ISSUE 135, October 31, 2024 | |

| |

|

Ryan Statz, Merchant

BARLEY

| |

|

- With supply defined and quality assessments nearly complete, demand is starting to show up in spotty fashion in terms of qualities, timings, and quantities.

- Timing will likely start slow as feelers are put out in a non-knee jerk reaction type environment.

- Keep in mind, maltsters have trended very slow/discretely the last 6 months. They will tread lightly as they enter back into buying mode.

- Nonetheless, it will provide the market price definition. A welcomed change from the previous 4-6 months where many players were timid to taking on any chances.

- Yes, with the quality downticks, bullish waves are still floating in the market.

- However, ‘malt’ demand continues to retreat.

- Will the malt demand cuts outweigh the ‘malting barley’ quantity cuts?

- Feed Barley was hot and heavy in August/Sept as corn and other feed products became limited/tighter as they wait for corn new crop campaigns to start (Nov/Dec) as well as additional ‘malting barley’ rejection issues that pushed much of the original ‘malt’ product into the feed side.

- Also note the strengthening USD vs CAD. The US election results will continue to move the USD.

- Note, when the USD firms against the CAD…Canadian buyers are losing import buying power.

| |

- Durum action has been on the demand side of late. Not necessarily firm business, but enough tire kicking from multiple international buyers that is bringing some excitement to all players on both sides. This is a welcomed change from September and early October.

- Market definition should ensue to help narrow up the bid / offer blackhole the market has been trading into.

- Farmer selling remains extremely subdued in Montana.

- Other production areas HAVE bought a decent chunk on grower bid rallies in Canada on the heels of this expected international business.

- A big wave of this demand is needed for North America if we want to spark this market at all…. otherwise, price will grind lower. Simply put, without the business, interior bushels will be carried forward into the new year.

- Keep in mind the overall crop size of ~8.0 MMT in US/Canada this year versus 5.6 MMT last year.

- With ho-hum exports Aug-Oct thus far, much of this volume will be looked at to move in a 6–8-month window. If markets are priced out of international business…carry-outs have the potential to be huge. Look out below if this is the case.

|

| |

|

WHITE WHEAT

Steve Yorke, Merchant

| |

|

As we move into late fall markets continue to chop around the $6.00 level mainly on steady white wheat demand from routine buyers and slow grower selling. If we continue to see steady demand and the grower stays on the sidelines, we have a good chance of staying above this mark and maybe even a touch higher but if either situation changes, we will drift lower once again. As mentioned, many times before Australia will be harvesting soon and their crop is still looking to be very big (30MMT). This will compete directly with our white wheat so prices will be pressured going forward. This week’s exports sales for white wheat were good once again and included one cargo to Indonesia which was a welcomed surprise for this time of year. As always, we have plenty weather and war related issues to play out in the months ahead so have your orders in with our buyers to insure you capture rallies. Grower meetings have been set for the first week of December. Locations and times will be available soon. |

| |

|

Joe Foley, Merchant

SOYBEANS

| |

|

|

Choppy markets have been the feature for prices since our last update, with futures 10-15cnts lower overall. Harvest in the U.S. is now more than 90pct complete, and in ND we’re well wrapped up. ND yields have been largely better. than expected, especially so for corn, and the PNW export market is in full throttle mode with nearly 1mmt exported each of the previous two weeks. That’s the equivalent of 166 soybean shuttles! Harvest in ND came and went fast as the weather has been extremely and atypically suitable. This has been good for those seasonally concerned about adverse weather delaying the cutting of their row crops, but on the flipside, it has made for quite challenging logistics as there simply isn’t adequate space to handle both crops without a pause. Hats off to our guys in the interior, looking for every nook and cranny to carry our producers’ bushels until conveyance arrives.

Export sales overall have been good, exceeding last year at this time by 3.1mmt basis. today’s export sales report. In S. America, Brazil and Argentina have been getting them needed rains for planting next year’s crops. This latter point has been a negative input. for prices, but certainly the weather down there needs to be monitored going forward.

| |

|

Values are about unchanged over the last couple weeks with corn harvest well ahead of schedule, some 81pct completed nationally. Yields have been generally good, and hedge pressure, along with better rains in S. America, have been offsetting the positive effects of a very strong start to U.S. exports. On this latter point, nationally we have 25.8mmt of export commitments (shipped + unshipped sales) on the books since 9/1/2024, some 41pct higher than last year’s 18.3mmt at this juncture. The PNW is competitive, and we accordingly expect a robust export program starting in late.

