|

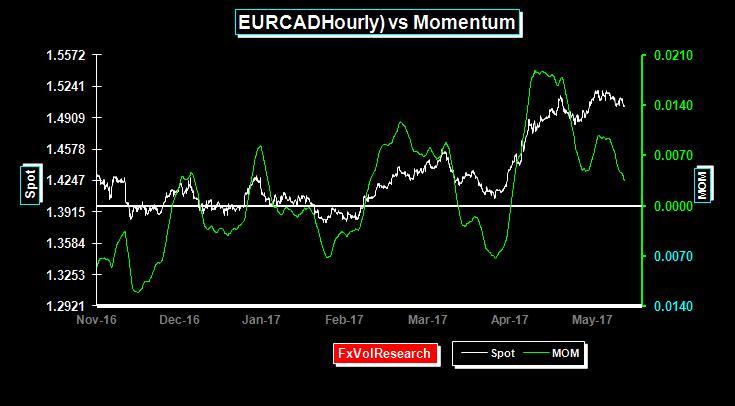

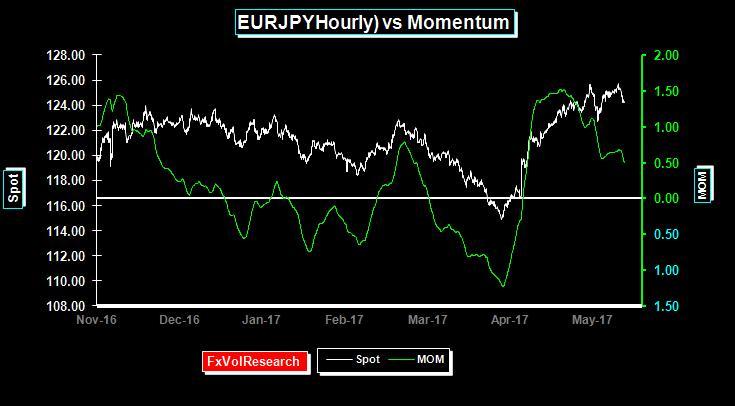

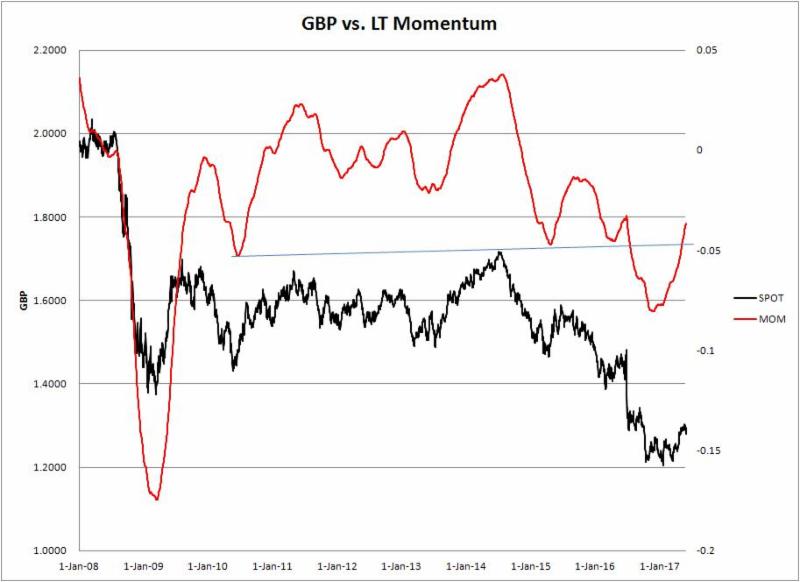

Momentum divergence is a useful indicator, more so than momentum on its own. Using signals generated from simple momentum indicators generally produces a profit and loss account than mean reverts over time. However momentum divergences, in our view, have a better track record in identifying countertrend price action.

|