's reported adjusted earnings of $2.97 per share for the quarter, down from $3.17 one year ago.

- This missed the average analyst estimate of $3.07 tracked by FactSet. Revenue was flat at around $6.49 billion, falling short of the average analyst estimate of $6.62 billion.

- For the April-June period, sales at burger shops fell 1% worldwide.

- This was the first decline since Q4 2020, when the government-enforced shutdown and panic doom broadcasted by MSM kept everyone out of stores and hiding in their homes. In the US, same-store sales fell about 1%.

Here's a snapshot of the second quarter financial performance (courtesy of MCD).

Global comparable sales decreased 1%, reflecting negative comparable sales across all segments:

- US decreased 0.7%.

- International Operated Markets segment decreased 1.1%.

- International Developmental Licensed Markets segment decreased 1.3%.

- Consolidated revenues were flat (increased 1% in constant currencies).

- Systemwide sales decreased 1% (increased 1% in constant currencies).

- Consolidated operating income decreased 6% (5% in constant currencies). Results included $97 million of pre-tax non-cash impairment charges and $57 million of pre-tax restructuring charges associated with Accelerating the Organization. Excluding these current year charges, as well as prior year pre-tax charges of $18 million, consolidated operating income decreased 2% (was flat in constant currencies).

- Diluted earnings per share was $2.80, a decrease of 11% (10% in constant currencies). Excluding the current year charges described above of $0.17 per share, diluted earnings per share was $2.97, a decrease of 6% (5% in constant currencies) when also excluding prior year charges.

| |

|

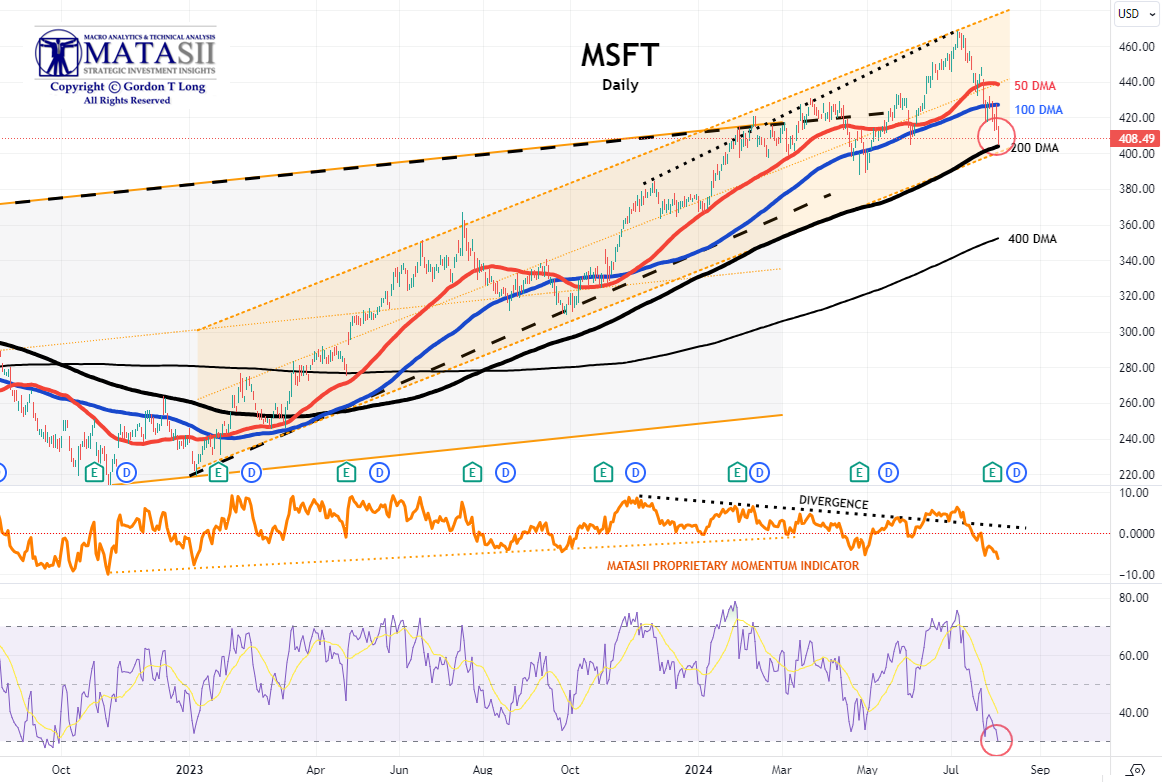

MICROSOFT (PC Software)

- Microsoft Corp (MSFT) Q4 2024 (USD): EPS 2.95 (exp. 2.93), Revenue 64.73bln (exp. 64.39bln), Intelligent Cloud rev. 28.52bln (exp. 28.72bln). Co. shares were lower by 2.7% after-hours.

Despite beating on revenue and EPS, Microsoft missed on Cloud. Investors however are focused on the AI-heavy cloud segment.

Azure posted a 29% revenue gain in the quarter, decelerating from the 31% growth in the previous period, with revenues just missing estimates.

Microsoft has been infusing product line with AI technology from partner OpenAI, including digital assistants called Copilots that can summarize documents and generate computer code, emails and other content. The company also is selling Azure cloud subscriptions featuring OpenAI products. However, judging by the disappointing cloud numbers, chatbots, pardon AI is rapidly emerging as the next "3D TV" megadud.

The stock initially plunged 8% on Tuesday night - or roughly $250 billion in market cap - in after hours trading on the small miss in cloud revenue.

| |

|

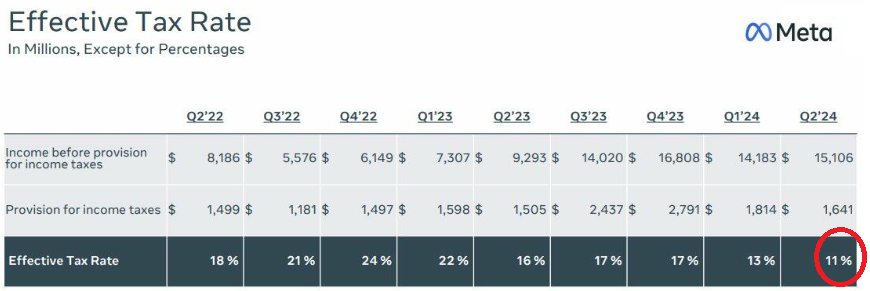

META (Social Media)

The stock jumped after the company beat on sales and earnings despite the all-important for AI CapEx print coming in soft.

- Revenue $39.07 billion, +22% y/y, beating estimates of $38.34 billion

- Advertising rev. $38.33 billion, +22% y/y, beating estimates of $37.57 billion

- Family of Apps revenue $38.72 billion, +22% y/y, beating estimates of $37.76 billion

- Reality Labs revenue $353 million, +28% y/y, beating estimates of $376.9 million

- Other revenue $389 million, +73% y/y, beating estimates of $344.6 million

- Operating income $14.85 billion, beating estimates of $14.59 billion

- Family of Apps operating income $19.34 billion, +47% y/y, beating estimates of $18.69 billion

- Reality Labs operating loss $4.49 billion, +20% y/y, estimate loss $4.53 billion

- Operating margin 38% vs. 29% y/y, beating estimates of 37.7%

- EPS $5.16 vs. $2.98 y/y, beating estimates of $4.72

| |

|

AMAZON (Online Retail)

Mixed results which saw revenues mostly miss and guidance disappoint, despite strong results from AWS.

The company's guidance was soft on the top line but disappointed on earnings:

- Revenues expected to be between $154.0 billion and $158.5 billion, or grow between 8% and 11% YoY, with the midline of 154.25 billion below the consensus estimate of $158.43 billion.

- Operating income is expected to be between $11.5 billion and $15.0 billion, compared with $11.2 billion in third quarter 2023, and also below the consensus estimate of $15.66.

- If accurate, that would mean Q3 revenue will grow at the slowest pace since Dec 2022.(Chart Right)

| |

| |

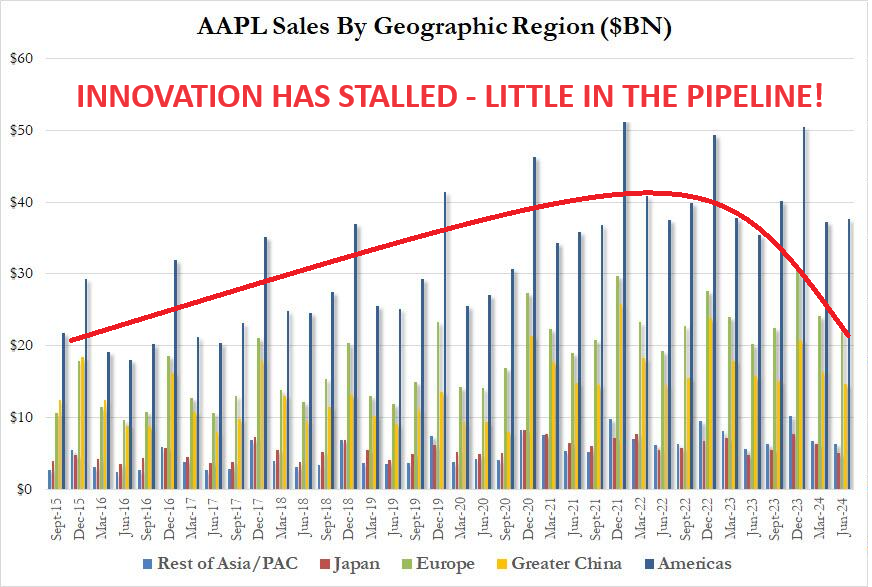

APPLE (Personal Electronics)

China revenues unexpectedly tumbled 6.5% Y-o-Y:

- Greater China rev. $14.73 billion, -6.5% y/y, missing estimates of $15.26 billion

- Sharply below the estimate of $15.3BN

The long run chart shows that revenues across most regions were flat at best, even ignoring the ongoing China weakness which will only get worse if Trump becomes president.

- Apple Inc (AAPL) Q3 2024 (USD): EPS 1.40 (exp. 1.35), revenue 85.78bln (exp. 84.53bln)

- Products rev. USD 61.56bln (exp. 60.63bln), iPhone rev. USD 39.30bln (exp. 38.95bln), iPad revenue USD 7.16bln (exp. 6.63bln), Mac rev. USD 7.01bln (exp. 6.98bln), Wearables, home and accessories rev. USD 8.10bln (exp. 7.79bln), Service rev. USD 24.21bln (exp. 23.96bln), Greater China rev. USD 14.73bln (exp. 15.26bln). Shares rose 0.6% after-hours.

Bloomberg's Mark Gurman had a scathing, and accurate, assessment:

"My big picture takeaway is that, financially, everything is *fine* at Apple. But this is a company that has dramatically lost its pace of innovation and has probably missed on its latest major new product, while canceling future sources of growth like in-house screen technology and cars. I am seeing nothing in the Apple product roadmap in the next 2-3 years that is a game-changer. Anything new and meaningful is not coming until around 2027 in my view."

| |

|

PROFIT MARGINS & CAPEX:

Profit margins typically lead capex growth by 4-5 quarters and currently capex growth is accelerating for Tech but remains muted outside Tech.

Over the next two quarters it will be important to monitor margins outside Tech to confirm the increased longevity of the business cycle.

| |

|

2- BoJ RAISES RATES - REDUCES JGB PURCHASES

- BoJ raised its short-term interest rate to 0.25% (prev. 0.00-0.10%).

- BoJ also announced a change in bond purchases in which it will no longer provide a range, but will instead specify amounts.

- BoJ is to reduce scheduled monthly bond buying by around JPY 400bln each quarter and with bond purchases to be JPY 3tln a month as of Q1 2026.

- BoJ said the decision on rates was made by a 7-2 vote with Nakamura and Noguchi the dissenters, while the decision on bond buying made unanimously.

- BoJ stated that it may modify the bond-taper plan upon mid-term view as appropriate, if deemed necessary for functioning of JGB market, and at the June 2025 meeting, the BoJ will discuss the guideline for its JGB buying from April 2026 and announce results.

- BOJ meeting delivered the full package of hawkishness:

- A rate hike

- Hawkish statement

-

BOJ Governor who tried to back it up with hawkish forward guidance.

- BoJ’s Ueda: Upside risks to prices require attention.

- Will continue to lift rates and adj. the degree of easing, if the current economic/price outlook is realized

- "We don't have a 0.5% policy rate in mind as a ceiling."

- Main issue is where to stop raising rates, when approaching the neutral rate. Policy response this time was made considering the upward risks to prices as being considerably large.