November, through at least April/May; that’s good news for our producers in ND as their yields are providing ample stem for the PNW exporter. Look for S. America weather to gain more and more attention as their planting pace and early crop conditions take center stage.

|

| |

|

PULSES

Matt Searcy, Merchant

| |

| |

|

LENTILS

Fireworks continue in recent thanks to USDA government tender for 7,200 MT. Discussion surrounding green lentils at the SIAL food show in Paris with global traders consisted around the continued strength in demand globally. Early in the crop cycle it would appear despite the large increase in acres that due to yields, supply was not heavy enough to maintain lower prices. USA exports for August and September are set to be near record pace, giving strong efforts to clear the stocks.

CHICKPEAS

Argentina new crop set to harvest in coming weeks and putting downward pressure on to market. Algeria tendered last week with the option for many origins. They bought only Mexican origin, finding it the best value for the size. A continued rise in ocean freight is challenging heavy chickpea exports as rates and container availability are causing disruptions. European markets continue to demand large caliber, high quality beans but volumes struggle to push prices higher.

PEAS

The spread between green and yellow peas continue to widen. Yellow pea market in India continues to fall from heavy stocks and continued imports from both Canadian and Russian new crop. Strong Montana and North Dakota yields have seen yellow peas availability not to be of concern at this point in the year with current demand. Green peas have shown strong demand, mainly contributed to a consistent reduction in acres. Would recommend looking into new crop 2025 green peas with consistent premiums being offered to yellow peas over last 2 years.

DRY BEANS

Markets have been active the past several weeks with Mexico importers ‘digesting’ the size of the Mexico Dry Bean crop. Reports are stating yields are most disappointing in Chihuahua and Northern Durango with Southern Durango, Zacatecas, and San Luis Potosi being slightly better. Overall, total Mexico Dry Bean production is estimated to increase 20% above last year’s disaster-drought but well below the 5-year average production. Given the increased production in the US, it’s unclear today how much supply Mexico will need from the US.

|

| |

|

HARD RED

WINTER & SPRING WHEAT

Justin Beach, Merchant

| |

|

The spring wheat market has been continued to see exports outpace USDA projections, but we are currently losing PNW demand to Canadian wheat. They have been 70-80c cheaper as of late for Jan forward business. Houston has seen strong demand and Mexico has been a big buyer as of late. Domestic mills remain coy but have a large amount of buying to do January forward with holes to fill in November and December. This all seems to be better news for the ND farmer than the MT farmer as domestic and eastern gateway needs continue to outpace PNW on a relative basis. The PNW market will continue to be extremely dependent on Montana movement to generate the DHV needed to get vessels loaded to proper specifications. The HRW market is seeing increased strength domestically and in the Gulf with buyers coming to market. The PNW remains quiet after a large flush of business late July through September. The market is digesting increased Northern Tier HRW acreage, dry conditions domestically and forecasted rains now in conjunction with Black Sea production prospects. Recently Russia increased their export tariff, and values continue to ebb-and-flow domestically. HRW will get tighter in the north, but the market has needed to work through heavy front-end movement. We will continue to watch global crop conditions and the USD closely for price direction. Overall, Red Wheat has seen decreased demand but still considerably better than the last 2 crop years with lower prices. |

