CURRENT MARKET PERSPECTIVE | |

|

EYES ON THE US TREASURY REFUNDING THIS COMING WEEK

EQUITIES TO TRADE ON YIELDS, EARNINGS & TREASURY SIGNALS

Click All Charts to Enlarge

| |

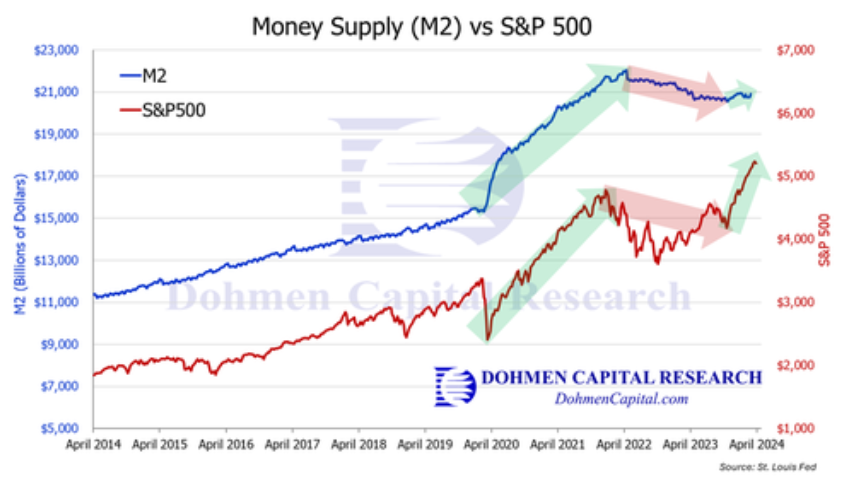

M2 MONEY SUPPLY TURNS: Late last year the Fed started stimulating again, contrary to what Fed officials said publicly. The chart of M2 vs the S&P 500 above confirms that money supply is growing again. The rate of change turned nicely positive. That is the green light for reflating markets….and inflation!! | |

|

1 - SITUATIONAL ANALYSIS

Stock Market remains in fear for the 8th consecutive trading day. The Fear Index has been gradually lessening. It was 31 last week and now registers 42. (chart right)

In terms of market volatility the VVIX has collapsed and is trading at lower levels than prior to this latest mini panic move. The VIX is also significantly down. Both indicating that worry is subsiding though intra day volatility is causing a lot of trading frustration.

So far this is just a "normal" bounce post the sell off. 5150 appears to be the key in SPX to the upside. The short term negative trend line comes in there, as well as the 21 day moving average, sloping negatively.

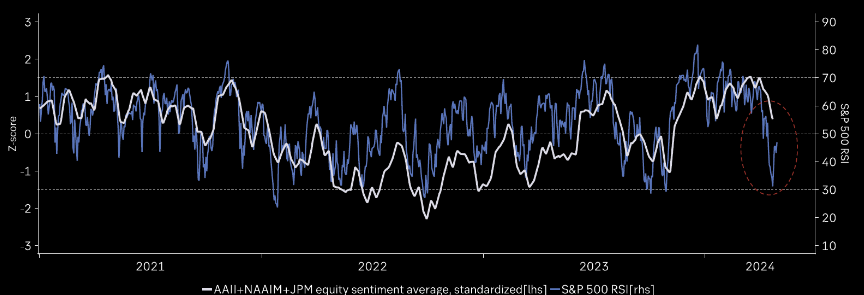

CHART BELOW: Retail Investors are now the most pessimistic / least optimistic about stocks since November

|  | |

Your copy should address 3 key questions: Who am I writing for (audience)? Why should they care (benefit)? What do I want them to do (call-to-action)?

Create a great offer by adding words like "free," "personalized," "complimentary," or "customized." A sense of urgency often helps readers take action, so consider inserting phrases like "for a limited time only" or "only 7 remaining!"

| |

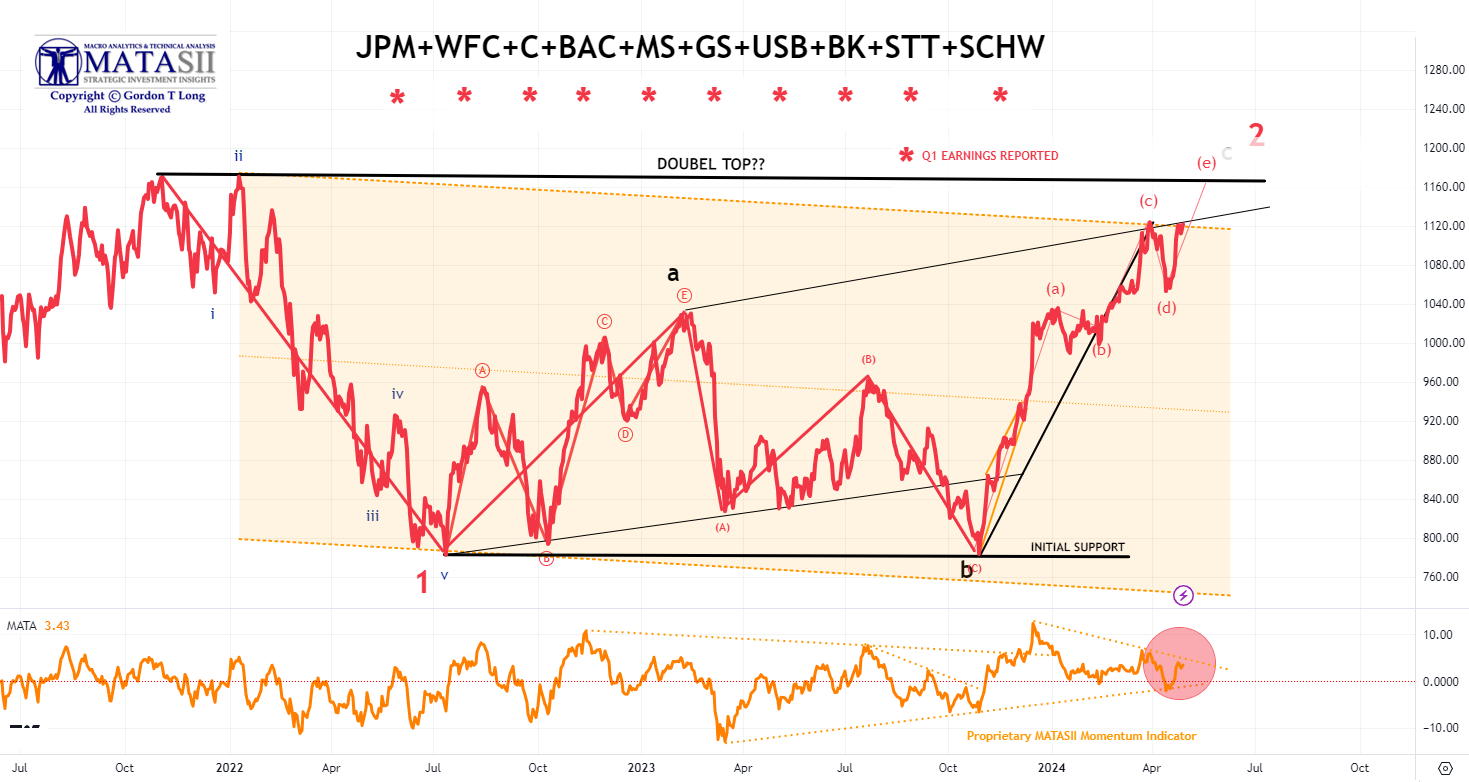

AS GO THE BANKS, SO GO THE MARKETS - AS GO THE FINANCIALS, SO GO THE BANKS! | |

|

1- BANKING STOCKS

Bank stocks though initially weak on earnings release have been trending up ever since, while the overall market weakened until recently rising along with Bank stocks.

