CURRENT MARKET PERSPECTIVE | |

|

INFLATION WORRY RE-IGNITED

YIELDS FOLLOW GOLD, SILVER, OIL AND BITCOIN (MUCH) HIGHER!

Click All Charts to Enlarge

| |

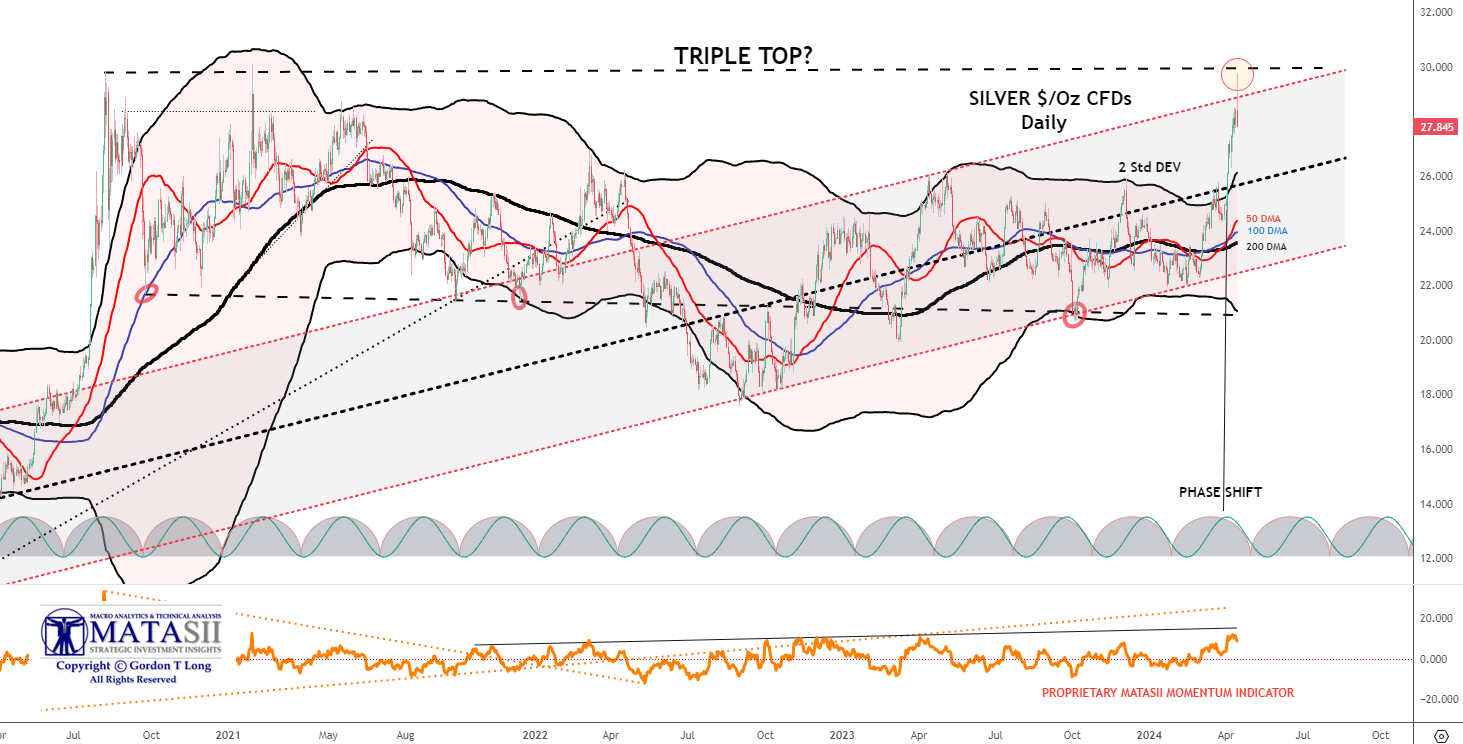

SILVER: Silver following Gold higher (and other Inflation hedges) to new highs! | |

|

1 - SITUATIONAL ANALYSIS

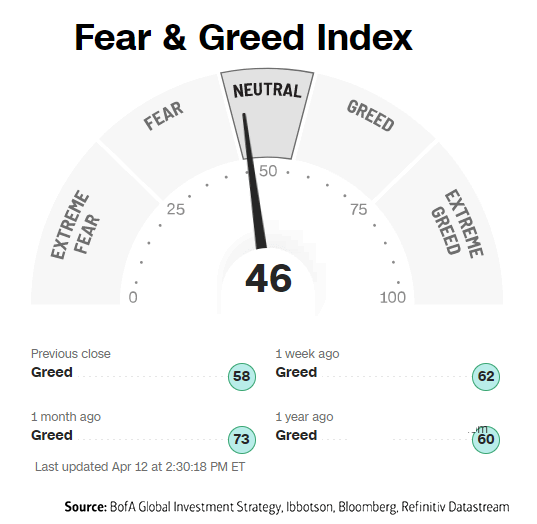

SENTIMENT "ADJUSTING"!

Last week with the Fear & Greed Index down to a reading of 61 we said: "We have seen some degree of market weakness over the last week as the S&P 500 tested the 21 DMA for support. It appears that increasing numbers of investors are nervous about some degree of pullback after a historic run-up without any real corrective consolidation.

The Fear & Greed Index reflects this as it has lowered quite noticeably though registering a Greed reading."

This week we see the Fear & Greed index down to 46, a neutral reading and the S&P 500 lower at its 50 DMA level.

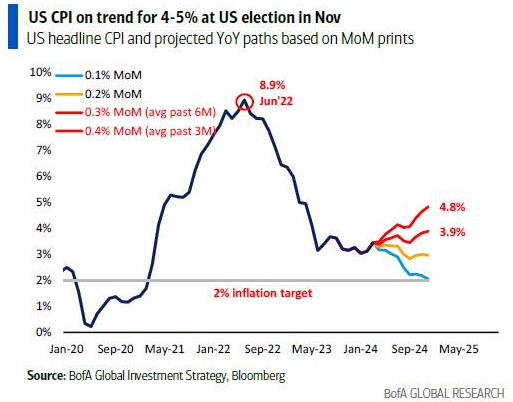

As we pointed out in Wednesday's subscriber's mid-week charts update, the CPI, PPI and Bond Auctions (historic "tails") shock the markets with a reignited worry about Inflation. The long expected June Rate cuts have been abruptly taken off the table and the markets are adjusting to it.