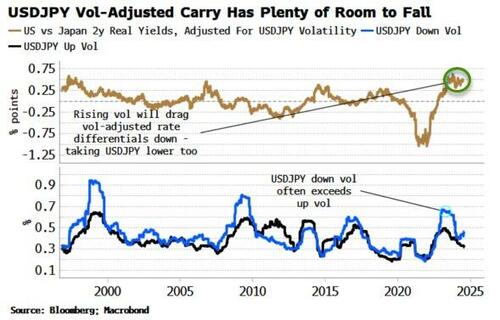

BOTTOM LINE: US rate cuts will shrinking rate spread, which along with a strengthening Yen, will place pressures on the viability of the $3.5T Japanese Carry Trade to continue to finance US & EU debt and fiscal deficits.

|  | |

As the JPY rallies, it increases the likelihood the loss on the FX part of the trade exceeds the profit made on the yield differential.

As yen volatility picks up, more carry traders are likely to head for the exit, taking the yen higher in the process.

But, as the chart to the right shows, vol-adjusted USD versus JPY real-yield differentials remain extremely wide, (and have barely started to move. Yet - net shorts of speculators in the yen, a proxy for carry traders, have started to fall but still remain close to historic highs).

So, while some might see this as 'plenty of room to run on the unwind', the 'carry' remains extremely attractive. And, there is still no real alternative to the yen as a funding currency.

Rates elsewhere in G-10 are too high in comparison. The rate differential between the US and Japan remains wide. The 1-year cost of carry based on the forwards is as much as 4.4%. And the Swiss franc is benefiting as the haven currency of choice given geopolitical tensions. That keeps the yen as the primary candidate within G-10.

| |

DEVELOPMENTS

US TREASURY: QUARTERLY REFUNDING ANNOUNCEMENT

PREVIEW

-

Q3 funding needs were revised lower to $740 billion from $847 billion projected last quarter. According to the Treasury, the borrowing estimate was $106 billion lower than announced in April 2024, largely due to lower Federal Reserve System Open Market Account (SOMA) redemptions and a higher beginning-of-quarter cash balance.

- In other words, the QT taper is primarily responsible for the lower funding needs.

- The Treasury also kept its quarter-end cash balance estimate unchanged at $850 billion.

-

Q4 funding needs are estimated at $565 billion, $115 billion above estimates of $450 billion, which is quite a bit higher than expected, but which is also due in part to the higher TGA estimate of $700 billion.

-

IN SUMMARY: The Treasury expects to borrow just over $1.3 trillion by year-end. (Although this number will end up being much higher if Trump becomes president and the US "unexpectedly" collapses into recession in the first days of the new presidency).

ANNOUNCEMENT

-

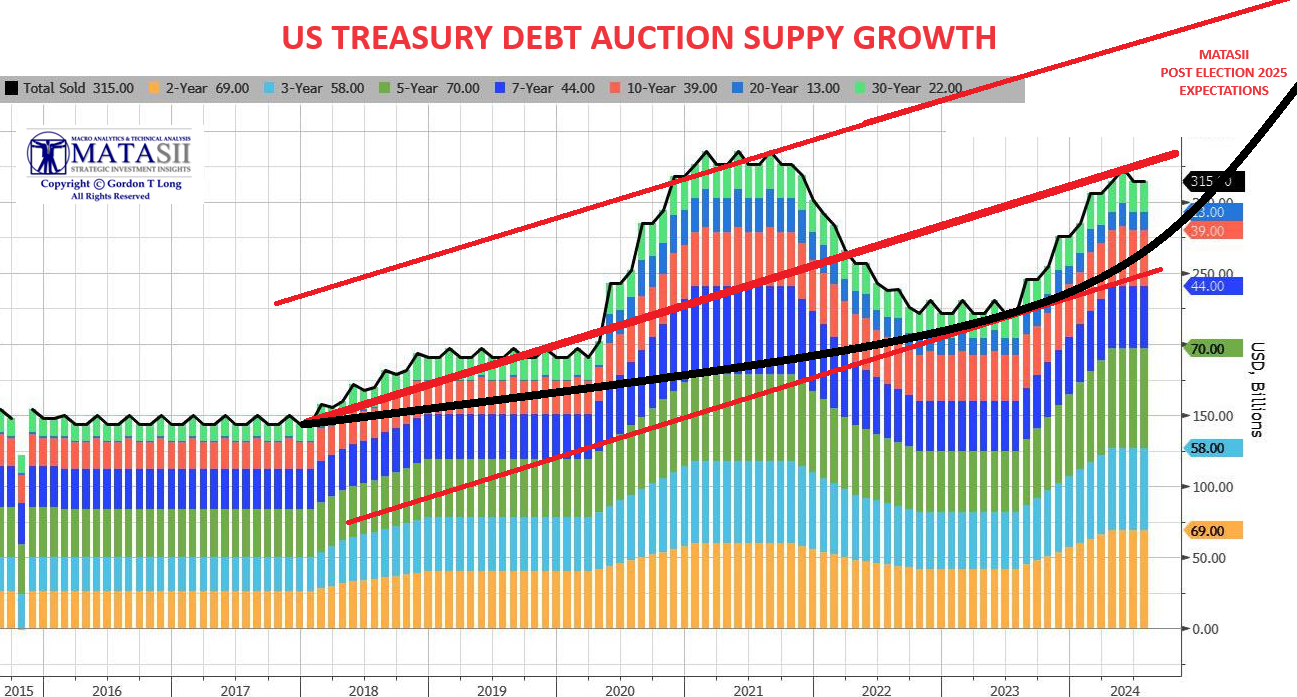

AUGUST - US Treasury quarterly refunding package was mostly identical to the one in May, with $125bn in gross issuance across 3y, 10y and 30y auctions. In addition, unchanged 5y TIPS new issue and 30y TIPS reopening (at $23bn and $8bn, respectively), and a $1bn increase to the 10y TIPS reopening (to $17bn) to commensurate with the increase in the 10y TIPS new issue auctioned this month. The quarterly refunding would be $125 billion, with issuance raising $14 billion in new cash from private investors, as follows:

- $58 billion in 3-year notes

- $42 billion in 10-year notes

- $25 billion in 30-year bonds

The refunding total is just shy of the record $126BN first reached in Feb. 2021; auction sizes across the curve began rising in 2018 to finance tax cuts and surged in 2020 to finance federal pandemic response.

| |

|

The Treasury confirmed expectations that the balance of Treasury financing requirements over the quarter will be met with regular weekly bill auctions, cash management bills (CMBs), and monthly note, bond, Treasury Inflation-Protected Securities (TIPS), and 2-year Floating Rate Note (FRN) auctions.

It also said that "its current auction sizes leave it well positioned to address potential changes to the fiscal outlook and to the pace and duration of future SOMA redemptions." More importantly, the Treasury forecast that "based on current projected borrowing needs, Treasury does not anticipate needing to increase nominal coupon or FRN auction sizes for at least the next several quarters."

The real question should be not what the Treasury projects for Q3 and Q4, but Q1, which is when as we now know Biden will finally leave the White House forever, and be replaced by either Trump or Kamala (or Big Mike) and when all the lipstick on this pig will finally wash off. (See our MATASII expectations represented by black line above.)

| |

FOMC - JULY MEETING

KEY HEADLINES (via Bloomberg)

- Federal Open Market Committee votes unanimously to leave benchmark rate unchanged in target range of 5.25%-5.5%, a more than two-decade high, for the eighth straight meeting.

-

Statement tweaks language to say “the committee is attentive to the risks to both sides of its dual mandate”; had previously said officials were “highly attentive to inflation risks”.

-

Statement repeats prior language, saying the FOMC doesn’t expect to cut rates “until it has gained greater confidence that inflation is moving sustainably toward 2%.”

- Fed also tweaks language to say price pressures remain “somewhat” elevated, and acknowledge “some further progress” toward inflation goal, from “modest further progress” in previous statement.

- Officials also adjust their assessment of the labor market, saying job gains “have moderated” and the jobless rate “has moved up but remains low”.

- Statement notes that risks to achieving employment and inflation goals “continue to move into better balance”.

- Decision is unanimous for 17th straight meeting.

The FOMC has a hawkish bias to it compared to the market's dovishness.

Global head of markets strategy at BBH, says:

"I think they will cut, but the Fed is playing its cards close to its chest. Marginally less dovish than expected.”

George Goncalves, head of US macro strategy at MUFG, says the latest FOMC statement shows:

“There are enough elements that were re-written that it seems to us that there was careful consideration to how to express the start of a pivot towards easing.”

| |

|

GLOBAL ECONOMIC INDICATORS:

What This Week's Key Global Economic Releases Tell Us

| |

US LABOR REPORT - NFP

The US added just 114K payrolls, a huge miss to expectations of 175K and also a huge drop from the downward revised June print of 206K, now (as always ) revised to just 179K. This was the lowest print since December 2020, (at least prior to even more revisions), and a 3 sigma miss to the median estimate of 175K.

SAHM RULE TRIGGERED = RECESSION

While we have long known that the real payrolls number is far worse than reported, what was the true shock in today's "data" is the long overdue admission that the US is effectively in a recession because, as the rule named for pro-Biden/Kamala socialist Claudia Sahm indicates, a recession has now been triggered. The rule, for those who don't remember, is that a recession is effectively already underway if the unemployment rate (based on a three-month moving average) rises by half a percentage point from its low of the past year. And that's what just happened, with the unemployment rate surging 0.6% from the year's low.

NOTES

- US jobs report for July was very soft, and sparked massive risk off sentiment, huge dovish Fed money-market repricing, alongside banks such as JPMorgan and Goldman Sachs revising their Fed forecasts, with the latter seeing 50bps cuts in September and November.

- Overall, the data added to fears regarding US growth and followed in the footsteps of the poor ISM Manufacturing PMI on Thursday, which of course came after Fed Chair Powell said in his presser on Wednesday that upside risks to inflation have decreased, and downside risks to employment mandate are real now.

- Regarding the data, the headline fell to 114k from 179k, beneath the expected 175k, with BLS noting Hurricane Beryl had no discernible impact for the July data, and response rates were within normal ranges.

- Unemployment unexpectedly rose to 4.3% from 4.1% (exp. 4.1%), invoking the Sahm rule, which historically indicates the economy is in recession, but that is not the case now.

- Average workweek hours dipped to 34.2hrs from 34.3hrs and participation rate ticked higher to 62.7% from 62.6%.

- Average earnings for both M/M and Y/Y declined to 0.2% (exp. & prev. 0.3%) and 3.6% (exp. 3.7%, prev. 3.8%), respectively.

- Oxford Economics notes there was a sharp increase in the number of workers on temporary layoff, which may be hurricane-related.

- Overall, the July jobs report showed a labor market losing and all but ensures a rate cut for September, but the debate is to what degree.

- Goldman Sachs sees 25bps in September, followed by the same degree in Nov. and Dec, while JPM sees 50bps in both Sept. and Oct.In terms of money market pricing, 115bps of cuts are priced in by year-end vs. 88bps pre-data.

| |

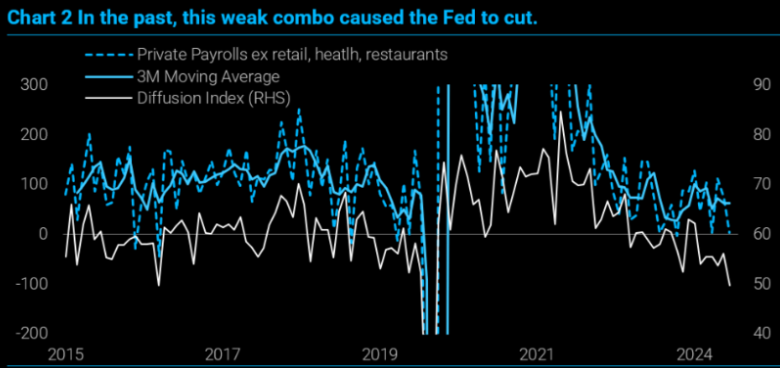

JOLTS, QUITS & HIRES

HIRES v QUITS - A tightening labor market (Chart Right)

JOLTS

- US JOLTS Job Openings (Jun) 8.184M vs. Exp. 8.0M (Prev. 8.14M, Rev. 8.23M)

The government "manipulation" game here is to see a spike in "government" openings, which are then revised away, and for the June print to drop from the revised May print. That is what happened once again.

| |

- While private jobs saw another broad drop in openings across private sectors, this was almost fully offset by the relentless surge in government job openings.

