|

TARIFFS, TARIFFS, TARIFFS

Kurt Haarmann

| |

It’s safe to say that if you have been upright and breathing over the past month, you’ve heard plenty about tariffs. It was well known before the election that President Trump favors the use of tariffs as both a foreign policy motivational tool and a means of domestic revenue generation. The market widely expected to see some action on tariffs under the Trump Administration. However, the pace, depth and volatility of their announcement and application has kept heads in the market spinning, as growers, buyers, sellers and processors try to keep up with the latest development. Here is a brief discussion on tariffs without getting into the specific levels of each tariff on each commodity, good or service, as these are literally changing by the minute. What was true when this was written could be completely out of date by the time it is read.

There has been a lot of discussion in popular press and on social media as to the impacts and effects of tariffs in general. Each side of those discussions is going to state things in absolute terms to bolster their case. This is true of both statements: “Tariffs are a tax on the consumer” and “Tariffs are paid by the exporting country”. As is usually the case, the truth lies somewhere in between and is usually based on what the market will bear. In a market where there is little competition or replacement for a good/service, and high static demand, the tariff becomes a tax on the consumer, as virtually all of the tariff cost will be passed along. In a situation where there are ample alternatives, or very price-sensitive demand, the tariff will either be subsidized by the exporter, or the amount of those goods/services being imported will decline to a point that end price can absorb the tariff.

Agricultural commodities are no different in terms of their application. For a product like Avocados, there is very little domestic production, and an inability to increase domestic production (growing conditions) combined with a real inability for Avocado growers to absorb the price hit, so any import tariff on them will be passed directly to the consumer or the products won’t be imported.

Wheat, Corn and Soybeans are each a little different. These commodities each compete in a global market, and while they have significant domestic demand, they still require large export bases to maintain current market prices (at any given time). If a 25% tariff is imposed on Canadian Wheat, it will lead to less imported Canadian wheat for domestic US milling and the price of US Wheat will rise nominally. The price rise in the US will also make Canadian Wheat more competitive overseas and US Wheat will lose export market share commensurate with the amount of domestic market share it gains. The total of domestic and international demand (and supply) remains unchanged in a zero-sum game; the only thing that changes are the supply channels.

In the case of Corn, the major threat to exports would be retaliatory tariffs from Canada, Mexico, Japan, Korea or Taiwan. China would play a much larger role if they were importing a lot of corn, but they currently are not. Assuming that issues with Japan, Korea and Taiwan can we be worked out, the big threat is Mexico. It is difficult to imagine significant tariffs going into Mexico, because theirs is a market where the costs of tariffs would have to be passed directly to the consumer. Their government cannot afford to subsidize the cost. The government of Mexico is also not likely to endorse any plan that would lead to food price inflation; this last year proved that food price inflation is very politically unpopular both here and abroad.

Soybeans exists in another place altogether. Despite sizable increases in domestic crush capacity linked to biofuels, the Soybean crop throughout the US, but particularly in the north, relies on a solid export program to underpin demand. We have seen the tariff/trade war scenario play out in Soybeans before, most notably in 2018 and 2019, when China did everything in its power, including import tariffs, to buy Soybeans from any other country than the US. The difference this time, is that the trade disruption will occur in a market where US growers already have record South American Soybean production as competition. Should China choose to proceed in a fashion similar to previous year, it will be much easier and cheaper for them to execute the plan this time.

As always, if you have any questions regarding the current state of affairs (meaning literally that minute), please do call your local elevator manager, buyer or merchant. At Columbia Grain we are well experienced at dealing with these issues and we are here to help support our growers through these volatile and challenging times.

|

|

|

AGRONOMY

Blaise D Boyle, Seed Division Manager

| |

Importance of Using Certified Seed – Blue Tagged

Have you ever wondered why it is recommended to purchase certified seed? Do you know, what is the purpose of that blue tag that says “certified seed” sewn on the seed bag you are wanting to buy?

This time of year, brings about numerous challenges and decisions that all growers go through in preparing for the growing season. One critical decision being what seed do I purchase this season! After all, high quality seed is one of the critical first inputs for CGI’s growers to boost both their operations yield and productivity.

What’s the Purpose: Seed that carries the easily identified blue tag, properly identifies varieties as being true to type with high-quality purity standards for anyone who handles, grows and distributes this product. This tag provides quality assurances that growers look for when purchasing their seed.