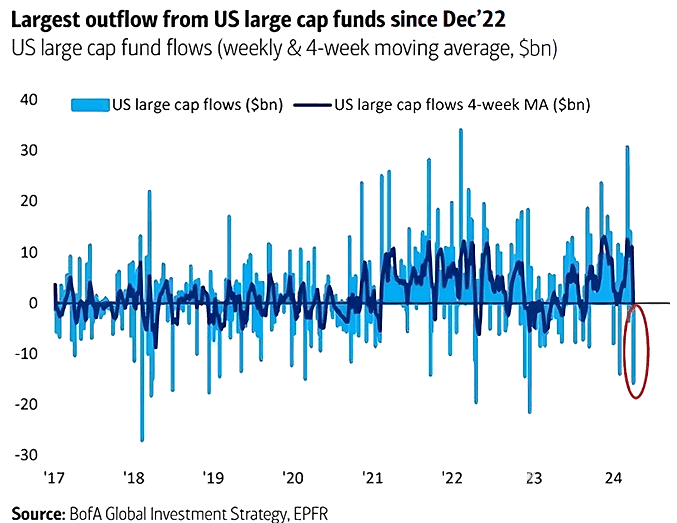

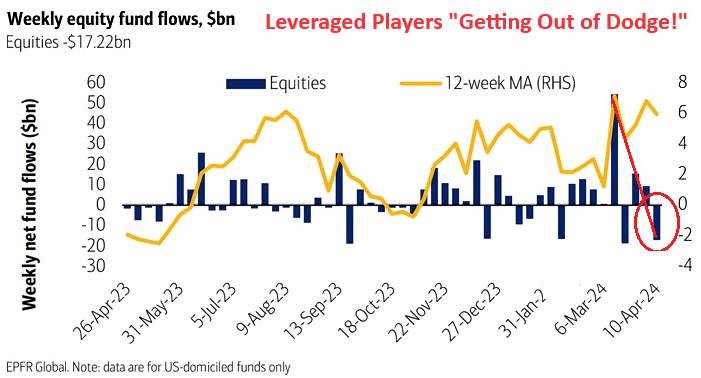

EQUITY FUND OUTFLOWS PICK-UP STEAM

The chart below shows that weekly Equity Funds Flows turned negative following steady weakness over the past couple of weeks. The chart to the right shows that even the US Large Cap funds saw impressive outflows. This is what initially has taken the S&P 500 to the 50 DMA.

|  | |

|

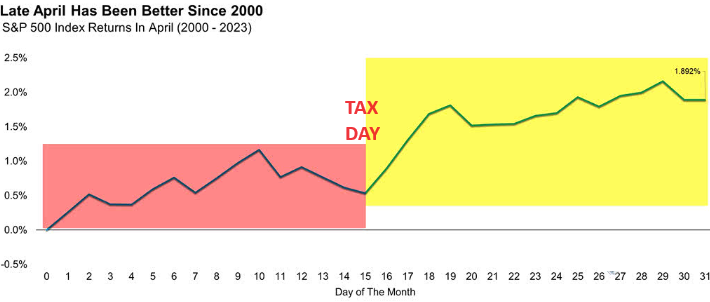

APRIL SEASONALITY (POST TAX DAY) HAS BEEN HISTORICALLY STRONG | |

|

2 - FUNDAMENTAL ANALYSIS

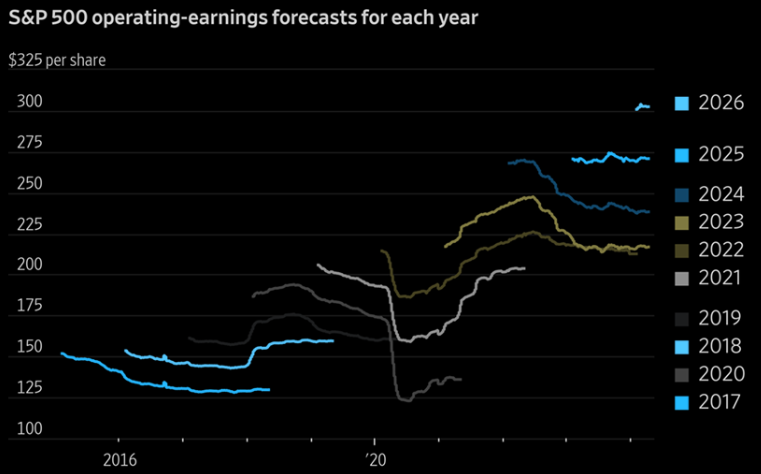

Wall Street expects a lot of profit this year, next year and, in early forecasts, 2026. The future is bright, investors and analysts think, even though it’s extremely rare for reality to come in better than originally hoped! (chart right)

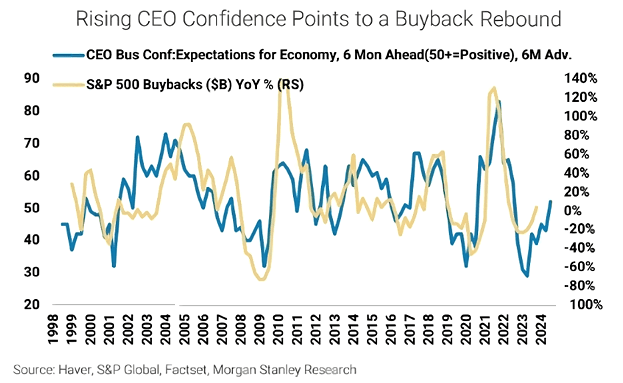

CEO'S INCREASINGLY MORE CONFIDENT!

Any potential corrective / consolidation is to likely be short lived since CEOs are becoming increasingly more confident with earnings outlooks looking strong. Typically this has led to increased buyback levels (see chart below).

NOTE: Corporate Buybacks are in a closed window due to their pending Q1 earnings releases. As they release their earnings it is expected they will again begin their planned buybacks.

| |

|

CREDIT MARKETS

Since Credit always leads markets, we are watching it closely. This includes:

- Inverted yield curves

- Negative swap spreads

- Collateral shortages

- Tightening of credit standards by banks and

- Reduced commercial lending

- The High Yield Corporate "JNK" Market. (BELOW)

CHART RIGHT ABOVE

Goldman Sachs: "We continue to advocate adding hedges to portfolios given rock-bottom levels of implied volatility".