- May was indeed revised lower, June saw another bizarre jump in government job openings, surging to a near record 1.094 million, driven by a 118K spike in State and Local job openings.

- Private sector job openings plunged to a level seen back in late 2018. Government job openings are just shy of a record high!

| |

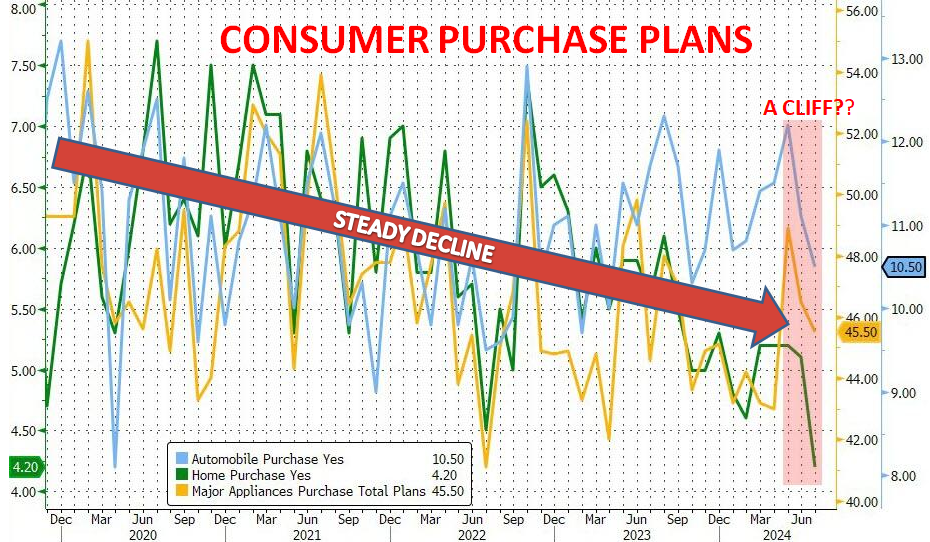

CONSUMER CONFIDENCE - Expectations

The overall trend in the labor market indicator remains weaker. (Chart Right)

CHART BELOW

Purchase plans for homes, cars and appliances have all plunged.

| |

|

GLOBAL MACRO

WHAT DOES YOUR SCAN OF THE DATA BELOW TELL YOU? - THE MEDIA AVOIDS BAD NEWS!

We present the data in a way you can quickly see what is happening.

THIS WEEK WE SAW

Exp=Expectations, Rev=RevisiEU Consumer Confidence Flash (Jul) -13.0 vs. Exp. -13.4 (Prev. -14.0)on, Prev=Previous

| |

|

UNITED STATES

- US Dallas Fed Manufacturing Business Index (Jul) -17.5 (Prev. -15.1)

- US Consumer Confidence (Jul) 100.3 vs. Exp. 99.7 (Prev. 100.4, Rev. 97.8)

- US Monthly Home Price YY (May) 5.7% (Prev. 6.3%, Rev. 6.5%)

- US CaseShiller 20 YY NSA (May) 6.8% vs. Exp. 6.7% (Prev. 7.2%, Rev. 7.3%)

- US JOLTS Job Openings (Jun) 8.184M vs. Exp. 8.0M (Prev. 8.14M, Rev. 8.23M)

- US Employment Costs (Q2) 0.9% vs. Exp. 1.0% (Prev. 1.2%)

- US ADP National Employment (Jul) 122.0k vs. Exp. 150.0k (Prev. 150.0k, Rev. 155k)

- US Pending Sales Change MM (Jun) 4.8% vs. Exp. 1.5% (Prev. -2.1%, Rev. -1.9%)

- US Chicago PMI (Jul) 45.3 vs. Exp. 45.0 (Prev. 47.4)

CHINA

- Chinese Industrial Profits YY (Jun) 3.6% (Prev. 0.7%)

- Chinese Industrial Profits YTD YY (Jun) 3.5% (Prev. 3.4%)

- Chinese Manufacturing PMI (Jul) 49.4 vs Exp. 49.3 (Prev. 49.5)

- Chinese Non-Manufacturing PMI (Jul) 50.2 vs Exp. 50.2 (Prev. 50.5)

- Chinese Composite PMI (Jul) 50.2 (Prev. 50.5)

- Chinese Caixin Manufacturing PMI Final (Jul) 49.8 vs. Exp. 51.5 (Prev. 51.8)

JAPAN

- Japanese Unemployment Rate (Jun) 2.5% vs. Exp. 2.6% (Prev. 2.6%); Jobs/Applicants Ratio 1.23 vs. Exp. 1.24 (Prev. 1.24)

- Japanese Jobs/Applicants Ratio (Jun) 1.23 vs. Exp. 1.24 (Prev. 1.24)

UK

- UK Mortgage Approvals (Jun) 59.976k vs. Exp. 60.4k (Prev. 59.991k, Rev. 60.134k); Lending (Jun) 2.653B GB vs. Exp. 1.2B GB (Prev. 1.212B GB, Rev. 1.26B GB)

- UK M4 Money Supply (Jun) 0.5% (Prev. -0.1%)

- UK BRC Retail Shop Price Index YY (Jul) 0.2% (Prev. 0.2%)

- UK Nationwide house price MM (Jul) 0.3% vs. Exp. 0.1% (Prev. 0.2%); YY 2.1% vs. Exp. 1.8% (Prev. 1.5%)

- UK S&P Global Manufacturing PMI (Jul) 52.1 vs. Exp. 51.8 (Prev. 51.8); “Inflationary pressures remain a blot on the copybook, however, with input costs rising to the greatest extent in one-and-a-half years." Adding “Selling prices are also rising at the quickest rate since mid-2023. Policymakers are likely to take a cautious approach to loosening monetary policy amid these signs that inflationary pressures may be pivoting away from services and towards manufacturing.”

AUSTRALIA

- Australian Building Approvals (Jun) -6.5% vs. Exp. -1.5% (Prev. 5.5%, Rev. 5.7%)

- Australian Building Approvals (Jun) -6.5% vs. Exp. -1.5% (Prev. 5.5%, Rev. 5.7%)

- Australian Weighted CPI YY (Jun) 3.8% vs. Exp. 3.8% (Prev. 4.0%)

- Australian CPI QQ (Q2) 1.0% vs. Exp. 1.0% (Prev. 1.0%)

- Australian CPI YY (Q2) 3.8% vs. Exp. 3.8% (Prev. 3.6%)

- Australian RBA Trimmed Mean CPI QQ (Q2) 0.8% vs. Exp. 1.0% (Prev. 1.0%)

- Australian RBA Trimmed Mean CPI YY (Q2) 3.9% vs. Exp. 4.0% (Prev. 4.0%)

- Australian RBA Weighted Median CPI QQ (Q2) 0.8% vs. Exp. 1.0% (Prev. 1.1%)

- Australian RBA Weighted Median CPI YY (Q2) 4.1% vs. Exp. 4.3% (Prev. 4.4%)

- Australian Trade Balance (AUD)(Jun) 5.59B vs Exp. 5.00B (Prev. 5.77B)

- Australian Exports MM (Jun) 1.7% (Prev. 2.8%)

- Australian Imports MM (Jun) 0.5% (Prev. 3.9%)

- Australian Export Prices (Q2) -5.9% (Prev. -2.1%)

- Australian Import Prices (Q2) 1.0% (Prev. -1.8%)

- Australian PPI QQ (Q2) 1.0% (Prev. 0.9%)

- Australian PPI YY (Q2) 4.8% (Prev. 4.3%)

NEW ZEALAND

- New Zealand ANZ Business Outlook (Jul) 27.1% (Prev. 6.1%)

- New Zealand ANZ Own Activity (Jul) 16.3% (Prev. 12.2%)

SWITZERLAND

- Swiss CPI YY (Jul) 1.3% vs. Exp. 1.3% (Prev. 1.3%); MM (Jul) -0.2% vs. Exp. -0.2%

SWEDEN

- Swedish GDP YY Prelim (Q2) 0.0% vs. Exp. 0.3% (Prev. 0.7%); QQ -0.8% vs. Exp. -0.4% (Prev. 0.7%)

| |  |

|

EU

- EU Consumer Confidence Final (Jul) -13.0 vs. Exp. -13.0 (Prev. -13.0)

- EU Selling Price Expectations (Jul) 6.8 (Prev. 6.1, Rev. 6.2); Consumer Inflation Expectations 11.2 (Prev. 13.1)

- EU GDP Flash Prelim QQ (Q2) 0.3% vs. Exp. 0.2% (Prev. 0.3%)

- EU GDP Flash Prelim YY (Q2) 0.6% vs. Exp. 0.5% (Prev. 0.4%)

- EU Services Sentiment (Jul) 4.8 vs. Exp. 5.5 (Prev. 6.5, Rev. 6.2)

- EU Industrial Sentiment (Jul) -10.5 vs. Exp. -10.7 (Prev. -10.1, Rev. -10.2)

- EU Economic Sentiment (Jul) 95.8 vs. Exp. 95.4 (Prev. 95.9)

- EU Consumer Confidence Final (Jul) -13.0 vs. Exp. -13.0 (Prev. -13.0)

- EU HICP Flash YY (Jul) 2.6% vs. Exp. 2.5% (Prev. 2.5%); Ex-Food & Energy 2.8% vs. Exp. 2.7% (Prev. 2.8%); Ex-Food, Energy, Alcohol & Tobacco 2.9% vs. Exp. 2.8% (Prev. 2.9%)

- EU Unemployment Rate (Jun) 6.5% vs. Exp. 6.4% (Prev. 6.4%)

- EU HCOB Manufacturing Final PMI (Jul) 45.8 vs. Exp. 45.6 (Prev. 45.6)

GERMANY

- German Data Summary/Reaction (Regional CPI & Q2 GDP): A weak set of Q2 GDP data saw Bunds revisit the earlier 133.43 peak (printed on the Spanish Flash CPI numbers), thereafter a net slightly hawkish (vs. mainland exp.) set of German regional CPIs saw Bunds reverse and fall to 133.20. From the Regional CPI, expectations for the mainland M/M are perhaps subject to a modest upward skew vs. 0.2% (prev. 0.1%) consensus set before the regional release while the Y/Y view is broadly in-fitting at 2.2% (prev. 2.2%) as the regional numbers were somewhat mixed.

- German GDP Flash QQ SA (Q2) -0.1% vs. Exp. 0.1% (Prev. 0.2%)

- German GDP Flash YY NSA (Q2) 0.3% vs. Exp. 0.3% (Prev. -0.9%)

- German CPI Prelim MM (Jul) 0.3% vs. Exp. 0.2% (Prev. 0.1%)

- German CPI Prelim YY (Jul) 2.3% vs. Exp. 2.2% (Prev. 2.2%); Core 2.9% (prev. 2.9%)

- German Import Prices MM (Jun) 0.4% vs. Exp. 0.1%; YY 0.7% vs. Exp. 0.5% (Prev. -0.4%)

- German Unemployment Chg SA (Jul) 18.0k vs. Exp. 15.0k (Prev. 19.0k)

- German Unemployment Rate (Jul) 6.0% vs. Exp. 6.0% (Prev. 6.0%)

- German HCOB Manufacturing PMI (Jul) 43.2 vs. Exp. 42.6 (Prev. 42.6); "We are now expecting the overall economy to grow by just 0.2% this year, down from our previous forecast of 0.5%".