Why Buy Certified: Good crop production begins with planting the highest quality seed possible, and using seed that has been certified assures you the grower that you are getting the best possible third-party assurance of high-quality seed. Although standards do vary from crop to crop and from state to state, a blue certification tag on a bag of seed is the symbol of quality. It assures you, that the seed inside the bag is the variety stated and has met the standards for both Germination and Purity.

Deciding what to plant and the different seed choices available are not easy, especially with the uncertainties of today’s ag climate. Just be assured that you are always making the right choice if the seed you buy has the Certified blue tag.

At Columbia Grain we are here to help, don’t hesitate to reach out to either Madison Fritz or myself and together let’s get your season off to the start it needs.

|

| |

|

INTERNATIONAL

Wiley Wang, Merchant

| |

|

|

Global commodity market is closely watching the USTR’s investigation in Section 301 of China's Targeting of the Maritime, Logistics, and Shipbuilding Sectors for Dominance. It is important to balance global shipping market with more diversified ship building capacities; but the proposed actions will put a lot of pressure for nearby logistics if it takes effect.

Black sea wheat is taking market shares for July and onwards; Australian wheat is very competitive in SE Asian markets. Canadian is maintaining their sharp price in comparison to our spring wheat. Global price for the very low end of the quality spectrum is increasing, but for the higher end continue to decrease. With the uncertainties in trade relationships, we are all hesitating to push more sales thus creates more room for our competitions.

Korean buyers appear to have completed their corn purchases for the APR shipment, with their next positions moving to May shipment. Despite a significant drop in freight rates this week, Korean buyers, like their Japanese counterparts, are still in a wait-and-see mode. Due to disruptions in shuttle operations, PNW ports are experiencing vessel congestion. Exporters are maintaining higher elevation margins as the impact on May shipments remains unclear. With Argentine FOB prices increasing by over 20 cents, PNW corn still maintains competitiveness for Asian destinations.

The soybean export market remains quiet. Following China's import ban, the three major companies need to adjust their strategies. Brazil's harvest has caught up, making their soybeans competitive in the market. Under these circumstances, there are no sales from PNW, with strong domestic demand becoming the main destination. The US-China trade war presents a different temperature compared to other countries, and it remains to be watched how long this situation will continue.

|

| |

|

Ryan Statz, Merchant

HARD RED SPRING WHEAT

| |

|

Risk off mode for the wheat market as of late has dominated the tone. Markets don’t like uncertainty, and we are getting that in heavy doses. Our new tariffs on China, Mexico and Canada have been met by retaliatory tariffs from Canada and China. We will wait and see on Mexico and if there is any easing on tariffs with China and Canada. The market does not know what the future brings, and it’s become a sell first, ask questions later type of market. The downturn in the board has completely shut off producer selling but the pipeline was very full following the last rally. We will need to see improvement in the board in coming weeks or basis will have to do heavy lifting in a period that the producer wants to get in the field. The US may need to backfill Canadian sales into the US market which had been very aggressive the past 60+ days. This could buoy eastern premiums relative to west, but my concern is Canadian wheat being shifted to Vancouver which will hurt US exports. The Dollar has relaxed, and inflationary fears have set in as well as some rumblings about potential US recession. For now, it’s wait and see but this market will need demand to completely change course. Cash prices are attractive to international buyers however the Canadians continue to take swing demand away from the US and higher BNSF secondary freight rates have hurt the US market. Protein premiums in the west have condensed but if Canadian 14s and 15s stop entering the market we may see a resurgence in protein upside that could be short lived going in to new crop as the vast majority of PNW and Domestic business is late May forward. |

|

- The old adage, “high prices cure high prices”, seems to have rung true, albeit in quicker fashion than most would have anticipated.

- Futures are down .70/bu from their February highs.

- Basis levels are also down .30-.40/bu from their February highs.

- Simply put, in this time period, the market received an overwhelming amount of new supply from growers. Much more so than could be sold due to prices being considerably higher than buyers were willing to take on. Demand was rationed and the market needed a reset as we work towards incentivizing demand once again.

- Now, at considerably lower flat prices, the market is starting to see interest again from international and domestic mill buyers. The big question now becomes, how much coverage is left?

- In addition to milling interest at these levels, HRW prices have also inched closer to pricing into feed wheat business for certain quality/protein markets.

- Will the milling and feed interest in conjecture be enough to tighten markets back up to see a price uptick, or has enough buying coverage been sought?

- Like ‘high prices curing high prices’, will ‘will low prices cure low prices?

- This remains the million-dollar question that all are trying to find answers to.

