|

AUD takes out the recent cyclical highs and dispersion readings remain low. Both are signs that the uptrend is not yet extended. We have noted here the leveraged shorts on the AUD before primarily from the macro community that sees Australia as a derivative bet on a disorderly unwind of China. This trade like the shorts in CAD had become stretched. It may well prove correct in the long run, but in the short term, it is proving both crowded and vulnerable.

|

AUD risk reversals losing their premium for AUD puts. As noted in this Research Note, the AUD dollar is a biased currency. It tends to appreciate in a corrective fashion with declining volatility, and decline impulsively with rising volatility. Because of this the odds of the AUD risk reversals moving through par, and in effect become bid over for AUD calls is low. However, if this were to happen, even in the front end of the curve it would be a good sign of trend exhaustion.

|

|

Above is the AUD rolling Dispersion indicator which unlike the same indicator for $-CAD, implies more trending price action in the near term.

|

|

|

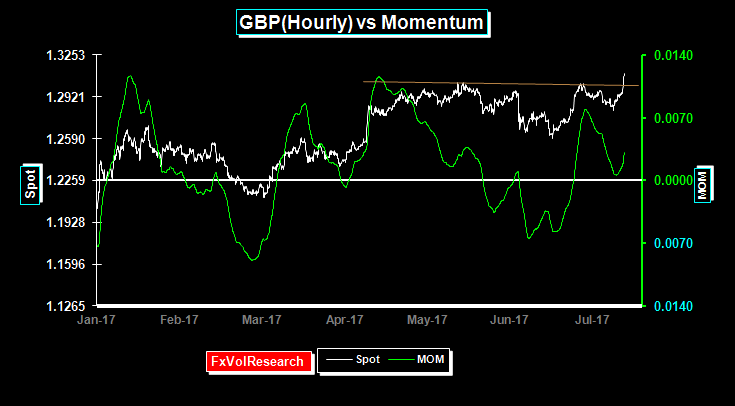

GBP punches through its previous tops however it does so without the corresponding rise in momentum. One has to attribute some of this recent GBP strength to the growing view that a so-called hard Brexit is off the table. However, it is hard to see the confusion in the UK government diminishing any time in the near term. Cable is likely to remain volatile and shorting GBP vol is ill advised. There is also the view expressed in some quarters, that Brexit will not really happen or rather that the negotiations will drag on for so long that they will seem less relevant particularly if Macron and Merkel are able to make changes to the EU constitution that makes EU membership more attractive to the UK. This idea may seem far fetched but it may not out of the question as it is extremely unlikely that the negotiations can be concluded before the two-year dead line.

|

| Similarly the EUR is holding on to the hourly trend line while we are seeing clear signs of short term momentum divergence. |

As pointed out here last week the CHF is threatening to break out of it consolidation patter while at the same time the dispersion readings have remainled low. As the bounderies of dispersion narrow the volatility is compressed further and is now approaching levels where the CHF is likelly to start to trend.

|

|

We are not far off a buy signals in the 3M and 6M periods of the CHF curve. This is the time to sit on the

bid

for 25-20 delta strangles. As is our preference it is best to just let the market come to you rather than to pay the bid-ask spread. It also makes sense to stagger orders over time in order to gradually build up a long position. We are not far off major historical lows in the CHF implied vols and the probability of success with this trade are high.

|

|

|

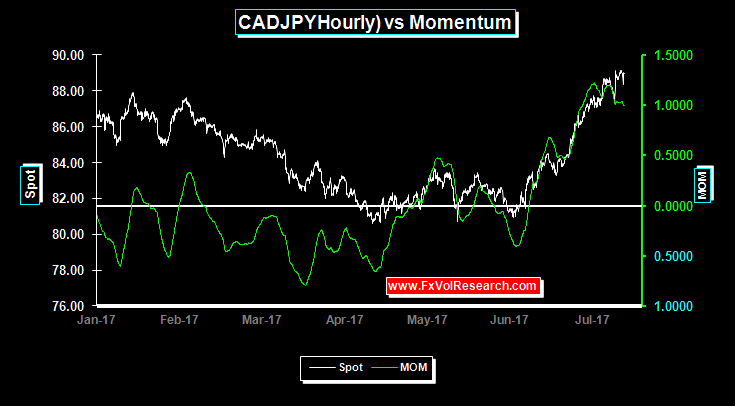

Signs of short term exhaustion in CADJPY. Last week it looked very much as if the JPY was breaking out of a long term symetrical triangle formation. However this reversed sharply on the week and proved a false dawn. It may nevertheless proove correct in the long term. The FX market sold the dollar off at the end of last week on what was seen as inflation readings well below expectations. This may well be the correct response in the short term. However down the road the market, and the JPY in particular, will have to overcome the consequence of the Fed's balance sheet tightening.

|

|

Again, in a week inwhich the CAD continued to rally the risk reversals moved in favour of USD$ calls. At the same time front end vols from the one month on out edged lower. That confirms the suspicion expressed here last week that the market is moving into an area of long strike inventory. It should be noted that this is the contrary price action to what we noted above with respect to the AUD, suggesting, that the FX market is more dangerously short AUD than CAD.

|

|

|

Momentum indicators on CAD are now very oversold but not yet showing any signs of divergence. Indicators based on the correlation of implied vol and spot are suggesting further that that the CAD dollars upside from here is far more limited. However, before implementing any counter-trend trade it would still be prudent to wait until the rolling Dispersion has peaked. When this does occur, I would have a look at a butterfly trade for DEC expriation. For example, Buy the DEC 81 CAD put, sell twice the number of DEC 76 Puts, and buy one time the 71puts. This trade can be implement at roughly a cost of 174 tics, with a break even expiration rate of 79.26, or 1.2616. If the spot remains range bound the 81 puts will actually have some positive decay because of a small pick up of the forward points and because of their higher delta. This is not a trade you would likely hold to expiration but would unwind based on a move back to 6% in the vols and the spot back up to the short strike at .7600 or 1.3150 area. The maximum profit is the difference between the strike (500points) less the premium paid. The max loss is the premium paid.

|

|

Copper vols are drifting lower as the spot slowly grinds higher. Admittedly, the commodity bloc currencies, CAD and AUD, may be getting some muted support from commodity prices but in general, but the price action as exemplified by copper above, has been characterized by broad consolidation and volatility compression.

Copper trending slowly higher is consistent with the evidence of a synchronized global recovery, but it is hard to find evidence, so far at least, a long term secular bull market. Global reflation is intact, but the lack of strong momentum in commodity prices suggest that the global recovery is still fragile.

|

|

Links to previous FxWeekly Short Version

|

|

Research Director

Direct: 604-685-4414

skype: jamesrider1

Join the FxVol Free Weekly: here

|

|

| |

|

|