FRANCE

- Spanish CPI YY Flash NSA (Jul) 2.8% vs. Exp. 3.1% (Prev. 3.4%); Core 2.8% (prev. 3.0%)

- Spanish HICP Flash YY (Jul) 2.9% vs. Exp. 3.2% (Prev. 3.6%)

- French GDP Preliminary QQ (Q2) 0.3% vs. Exp. 0.2% (Prev. 0.2%, Rev. 0.3%); Consumer Spending MM (Jun) -0.5% vs. Exp. 0.2% (Prev. 1.5%, Rev. 0.8%)

- French CPI Prelim YY NSA (Jul) 2.3% vs. Exp. 2.4% (Prev. 2.2%); MM 0.1% vs. Exp. 0.3% (Prev. 0.1%)

- French CPI (EU Norm) Prelim YY (Jul) 2.6% vs. Exp. 2.7% (Prev. 2.5%)

SPAIN

- Spanish CPI YY Flash NSA (Jul) 2.8% vs. Exp. 3.1% (Prev. 3.4%); Core 2.8% (prev. 3.0%)

- Spanish HICP Flash YY (Jul) 2.9% vs. Exp. 3.2% (Prev. 3.6%)

- French GDP Preliminary QQ (Q2) 0.3% vs. Exp. 0.2% (Prev. 0.2%, Rev. 0.3%); Consumer Spending MM (Jun) -0.5% vs. Exp. 0.2% (Prev. 1.5%, Rev. 0.8%)

- UK BRC Retail Shop Price Index YY (Jul) 0.2% (Prev. 0.2%)

- Spanish CPI MM Flash NSA (Jul) -0.5% vs. Exp. -0.2% (Prev. 0.4%)

- Spanish CPI YY Flash NSA (Jul) 2.8% vs. Exp. 3.1% (Prev. 3.4%)

ITALY

- Italian GDP Prelim QQ (Q2) 0.2% vs. Exp. 0.2% (Prev. 0.3%)

- Italian GDP Prelim YY (Q2) 0.9% vs. Exp. 0.9% (Prev. 0.7%)

- Italian Consumer Price Prelim YY * (Jul) 1.3% vs. Exp. 1.2% (Prev. 0.8%); MM 0.5% vs. Exp. 0.2% (Prev. 0.1%)

SOUTH KOREA

- South Korean CPI MM (Jul) 0.3% vs. Exp. 0.25% (Prev. -0.2%)

- South Korean CPI YY (Jul) 2.6% vs. Exp. 2.5% (Prev. 2.4%)

| |

|

CURRENT MARKET PERSPECTIVE

(NOTE: You missed our Subscriber Mid-Week Update - You Are working with only half the info!)

| |

|

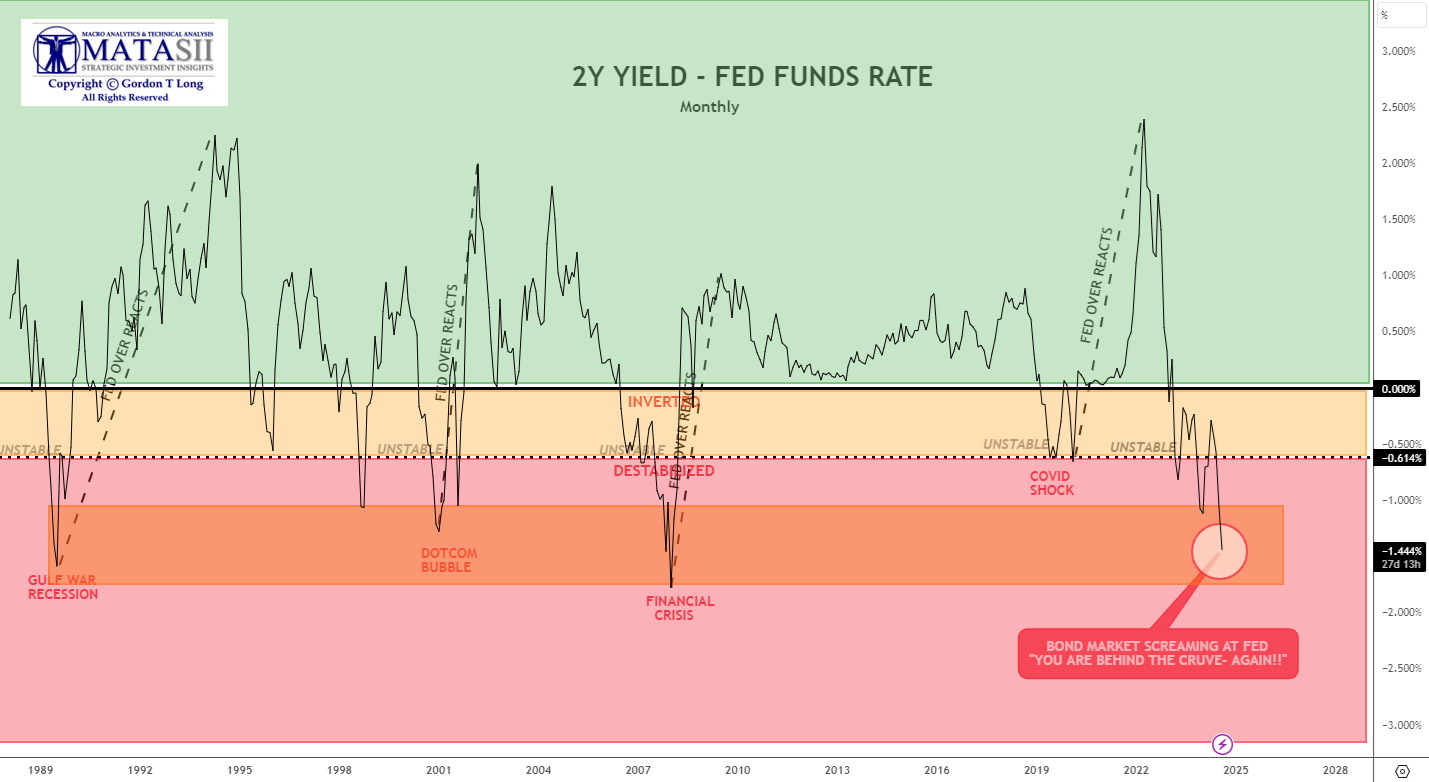

LABOR REPORT SAYS FED BEHIND CURVE - AGAIN!

2 YEAR TREASURY YIELD (BOND MARKET) SCREAMING!

Click All Charts to Enlarge

| |

|

2 YEAR TREASURY YIELD: The Bond Market is screaming at the Fed - "You are wrong again!" Friday was the biggest drop in 2Y yield since Dec 2023 (Powell pivot) and the biggest weekly drop since March 2023 (SVB collapse). The yield curve has dis-inverted (2s30s now at its steepest since July 2022).

JP MORGAN

Even if the softening in labor market conditions moderates from here going forward, it would seem the Fed is at least 100bp offsides, probably more. So we now think the FOMC cuts by 50bp at both the September and November meetings, followed by 25bp cuts at every meeting thereafter. From a risk management perspective we think there’s a strong case to act before September 18th. But perhaps Powell doesn’t want to add more noise to what has already been an event-filled summer.

| |

|

1 - SITUATIONAL ANALYSIS

On Thursday prior to Friday's Labor Report, US stocks sold off in the wake of the disappointing US ISM Manufacturing PMI data as the headline surprisingly declined, which printed outside the bottom end of the forecast range and prices paid rose, while other data also showed a larger-than-expected rise in jobless claims. There was a distinct flight-to-quality throughout the session which benefitted the Dollar and Treasuries.

Following the soft US jobs report on Friday, there has been an aggressive repricing in money markets, which now see 117bps of rate cuts by year end and 43bps in September.

- From banks, BofA Global Research expects the Fed to start cutting rates in Sept. (prev. Dec.) with 25bps, and also sees a cut in Dec.

- GS expects the Fed to dispatch an initial string of consecutive 25bps cuts in Sept., Nov. and Dec. (prev. cuts every other meeting).

- Both Citi and JPM see the central bank cutting 50bps in Sept. and Oct.

| |

|

A BIG THREE DAY: Jobless claims have surged, Manufacturing surveys have slumped, Construction spending has tanked ..... all creating growth anxiety which sent rate-cut expectations higher, bond prices higher and Yields lower!

CHART RIGHT: TS Lombard's Steve Blitz:

"It is the Fed's turn to move in this immaculate disinflation game. July data are not recessionary, but Powell said they are not going to wait for bad news to act, knowing that it means they are too late. Good news is that excess liquidity will make the Fed's job easier."

| |

BoA's Chief Strategist Michael Hartnett:

"People underestimate how much lower rates may need to go to stimulate a weak economy no longer juiced by government spending".

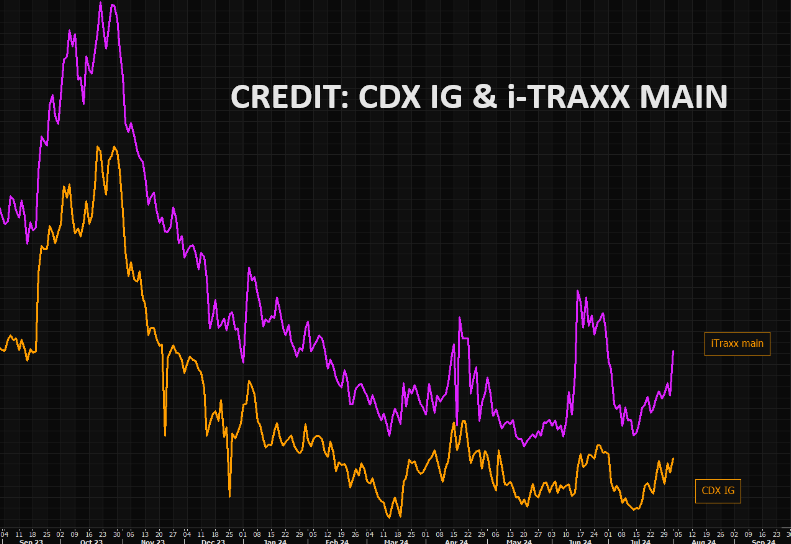

CREDIT ALWAYS LEADS

CHART RIGHT: CDX IG and iTraxx main.

The key credit spreads that would signal harder landing:

- CDX IG >60bps (now 55bps)

- CDX HY >375bps (now 348bps).

| |

SENTIMENT

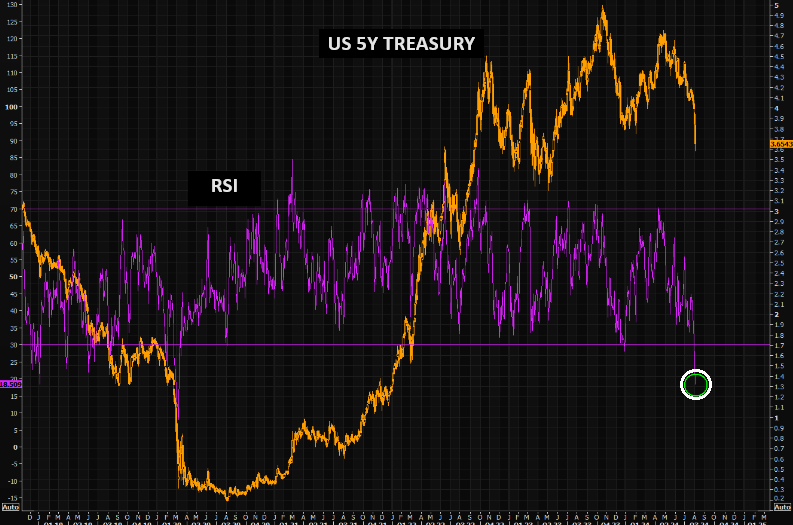

- US 5 year RSI at 18.5...was lower once in "modern times", during the Covid panic.(Chart Right)

- The TDEX Index measures the cost of options that hedge against a three standard deviation drop in price. It was up 150% (on the day) late Friday PM.

- The VIX 2/8 months futures spread is trading at levels not seen in a very long time. This is basically entering pure panic land.

- The options markets sh...t the bed with VIX exploding to almost 30 at its peak today (highest since Oct 2022), and VVIX smashing above the critical scare level of 100, (to its highest since March 2022).

- Last time VVIX was here, the VIX traded at 32. Doesn't really work that way, but the explosion in fear is absolutely massive.

- Crazy bid skew is a clear sign of panic buying of downside hedges. SDEX has not closed this high since April 2022.

| |

Nomura's McElligott sums it up:

"Former “High Sharpe” Momentum- and Carry- trades see waves of risk-management unwind and stop-out in crowded Risk-Asset trades (SMH -9.3% since Wednesday, TOPIX Banks -11.0% overnight, a -6.5 z-score 1d move 1y rel), building off the back of the FX unwinds felt over the past few weeks as the Yen short-squeeze metastasized around hawkish BoJ signaling".

CHART RIGHT: On Wednesday night we said: "Say hello to fear! The CNN Fear-Greed Index touched Greed territory then abruptly reversed to Fear." We were at 40 (Chart). Do we see EXTREME FEAR kick in soon?

CHART BELOW: We showed this CNN Fear-Greed Index chart Wednesday night (chart) suggesting, though we were in fear land, we have seen "deeper" fear kick in before markets decided to bounce. (NOTE: Here is the same chart as of Friday. You might want to see how predictive the chart was.)

| |

BofA's RISK-LOVE INDEX has come down from recent highs, but remains at elevated levels. | |

|

HARD CUTS

"Fed cuts into "hard landing", e.g. 1973, 1974, 1980, 1981, 1989, 2001, and 2007; -ve for stocks (S&P 500 -6% in 3 months) and +ve for bonds (10-year UST yield down 38bps in 6 months), plus big yield curve steepening (95bps for 2s10s yield curve in 6 months after" (BofA). The investment bank says "sell the 1st cut", as hard landing risk is increasing as well as the fact stocks have "front run" Fed cuts.