|

|

| |

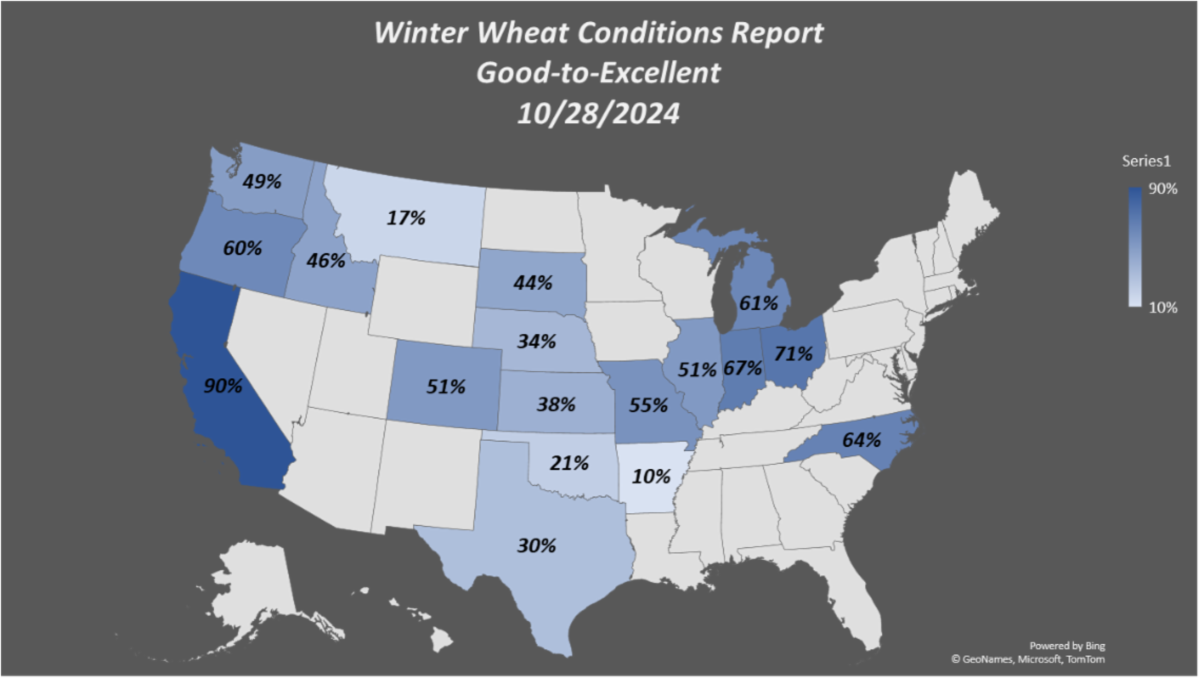

Uncertainty plays a huge role in farming influencing the price direction the markets follow. We have some uncertainty from a political standpoint just around the corner with the Election next week and will more than likely have some implications on price direction as a result. One aspect that did take some of the trade by surprise this week was the crop progress report and the Winter Wheat conditions report. This specific report rates the potential for the wheat crop and rates the crop in 5 separate stages: Excellent, Good, Fair, Poor and Very Poor. The trade tends to view the ‘G/E’ ratings (good to excellent rantings) the Chart below looks at the winter wheat states in the US and the numbers that were released earlier this week. The state average for G/E ratings on winter wheat were released at 38% Which is 9% below last year at this time. So, this number did take the trade by surprise to a certain degree, as a result the market did rally higher the following day. But since then, cooler heads have prevailed and remembered that there is a lot of time and weather to still play into the winter wheat crop and much, much too soon to think the crop is doomed to fail. As a result, the Wheat futures markets rallied 15 cents from the surprise – but as of this writing all that gain has been taken back.

But with this we need to be ready for these knee jerk reactions and take advantage of these opportunities when they become available. Utilizing the tools we have available in Columbia Producer Solutions helps to alleviate some of the analysis paralysis that may develop when you are trying to build out your marketing plan. Diversify the marketing tools that you use to help enhance and cultivate the return that you can extract from the market using a host of Accumulator contracts and look at our “Ca$h +” Cash Plus contracts as well. This tool is a great way to add a premium to your ‘old crop’ grain sales.

Be sure to reach out to your local manager and buyers to get your orders working, remember we can work order for just about all the marketing alternative we have in our Columbia Producer Solutions platform.

| | |

|

Sean Ferguson, Merchant

CANOLA

| |

|

|

ICE Canola futures hang in the balance of bullish global vegetable oil markets and uncertainty of future legislation of biofuel blending mandates in the US. Palm oil has been the leader of upward price movement for vegetable oils as production has fallen off sharply and biofuel consumption mandates have been put forth in Indonesia. US domestic oil values have increased with the support of palm oil as well as speculation on the 45Z tax credit for biofuel production/blending. Many crushers are waiting on the sidelines to see what unfolds in the current election and subsequent biofuel mandates. In any case, ample nearby supply mixed with support in oil markets has meant firmer domestic crush margin in the nearby.

The CAD/USD has broken through the psychological support level of .72 in the December contract. The USD has been supported on increased bets of another Donald Trump presidency. Trump’s stance on tax and immigration can be seen as inflationary, which explains the nearby support for the USD.

| |

The flax market has remained steady to slightly weaker with little demand in the nearby. Stocks remain prominent on the farm in lower SK/ND, which could further suppress the market, unless the export market gains serious steam. Currently, Russia remains the prominent supplier to China for flax. As long as supplies in the Black Sea remain ample and market ready, Canadian flax will have to ration price to work its way into viable export channels. |

| |

|

INTERNATIONAL

Tomo Watanabe, Merchant

| |

|

|

Wheat market continues to seek cheaper alternatives, so we continue to see some of the traditional demand switch to Canadian wheats. With Canadian dollar trades at the lowest level in a year, it provides additional support to their export pipeline margins. Our exporting facilities are pumping out soybean and corn boats day after day so it is harder to squeeze in much more wheat shipments if they cut into the overall efficiency.

Last week, Japanese buyers made numerous purchases for Jan/Feb/Mar shipments of corn. This week, four contracts for Jan shipments were signed for Korea, maintaining PNW’s competitiveness. Due to the declining water levels in the Mississippi River, USG has lost competitiveness, and Brazilian supplies remain scarce.

With the U.S. presidential election approaching next week, Chinese soybean purchases have slowed. Regardless of whether the Republican or Democratic candidate wins, a tough stance toward China is expected, making it difficult to recommend purchases due to execution risks. Currently, PNW has a price advantage, but Brazil’s previously delayed planting is catching up, and optimism around new crop production is increasing, so it’s important to keep a close watch on this going forward.

|

| | | |