| |

|

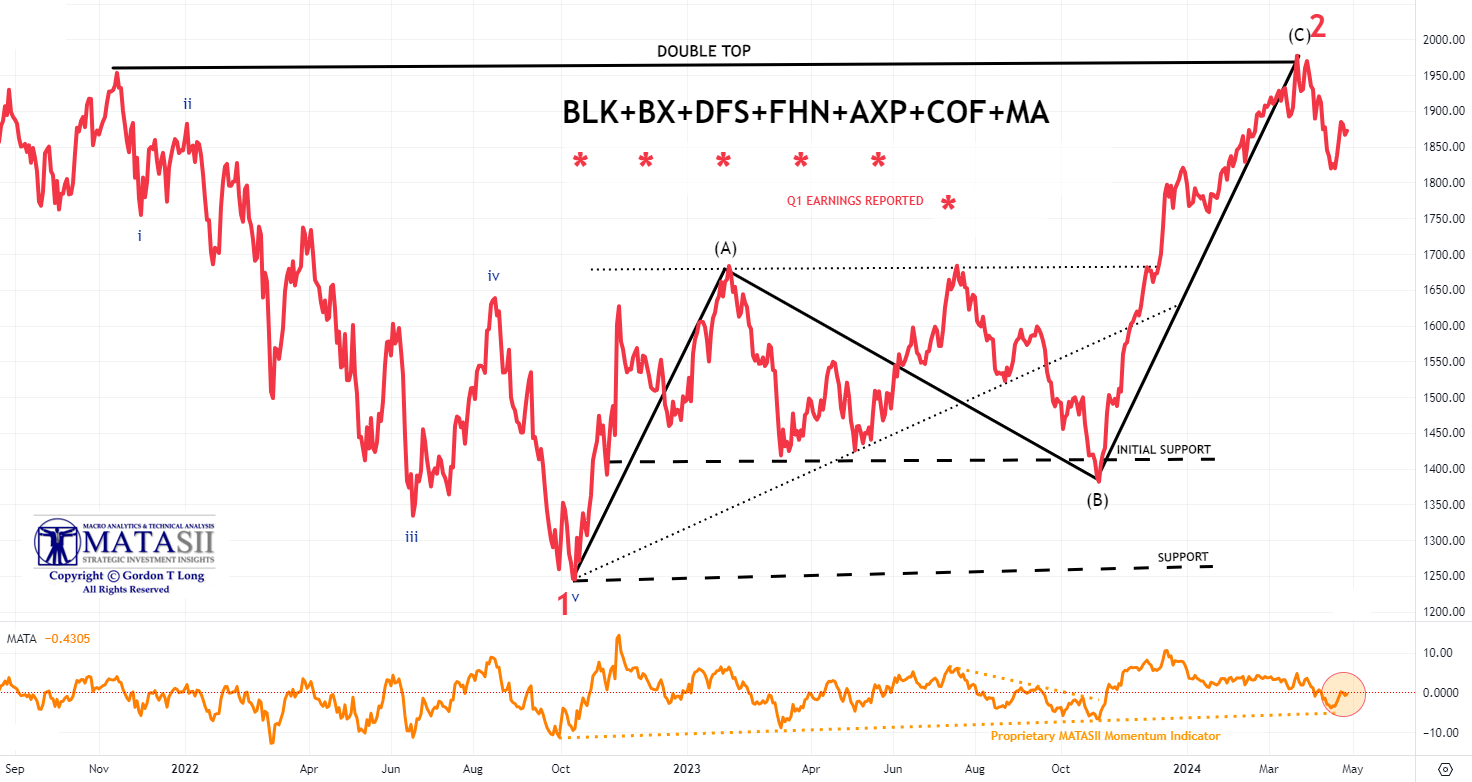

2- FINANCIALS STOCKS

The Financials appear to be trying to follow the Banking stocks higher against the overall trend of the market. The MATASII Financial Index has reached overhead momentum resistance (lower pane).

| |

|

2 - FUNDAMENTAL ANALYSIS

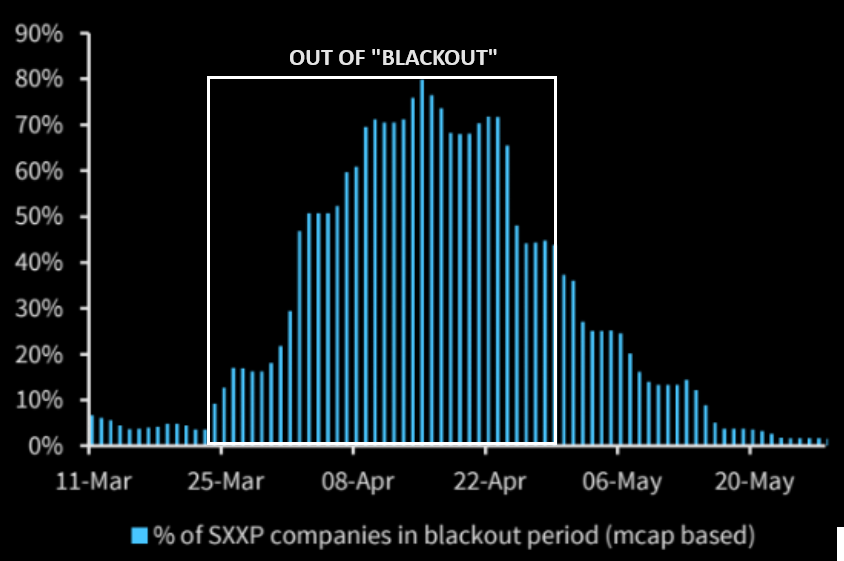

CORPORATE BUYBACKS

On the authorization front, 2024 YTD authorizations stand at $317.4B vs $377.0B 2023 YTD authorizations. Expectations are that authorizations this year will finish higher. Estimates for 2024 authorizations are to finish $1.15T (up ~16%) according to Goldman Sachs.

CHART RIGHT: Buyback blackout window ending.

CHART BELOW

Buyback yield strategy has outperformed in the US, where buybacks and therefore compounding have been part of the equity culture for a long time.

| |

|

CREDIT LEADS

The High Yield Credit sector as represented by the "JNK" is currently reflecting nothing more than a consolidation to the 200 DMA then completing a potential final leg up. Though expected to be of short duration this is normally good for the equity markets.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

3 - TECHNICAL ANALYSIS

OVERALL EQUITY MARKET

We are just above critical support lines in the Nasdaq. NASDAQ's short term must hold is down around the 17100 area. We are presently falling below the 100 day .

The 50 day is reversing and has just started sloping negatively. Indicates are we are slowly rolling over.

MAGNIFICENT 7

- We are reaching the vertical lift part of the parabolic (geometric) lift shown by the dashed red line.

- We have intermediate term Divergence with momentum (bottom pane).

In the short term Momentum has rolled over but hasn't yet decisively broken the Momentum trend line support.