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

3 - TECHNICAL ANALYSIS

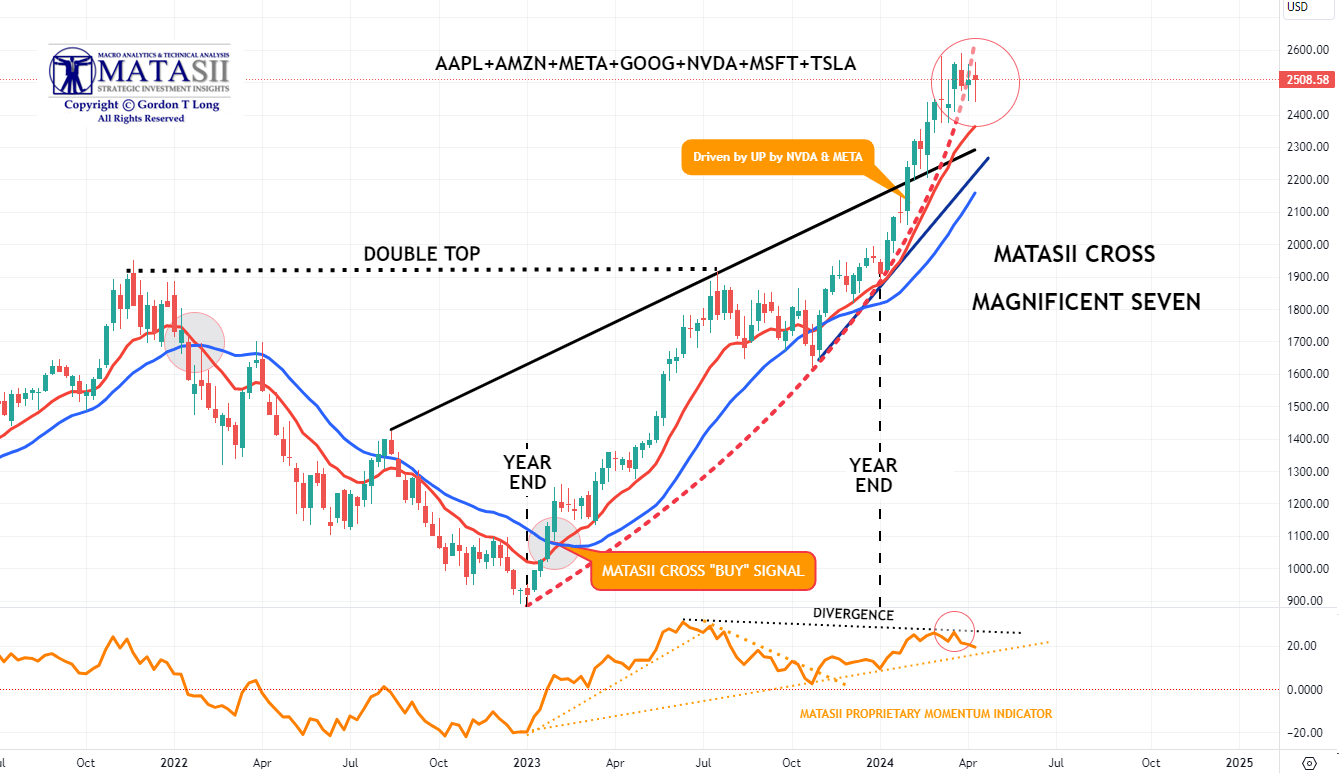

THE HEADLINE MARKET: MAGNIFICENT 7

- We are reaching the vertical lift part of the parabolic (geometric) lift shown by the dashed red line.

- We have intermediate term Divergence with momentum (bottom pane).

- In the short term Momentum appears to be rolling over (bottom pane).

| |

CHART RIGHT ABOVE: The stress in VIX is huge and the gap between SPX and VIX is widening big time. The crowd is ending the week on an extremely nervous note. Chart shows SPX vs VIX inv since Feb.

CHART RIGHT: It appears that the VIX and VVIX are in full panic mode?

MATASII CROSS: WEEKLY - CONTINUES TO SIGNAL A MAG-7 BUY

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

"CURRENCY" MARKET (Currency, Gold, Black Gold (Oil) & Bitcoin)

CONTROL PACKAGE

There are EIGHT charts we have outlined in prior chart packages which we will continue to watch closely as a CURRENT "control set".

-

US DOLLAR -DXY - MONTHLY (CHART LINK)

-

US DOLLAR - DXY - DAILY (CHART LINK)