- In addition to futures action, the market continues to watch:

- Rail Freight / Transportation

- Global crop conditions/turmoil – particularly Russia/Black Sea

- World ‘feed’ markets.

- USD currency firmness

- Tariffs

|

| |

|

WHITE WHEAT

Steve Yorke, Merchant

| |

|

The downward spiral continues for the grain markets. Uncertainty with tariffs and a round of fund liquidation leading the way. Currently the U.S. is having to discount their grain to make it appealing to some buyers. How long this will last is any one’s guess. The easing of levies is the talk this morning but at what level and when remain unanswered. Weekly export sales for wheat were in line with expectations. White wheat didn’t have any surprises so to date this put’s exports at 199MBU. USDA’s export number for this marketing year of 220MBU appears to be in play and will help tighten what was once a burdensome carry out for white wheat. We are closer to 50-60MBU at this time, using USDA’s current export estimate. Australia is getting more aggressive, and this should be the pattern for the next 5-6 months so watch for lighter exports on the white wheat side, especially into Korea. The feed cargos that were once trading out of the PNW are most likely gone for the moment. One thing to keep a close eye on moving forward will be white wheat basis levels. I see lots of volatility in the months ahead. Chicago wheat especially should see wild swings which could create some opportunities to lock in basis levels that we have not seen since early last year. Keep in touch with your local office and have orders placed so rallies in futures and basis are captured. |

| |

|

PULSES

Cameron Underwood, Merchant

| |

|

|

PEAS

Peas have received full clarification on India import policy in regard to yellow peas. Import will be restricted, and India will go back to only using local production. In 2024 India imported 3 MMT of peas (110 million bushels), going forward this supply will need to find new markets. For yellow peas to price into China feed markets, pricing will need downward movement. USAID has not shown any signs of a quick return and lack of business into this channel could hurt domestic values for yellow peas in USA. Potential Canadian tariff could be supportive of USA yellow peas by stopping the import of Canadian peas. Green peas continue to be firm in both current and new crop as supplies continue to be low and pea acres have heavily swung to yellow peas.

CHICKPEAS

India harvest has begun, and market has felt downward price pressure from the increased acres. India market has offered down on Kubali market in hopes of quickly moving volume from the said to be large crop. USA stocks continue to build as exports in 2024 crop have been very poor to this point. USA has heavy imports of average 70,000 MT from Canada that could be heavily affected from tariff. Mexico crop is increased in acres but large concerns of yields and caliber with hot and dry conditions persisting.

LENTILS

Current crop lentils continue to hold firm footing as green lentil exports continue to be large from USA. India has gone quiet but other regions globally are working to catch up on purchases with India out of the market. Pricing spreads between current crop and new crop continues to widen amid speculation that new crop acres will be increased in both the USA and Canada while old crop remains difficult to buy.

DRY BEANS

Markets are on the defensive with US/Mexico/Canada/China tariffs going into effect on 3/4/25. The next focus is on potential Mexico retaliatory tariffs and further escalation of a trade war. Claudia Sheinbaum, the Mexico President, has long voiced that trade tariffs with the US hurt both the US and Mexican economies and that she does not see the justification. A further escalation in trade war with Mexico will create currency volatility, something the Mexico economy is extremely vulnerable to. There is a sizeable Mexico Pinto and Black Bean export program executing right now that will be at risk. The next USDA report will be the Prospective Planting report on 3/31/25 which will show the market the first glimpse of potential New Crop Supply & Demand.

|

| |

|

BARLEY

Matthew Schorn, Merchant

| |

|

|

Tariffs Update

As of March 4, 2025, the United States has imposed significant tariffs on imports from Canada, Mexico, and China. Canada has retaliated and imposed a 25% tariff on $20 Billion dollars’ worth of goods, with another $100 billion to come into effect in 21 days.

- US feed barley exports to Canada have halted as a result of the tariffs, which has had an immediate impact on the price of feed barley in Montana. Alternative barley markets for Montana grain are bid at a discount to the Southern AB feed market.

- Both buyers and suppliers are hopeful that a long-term resolution to these tariff discussions will be reached, however, the market remains extremely volatile.

Malt Demand and Price Trends

Malt demand remains limited with no participation from buyers in both the old and new crop positions.

- Prices continue to decline as the market adjusts to this sluggish demand, and in many cases, there are no bids for nearby delivery periods.

- Malt-feed spread narrows as malt barley looks for alternative outlets as quality comes into question.

- Consumer preferences continue to shift away from beer, with increasing interest in wine, seltzers, and cannabis products.