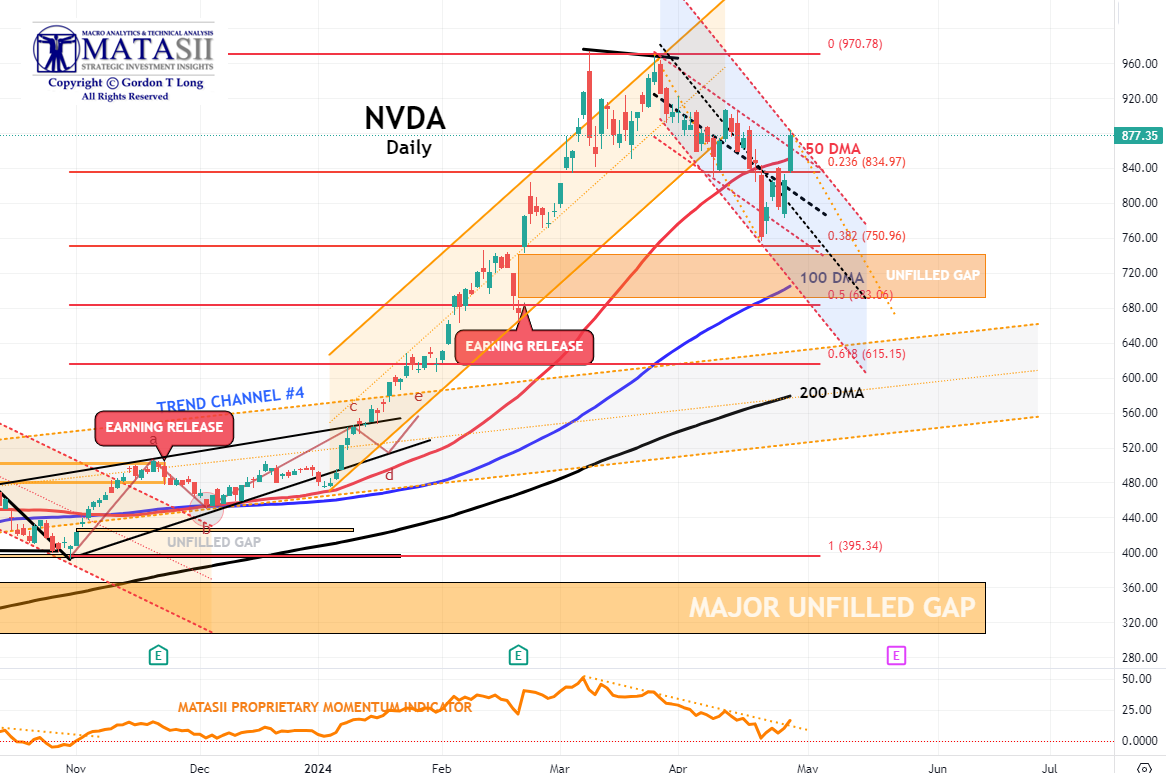

NVDA - Daily

- NVDA broke through the overhead 50 DMA on a retest.

- NVDA Momentum (lower pane) has also broken through its overhead resistance trend line.

- This counter rally is noticeably strong for NVDA and may lead the market higher - at least in the short term.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

"CURRENCY" MARKET (Currency, Gold, Black Gold (Oil) & Bitcoin)

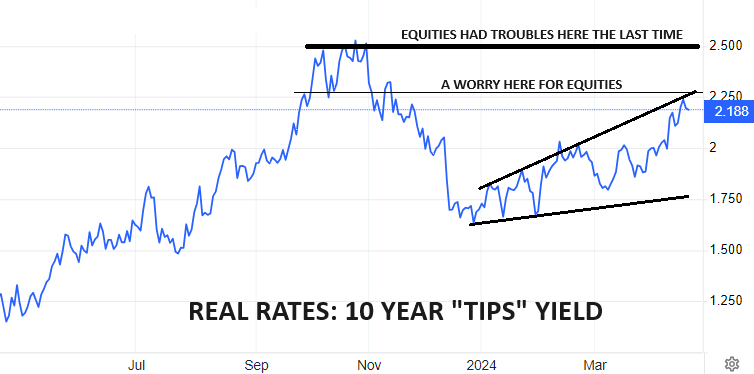

CHART RIGHT: As gold pushes to higher & higher record highs (in USD terms), Real yields have so far refused to play along (right)?? Normally Gold falls when real yields rise and are historically negatively correlated.

What we believe is that what we are seeing is Gold aggressively discounting a coming collapse in Real Rates which we expect between 2.25% - 2.5%.

CONTROL PACKAGE

There are NINE charts we have outlined in prior chart packages which we will continue to watch closely as a CURRENT "control set".

-

US DOLLAR -DXY - MONTHLY (CHART LINK)

-

US DOLLAR - DXY - DAILY (CHART LINK)

-

GOLD - DAILY (CHART LINK)

-

GOLD cfd's - DAILY (CHART LINK)

-

GOLD - Integrated - Barrick Gold (CHART LINK)

-

OIL - XLE - MONTHLY (CHART LINK)

-

OIL - WTIC - MONTHLY - (CHART LINK)

-

BITCOIN - BTCUSD - WEEKLY (CHART LINK)

-

10y TIPS - Real Rates - Daily (CHART LINK)