-

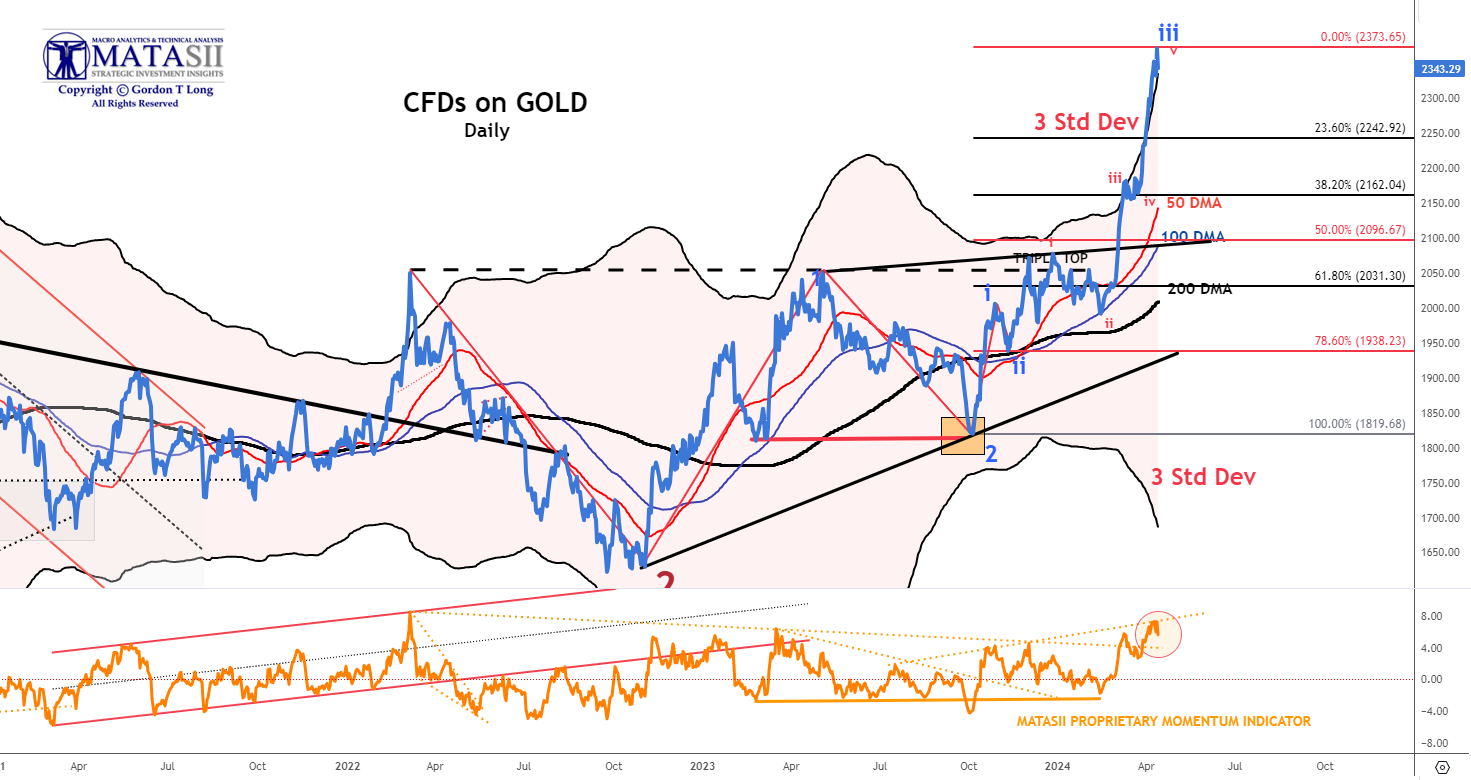

GOLD - DAILY (CHART LINK)

-

GOLD cfd's - DAILY (CHART LINK)

-

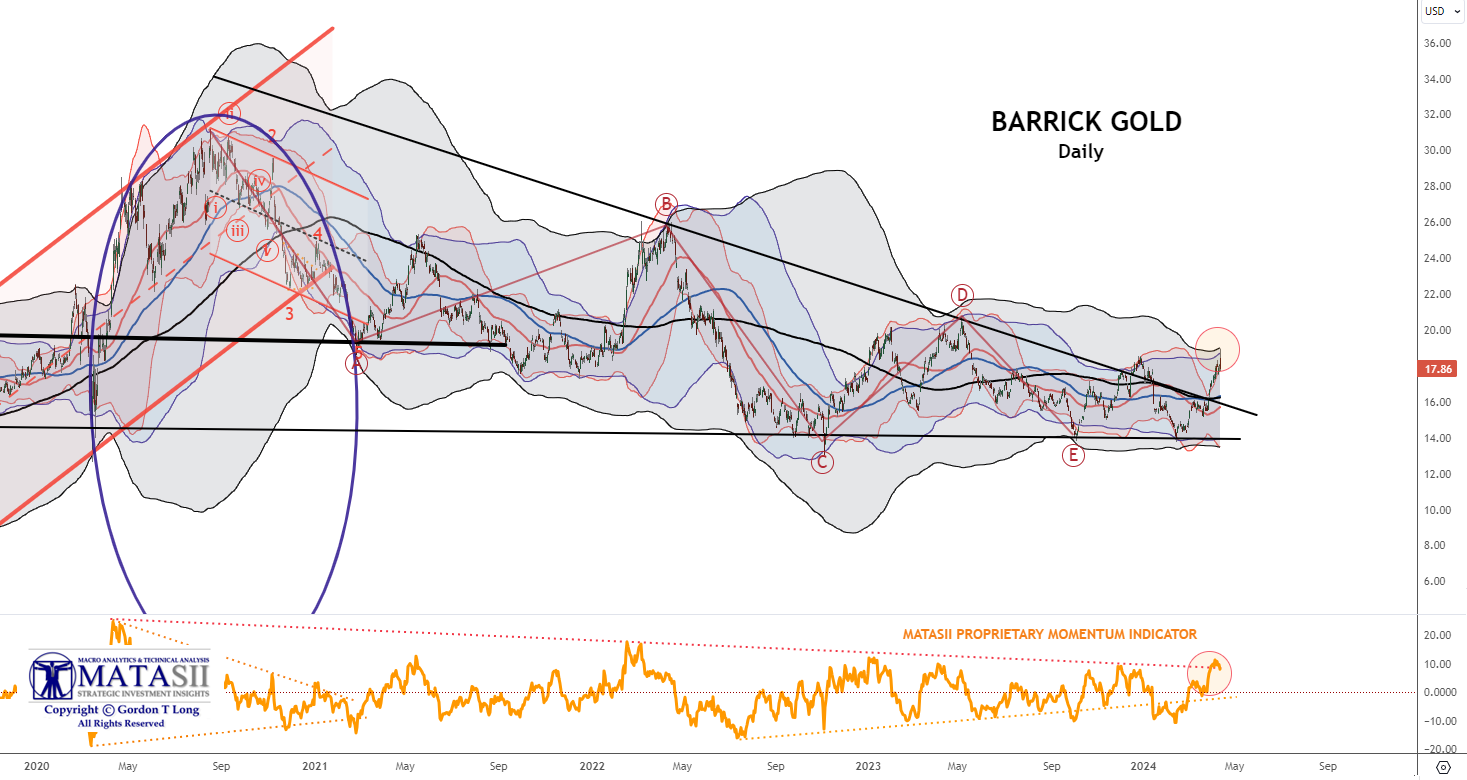

GOLD - Integrated - Barrick Gold (CHART LINK)

-

OIL - XLE - MONTHLY (CHART LINK)

-

OIL - WTIC - MONTHLY - (CHART LINK)

-

BITCOIN - BTCUSD -WEEKLY (CHART LINK)

CHART ABOVE RIGHT

As gold pushes to higher & higher record highs (in USD terms), Real yields refuse to play along?? I side with BoAML's Michael Hartnett and believe that what we are seeing is Gold aggressively discounting a coming collapse in Real Rates.

GOLD cfd's - DAILY

The 3 Std Deviation band for Gold has gone almost vertical with Gold prices tracking it!! Frankly, in over 40 years I don't believe I have seen this technically occur with a 3 Std Dev in Gold? Something is either broken, panic has set in somewhere or there is an "elephant(s)" now playing the market?

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

INTEGRATED GOLD MINERS

We have a close eye on Gold and the INTEGRATED GOLD MINERS as represented by Barrick Gold. Barrick It has broken out of its long term declining overhead resistance trend. It is likely time to be adding to your Gold and Silver positions on any pullback opportunities.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

US EQUITY MARKETS

CONTROL PACKAGE

There have FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set".