SOFT CUTS

Fed cuts into "soft landing", e.g. 1984, 1995, 2019; +ve for stocks (S&P 500 up 10%) and bonds, (10-year UST yield down 56bps in 6 months after 1st cut)" (BofA)

PANIC CUTS

Fed cutting in response to Wall St crash/credit event, e.g. 1987 & 1998; panic cuts = risk-on (S&P 500 up 20% on average 6 months post 1st cut), so long as Wall St "event" not felt on Main St (e.g. LTCM in '98 was not, whereas Lehman in '08 was.)" (BofA)

| |

BEHIND THE CURTAIN: A JAPANESE CARRY TRADE PANIC

CHART RIGHT:

Nikkei futures have extended the crash, now down some 18% from July 11. RSI is beyond oversold and we are well below the 200 day. Things are not "healthy" when big cap index charts look like small cap stocks post a profit warning.

CHART BELOW:

JPY and NASDAQ moving in tandem!

|  | |

JULY RECAP

-

S&P 500 managed very modest gains in July.

- There was a massive divergence between Small Caps (+12% in July) and Nasdaq (-1.5% in July).

- The Crowded consensus trades suffered in July. (e.g., A.I).

-

NASDAQ / RUSSELL: July saw the biggest Nasdaq underperformance of Russell 2000 since the peak of the Dotcom bubble's bursting.

-

MAGNIFICENT 7: Thanks to a massive $440BN surge Wednesday, (the biggest day since Feb), the market cap of Magnificent 7 stocks ended the month down only 2.5% (though admittedly down 10% from the highs).

-

MSFT bounced back hard from its post-earnings plunge and NVDA exploded (after touching $100).

-

NVDA added a stunning $330BN in market cap today - its largest single-day gain ever.

-

TREASURY YIELDS: plunged in July with the short-end down 45bps, dramatically outperforming the long-end.

-

BONDS & BULLION: Outperformed in July with the dollar down and oil getting hammered.

- The yield curve steepened dramatically in July, dis-inverting at 2s30s...

-

Gold soared to its highest monthly closing level ever, rebounding the last few days...

-

Crude had an ugly month overall, today saw a sizable bounce as MidEast tensions re-escalated.

-

CRYPTO / BITCOIN: It was a mixed month for crypto with Bitcoin managing gains (+4.5%), but Ethereum dumped (-4.5%), despite the launch of the ETH ETFs.

-

Bitcoin touched $70,000 intraday at its highs this month, but has fallen back since (testing $65k Wednesday).

-

.FOMC: The market's initial reaction to the FOMC statement was muted.

-

Powell reiterated that “We have made no decisions about future meetings and that includes the September meeting."

-

Powell dropped the dovish hammer: “I can imagine a scenario in which there would be everywhere from zero cuts to several cuts.”

- Powell's comments on the job market and inflation during the presser also sent yields and the dollar lower.

- Fed ready to move if easing in Labor Market goes beyond ‘gradual’ and would not want to see ‘further material cooling’. This will likely heighten the focus on Friday’s print.

- Inflation – very benign take from Powell re recent progress defined as ‘broader disinflation’ /high quality progress (including housing and non-housing services).

| |

|

US corporate bonds best "tell" whether cutting into "soft" or "hard" landing…

we say "harder" landing thus ==> "sell the 1st cut".

| |

RECESSION - Not "If" But Rather Whether a "Hard or Soft" Landing?

The data is becoming a little overwhelming that we will have a US recession within the next 12 months. The magnitude of recession is still in question.

We believe it will be a hard landing as the ~7T "sugar high" ends and the hard reality of the dire situation of the US and global economies is fully realized with Geo-Political tensions, trade tariffs and social unrest compounding a tenuous situation.

| |

|

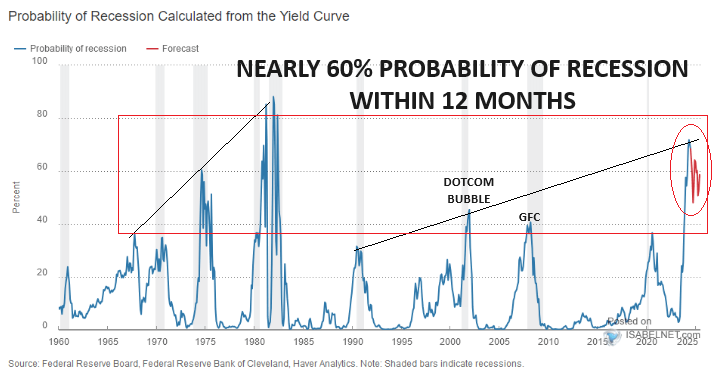

RETURN TO INCREASING RECESSION PROBABILITIES

CHART RIGHT

We currently have a 57.8% probability of a Recession within the next 12 months.

CHART BELOW

June's Retail Sales indicated NEGATIVE 0.68% Y-o-Y nominal growth. The US is a slightly less than 70% consumption economy. In the past. Retail sales trended sideways preceding a Recession.

| |

Equities have outperformed bonds despite a rise in the unemployment rate. | |

|

CREDIT LEADS -- HIGH YIELD BONDS - JNK

- CREDIT REACHED OUR TARGET OBJECTIVE

- Prices had steadily rose with the 50 DMA crossing the 100 DMA until our target price was reached, then abruptly fell off with Friday's Labor Report.

- We appear to have completed our ABCDE Corrective pattern within Wave 2.

- Wave 2, which we expected to end in August, did so - however, a little sooner than we thought.

- HY JNK Prices can now be expected to likely fall with spreads then widening, (especially if/when the Fed cuts Rates).

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

CHART BELOW:

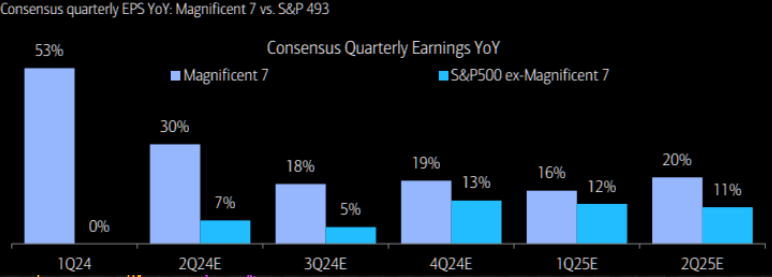

EARNINGS: Expect a "time for the rest" for the Mag-7 stock earnings - Mag7 to earnings to begin to decelerate, while the rest of the market is currently supposed to improve with few analysts building in earnings decline from a recession.

| |

|

MARKET DRIVERS

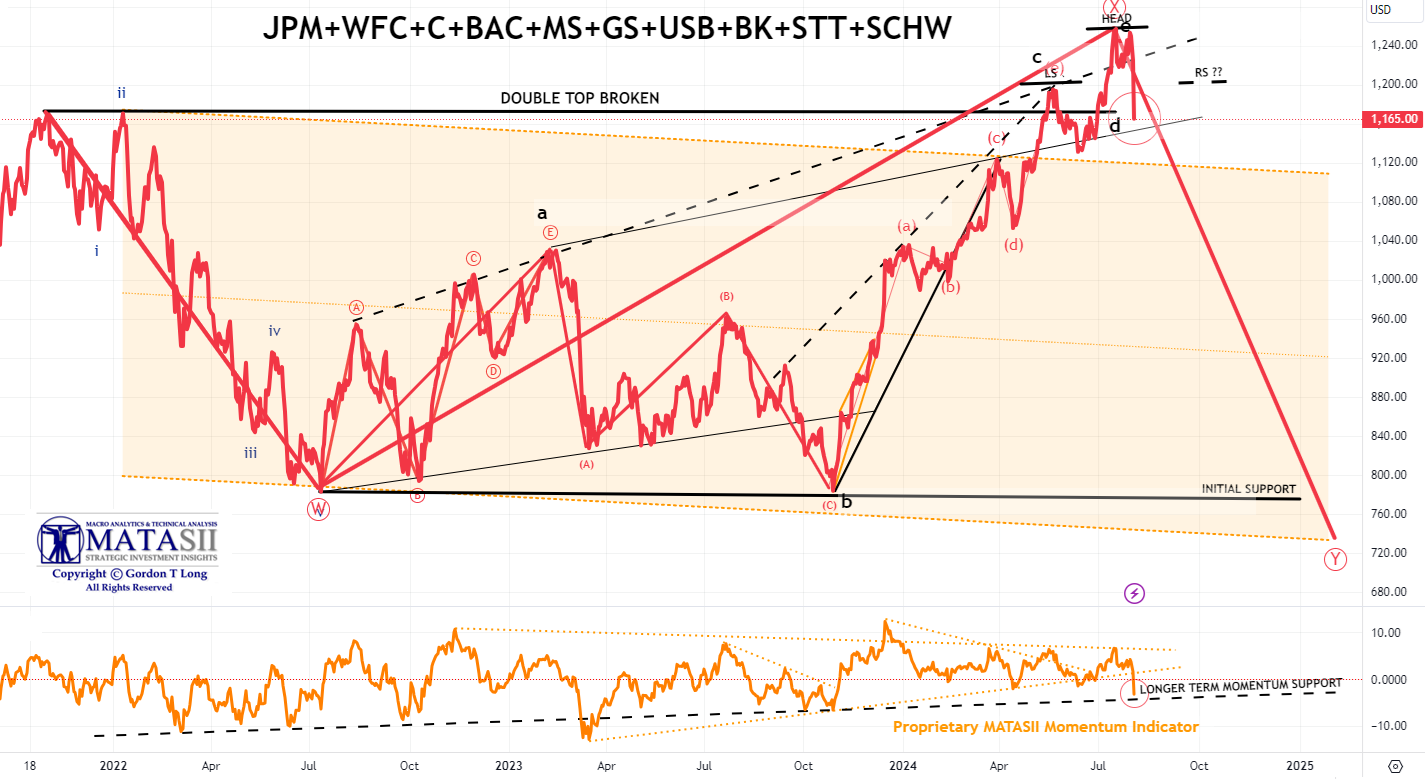

"AS GO THE FINANCIALS, SO GO THE BANKS: AS GO THE BANKS, SO GO THE MARKETS."

MATASII FINANCIAL STOCK INDEX

We continue to keep an eye on both the Bank and Financial stocks to give us an early signal of market direction.

- The MATASII Financial Index may have put in an Intermediate High (Possibly a Longer Term High)?

- We may be putting in a Head & Shoulders pattern as labeled in the Banking stocks (further below).

- Momentum (bottom pane) appears to be headed still lower to find the Longer Term Support trend line (see the black arrow).