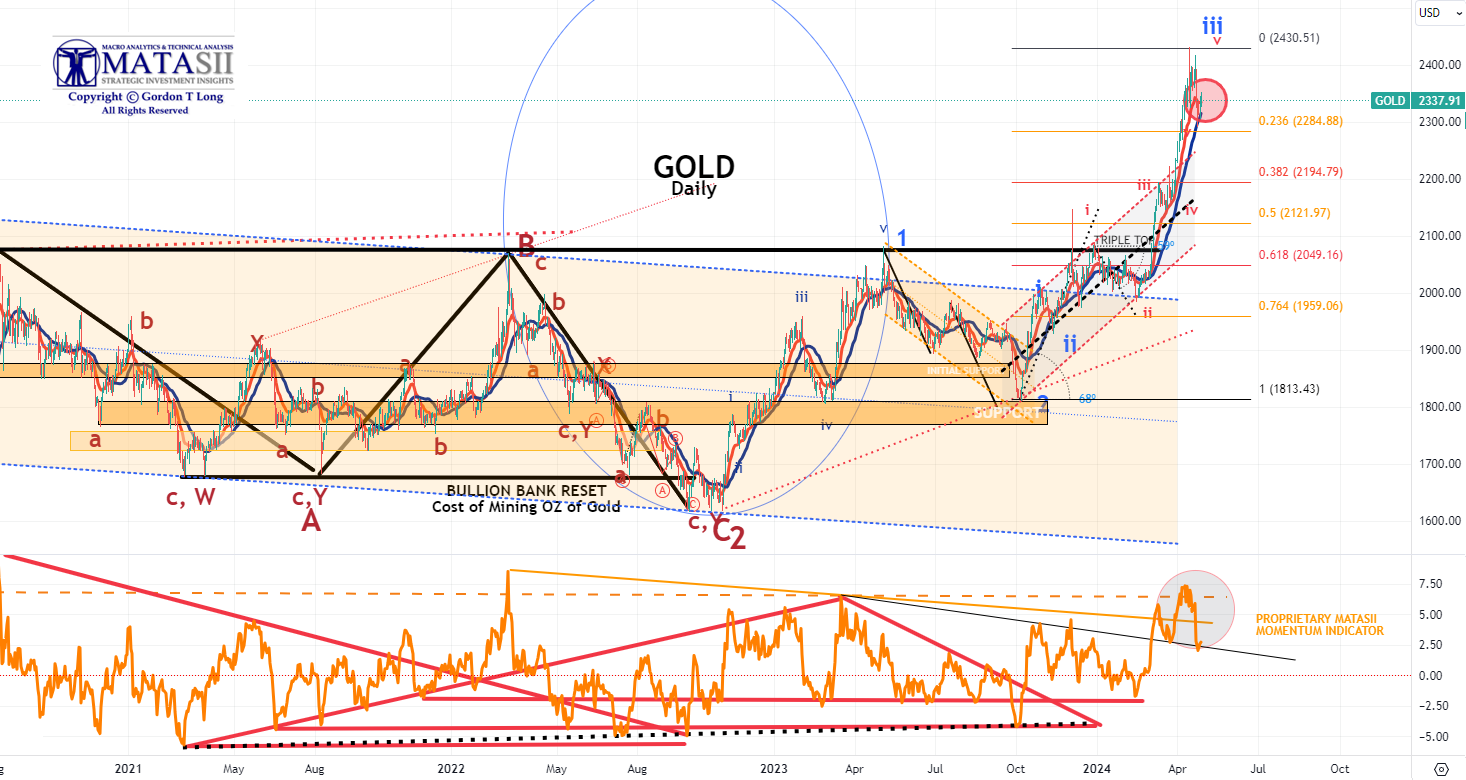

GOLD cfd's - DAILY

- Gold pulled back on Monday finding initial support at the 23.6% Fibonacci Retracement level.

- God Momentum (lower pane) also found support (dotted black trend line).

- It appears that this initial corrective leg is an "A" wave of an ABC corrective pattern before heading higher when completed. The "C" down leg of the ABC is likely to find firm support at the 38.2% Fibonacci Retracement level.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

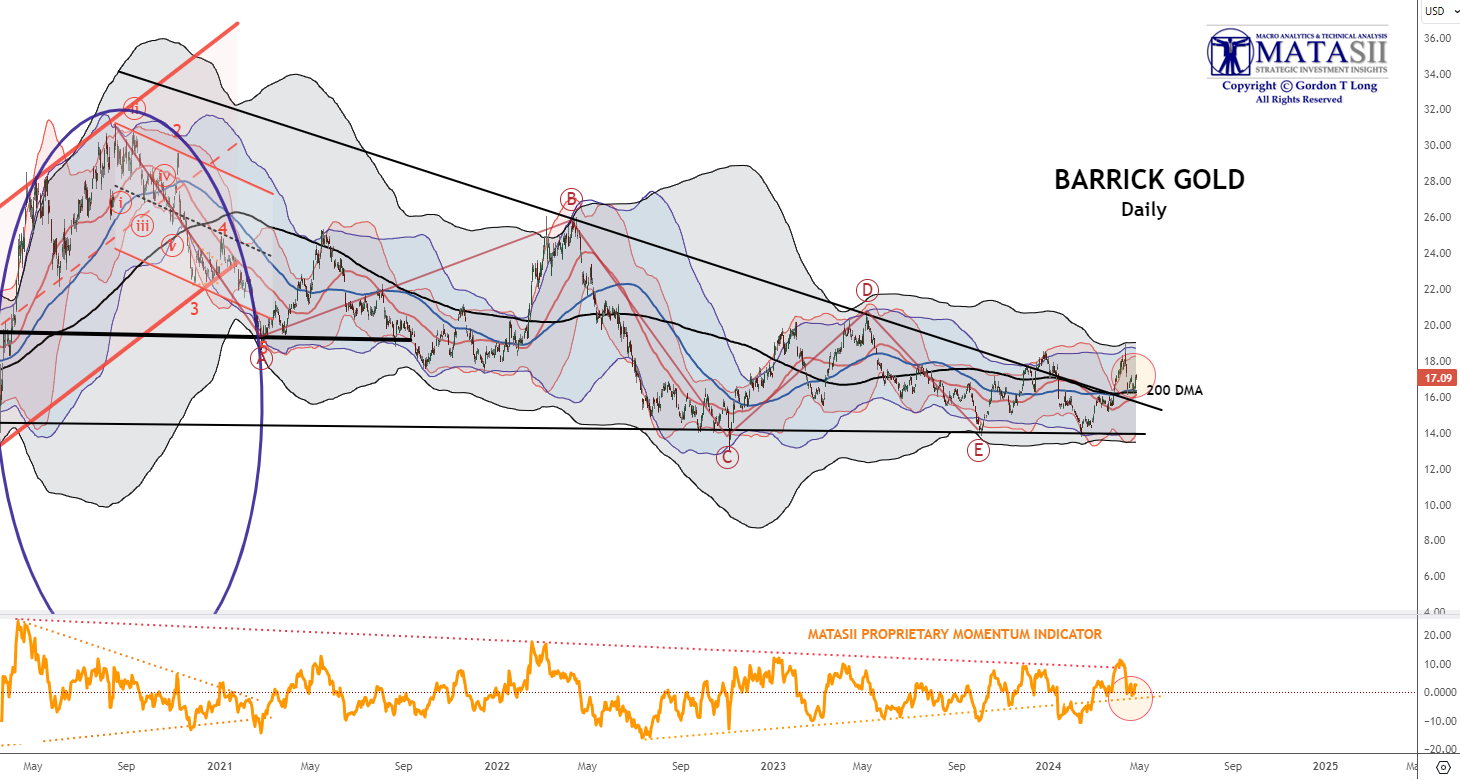

INTEGRATED GOLD MINERS

We continue to have a close eye on Gold and the INTEGRATED GOLD MINERS as represented by Barrick Gold. Barrick has broken out of its long term declining overhead resistance trend.

Barrick has been pulling back this week as Gold Bullion has. It may be a good opportunity to be adding to your Gold and Silver positions on any further pullbacks.

| |

|

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

|

US EQUITY MARKETS

If this is a mild 5-10% correction, investor sentiment should bottom soon around neutral. (Chart Right)

CONTROL PACKAGE

There have FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set".

-

The S&P 500 (CHART LINK)

-

The DJIA (CHART LINK)

-

The Russell 2000 through the IWM ETF (CHART LINK),

-

The MAGNIFICENT SEVEN (CHART ABOVE WITH MATASII CROSS - LINK)

-

Nvidia (NVDA) (CHART LINK)