-

The S&P 500 (CHART LINK)

-

The DJIA (CHART LINK)

-

The Russell 2000 through the IWM ETF (CHART LINK),

-

The MAGNIFICENT SEVEN (CHART ABOVE WITH MATASII CROSS - LINK)

-

Nvidia (NVDA) (CHART LINK)

| |

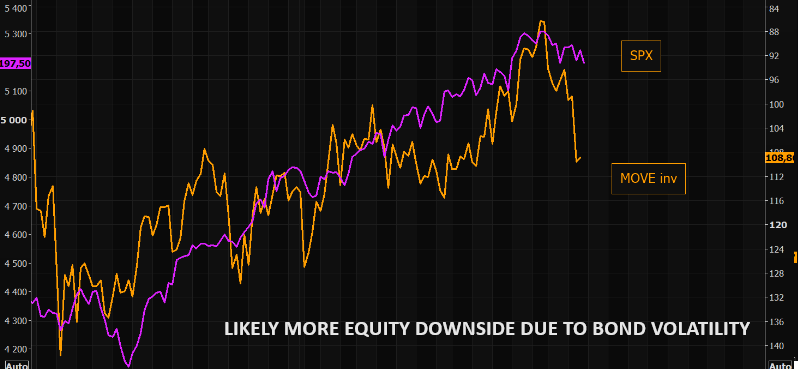

CHART RIGHT: What if SPX starts paying attention to bond volatility again? Chart shows SPX vs MOVE inv.

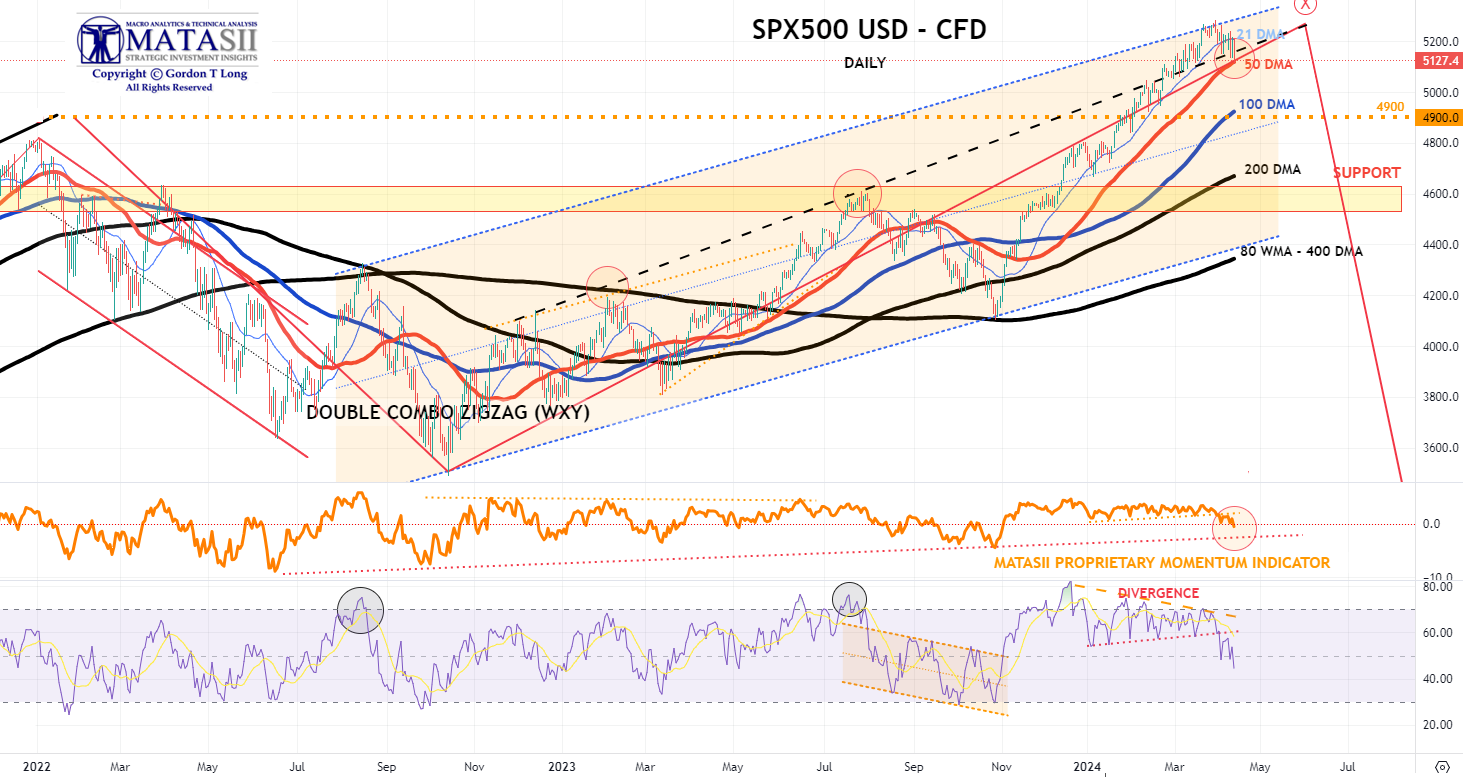

S&P 500 CFD

The S&P 500 cfd has put in a near term high and retraced to very close to the 50 DMA.

It is a testament to the strength of the equity market that with both yields moving so much higher and the dollar surging, that the equity market didn't sell off much further?

