|

Our last Market Now series came in March 2022 [link] after Covid had peaked and begun to fade, when Russia invaded Ukraine. This week we think another pause to review conditions is appropriate given a number of dynamics at play.

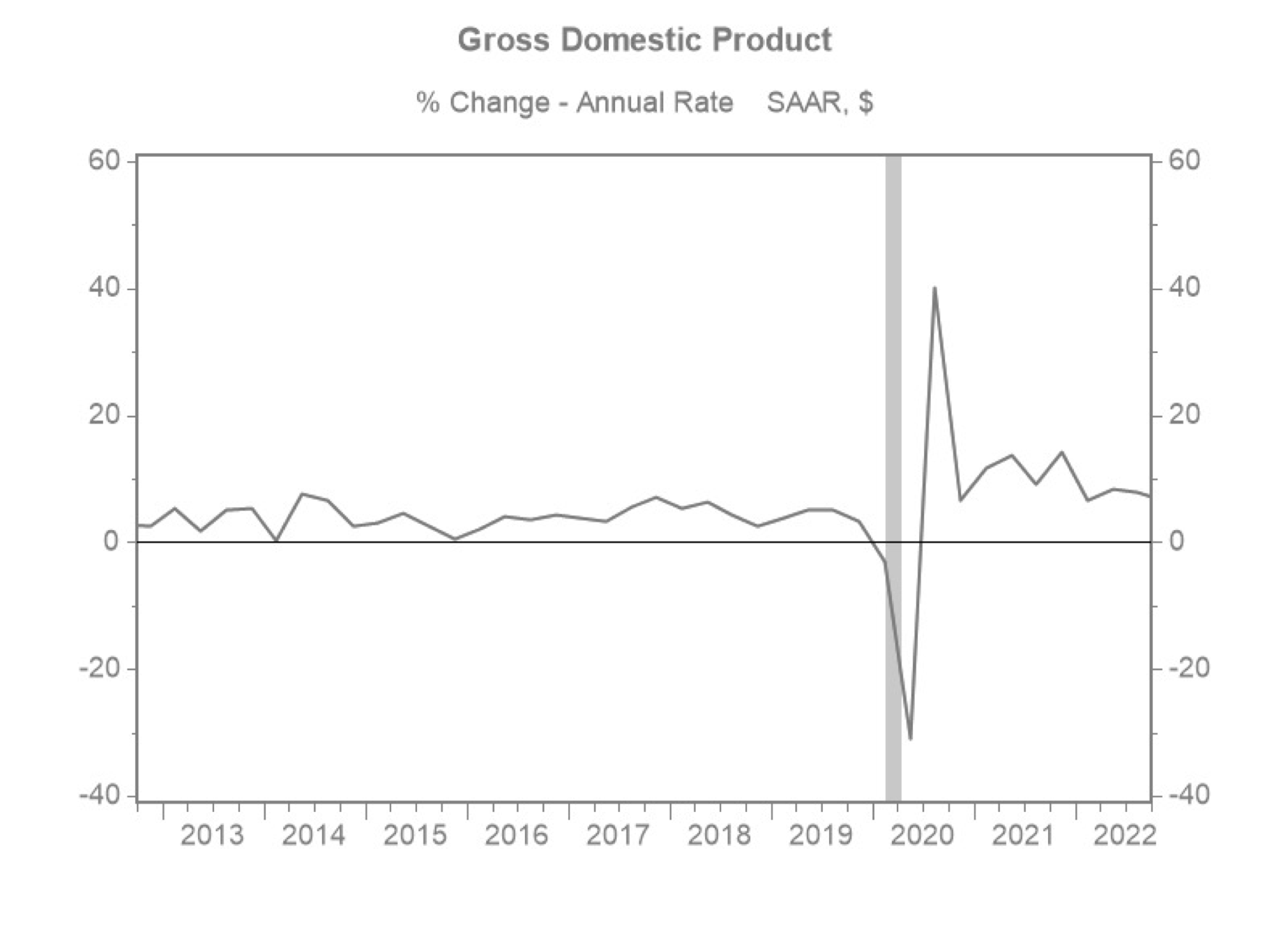

First, the Fed has paused in its rate hikes as their gravity seems to have pulled many inflation indicators down. Employment remains tight, but shows signs of loosening. Real GDP rose at a healthy 2.4% pace for 2Q, yet real personal consumption decreased from 4.2% in the first quarter to 1.6% (see our Chart of the Week).

Public equity markets have responded in a buoyant fashion with the S&P 500 and DJIA up 18% and 7% for the year, respectively...

|