| |

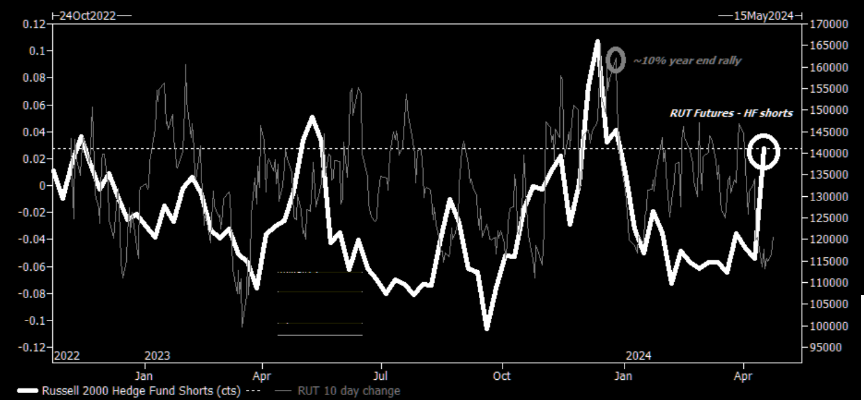

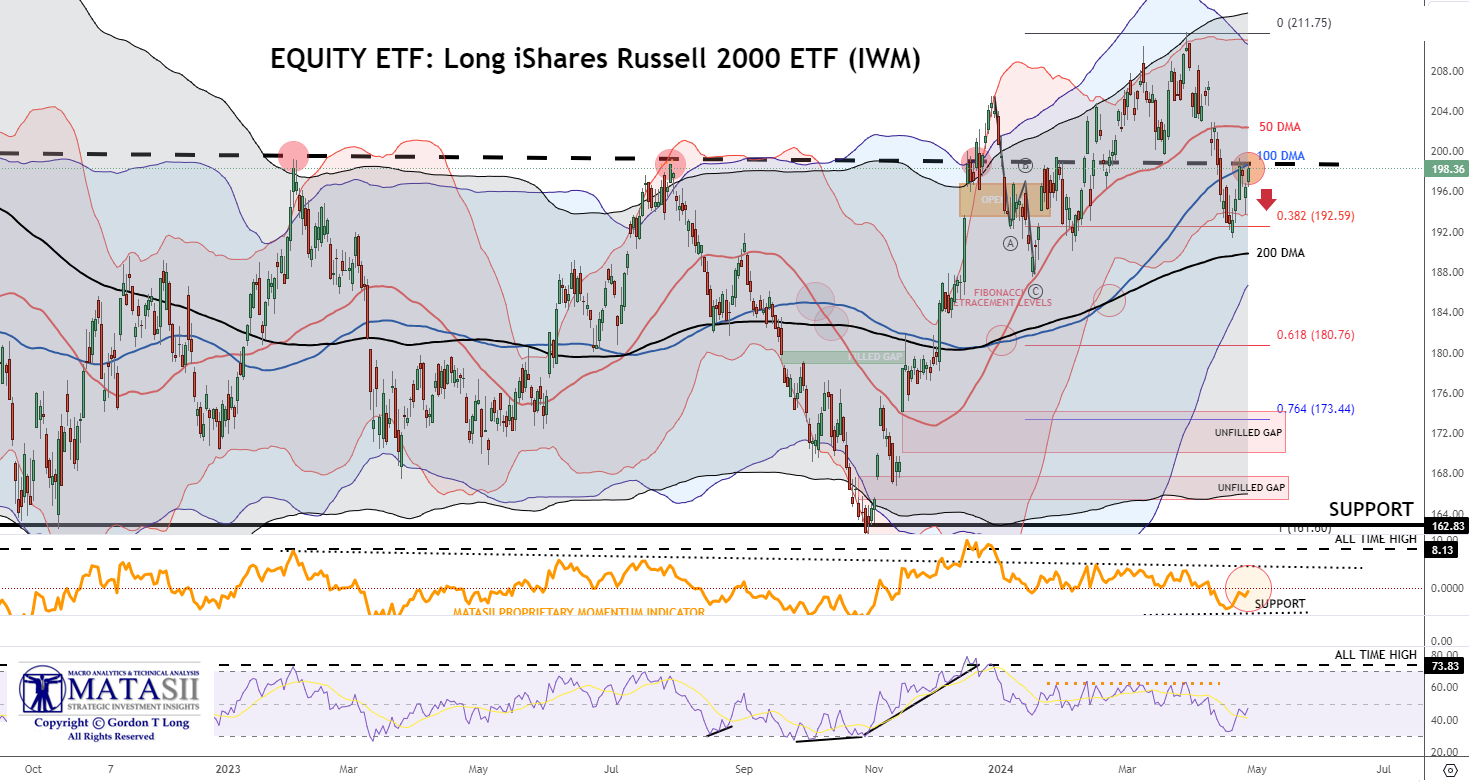

RUSSEL 2000

Hedge funds have been strongly adding RTY shorts!

NOTE: The positioning is approaching levels that preceded the sharp short covering we saw at the end of last year (CHART RIGHT)

EQUITY ETF: Long iShares Russell 2000 ETF (IWM)

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

NOTE: Though Hedge funds net bought global equities at the fastest pace in nearly 3 months as overall gross trading activity increased for the 16th straight week, driven by long buys outpacing short sales (~3.6 to 1) THE ACTIVITY HAS BEEN DOMINATELY SLANTED TOWARDS THE EU.

Earnings sentiment for Europe is trending upwards.(Chart Right)

| |

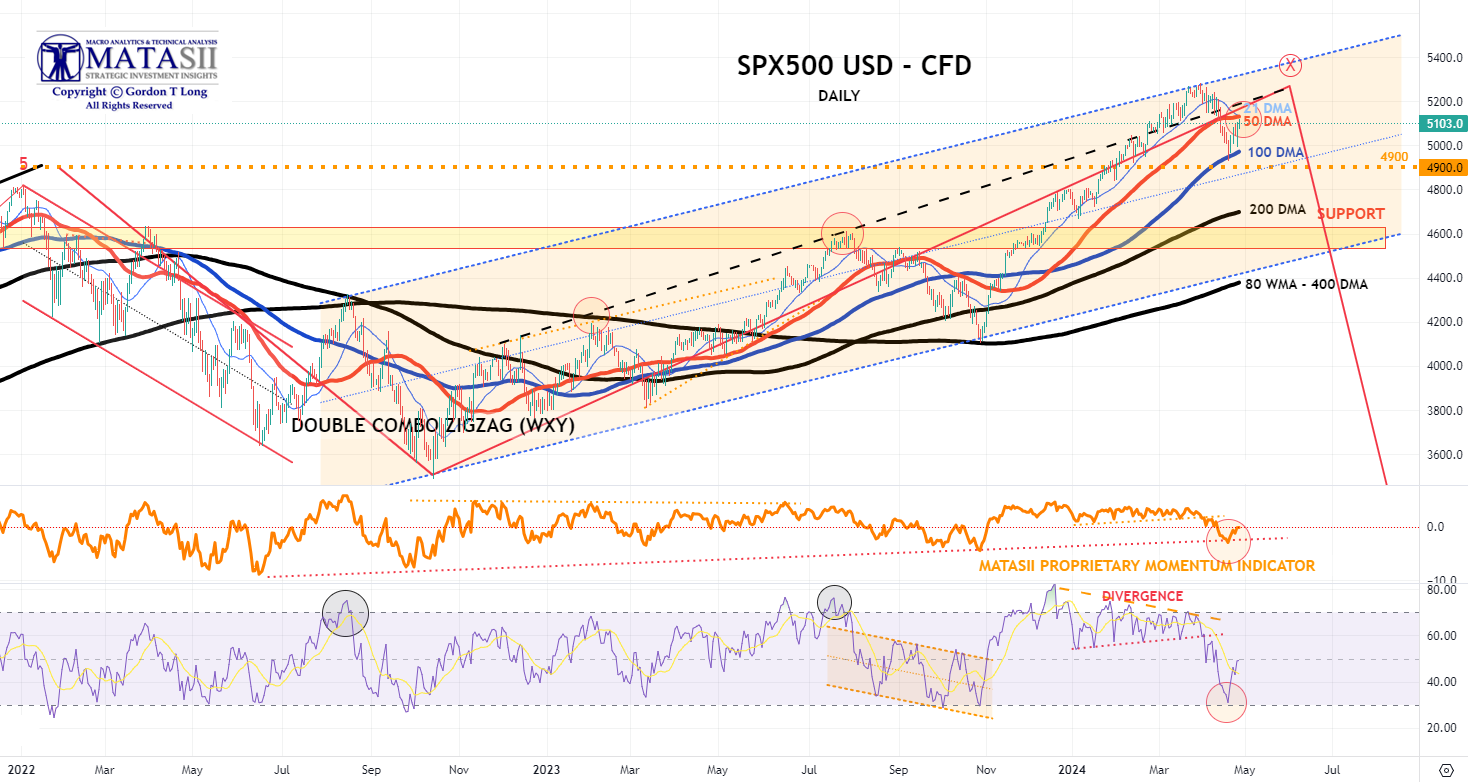

S&P 500 CFD

The S&P 500 cfd bounced off its 100 DMA an subsequently retraced to test its 50 DMA. Momentum (lower pane) also bounced off its lower support to a more neutral level.

