Advisor Solutions - Spring Edition |

|

Happy Spring!

As tax time comes and goes for another year, many of you are beginning to address your clients' charitable giving goals in earnest. With that in mind, our newsletter covers three topics that very well could be on your clients' minds as they emerge from winter and tax season.

Thank you for all you do for our community! We appreciate the opportunity to work with you as you serve your clients. Together, we are making our community a better place for everyone.

|

|

Christine

Senior Vice President Philanthropic Services

(831) 375-9712 x126

|

|

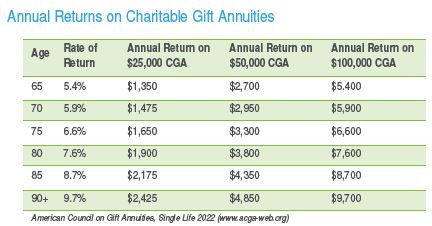

Charitable gift annuities (CGAs) are a good fit for your clients who like the idea of an up-front tax deduction, a steady lifetime income stream, and a remainder gift to charity. CGAs are increasing in popularity for a few reasons.

-

Increase in payout rates The American Council on Gift Annuities voted to increase the rate of return assumption from 4.50% to 5.25% effective on January 1, 2023.

-

New Legacy IRA opportunities New rules allow for a once-in-a-lifetime, $50,000 QCD from an IRA to a split-interest vehicle. CGAs created to receive a QCD contribution are different from other CGAs in a few important respects under the new law. For example, annuity payments are taxable, and must be at least 5%.

-

Tax benefits of gifts of appreciated assets Gifts of appreciated assets are always a strong planning technique, especially to a CGA. When a taxpayer contributes highly-appreciated stock to a CGA, the taxpayer typically is eligible for an income tax deduction at the stock’s fair market value on the date of the gift. When the recipient charity sells the stock, the charity pays no capital gains tax. Note that the taxpayer would have paid capital gains tax had the taxpayer sold the stock. Plus, the taxpayer gets the benefit of the upfront tax deduction, presumably in a tax year where income is higher (and therefore taxed in higher brackets) than it will be when the taxpayer retires at a future date.

Contact us any time to run personalized gift illustrations for your clients.

|

|

IRA Qualified Charitable Distributions for

|

|

Most attorneys, accountants, and financial advisors are well-aware of donor-advised funds and the reasons behind their popularity. Especially when a donor-advised fund is established at the CFMC, this vehicle is an excellent way for your clients to organize their charitable giving and get even more connected to the causes they care about.

Your clients can give nearly any type of asset to a donor-advised fund. A notable exception, though, is the Qualified Charitable Distribution (QCD). A QCD allows a taxpayer 70 ½ or older to make a direct transfer of up to $100,000 annually from an IRA to a qualifying charity. A donor-advised fund is not considered to be a qualifying charity.

The Council on Foundations defines a “field of interest fund” as, “A fund held by a community foundation that is used for a specific charitable purpose such as education or health research.” Perhaps your client is passionate about cancer research, food insecurity or preserving works of art, for example. Your client selects the name of the fund (e.g., family name or cause-related) and then, the CFMC distributes grants from the field-of-interest fund in a way that is aligned with your client’s values and charitable wishes outlined in the fund documentation.

Designated funds are defined as, “A type of restricted fund in which the fund beneficiaries are specified by the grantors.” These are a good choice for a client who knows they want to support a particular charity or charities for multiple years. The client names the fund and the CFMC fulfills the distributions. Distributions are aligned with your client’s wishes set forth in the original fund document.