Canadian Domestic Feed Market

Domestic feed values in Canada remain flat, with the Canadian feedlot well covered for March and April requirements.

- Feeders have been cautious in placing new cattle orders and are struggling to buy replacement cattle from the market.

- Drop in corn futures has made imported corn competitive in the feed ration, but 25% tariffs on US corn exports to Canada push demand back to Canadian domestic barley.

- When the US dollar strengthens against the Canadian dollar, Canadian buyers lose import purchasing power, making US corn and barley more expensive compared to locally. The inverse is also true, as we have seed the Canadian dollar come off the lows in recent sessions.

|

| |

|

Joe Foley, Merchant

SOYBEANS

| |

|

|

Prices have dropped some 50cnts/bu. since our last update, under the weight of a massive Brazil soybean harvest along with the general selling off of assets in grains, equities, etc. Expect, at a minimum, heightened volatility going forward, with the latest tweet often starting and then crushing rallies. Harvesting in Brazil is just passing the 50pct completion mark, with most estimates still calling for 170-173mmt of production. The most recent USDA projection is 169, vs. last year’s 153mmt crop. Accordingly, we are expecting acute export competition from Brazil all the way thru 2025 for the PNW exporter, before even throwing in trade war discussions.

The stop and start nature of the current tariffs and retaliation is making it almost impossible to conduct business, which if it persists, will sharply curtail U.S. access to foreign markets. Lower, if not sharply lower prices are certainly plausible. In addition to above, the market will be increasingly attentive to new crop acreage prospects here in the U.S. The USDA February outlook forum is calling for 94 million corn acres and 84 million acres for soybeans, up 3.4 and down 3.0 million respectively for the 2025 crop. The all-important march1 grain stocks and prospective plantings reports will be released later this month which can always move markets, but frankly the above daily macro drama is overshadowing everything at the moment.

| |

|

Corn futures have been pounded lower, following the seemingly daily talk of implementing tariffs, retaliatory tariffs, and then delaying the implementation. There was always the risk of a violent move down in prices with managed money long some 350k contracts; All that was needed was a call for the exits, and the current state of our export markets certainly is providing that. We will see tomorrow on the weekly commitment of traders report how much fund selling occurred thru March 4th but certainly expect at least 100K contracts. In South America, row crop harvests are under way with Brazil some 35pct harvested of their summer corn crop, and Argentina is just getting underway.

Safrinha (winter corn) acres are nearly 70pct planted in Brazil which is about 10-15 pct ahead of normal, and the market will be watching carefully how the weather forecasts come to fruition, as this 2nd corn crop in Brazil will largely determine how much Asian business they capture, typically August thru November. Volatility is likely here to stay with U.S. planting ideas, weather and the macro craziness all coming into focus. It’s probably a good idea to have limit orders and stop orders in for cash pricing.

