News & Updates

November 6, 2024

| |

|

Inflation Adjustments for 2025 | |

As the end of the 2024 calendar year grows near, many individuals begin to reflect on this past year in efforts to prepare for the 2025 New Year. As of October 22nd, 2024, the IRS released their annual inflation adjustments for the 2025 tax year (2026 filing year). As year-end tax planning approaches, understanding these key changes could help taxpayers comprehend where they stand for the upcoming tax year and allow plenty of time to make necessary adjustments to maximize potential tax saving opportunities. Let us take a look at the potential upcoming adjustments. | |

|

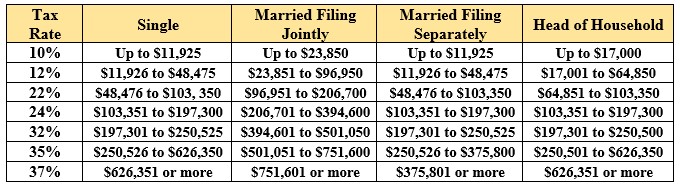

Changes in Personal Income Tax Brackets & Tax Rates

The chart below displays the new 2025 income levels matched to their tax bracket. All 7 tax rate percentages remain the same.

| |

|

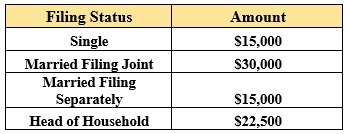

Increase in Standard Deductions

For 2025, the Standard Deduction amounts have increased for each of the following filing categories:

| |

The additional standard deduction amount for the aged or blind taxpayer is $1,600. ($2,000 if unmarried) | |

|

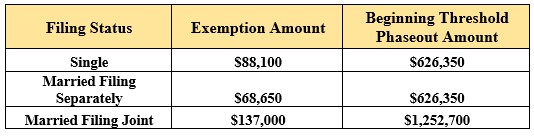

Alternative Minimum Tax (AMT)

The AMT exemption amounts for the 2025 tax year are:

| |

| |

Tax Credits & Itemized Deductions

The adjusted changes for the following 2025 tax credits and itemized deductions are:

-

Child Tax Credit – The CTC will remain the same at $2,000 with a refundable amount of $1,700.

-

Earned Income Credit – The maximum amount available to qualifying taxpayers with no children is $649, for those with one child is $4,328; for taxpayers with two children is $7,152, and for taxpayers with 3 or more children is $8,046. Income phaseouts do apply. For taxable years beginning 2025, you won't be eligible for the EITC if your investment income exceeds $11,950.

-

Adoption Assistance Credit – The credit allowed for an adoption of a child with special needs is $17,280.

-

Health Flexible Spending Arrangements – the dollar limitation for employee salary reductions for contributions to a health flexible spending arrangement increases to $3,300. The maximum carryover is $660 for cafeteria plans that permit the carryover of unused amounts.

-

Foreign Earned Income Exclusion – The foreign earned income exclusion amount is $130,000.

-

Educator Deduction – The deduction amount that eligible educators can claim for books, supplies, computer equipment and other supplies is $300. If the taxpayers are married and filing jointly, and are both educators, the maximum amount they are able to claim is $600.

-

Medical Savings Accounts (MSA) –

.................- For participants who have self-only coverage in a MSA, the plan ...................must have an annual deductible not less than $2,850 but not more ...................than $4,300.

.................- Self-only coverage maximum out-of-pocket expense amount is ...................$5,700.

.................- For participants with family coverage, the new annual deductible is ...................$5,700 and the deductible cannot be more than $8,550. For the ...................family coverage, the out-of-pocket expense limit is $10,500.

-

Medical and Dental Expenses – The floor for medical and dental expenses is 7.5%. In other words, taxpayers can only deduct expenses which exceed 7.5% of their AGI.