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

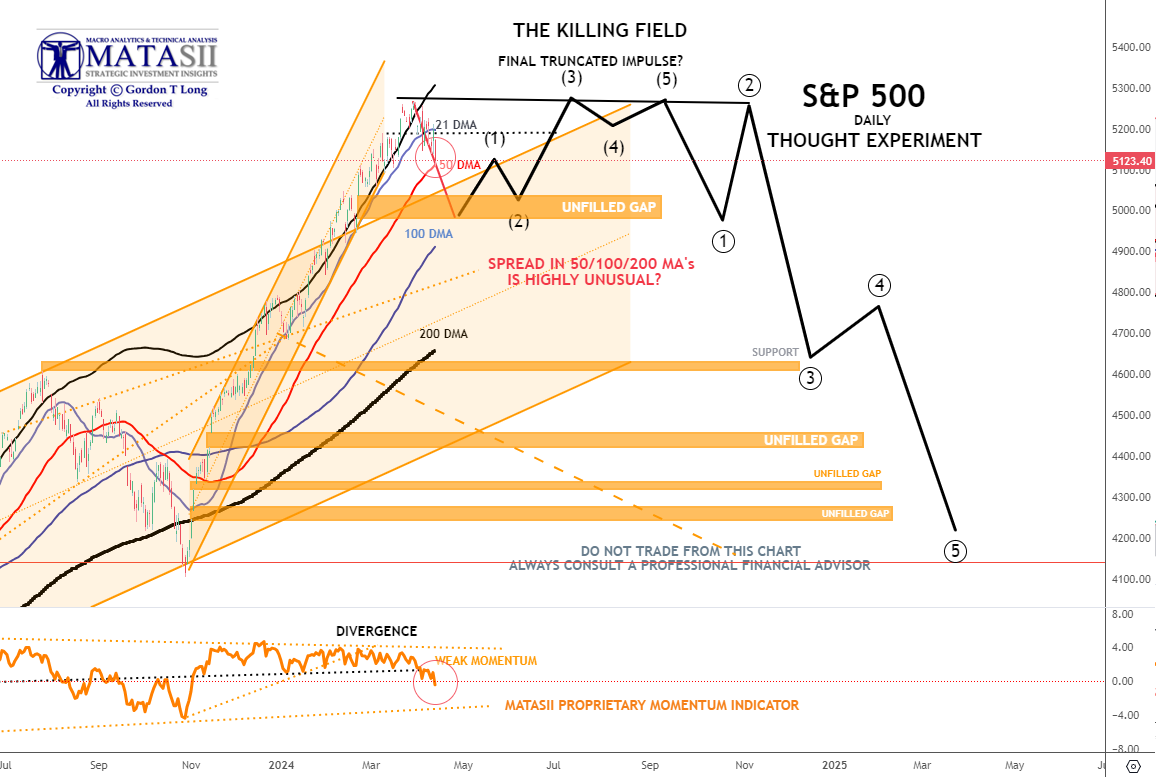

S&P 500 - Daily - Our Though Experiment

Our Though Experiment, which we have discussed previously, suggests we have put in a near term top and will now consolidate before possibly completing one final small impulse higher or put in a 1-2 Wave of a much higher degree.

NOTE: To reiterate what I previously wrote - "the black labeled activity shown below, between now and July, looks like a "Killing Field" where the algos take Day Traders, "Dip Buyers", "Gamma Guys" and FOMO's all out on stretchers!"

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

STOCK MONITOR: What We Spotted

MONDAY

- It was calm before the storm on Monday as participants await key risk events, namely US CPI on Wednesday, but also several Central Bank decisions, including from the ECB, BoC and RBNZ, while the FOMC Minutes will also be released post-CPI.

- Earnings season also starts at the tail end of this week.

- Stocks finished little changed but the Russell 2000 outperformed. In FX, the Dollar was sold and the Euro bid, but Antipodes outperformed and Swissy lagged.

- JPY was ultimately little changed, but it did test 152.00 to the upside with traders cognizant of any intervention on a move above this level, particularly with CPI on Wednesday which could have a large sway in the pair.

- Crude prices saw choppy price action on mixed geopolitics report regarding a ceasefire which was ultimately rejected by Hamas while Iran was punchy on retaliatory language against Israel following the attack on its consulate. It also was pointing responsibility towards the US.

- Elsewhere, modest pressure was seen in oil on the Reuters report that Iraq has completed the first stage of repairing oil export pipeline to Turkey.

- Treasuries were firmer across the curve ahead of supply and the aforementioned risk events.

INFLATION BREAKEVENS: 5yr BEI +1.0bps at 2.442%, 10yr BEI +1.3bps at 2.396%, 30yr BEI +0.9bps at 2.333%

REAL RATES: 10Y -- 2.0139%

STOCK SPECIFIC

- Alibaba (BABA) flat: Alibaba Cloud announces price cuts.

- United Airlines (UAL) +0.5%: Postponed its investor day planned for next month due to a US FAA review following safety incidents.

- Tesla (TSLA) +5%: CEO Musk said the EV-maker would unveil its "Robotaxi" on August 8th.

- TSMC (TSM) +1%: Has agreed to a USD 6.6bln subsidy for TSMC Arizona chip production; and up to USD 5bln in low-cost government loans.

- Perion Network (PERI) -41%: Cuts FY24 revenue and adj. EBITDA outlook citing Microsoft Bing modifications.

- Boeing (BA) -1%: FAA to investigate the loss of engine cover on Southwest Boeing 737-800.

- Apartment Income REIT (AIRC) +22.5%: Agreed to be acquired by Blackstone (BX) for about USD 10bln or USD 39.12/shr. Note, AIRC closed Friday at USD 31.35/shr.

- Model N (MODN) +10%: To be acquired by Vista Equity Partners for USD 1.25bln or USD 30/shr. Note, MODN closed Friday at USD 27.09/shr.

- Micron (MU) -0.5%: Intends to sequentially increase its DRAM module and SSD prices by more than 25% during Q2, according to DigiTimes citing sources.

- Global Foundries (GFS) -0.5%: Downgraded at Cantor amid 2024 fundamentals.

TUESDAY

- Stocks ultimately saw slight gains despite a choppy session.

- Strength in the futures was seen pre-market after reports Google (GOOGL) is expanding its in-house chip efforts and a slew of cloud deals amid the start of the Google Cloud event.

- Nonetheless, a sharp-sell off in Nvidia (NVDA) hit sentiment after the open through to the European close before a late trade reversal in stocks was observed.

- The upside was supported by commentary from Fed's Bostic who suggested it would be good news for the Fed if US CPI is in line with expectations on Wednesday, noting if the disinflation progress continues, the Fed could bring forward rate cuts.

- Elsewhere, Treasuries were bid across the curve in a lack of catalysts ahead of CPI on Wednesday while the weak 3yr auction did little to prevent the upside.

- Crude prices slid on a lack of geopolitical escalation while Israel Defense Minister appeared to contradict PM Netanyahu noting there is still no date for the Rafah operation.

- FX was largely flat ahead of key risk events but the NZD outperformed ahead of the RBNZ rate decision tonight. All eyes on US CPI on Wednesday.

INFLATION BREAKEVENS: 5yr BEI -2.9bps at 2.418%, 10yr BEI -2.0bps at 2.380%, 30yr BEI -1.7bps at 2.320%.

REAL RATES: 10Y -- 2.0006%

STOCK SPECIFIC

- Google (GOOGL) +1%: Expands in-house chip efforts and is to roll out new hardware in costly AI battle. In addition, with Google’s Cloud event over the coming days, there has been a slew of deals announced. One of the highlights, Broadcom (AVGO) is to migrate VMware workloads to Google Cloud.

- NetEase (NTES) +4%: Reportedly to revive partnership with Microsoft’s Blizzard.

- Netflix (NFLX) -1.5%: Initiated a significant restructure in its film department.

- General Motors (GM) +1%: Self-driving car unit, Cruise, plans to resume testing robotaxis.

