- New Normal Rates: The new macro and what this means.

The US economy continues to roll along. December’s labor report showed 261,000 new jobs, a vigorous uptick from the 173,000 number in November. Market observers took this as a sign that the Fed’s projected three rate cuts for 2024 may be more back-ended. The current QT policy, draining liquidity from the financial system and bank reserves, may also be under review. Even slowing that tightening would improve market volatility and lower Treasury yields.

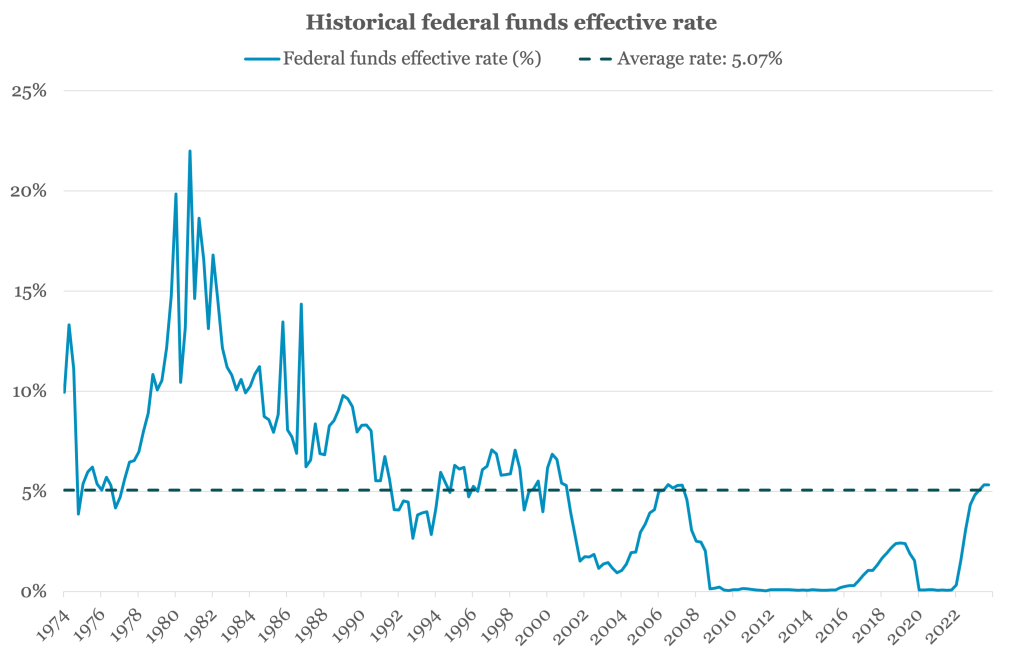

In June 2006 the Federal funds rate rose to 5.25%, the highest level for the benchmark since early 2001 before the dot.com bubble burst. That ushered in over a decade of generations-low rates, a period that finally ended in March 2022. Because many younger financial professionals began their careers during or after the 2008 downturn, their experience has been limited to near-zero interest rates. That leads to a false sense of confidence in the ability of more leveraged borrowers to withstand significantly higher rates and a potential recession...

|