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

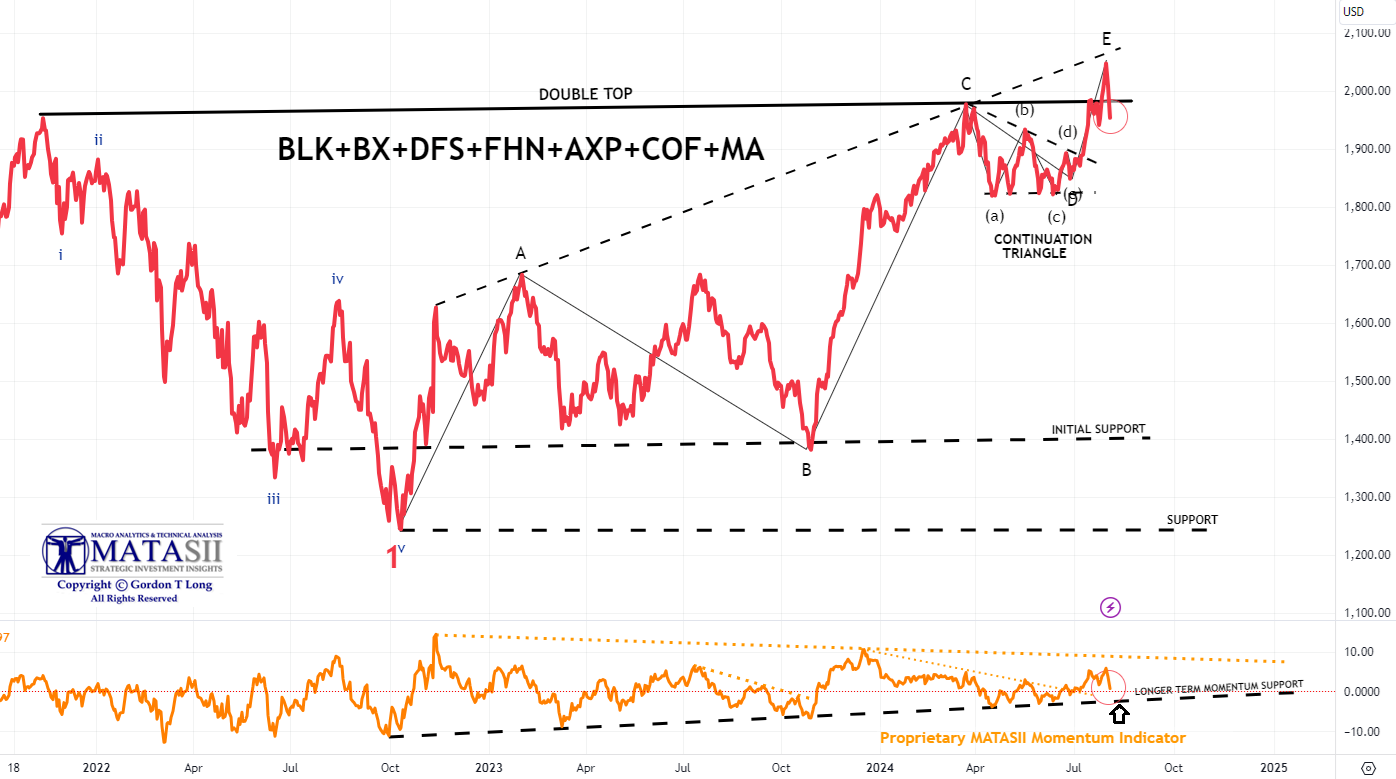

MATASII BANK STOCK INDEX

- The MATASII Bank Index appears to have potentially put in an Intermediate High (or possible a Long Term High).

- The "e" Wave appears completed here, near our original target price.

- The MATASII Proprietary Momentum Indicator (bottom pane) needs only a slightly lower price move to achieve support at its long term support line (black dashed line).

- We now need to pay particular attention to the possibility of a Head & Shoulders pattern forming, which often occurs at major reversals (tentatively labeled in the chart below).

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

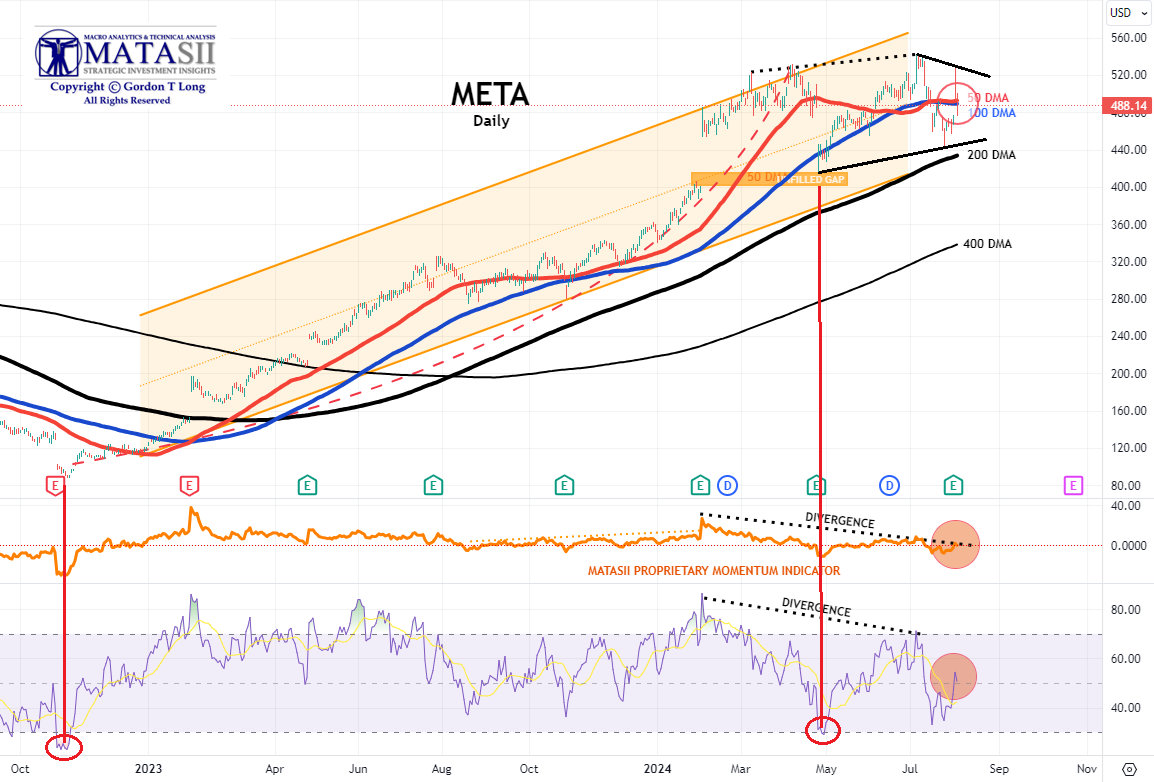

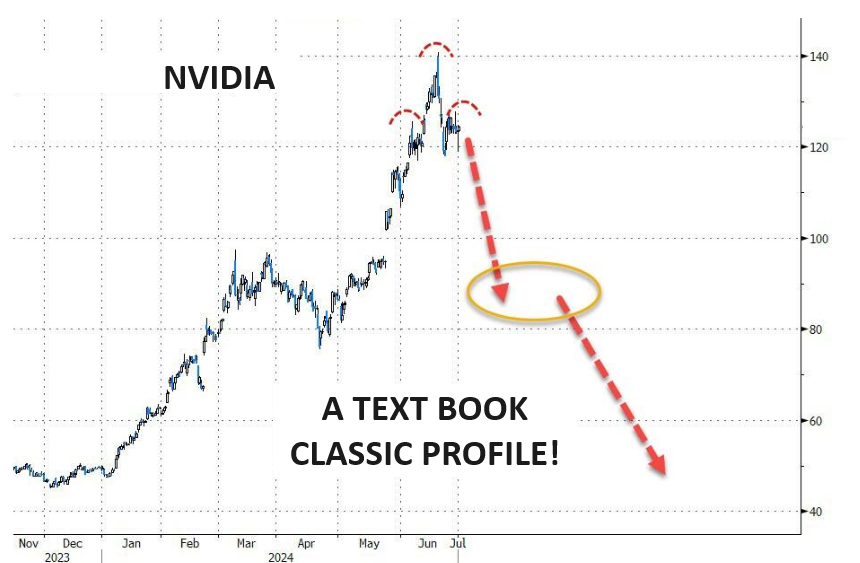

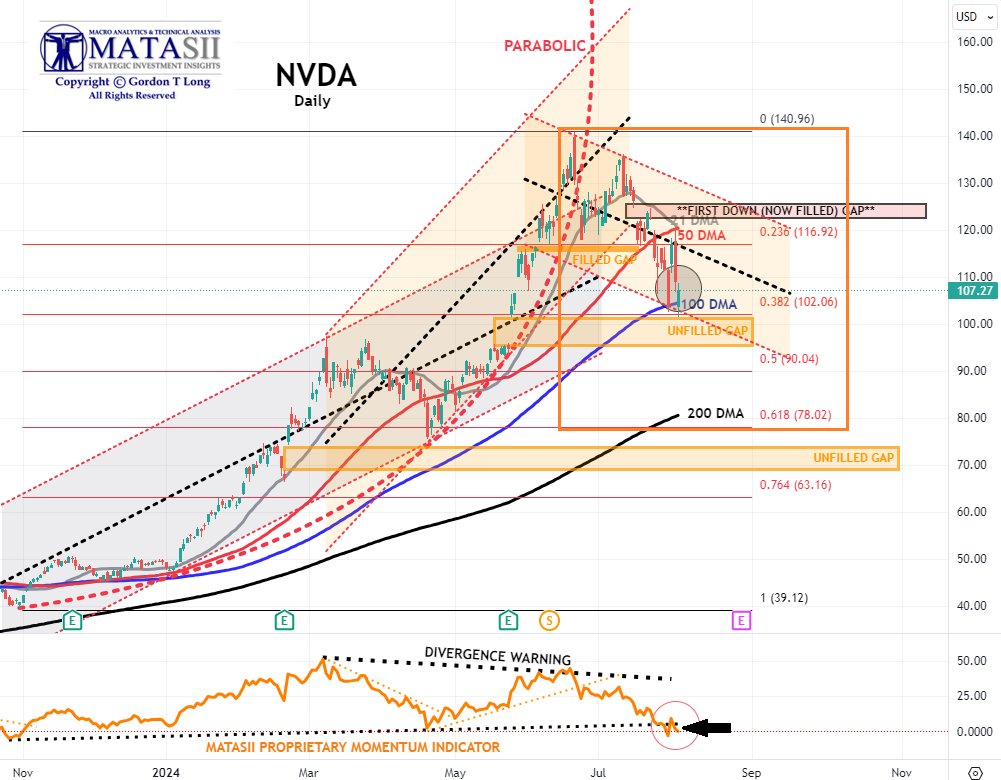

As goes NVDA, so goes the MAG-7, As Goes Mag-7 so goes The Market. | Investment benefactors are often not the big winners. | |

NVDA - Daily

CHART RIGHT: NVDA v the dominant darling CSCO of the Dotcom Bubble (for those who recall):

- NVDA found initial support at the 100 DMA.

- The MATASII Proprietary Momentum Indicator (lower pane) also offered support.

- The Momentum support trend line is likely to precipitate a counter rally - however, the trend is now clearly down.

- The Dotted Black Trend line in the MATASII Proprietary Momentum Indicator (lower pane below) has been signaling this sell-down was coming for some time now.

|

- Divergence is normally seen as a warning to the downside and is still ahead if the Divergence isn't removed by a movement higher in Momentum.

- At some point, the major unfilled gaps (at much lower levels) must be filled. NVDA therefore may no longer become a Short to Intermediate Long Term hold, but rather a position trading stock as other competitors enter the space and force margins and the earnings grow rate to contract.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

MAGNIFICENT 7

The Magnificent 7 stocks are now down an incredible $2.3 trillion market cap from their record highs.

- The basket of 'Magnificent 7' stocks appear to have found support at the Intermediate Momentum Indicator trend line. (Lower pane marketed by the black arrow.)

- A brief counter rally may ensue next week, but it is highly likely that Longer term Momentum Support (lower pane black dashed line) will soon be tested.

- Continued caution is advised since major global "Dark Pools" have been identified as presently operating behind the scenes on the Mag-7.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

"CURRENCY" MARKET (Currency, Gold, Black Gold (Oil) & Bitcoin) | |

|

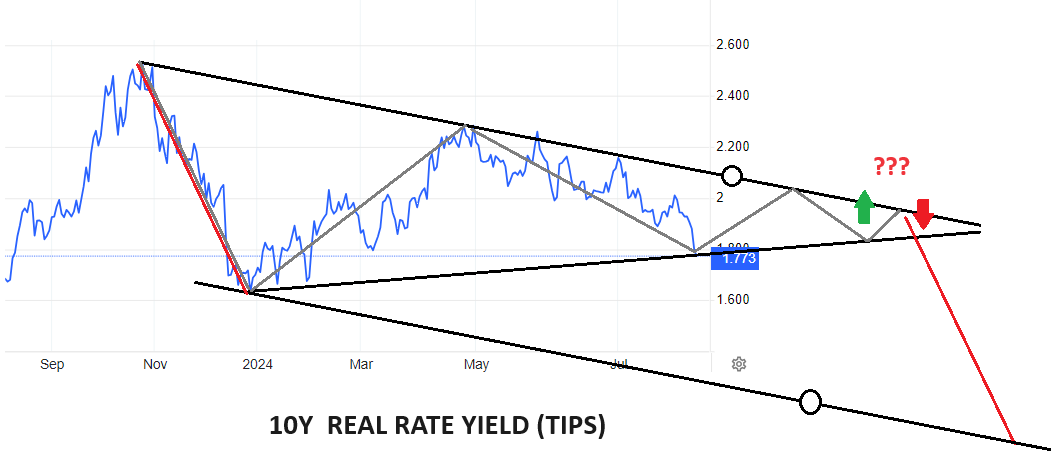

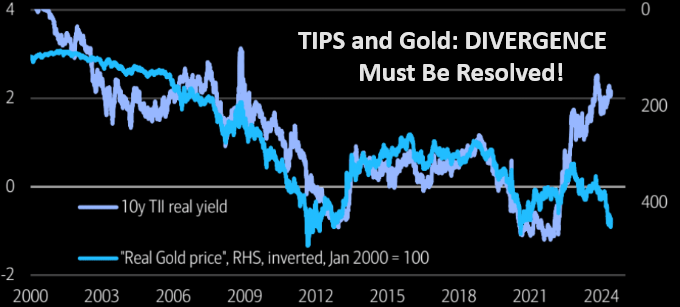

10Y REAL YIELD RATE (TIPS)

Real Rates bounced-off our support trend line. There are a number of alternative counts that could occur, with no alternative resolutions being possible (shown in the chart to the right). Developments in the coming week (FOMC Meeting) will likely determine the direction.