- Microsoft (MSFT) +0.5%: To reportedly invest USD 2.9bln in Japanese data centers amid AI boom.

- Pfizer (PFE) +0.5%: Abrysvo meets primary Phase 3 endpoint in RSV disease.

- InMode (INMD) -7%: Lowers Q1 and FY24 revenue outlook.

- BP ADR (BP) +1%: Sees higher oil and gas production.

- Freeport-McMoRan (FCX) +2.5%: Upgraded at BofA saying it has “blue chip copper exposure.”

- Nvidia (NVDA) -2%: UBS analyst note was doing the rounds, and it had some cautious comments on Nvidia's (NVDA) October/Q3 report, also saying sentiment on semis is as optimistic as "I can ever remember".

- Intel (INTC) +1%: Reveals details of new AI chip to fight Nvidia (NVDA) dominance.

- Boeing (BA) -2%: FAA investigates claims by Boeing (BA) whistle-blower about flaws in the 787 Dreamliner, according to New York Times.

THURSDAY

- Stocks rallied on Thursday with Big Tech/NDX leading the charge as participants gear up for earnings.

- A dovish ECB, soft PPI, and dismissive Fed Speak (of CPI) saw the front end of the Treasury pare some recent losses, although the back end continued to trade lower, with a lack luster 30yr auction - albeit not as bad as Wednesday's 10yr - keeping duration offered.

- It was noteworthy that stocks accelerated their gains once the auction was in the rearview, in a seeming "relief rally".

- Apple (AAPL) accelerated gains on Bloomberg reports about its new M4 chip products being in the works, while Nvidia (NVDA) also saw massive gains on no fresh catalysts.

- There appears to be an appetite to get long stocks for this earnings seasons, where analysts flag the bar for beats is relatively low.

- Big banks kick things off on Friday.

- In commodities, oil trundled lower, with concerns around an Iran response somewhat softened by reports that any attack would be "controlled and non-escalatory".

- However, that didn't stop Gold, with the yellow metal going on to print new record highs above USD 2,375 at time of writing, perhaps benefitting from the Fed Speak, where Williams, an influential voter, indicated little change in his outlook that cuts will "eventually" be needed despite inflation bumps.

- In FX, the DXY was ultimately flat, with activity currencies outperforming, while the Euro was flat to slightly lower despite Lagarde's mentioning there were some calls for a cut at today's meeting.

INFLATION BREAKEVENS: 5yr BEI -1.6bps at 2.456%, 10yr BEI -0.1bps at 2.414%, 30yr BEI +0.1bps at 2.345%.

REAL RATES: 10Y -- 2.184%

STOCK SPECIFIC

- Apple (AAPL) +4%: Plans to revamp entire Mac line with AI-focused M4 chips, according to Bloomberg; M4 Macs designed to bring AI capabilities and boost memory. First wave of M4 Macs to debut in late 2024, early 2025.Separately, it warned users of a spyware attack.

- Amazon (AMZN) +1.7%: Ordered to pay USD 525mln patent violation fine. Elsewhere, as they look towards 2024 (and beyond), they are not done lowering cost to serve.

- Costco (COST) +1.4%: Boosts quarterly dividend to USD 1.16/shr (prev. 1.02).

- US Steel (X) -0.9%: DoJ is probing Nippon Steel's acquisition of X amid national security concerns.

- CarMax (KMX) -9%: EPS and revenue missed accompanied by downbeat comms.

- Constellation Brands (STZ) +1.2%: Top and bottom line beat, raised quarterly dividend and FY25 EPS outlook surpassed expectations.

- Fastenal (FAST) -6.5%: Earnings disappointed which were affected by adverse weather.

- Alpine Immune Sciences (ALPN) +37%: To be acquired by Vertex (VRTX) for USD 4.9bln in cash or USD 65/shr. ALPN closed Wednesday at 47.04.

- Nike (NKE) +3.4%: Upgraded at BofA with expectations rebased.

- Robinhood (HOOD) +3.6%: Downgraded at Citi.

- Globe Life (GL) -53%: Fuzzy Panda short on the name.

- Ford (F) flat: Cuts prices of electric F-150 pickup by up to USD 5,500 to boost sales.

- Blackbaud (BLKB) +4.2%: Clearlake said to renew pursuit of software firm Blackbaud, according Bloomberg sources.

- Marvell (MRVL) +0.2%: Gave an AI update at its event; Recorded over USD 550mln in AI related revenue in 2023. Looking ahead, sees AI contributing close to 30% of total revenue in 2024 and tripling to over USD 1.5bln, and sees USD 2.5bln for 2025 as a "solid base".

FRIDAY

- Stocks were sold on Friday with Iran fears and poor bank earnings weighing into the weekend, with small caps suffering the most.

- Treasuries saw strong gains, paring some of the week's losses amid the Iran concerns and risk aversion.

- JPM saw heavy selling after investors were let down by the lack of guidance increase to its NII, while WFC and C performed relatively better.

- Chip names saw particular pressure amid WSJ reports China had told telecom carriers to phase out foreign chips.

- Bitcoin and crypto saw heavy losses amid the risk aversion. It was a rollercoaster session for oil and gold, with the pair of them having made fresh peaks on a slew of reporting in the NY morning of an imminent Iran response (which we still await), only to reverse lower into the close with many traders expecting a response that does not threat an escalation.

- The Dollar saw strong gains with the Iran fears underscoring the policy divergence of the Fed vs other central banks, particularly in Europe, who are seemingly much closer to beginning rate cuts.

- In data, the highlight was the University of Michigan survey's consumer inflation expectations, which both saw an unwelcome rise, albeit to levels that are consistent with post-COVID ranges, but that saw little price reaction.

- We also had a slew of Fed Speak from Collins, Schmid, Daly, and Bostic, who are all expressing caution in rushing into rate cuts, something which money markets have already adjusted to.

INFLATION BREAKEVENS: 5yr BEI -0.4bps at 2.454%, 10yr BEI -0.9bps at 2.402%, 30yr BEI -0.7bps at 2.337%.

REAL RATES: 10Y -- 2.122%

STOCK SPECIFIC

- Globe Life (GL) +20%: After declining 53% yesterday on a Fuzzy Panda short report, it issued a statement where it refuted the allegations.

- Intel (INTC) -5%, AMD (AMD) -4%: China has reportedly told telecom carriers to phase out foreign chips.

- Morgan Stanley (MS) -1%: Following a 5% decline on Thursday, after news its wealth management unit probed ahead of its earnings next week.

- Arista Networks (ANET) -8.5%: Double downgraded at Rosenblatt on AI boost skepticism.

