|

Nine Week Streak

The major U.S. stock indexes eked out their ninth positive week in a row as 2023 wrapped up, leaving the S&P 500 just 0.6% shy of its record closing high of January 3, 2022. For the week, the Dow rose 0.8%, the S&P 500 added 0.3%, and the NASDAQ edged upward 0.1%.

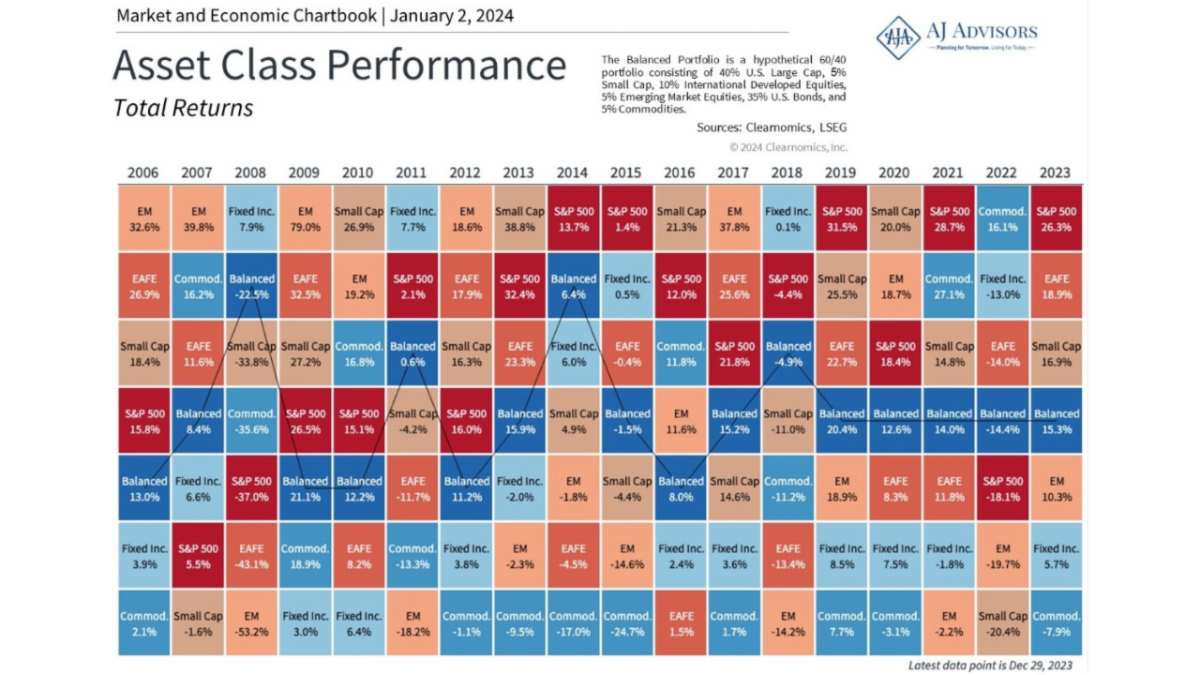

The S&P 500’s overall gain in 2023 marked the fourth positive year out of the past five—and a sharp turnaround from 2022’s negative result. The index generated a 26.3% total return, offsetting the prior year’s 18.1% decline. As for other indexes, the NASDAQ added 44.6% in 2023 and the Dow gained 16.2%.

A year-end 2023 shift in the interest-rate outlook sparked a turnaround in the government bond market, which saw big price declines and spiking yields in 2021 and 2022 amid rising inflation. In 2023, the yield of the 10-year U.S. Treasury peaked in mid-October near 5.00%—the highest since 2007—but then fell sharply and ended 2023 at 3.88%—the same as 2022’s year-end yield.

The past year produced a sharp equity-style performance rotation. A relatively small group of mega-cap growth stocks surged in 2023, lifting a U.S. large-cap growth index to a total return of 42.7%, compared with an 11.5% result for its large-cap value counterpart. In 2022, leadership had been flipped, with value trouncing the growth style.

The past year was notable for the concentrated nature of the U.S. stock market’s overall gains, as just seven mega-cap companies in the information technology, communication services, and consumer discretionary sectors did most of the heavy lifting. In 2023, those seven stocks collectively accounted for 62.2% of the total return of the entire S&P 500, according to S&P Dow Jones Indices.

Although they made up plenty of ground in the last two months of the year, U.S. small-cap stocks trailed large caps by a wide margin in 2023. A small-cap benchmark, the Russell 2000 Index, generated a 16.9% total return compared with 26.5% for a large-cap counterpart. The small-cap index surged 22% in the final two months of 2023.

The year saw wide disparities in U.S. equity performance at the sector level. Information technology and communication services were far and away the top-performing sectors, generating total returns of 57.8% and 55.8%, respectively. In contrast, two sectors generated negative results, with utilities at –7.1% and energy at –1.3%.

A labor market update due out on Friday is likely to be the most closely watched economic report in 2024’s opening week. The release covering December follows a better-than-expected November report that showed the economy generated 199,000 new jobs—above October’s jobs growth of 150,000 but below the 12-month average of 240,000.

Source: John Hancock Investment Management

|