NOTE: Gold is suggesting it will be resolved by a fall in real rates (chart lower right) with rising Gold prices.

| |

CONTROL PACKAGE

There are TEN charts we have outlined in prior chart packages, which we will continue to watch closely as a CURRENT Control Set:

-

US DOLLAR -DXY - MONTHLY (CHART LINK)

-

US DOLLAR - DXY - DAILY (CHART LINK)

-

GOLD - DAILY (CHART LINK)

-

GOLD cfd's - DAILY (CHART LINK)

-

GOLD - Integrated - Barrick Gold (CHART LINK)

- SILVER - DAILY (CHART LINK)

-

OIL - XLE - MONTHLY (CHART LINK)

-

OIL - WTIC - MONTHLY - (CHART LINK)

-

BITCOIN - BTCUSD -WEEKLY (CHART LINK)

-

10y TIPS - Real Rates - Daily (CHART LINK)

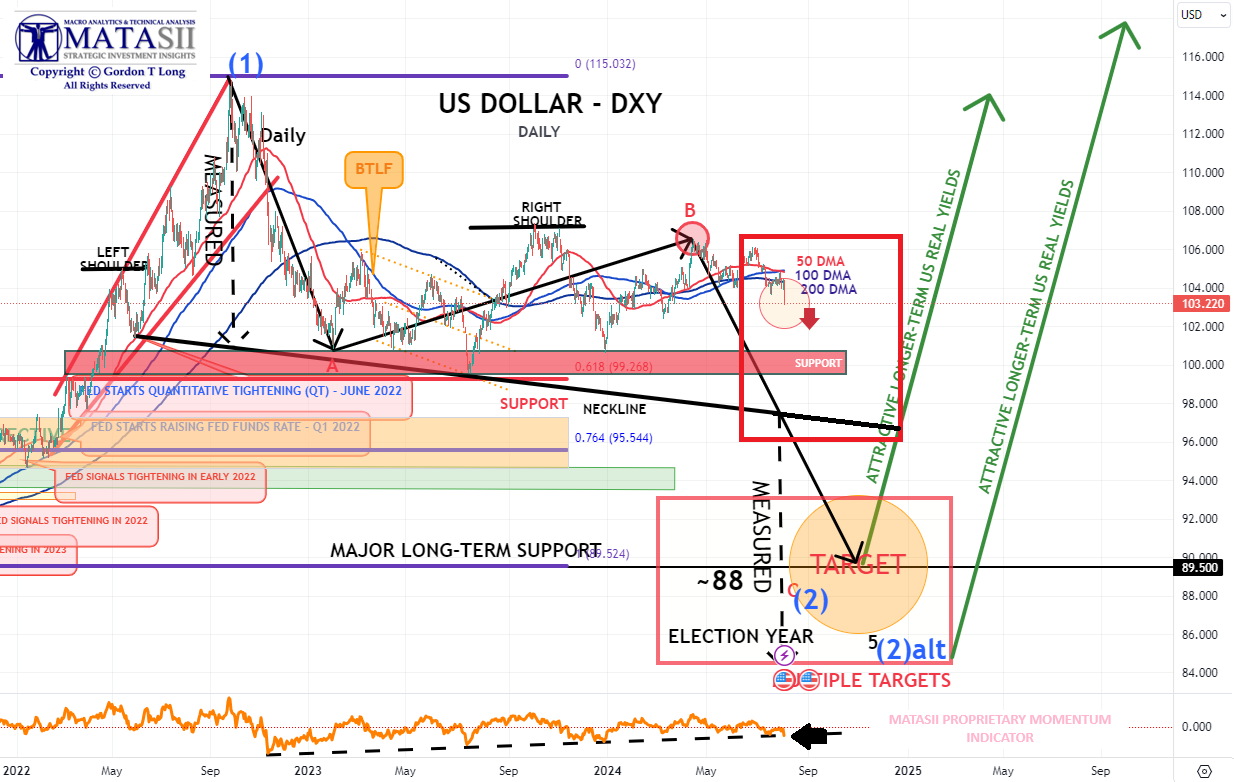

US DOLLAR - DXY

FRIDAY'S ACTION'S saw the Dollar Index markedly weaker, with the flight-to-haven trade ramping up after the US jobs report as Yen and Franc's strength sent the index lower.

- The Dollar was initially weaker before the US Jobs report, with losses accelerating once it was unveiled the US added way fewer jobs than expected, as well as the Unemployment Rate unexpectedly ticking higher by 0.2%.

- Fed pricing reacted extremely dovishly to the data, which added to US growth fears, as there is now 117bps of rate cuts by year-end (prev. 88bps).

- As such, bonds soared, with US 10y yields falling over 16bps, adding further pressure to the Buck.

- The dovish reaction was highlighted in Investment Bank projections, particularly Goldman Sachs and Citi, who now see a 50bps Fed rate cut in both September and November, alongside BofA and Goldman Sachs seeing additional rate cuts by year-end. Elsewhere,

- Friday saw Fed's Goolsbee reiterated the Fed's narrative, namely, they'd never want to overreact to one month's data, while Barkin noted the 114k jobs are still a 'reasonable' number, even if it marks a slowdown.

- Looking ahead, ISM Services PMI (Jul) on Monday acts as the next possible dollar catalyst, with US data release light for the remainder of the week.

- The Dollar should now be expected to fall as/if Fed Rate expectations are taken down.

- There are key lower support levels that should be expected to offer important support.

- The Dollar has found initial support at the longer term MATASII Momentum Indicator (lower pane black dotted line) - see black arrow.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

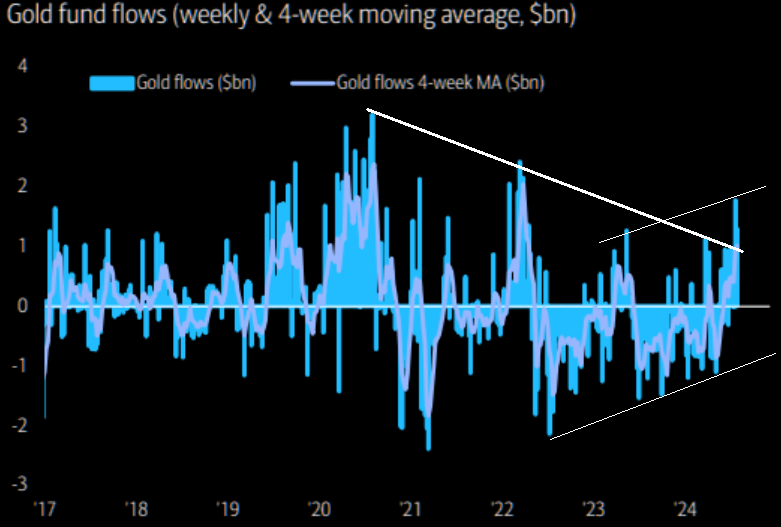

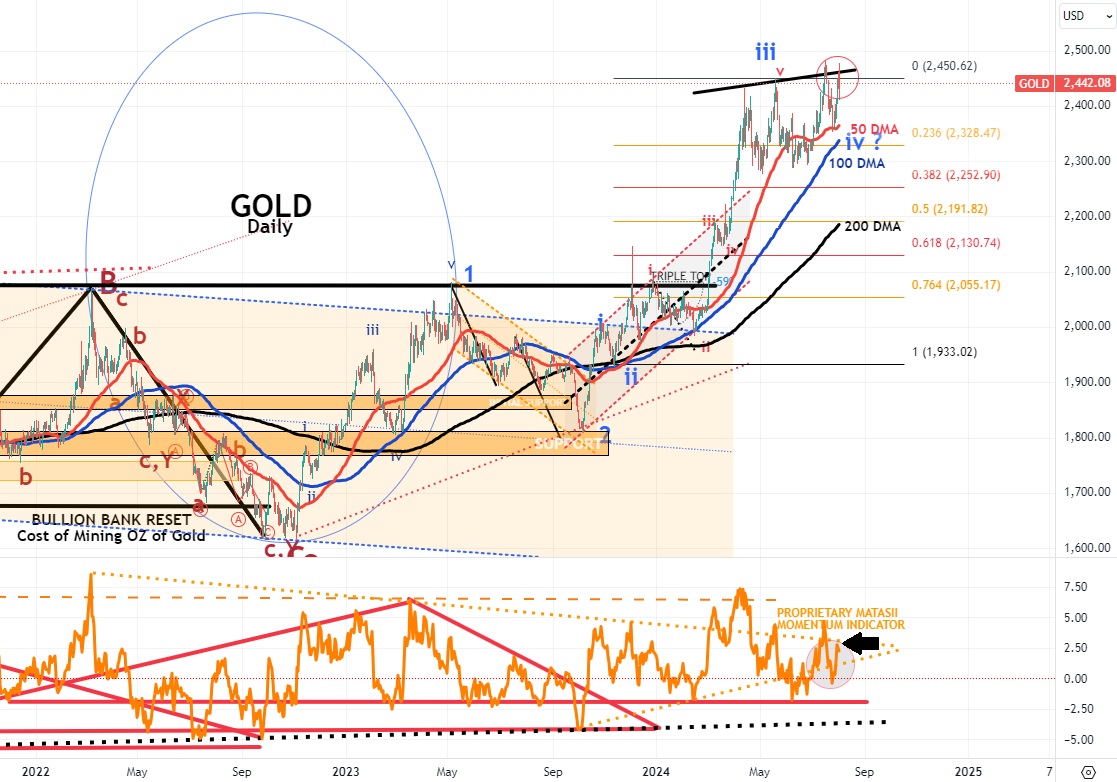

GOLD

CHART RIGHT:

We have just experienced the biggest 2-week inflow to gold since March '22.

CHART BELOW

- Gold tested its 50 DMA again at the end of last week before rising to our overhead resistance trend line (black line) this week.

- Gold normally rises with a weaker dollar, falls with weaker Yields and rises with falling real rates. Gold needs to see a resolution in a falling dollar potential and falling Real rates.

- It is concerning that Gold didn't rise more last week with major moves downward in the dollar and yields though Real rates fell. It appears gold investors are more concerned with US Real Rates versus US nominal rate movements.

- The MATASII Proprietary Momentum Indicator (Lower pane) is got in a momentum wedge.

- Gold likely needs stronger support at lower levels closer to a 38.2% retracement and the rising 200 DMA, before it breaks to the upside and through overhead resistance (black line).

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

CONTROL PACKAGE

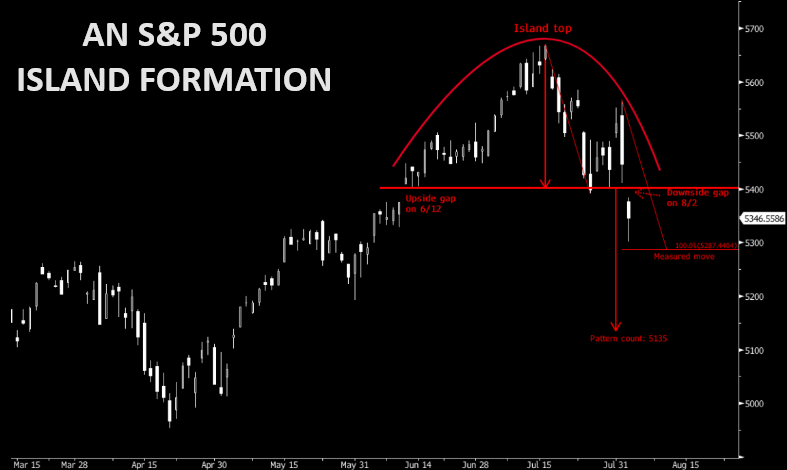

CHART RIGHT: Beware of the Island top Formation pattern in the SPX with downside projections at 5287 (measured move) and 5135 (pattern count).