|

| |

|

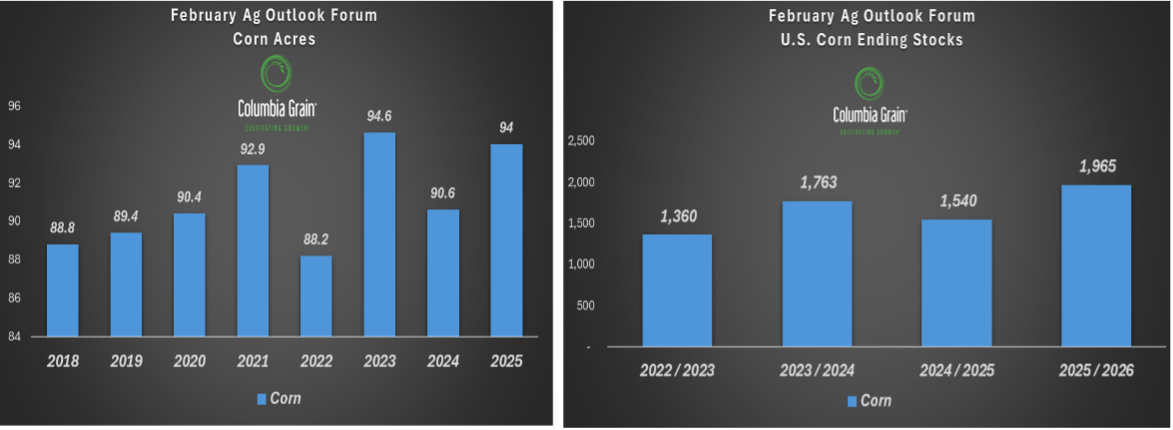

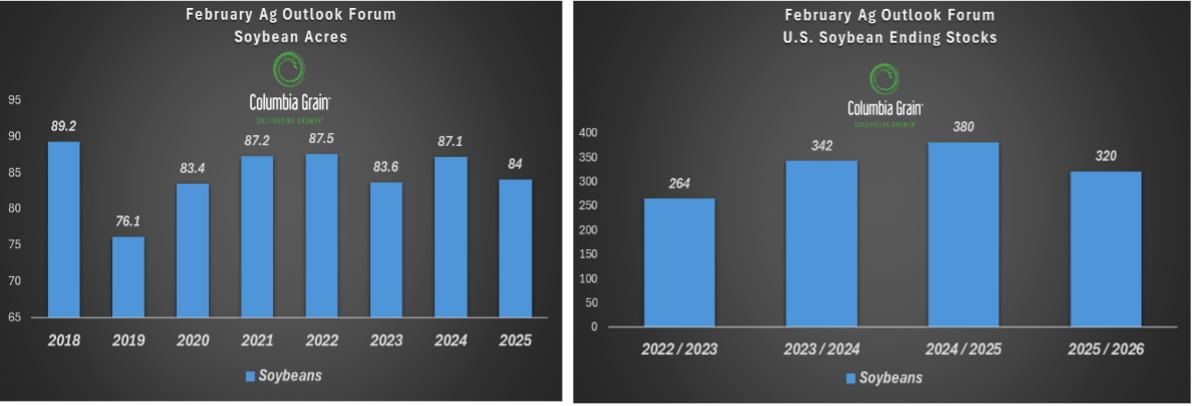

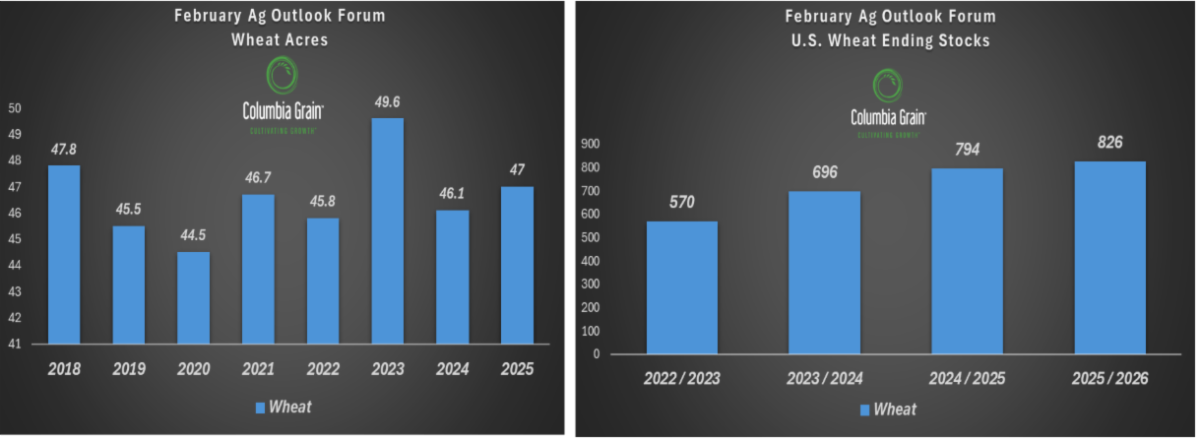

It’s almost time to spring the clocks ahead which means cabin fever is starting to really set in and we are all itching to get out to get some field work started. It also means we will be officially turning the corner to look at new crop planting intentions in the U.S. Last month, on February 27th the USDA held their 101st annual Agriculture Outlook Forum in Arlington Virginia. This is the event that gives us a first blush in terms of what we may expect in the coming year(s) from the USDA. I wanted to re-cap what was released and the implications it has had on the futures markets so far.