| |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

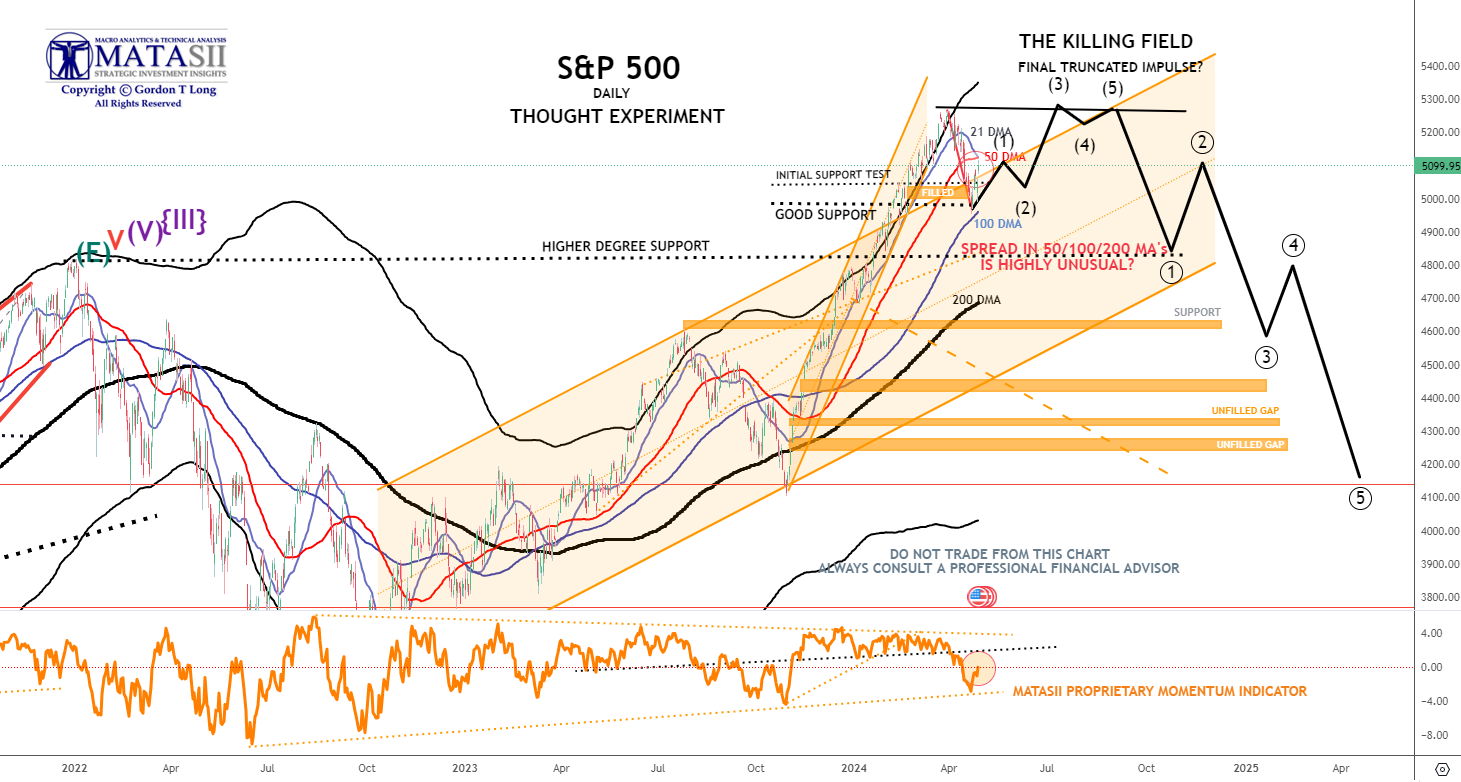

S&P 500 - Daily - Our Though Experiment

CHART RIGHT: So far this is just a "normal" bounce post the sell off. 5150 is key in SPX to the upside. The short term negative trend line comes in there, as well as the 21 day moving average, sloping negatively these days.

Our Though Experiment, which we have discussed many times previously in the way of a projection, suggests we have put in a near term top (or very close to it) and will now consolidate before possibly completing one final small impulse higher OR put in a final Wave 5 of a higher degree.

NOTE: To reiterate what I previously wrote - "the black labeled activity shown below, between now and July, looks like a "Killing Field" where the algos take Day Traders, "Dip Buyers", the "Gamma Guys" and FOMO's all out on stretchers!"

- The S&P 500 found support at its lower 100 DMA before retracing upward to retest the underside of its 50 DMA.

- Momentum )lower pane) also found support at its lower trend support line before retracing towards its upper trend momentum. From a momentum perspective it appears to still have further upside to go.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

STOCK MONITOR: What We Spotted

MONDAY

- US stocks managed to claw back some of the prior week's losses, with a rebound in Nvidia (NVDA) shares and in semis supportive of the move, underpinning technology outperformance. Elsewhere gold and oil prices were lower on a lack of geopolitical escalation seen over the weekend which also weighed on Treasuries overnight. T-notes eventually settled flat, paring the overnight losses as it tracked the bund higher ahead of a plethora of key risk events. In FX, the Dollar was flat while the Yen hit a 34-year low vs the buck ahead of the BoJ later this week. Antipodes and CAD meanwhile outperformed on the risk revival. Focus this week lies on a plethora of earnings, Tier 1 US data, including GDP and PCE, as well as the BoJ rate decision.

STOCK SPECIFIC

- Informatica (INFA) -10.5%: Confirmed it is not engaged in acquisition discussions; reaffirms FY24 outlook.

- Tesla (TSLA) -2%: Cut prices across its entire line-up in China, as well as some in other markets.

- Li Auto (LI) -5.5%: Has slashed prices by roughly 5% on four of its five models.

- Vista Outdoor (VSTO) +6.5%: It is engaged in talks with MNC Capital, although adds that it anticipates MNC will bump its prior bid.

- Quanex (NX) -3%: To acquire Tyman in a USD 1.1bln transaction.

- CNH Industrial (CNHI) -7%: Appoints Gerrit Marx to replace Scott Wine as CEO, after the latter surprisingly left to pursue other interests.

- Alcoa (AA) +2%: Upgraded at Morgan Stanley.

- Cardinal Health (CAH) -5%: Will not renew its pharmaceutical distribution contracts with UnitedHealth's (UNH) OptumRx unit, which expires at the end of June 2024.

- Paramount (PARA) -0.5%: CNBC's Faber says no bid from Apollo (APO) and Sony (SONY) has been submitted for Paramount (PARA).

- Verizon (VZ) -4.5%: Posted a mixed report; revenue missed while profit beat.

- Boeing (BA) +0.4%: Expects a slower increase in the rate of the 787 production and deliveries due to supplier shortages on "a few key parts"; Boeing (BA) said it still plans to steadily increase its rate to meet strong demand.

