|

Highlights of January 2025 USDA Supply/Demand Report

H. Scott Stiles, Program Associate, Agricultural Economics, University of Arkansas

The USDA’s much larger than expected reductions in the U.S. corn and soybean crops in the January Annual Crop Production report changed the fundamental perspective of both balance sheets, putting the U.S. corn balance sheet on a similar footing to that of 2022/23 and now modestly “tighter” than last year.

The U.S. soybean balance sheet has shifted to being fundamentally similar to last year after previous ideas several months ago indicated the potential for the most burdensome stocks situation in five years. While export demand concerns still exist, particularly for soybeans, the extremely negative perception of ending stocks for U.S. corn and soybean expressed just a few months ago has abated for now.

The ultimate sizes of the South American crops and their impact on U.S. export demand will be a key focus of the markets in the months ahead. Trade and biofuel policies of the new Trump administration will also be closely watched issues for U.S. agriculture.

The rice market saw mostly favorable numbers from USDA with both the U.S. long-grain and medium grain balance sheets seeing tighter ending stocks this month. However, the U.S. cotton balance sheet saw mostly bearish revisions that included an increase in production and a sizeable 300,000 bale reduction in exports.

Corn

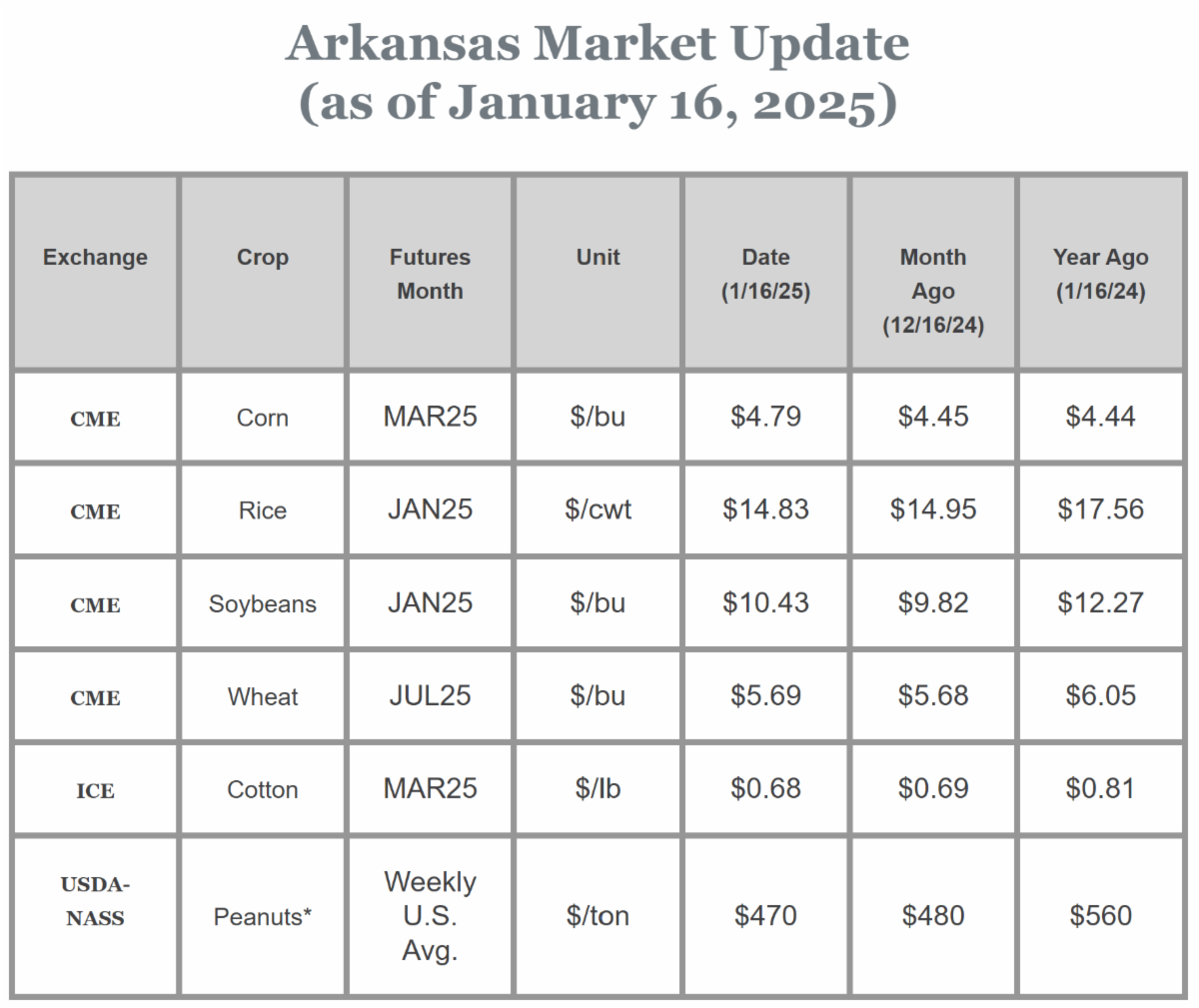

This month’s 2024/25 production is estimated at 14.9 billion bushels, down 276 million as a 3.8-bushel per acre cut in yield to 179.3 bushels was partially offset by a 0.2-million acre increase in harvested area. Total corn use was revised down 75 million bushels to 15.1 billion. Feed and residual use was reduced 50 million bushels to 5.8 billion. Exports were cut by 25 million bushels to 2.5 billion reflecting lower supplies. Ending stocks for 24/25 were lowered 198 million bushels to 1.54 billion and below last year’s 1.763 billion bushels. The season-average price received by producers was raised 15 cents to $4.25 per bushel

Soybeans

U.S. soybean production is estimated at 4.37 billion bushels, down 95 million from December. Harvested area is estimated at 86.1 million acres, down 0.2 million. Yield is estimated at 50.7 bushels per acre, down 1.0 bushel. With lower production, slightly higher imports, unchanged exports and crush, soybean ending stocks are projected at 380 million bushels, down 90 million from last month and comparable in size to last year’s 342 million bushel ending stocks. The U.S. season-average soybean price for 2024/25 is projected at $10.20 per bushel, unchanged from last month.

Rice

The NASS Crop Production Annual Summary estimated long-grain production at 172 million cwt, up 5.2 million from the previous estimate with the largest increases for Texas and Missouri. The long-grain average yield is estimated at a record 7,625 pounds per acre. Domestic and residual use was increased 6.0 million cwt to 128.0 million. Projected ending stocks were lowered by .8 million cwt to 30.3 million but 57 percent higher than the previous year’s stocks of 19.3 million. Adjustments were made to the 2024/25 season-average farm price forecasts. The Other State medium- and short-grain price was raised $0.30 per cwt to $14.80 on a 2.4 reduction in ending stocks, while the long-grain price was lowered $0.20 per cwt to $14.30 per cwt or $6.44 per bushel.

|