Now, it is important to remember this is their first blush at new crop estimates and nowhere near the final numbers, we will also see the March Planting Intentions report released on March 31st so there will be a lot of anticipation to see those numbers again this year. Futures markets have globed onto the Ag Forum numbers and are heavily trading them. The market action as of late can be attributed to a double whammy between the Ag Forum outlook numbers and coupled with uncertainty that continues to hit the market in terms of potential trade implications or trade wars, so more to come on that and something to have on the front burner to pay attention to. The initial thoughts released at the Ag Forum are to see more Corn acres this coming year along with less Soybeans area planted and slightly higher all Wheat acres (but less spring wheat acres potentially).

| For corn they are anticipating seeing acres come in at 94 million, this would be a 3.4-million-acre increase compared to last year’s numbers, but right back in line with the 2023 corn planted numbers. With the potential increase in acres this could result in the U.S. carry out stocks for corn to be increased from 1,540 billion bushels to 1,965 billion bushels. Now, it is important to remember that this is with the U.S. corn crop yielding 181 bu/acre (which would be a record high yield) so we do need to take these numbers with a grain of salt as they still are just estimates. As a result, we have seen the markets for new crop corn come down roughly 40 cents from the most recent high of $4.80. | For soybeans, we are seeing the opposite of corn in terms of potential acreage this coming year as the crop economics favor corn acres to soybeans. As a result the Ag Forum released a potential soybean planting number of 84.0 million acres, compared to 87.1 million acres ( a reduction of 3.1 million acres from last year). So easy to see that most of those soybean acres from last year will potentially shift over to corn acres in the coming year. With this the potential ending stocks of soybeans in the coming year could decline to 320 million bushels, down from the 380 million bushels that we are looking at for this year. It is interesting to see new crop soybeans have dropped close to 70 cents from the most recent high given the potential for a reduced acre, which would be counterintuitive. This most recent decline in soybean futures is more attributed to the uncertainty that is around with tariffs on the horizon along with the enhanced competition that we will be facing from South America soybean production. | |

All wheat acres are thought to come in at 47 million acres, which would be up slightly from lasy year but anticipating seeing fewer spring wheat acres in the coming year. As a net result the Ag Forum released their wheat balance sheet ideas posting a U.S. carry out number of 826 million bushels in the coming year. This would be an increase of 32 million bushels form the number that we are anticipating seeing at the end of the 24/25 marketing year of 794 million bushels. With this we have seen the Chicago September wheat futures trade down close to 80 cents since the most recent high.

We have seen the overall grain commodity complex trade lower over the last few weeks given the potential for new crop acres. There is a lot of time and weather to still play into the markets as the seed isn’t even in the ground yet. But this once again highlights the importance of getting your marketing plan built early to take advantage of pricing opportunities when they arise. And maybe more important this year to look to use stop loss orders to give yourself some kind of a safety net under the markets in the event they turn lower again.

Be sure to reach out to your local manager and buyers to get your orders working to take advantage of any knee jerk reactions we may have on the horizon and the weather markets and potential seeded acres are still to come.

| | |

|

Sean Ferguson, Merchant

CANOLA

| |

|

|

ICE canola futures have backed off recent highs the past week since the enactment of 25% tariffs on Canadian and Mexican goods. The tariffs placed on Canada will prove detrimental to many Canadian markets, one being the Canadian canola crush market. The US is by far the largest consumer of Canadian canola oil, which leaves Canadian crush companies scrambling to find additional domestic and/or alternate export demand for their canola oil. Expect Canadian crush facilities to continue operating at minimal capacity in efforts of minimizing losses. On the bright side, margins at US crush facilities will continue to be supported as vegetable oil buyers will look to buy product domestically. The market will continue to wade through uncertainty as we go forward. The unknown of timing on a resolution puts the trade in a tight spot. Do Canadian oil merchants look to sell into alternate exports markets, or do they continue to wait for a tariff resolution?

CGI is excited to announce a non-GMO canola Act of God contract. Contract specs include 20 bu/acre AOG on dryland and 40 bu/acre AOG on irrigated land. Experience the yields of commodity canola with the benefit of a healthy non-GMO price premium.

Planting seed is available for purchase. Please contact your local CGI representative for more information.

| |

|

The flax market continues to trade flat this past week. US buyers reached into Canada for nearby coverage prior to the enactment of tariffs; with their nearby coverage, US buyers stepped back to wait and see how everything unfolds. With the disconnect between the US and Canadian market, we can expect US flax to remain steady and Canadian flax values to weaken. Without the US market, Canadian flax will have to ration price to work into alternate export channels, or back into the US net of tariffs. Increases in flax prices globally will be capped due to ample stocks remaining in the Black Sea as well as expected flax acreage increases YoY in Kazakhstan and Russia. Canadian flax will continue to be in a tough spot if international buyers continue to comfortably buy out of the Black Sea and the US continues to longer be a viable option for Canadian flax.

CGI’s flax AOG pricing has now been released. Contact your local CGI elevator for up-to-date pricing.

|

| | | |