- Wolfspeed (WOLF) +8%: Jana partners urges co. to consider a potential sale, and other strategic alternatives, to boost its share price, Reuters reported.

TUESDAY

- Stocks continued their rally after the slump seen last week. The majority of the upside was sparked after the soft US PMI data with some cautious commentary on the labor market supporting the dovish move. As a result, the Dollar sold off throughout the session while T-Notes bull steepened. The 2yr auction was solid but it had little market impact with the PMI data driving price action throughout the session. In FX, the Dollar lagged while Pound outperformed after hawkish commentary from BoE Chief Economist Pill despite dovish remarks from Ramsden on Friday. The Yen saw some strength overnight on remarks from Finance Minister Suzuki that last week's discussions in Washington have laid the groundwork for Japan to take appropriate FX action. There was also a Nikkei sources article noting the BoJ will discuss the rapid slide of the Yen at their meeting later this week; helping keep USD/JPY sub 155.00. EUR/USD reclaimed 1.07 thanks to the dollar weakness. Meanwhile, on earnings, UPS, GE and GM figures were strong although Materials name underwhelmed.

INFLATION BREAKEVENS: 5yr BEI -0.4bps at 2.467%, 10yr BEI -0.5bps at 2.409%, 30yr BEI -0.3bps at 2.352%.

REAL RATES: 10Y -- 2.2285%

STOCK SPECIFIC

- Apple (AAPL) +0.5%: iPhone sales in China -19% in Q1 and down 24% Y/Y in the first six weeks of the year, according to Counterpoint Research.

- HashiCorp (HCP) +19.5%: IBM (IBM) reportedly nears a deal for HashiCorp, according to WSJ.

WEDNESDAY

- Stocks were sold on Wednesday with losses led by the Nasdaq as the Tech sector underperformed with semis weighed on by a poor ASML earnings report.

- Stocks had pared some of the weakness after a stellar 20yr bond auction before selling resumed into the closing bell.

- Elsewhere, the Dollar was sold as it tracked US yields lower which in turn supported the Yen, Franc and Euro but the Antipodes outperformed despite the risk-off tone of trade.

- GBP only saw slight gains vs the Buck but it was weaker vs the Euro despite hotter-than-expected inflation, but BoE officials did not seem too concerned. There were few developments on geopolitics today other than reports suggesting Israel was going to respond to Iran on Monday, but ultimately decided to wait - a response seems a given but it is still a matter of when and how.

- Elsewhere, trade concerns between the US and China are rising after US President Biden was calling for higher tariffs on Chinese steel.

- The lack of updates saw oil prices pare some of the recent strength with inventory data showing a larger build than expected supporting the move while gold prices saw slight losses, despite the weaker dollar.

- Attention turns to more Fed speak overnight and on Thursday, with Thursday US data focusing on Jobless Claims, Existing Homes Sales and the Philly Fed business index.

INFLATION BREAKEVENS: 5yr BEI +0.1bps at 2.468%, 10yr BEI +0.2bps at 2.411%, 30yr BEI +1.1bps at 2.362%.

REAL RATES: 10Y -- 2.241%

STOCK SPECIFIC

- Tapestry (TPR) -1% Capri (CPRI) -3%: FTC is preparing to sue to block Tapestry's USD 8.5bln takeover of Capri Holdings, according to NYT.

- Mobileye (MBLY) +3%: Secured orders for 46mln of the EyeQ6 Lite driver-assistance chips.

- Eli Lilly (LLY) +0.5%: Weight loss drug (Trezepatide) met all primary endpoints and key secondary endpoints in two Phase 3 clinical trials.

- Sage Therapeutics (SAGE) -20%: Phase 2 study of dalzanemdor did not meet primary endpoint.

- Autodesk (ADSK) -6%: Said it will further delay its annual 10-K filing due to an ongoing internal investigation of its board of directors.

- Knight-Swift Transportation (KNX) -4%: Lowers Q1 and Q2 guidance.

- Microsoft (MSFT) -0.7%: To reportedly avoid a formal EU probe over USD 13bln OpenAI deal, according to Bloomberg.

- Zuora (ZUO) +12%: Exploring potential options after receiving acquisition interest from potential buyers, according to Reuters sources.

- Snap (SNAP) +5%: US House Speaker Johnson says TikTok divest-or-ban bill is moving fast through Congress.

- Nvidia (NVDA) -3.5%: Set to acquire AI infrastructure orchestration and management platform Run:ai for around USD 700mln in the coming days, according to Calcalist. NVDA later confirmed the news.

- Social Media (SNAP -2.5%, META-0.5%): Senate approved a bill that could see TikTok banned in the US.

- UnitedHealth's (UNH) +0.5%Optum ending virtual care is a positive for Teladoc (TDOC) +0.5%, according to BofA

- IBM (IBM) +0.8% is said to offer about USD 35/shr for HashiCorp (HCP) +7.5%, according to Bloomberg

- David Einhorn Greenlight Capital Letter: New buys in HPQ, PENN and ROIV, reduced stake in TECK.

- UK CMA reportedly seeks views on Microsoft (MSFT) and Amazon's (AMZN) AI partnerships, according to Bloomberg.

THURSDAY

- Stocks were lower on Wednesday after a plunge in META post-earnings and a hot Q1 Core PCE Prices figure, which introduced upside risks to Friday's March PCE data, saw Fed pricing shift hawkishly.

- However, the indices closed well off worst levels with semiconductors leading the recovery ahead of more key earnings with INTC, MSFT, and GOOGL all set to report after the close on Thursday.

- Treasuries bear-flattened after the hot Q1 core PCE prices, overlooking the lower than expected headline Q1 GDP, with the long-end recovery somewhat into the close; there was little reaction to the 7yr auction which saw average demand.

- The Dollar was eventually lower, unwinding initial strength on the data gradually, while USD/JPY hit new peaks of c. 155.75 ahead of the BoJ on Friday.

- Oil prices were firmer in choppy trade after losses on the stagflationary headline US GDP figures were unwound through the session.

- Metals saw strong gains.

INFLATION BREAKEVENS: 5yr BEI -2.0bps at 2.452%, 10yr BEI +1.9bps at 2.434%, 30yr BEI +2.8bps at 2.394%.

REAL RATES: 10Y -- 2.281%

FRIDAY

- Stock Indices saw strong gains on Friday (SPX +1%, NDX +1.7%) although that appeared mostly a big tech earnings story (GOOGL +10%, MSFT +2%) with the equal-weight S&P flat.

- The macro highlight was the March Core PCE, +0.32% M/M vs exp. +0.3%, which led to a kneejerk relief dovish reaction after the hot Q1 GDP Prices data on Thursday stoked concerns over a hot March core PCE print today, with the hot Q1 data largely a function of upward revisions to the January data.

- Treasuries bull-flattened after the data (10s -4bps at 4.67%), with the long end outperforming (2s flat at 5.00%) ahead of next week's month-end, QRA, and FOMC.

- The Dollar Index saw notable gains although that was largely a function of the Yen posting its largest one-day fall of the year after a lack of hawkishness or intervention commentary at the BoJ, with USD/JPY hitting a new peak of 157.92 here at the close despite an earlier mini flash crash to lows of 155.00.

- Oil futures were modestly firmer in choppy trade, affirming a W/W gain for the first time in three weeks with little market-moving energy news flow.

- Metals saw strength.