-

Charitable Donations – The limit for charitable cash donations remains at 60% until 2025.

| |

|

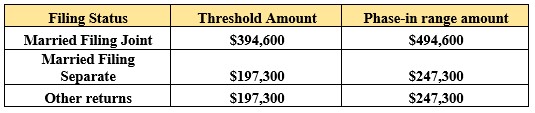

Qualified Business Income Deduction under Section 199 (Pass-through deduction)

Sole-proprietors and owners of pass-through businesses are eligible for a deduction of up to 20% of their qualified business income. Below are the thresholds and phase-in amounts.

| |

|

Federal Estate Tax Unified Credit – Estates of decedents who pass away during 2025 have a basic exclusion of $13,990,000 million, up from $13,610,000 million in 2024.

Limits to Personal Gifts – The 2025 annual exclusion for gifts increases to $19,000, compared to $18,000 in 2024. If gifts are split between spouses, then the total amount that can be gifted is $38,000.

| |

|

Retirement Accounts

401(K), 403(b), 457 Plans – Contribution limits for these popular retirement savings accounts will rise to $23,500 starting in 2025. Likewise, the catch-up contribution limit for individuals aged 50 and over will remain at $7,500. Under a change made in SECURE 2.0, a higher catch-up contribution limit of $11,250 applies for employees aged 60, 61, 62 and 63 who participate in these plans instead of $7,500.

| |

|

SIMPLE Retirement Accounts – The contribution limit for individuals with this type of account has increased to $16,500 (up $500 from 2024). Due to changes made in the SECURE 2.0 Act, individuals can contribute a higher amount to certain applicable SIMPLE retirement accounts. For 2025, this higher amount remains $17,600. The catch-up contribution limit that generally applies for employees aged 50 and over who participate in most SIMPLE plans remains $3,500 for 2025.

Another change in the SECURE 2.0 allows a different catch-up limit that applies for employees aged 50 and over who participate in certain applicable SIMPLE plans. For 2025, this limit remains $3,850. A higher catch-up contribution limit of $5,250 applies for employees aged 60, 61, 62 and 63 who participate in SIMPLE plans in 2025.

Traditional IRA – Contribution limits to an IRA will remain the same at $7,000 with an additional $1,000 catch-up amount allowed for those aged 50 and over.

| |

When a taxpayer meets certain conditions, their contributions to a Traditional IRA are deductible on their tax return. These conditions include filing status, AGI limits, and whether the taxpayer and/or spouse are covered by a workplace retirement plan. For 2025, the phase-out AGI limits were increased as follows: | |

-

Single Taxpayers covered by a workplace retirement plan – phase out range is increased to between $79,000 and $89,000, up $2,000 from last year.

-

Married Filing Jointly

...............- For the spouse making the IRA contribution and is covered by the .................workplace retirement plan, the phase-out ranges are increased to .................between $126,000 and $146,000. (Up $3,000 from 2024)

...............- For the spouse that is married to someone who is covered by a .................workplace retirement plan, the phase-out ranges increase to between .................$236,000 and $246,000. (Up $6,000 from 2024)

-

Married Filing Separately – the phase-out range is not subject to an annual cost of living adjustment and remains between $0 and $10,000.

| |

|

Roth IRA – The income phase-out range for taxpayers making contributions to a Roth IRA have increased as follows:

-

Single and Head of Household – between $150,000 and $165,000

-

Married Filing Jointly - $236,000 and $246,000

-

Married Filing Separately – The phase-out range is not subject to annual cost-of-living adjustments and remains between $0 and $10,000

| |

|

Let us help you prepare for next year!

These adjustments are some of the many tax provisions modified for the 2025 tax year. Please note that various adjustments are subject to change based on the outcomes of the election. Policy shifts or new legislative actions resulting from the election may lead to revised policy changes. Nonetheless, with an ever-changing economy and constant inflation fluctuations, knowing your tax options is highly important. If you would like a more in-depth discussion as to how these or any other tax provisions may affect you, feel free to contact our office. We are always ready to help assist our clients develop a sound tax plan for the future!

| |

GRIFFING & COMPANY, P.C.

One Sugar Creek Center Blvd., Suite 650

Sugar Land, TX 77478

(281) 491-8866 Fax (281) 491-8998

| | | | |