There are FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set":

- The S&P 500 (CHART LINK)

- The DJIA (CHART LINK)

- The Russell 2000 through the IWM ETF (CHART LINK)

- The MAGNIFICENT SEVEN (CHART ABOVE WITH MATASII CROSS - LINK)

- Nvidia (NVDA) (CHART LINK)

| |

S&P 500 CFD

- The S&P 500 cfd held tight to its rising 21 DMA before falling at the end of the week to its 100 DMA on the US Labor Report.

- The MATASII Proprietary Momentum Indicator (middle pane) supplied initial support at its longer term rising support trend line. it is likely that a counter rally will happen next week.

- We wrote in our Mid Week Report:

-

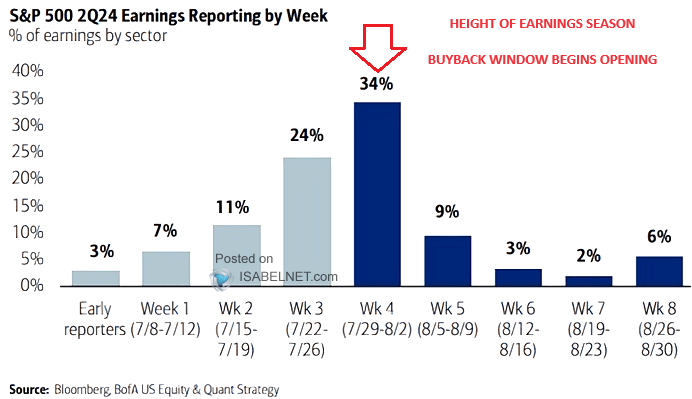

Note the rapid deterioration in the RSI (lower pane).This may be indicating a touch of the 100 DMA may still be ahead as the Q2 earning season unfolds further. Next week is the height of announcements.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

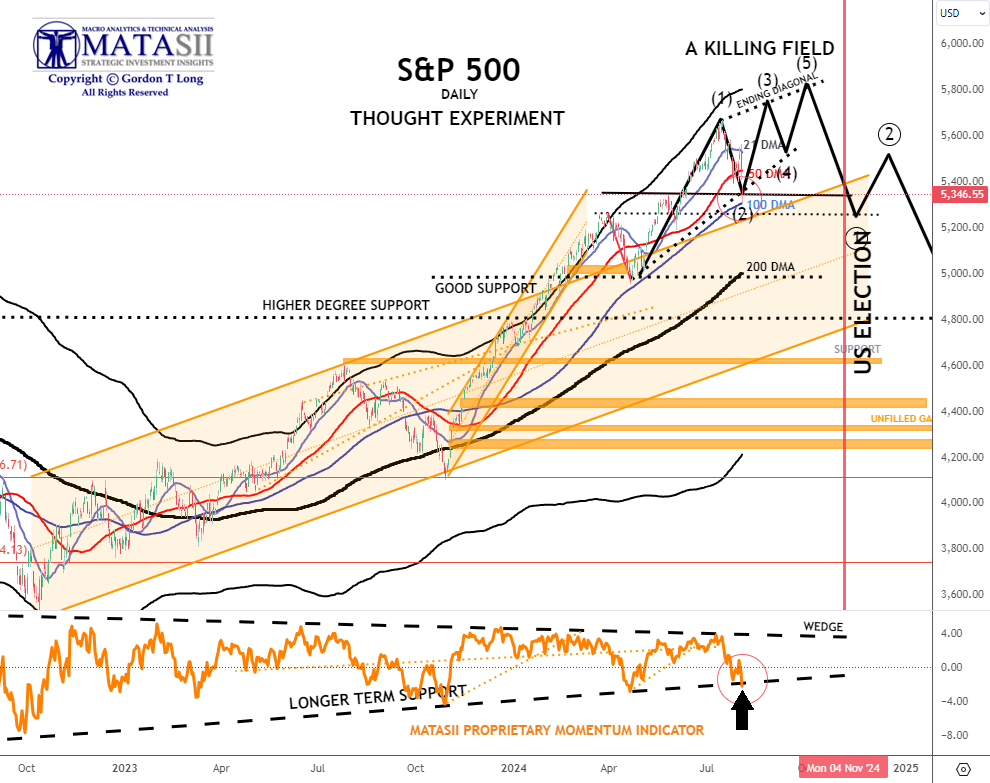

S&P 500 - Daily - Our Thought Experiment

OUR CURRENT ASSESSMENT IS THAT THE INTERMEDIATE TERM IS LIKELY TO LOOK LIKE THE FOLLOWING:

NOTE: To reiterate - "the black labeled activity shown below, between now and September, looks like a "Killing Field", where the algos take Day Traders, "Dip Buyers", the "Gamma Guys" and FOMO's all out on stretchers!"

WHY DID I CALL IT A KILLING FIELD?: "We remain in short gamma land. Dealers had to sell deltas into the 5450 support area during the July 30 move lower. The same dealers had to chase all that sold delta and much more at higher prices as they became shorter and shorter deltas as the market ripped higher yesterday. Today is another brutal day for the short gamma community as they have been forced to sell (at much lower prices) all that delta they bought yesterday. Add to it poor summer liquidity, and you realize why things are moving in an erratic way."

- The S&P 500 fell to its 100 DMA last week which offered initial support.

- The MATASII Proprietary Momentum Indicator (lower pane) appears to have supplied additional support (black arrow).

- Until a key event trigger occurs, the trend is still up and therefore a counter rally is likely next week.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

STOCK MONITOR: What We Spotted

| |

CONTROL PACKAGE

There are FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set":

- The 10Y TREASURY NOTE YIELD - TNX - HOURLY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - DAILY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - WEEKLY (CHART LINK)

- The 30Y TREASURY BOND YIELD - TNX - WEEKLY (CHART LINK)

- REAL RATES (CHART LINK)

FISHER'S EQUATION = 10Y Yield = 10Y INFLATION BE% + REAL % = 2.035% + 1.773% = 3.808%

| |

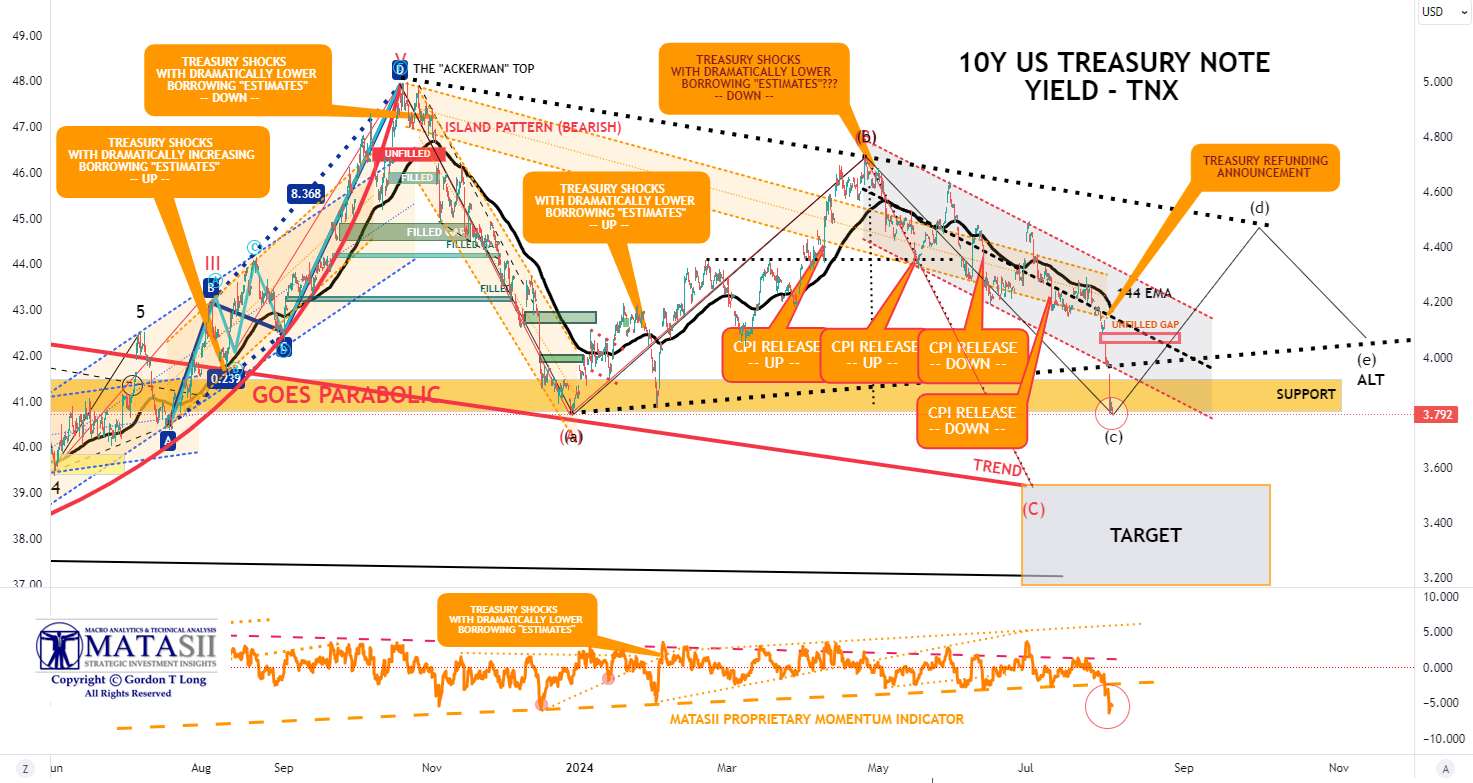

10Y UST - TNX - Hourly

there was significant risk-off sentiment and massive Fed repricing on Friday, which saw T-Note soar from 112-28 to 114-08 in an immediate reaction.

- As such, it sent the US yield curve from 2s through 10s convincingly below the 4.00% mark, with the 2yr yield knee jerking lower by over 20bp to a 3.89% base before slipping marginally further thereafter.

- Following this, Fed pricing moved very aggressively with 116bps of cuts now priced in by year-end, vs. 88bp pre-data.

- Following the data, a range of banks altered their calls, with JPMorgan now seeing a 50bps Fed rate cut in both September and November, while Goldman expects the Fed to dispatch an initial string of consecutive 25bps cuts in September, November, and December (prev. cuts every other meeting).

Jobless claims have surged, Manufacturing surveys have slumped, Construction spending has tanked ..... all creating growth anxiety which sent rate-cut expectations higher, bond prices higher and Yields lower!

- The TNX fell hard this week with the release of the US Treasury's Quarterly Refunding Announcement, comments from Fed Chairman Jerome Powell, ISM Manufacturing and Friday's highly disappointing Labor Report.

- The Momentum (lower pane) has fallen though longer term prior level lows. The Bond Market was in panic buy mode and Fed expectations that the Fed is maybe 100 basis point behind the curve.

- We are labeling a tentative Alternative ABCDE count that is inline with the movements in the Real Rate Yields (chart shown above).

QUARTERLY REFUNDING PREVIEW: The Treasury will announce next quarter issuance on Wednesday 31st July. At the last refunding, the Treasury announced USD 125bln of refunding for May, comprising USD 58bln in 3yr notes, USD 42bln in 10yr notes and USD 25bln in 30yr bonds. It also noted the "Treasury believes these cumulative changes leave it well positioned to address potential changes to the fiscal outlook and to the pace and duration of future SOMA redemptions". Adding that "Based on current projected borrowing needs, Treasury does not anticipate needing to increase nominal coupon or FRN auction sizes for at least the next several quarters. " Analysts at Wells Fargo expect coupon auction sizes to remain unchanged for the second consecutive quarter. Providing the Treasury keeps monthly auction sizes unchanged as expected, it is expected to maintain 2-yr supply at USD 69bln, 3yr at 58bln, 5yr at 70bln, 7yr at 44bln, 10yr at 42bln, 20yr at 16bln, 30yr at 25bln and FRNs at 28bln for August.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond ‘fair use’, you must obtain permission from the copyright owner.

========

| |

MATASII'S STRATEGIC INVESTMENT INSIGHTS | |

2020 VIDEOS OUTLINING THE COMING RISE IN INFLATION, STAGLFLATION & COMMODITY PRICES | |

IDENTIFICATION OF HIGH PROBABILITY TARGET ZONES | |

Learn the HPTZ Methodology!

Identify areas of High Probability for market movements

Set up your charts with accurate Market Road Maps

Available at Amazon.com

| |

The Most Insightful Macro Analytics On The Web | | | | |