- Southwest Airlines (LUV) -3.5%: Anticipates receiving only about half of the expected Boeing jet deliveries for 2024, significantly impacting its growth plans.

- Coupang (CPNG) +11.5%: Raising 'Wow' membership fee by 58%.

- Paramount (PARA) -3%: Asked by Barington Capital to engage Apollo (APO) on offer, according to Bloomberg.

EARNINGS:

- JPMorgan Chase & Co (JPM) -6.5%: NII was light and CEO Dimon said it fell on deposit margin compression and lower deposit balances. Looking ahead, GS remain alert to a number of significant uncertain forces. Reaffirmed FY NII view but was short of expectations for a raise.

- Wells Fargo & Co (WFC) -0.5%: Have been very choppy post-earnings: Top and bottom line beat, but net interest income and net interest margin missed. Looking ahead, affirmed it sees FY24 net interest income down between 7% and 9%.

- Citigroup (C) -1.5%: EPS and revenue beat, with the breakdown also strong, although net interest income did miss.

- Progressive (PGR) +1%: Profit, net premiums earned and written topped.

- BlackRock (BLK) -3%: EPS and revenue beat alongside AUM hitting a record USD 10.5tln.

- State Steet (STT) +2.5%: Revenue, EPS, NII, and AUM all topped street expectations.

| |

BOND MARKET

CONTROL PACKAGE

There have FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set".

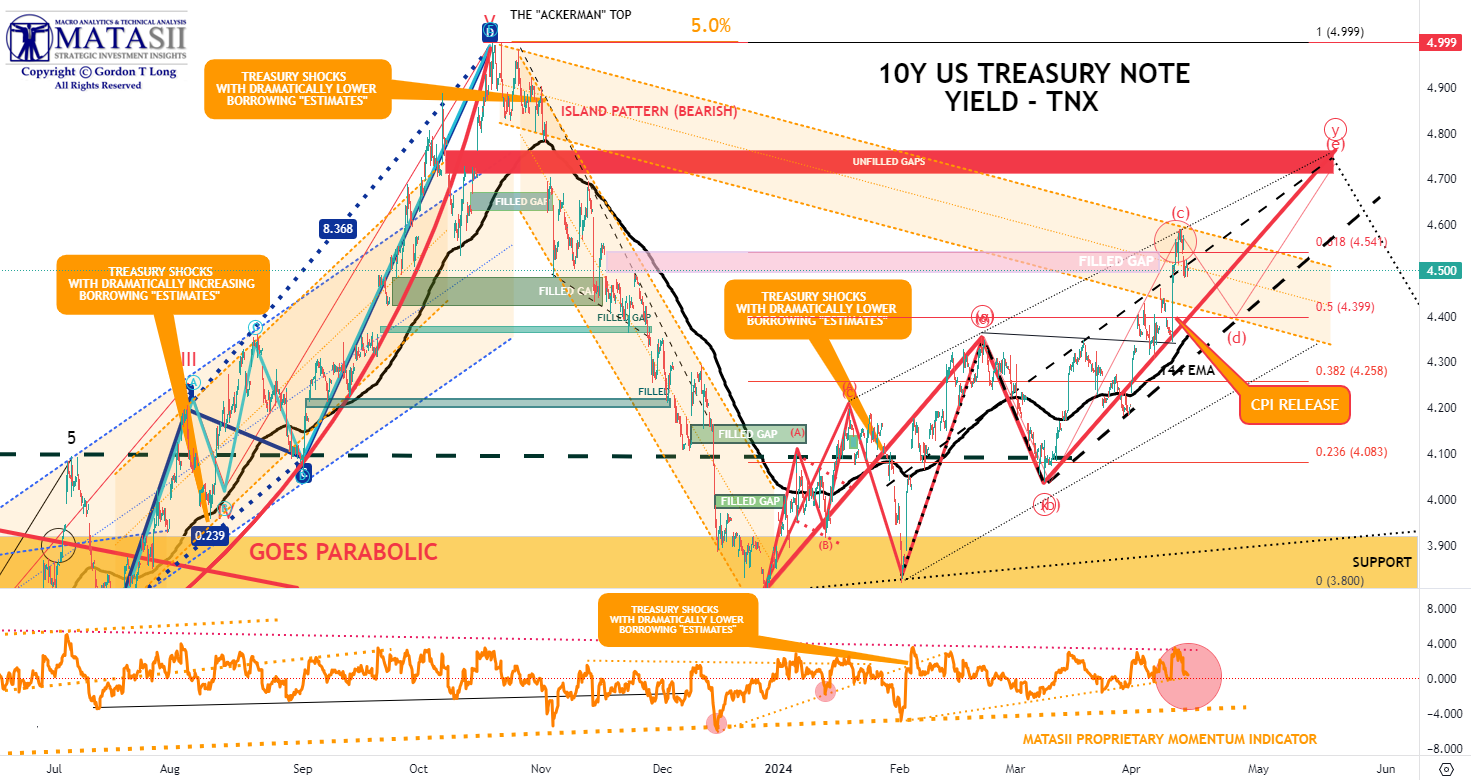

- The 10Y TREASURY NOTE YIELD - TNX - HOURLY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - DAILY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - WEEKLY (CHART LINK)

- The 30Y TREASURY BOND YIELD - TNX - WEEKLY (CHART LINK)

- REAL RATES (CHART LINK)

- FISHER'S EQUATION = 10Y Yield = 10Y INFLATION BE% +REAL % = 2.402% + 2.122% = 4.524%

| |

As rate-cut expectations fell from 6 this year to 3, Treasury yields rose... non-stop... all week with the belly of the curve underperforming (5Y yields up 28bps on the week). Yields all ended back up near their year-to-date highs.

Expectations changed over the week regarding the inflation outlook moving higher, which is reflected to the right.

As the chart below of the 10T Treasury Yield reflects, with the release of the CPI (orange text bubble) it was a straight lift of 25 bps to 4.6%, before retreating slightly.

The narrative has shifted to the 10Y Treasury Yield now trading to 5.0%. We currently see 4.8% with real yield of 2.5% being the upper limit before the equity markets crack from rates and the Fed is forced to react because of the political pressure of an election year.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond ‘fair use’, you must obtain permission from the copyright owner.

========

| |

IDENTIFICATION OF HIGH PROBABILITY TARGET ZONES | |

Learn the HPTZ Methodology!

Identify areas of High Probability for market movements

Set up your charts with accurate Market Road Maps

Available at Amazon.com

| |

The Most Insightful Macro Analytics On The Web | | | | |