INFLATION BREAKEVENS: 5yr BEI +0.5bps at 2.457%, 10yr BEI +0.3bps at 2.438%, 30yr BEI +0.7bps at 2.399%.REAL RATES: 10Y -- 2.247%

STOCK SPECIFIC

- U.S. Silica Holdings (SLCA) +21.5%: Apollo Funds is to acquire U.S. Silica Holdings for USD 15.50/shr in cash, according to Bloomberg. Note, SLCA closed Thursday at USD 13.06/shr.

- Boeing (BA) +0.5%: Fitch revises Boeing's outlook to negative, but affirmed Boeing's 'BBB-' long-term issuer default rating and 'F3' short-term IDR.

- Paramount (PARA) -2%: Reportedly considering removing CEO Bob Bakish as turmoil over sales talks deepen, according to WSJ.

| |

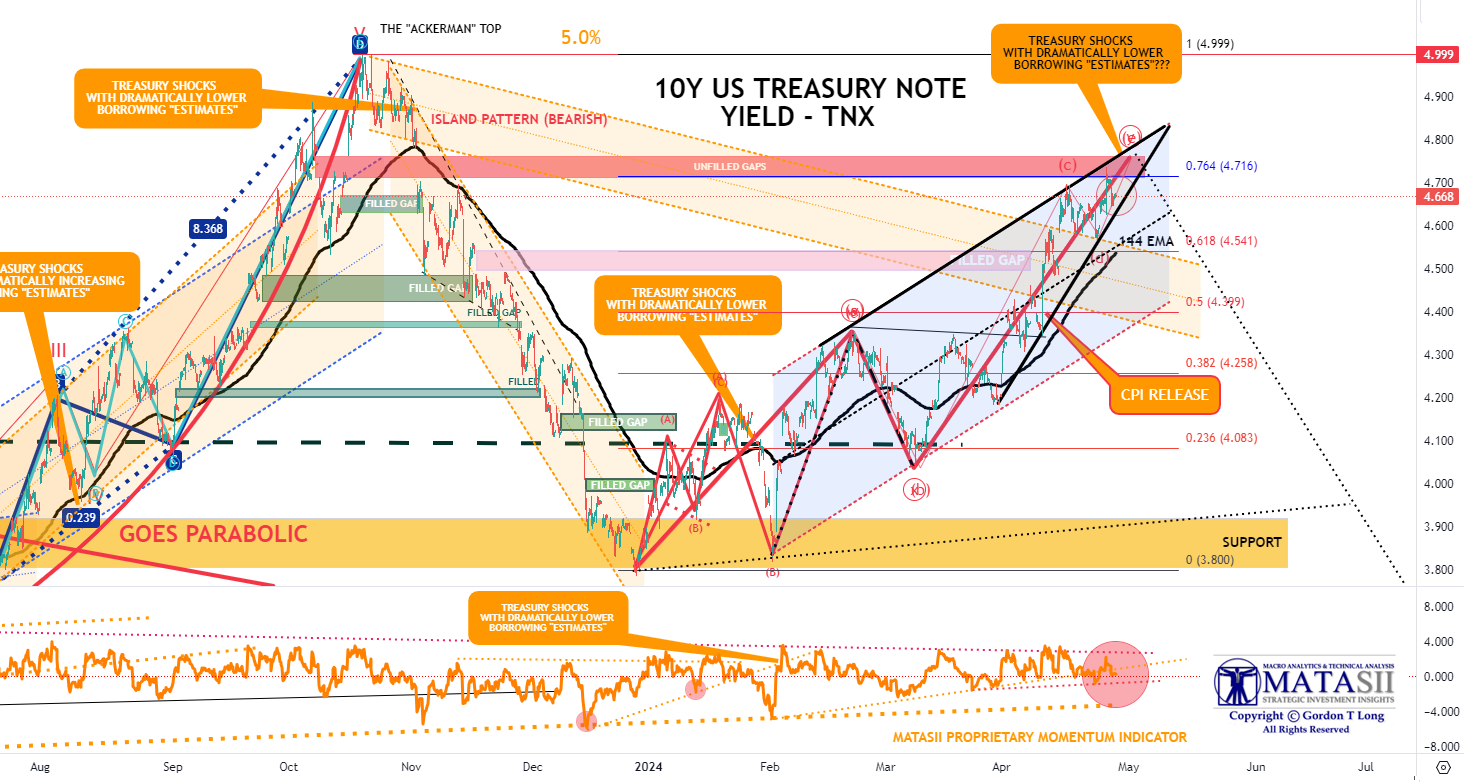

BOND MARKET

CONTROL PACKAGE

There have FIVE charts we have outlined in prior chart packages that we will continue to watch closely as a CURRENT "control set".

- The 10Y TREASURY NOTE YIELD - TNX - HOURLY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - DAILY (CHART LINK)

- The 10Y TREASURY NOTE YIELD - TNX - WEEKLY (CHART LINK)

- The 30Y TREASURY BOND YIELD - TNX - WEEKLY (CHART LINK)

- REAL RATES (CHART LINK)

FISHER'S EQUATION = 10Y Yield = 10Y INFLATION BE% +REAL % = 2.438% + 2.247% = 4.685%

THURSDAY 7Y TREASURY AUCTION

- A respectable, albeit not amazing, USD 44bln 7yr auction from the Treasury, stopping on the screws at 4.716%, not as strong as March's 0.8bp stop-through despite the c. 50bps of cheapening since then, albeit better than the six-auction avg. tail of 0.6bps.

- The auction was covered 2.48x beneath the prior 2.61x and avg. 2.57x.

- Dealers were left with 13.9%, more than March's 12.9% but beneath the avg. 15.1%, with the rise in Directs to 21% from 17.4% offset by the fall in Indirects to 65.1% from 69.7%.

- There were certainly some concerns that the rates volatility after the hot Q1 GDP prices release earlier on Thursday could have seen primary demand step back, but that has not been the case, despite the upside risks to Friday's March Core PCE data.

- Additionally, given the auction settles on April 30th, the offering likely benefitted from some month-end demand, given it is the last coupon auction of the month.

- Note also that next week's QRA is expected to be relatively uneventful, with the Treasury expected to keep coupon auction sizes unchanged.

- The Intermediate term rise in the 10Y TNX Yield appears to be completed with a touch of the 4.76%

- Monday's Treasury upcoming announcement of the size of auctions planned by treasury type and Wednesday QRA schedule of auctions with size will be extremely important to the Treasury market.

- Yellen has every incentive to signal slightly smaller sizes to the market now that she has taken the TGA to $1Trillion in size.

|  | |

YOUR DESKTOP / TABLET / PHONE ANNOTATED CHART

Macro Analytics Chart Above: SUBSCRIBER LINK

| |

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.

FAIR USE NOTICE This site contains copyrighted material the use of which has not always been specifically authorized by the copyright owner. We are making such material available in our efforts to advance understanding of environmental, political, human rights, economic, democracy, scientific, and social justice issues, etc. We believe this constitutes a ‘fair use’ of any such copyrighted material as provided for in section 107 of the US Copyright Law. In accordance with Title 17 U.S.C. Section 107, the material on this site is distributed without profit to those who have expressed a prior interest in receiving the included information for research and educational purposes. If you wish to use copyrighted material from this site for purposes of your own that go beyond ‘fair use’, you must obtain permission from the copyright owner.

========

| |

IDENTIFICATION OF HIGH PROBABILITY TARGET ZONES | |

Learn the HPTZ Methodology!

Identify areas of High Probability for market movements

Set up your charts with accurate Market Road Maps

Available at Amazon.com

| |

The Most Insightful Macro Analytics On The Web | | | | |