For the client aged 70 ½ through 72, a QCD removes funds from an IRA before the client reaches the age-73 threshold for Required Minimum Distributions (RMDs). This can lessen the eventual income tax hit that accompanies RMDs. And for RMD-applicable clients, the QCD counts toward their RMD. In both cases, the QCD transfers do not fall into the client’s taxable income.

|

|

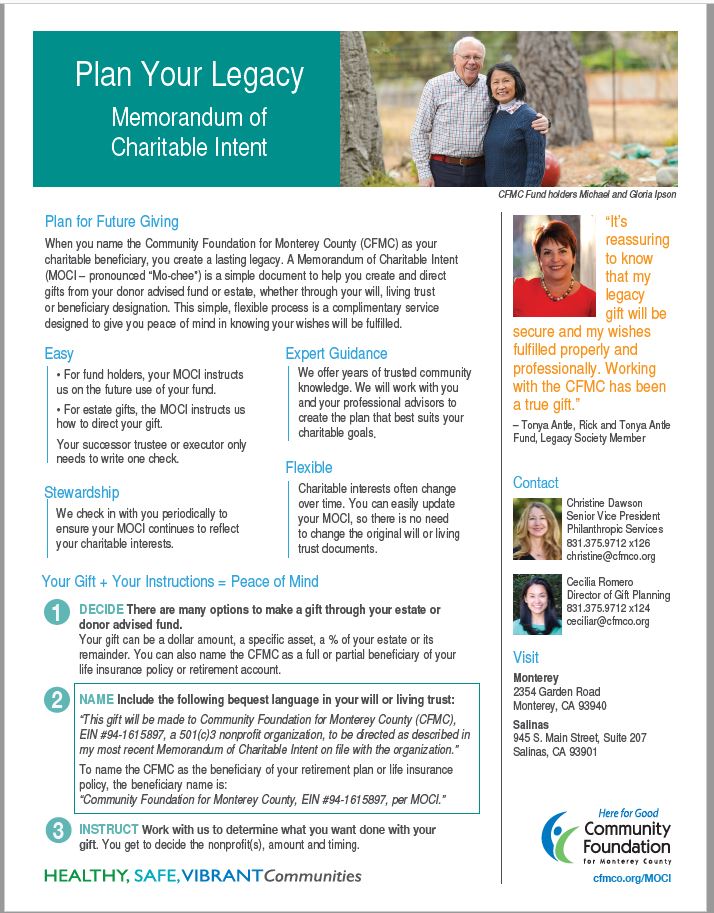

A Memorandum of Charitable Intent (MOCI – pronounced “Mo-chee”) is a simple document to help your clients create and direct gifts from their donor advised fund or estate, whether by will, living trust or beneficiary designation. This simple, flexible process is a complimentary service to our community and designed to give donors peace of mind in knowing their wishes will be fulfilled.

For current fund holders, their MOCI instructs us on the future use of their fund. For estate gifts, the MOCI instructs us how to direct their gift. A MOCI also offers flexibility. At the CFMC, we know that that charitable interests often change over time. MOCIs can be easily updated, so there is no need to change the original will or living trust documents. Please contact Cecilia Romero at 831.754.5880 with any questions or to help your clients get started.

|

|

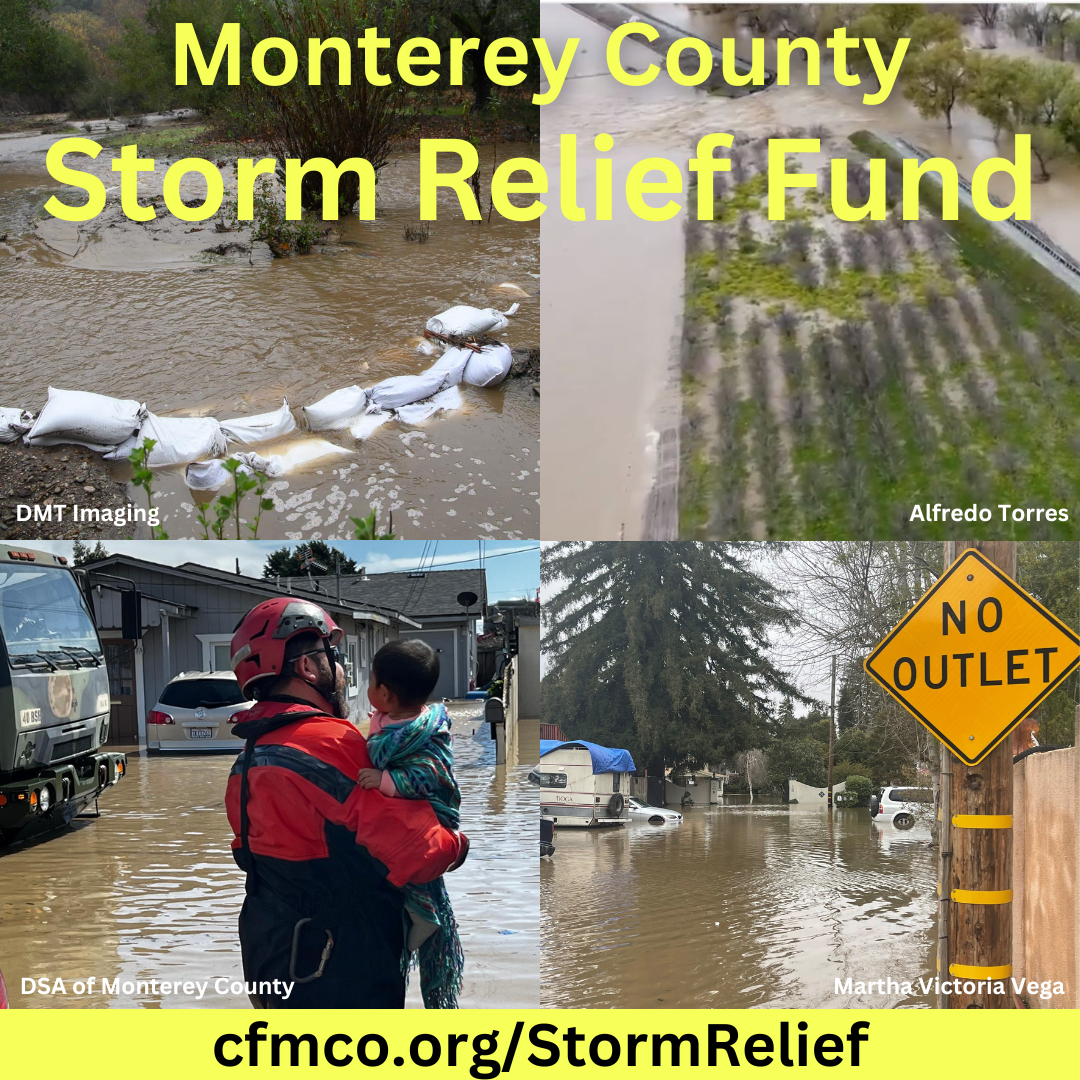

Unfortunately, disaster relief efforts have become far too common over the last few years. The CFMC can help your clients respond as a trusted partner. The CFMC Monterey County Storm Relief Fund has processed hundreds of gifts, including grants from DAFs and private foundations, and granted more than $1 million for storm relief and recovery.

Working with the CFMC helps your clients steer clear of scam sites which proliferate after disasters, whether near or far and can help secure tax planning benefits that can be missed when a client gives to charity on their own.

|

|

This guide (a CFMC publication) covers many ways donors can give during their lifetime or through their estate. You can view or download a copy online, or to request printed copies, please contact Cecilia Romero at 831.754.5880 x124.

|

|

Please contact Cecilia Romero, Director of Gift Planning, at ceciliar@cfmco.org or (831) 754-5880 x124.

|

|

|

The team at CFMC is pleased to be a resource and sounding board as you serve your clients. We understand the charitable side of the equation and are happy to help you find the best solutions to meet your clients’ needs. This newsletter is provided for informational purposes only. It is not intended as legal, accounting, or financial planning advice. |

|

To inspire philanthropy and be a catalyst for strengthening communities throughout Monterey County |

|

|

|

|

|

|