Weekly update from the National Housing Conference |

|

In this issue

April 30, 2023

Issue 92-15

· Senate hearing looks to address housing challenges

· Congressional members update, introduce housing-focused legislation

· HUD provides $5 million to address youth homelessness, $15 million for seniors

· HUD updating criminal record guidance

· HUD seeks comments on revisions to accessibility regulations

· CFPB issues zombie mortgage advisory opinion

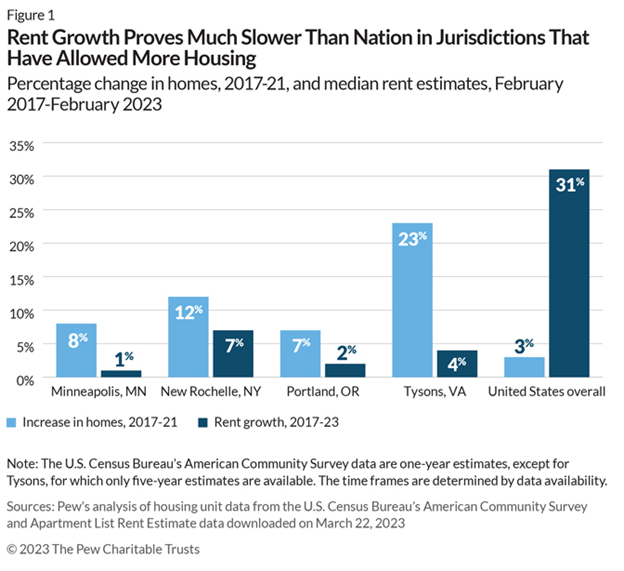

Chart of the week: : Zoning changes slow rent growth in some cities

|

|

Much Ado About Nothing – No one is paying more for a higher downpayment or a better credit score!

By David M. Dworkin

Last weekend, the Wall Street Journal wrote a scathing editorial alleging that “a new rule will raise mortgage fees for borrowers with good credit to subsidize higher-risk borrowers.” The truth is no one with the same credit score will pay more for making a larger downpayment, and no one with the same downpayment will pay more for having a better credit score. Those with good credit scores will not be subsidizing those with worse credit scores.

The problem is that most people don’t read mortgage pricing grids. What started as an ill-informed debate on an overly complicated mortgage policy was turned into a cynical way to draw homeownership into the “culture wars.” It won’t work. So, let’s take a careful look at the details and explain what happened, what is being done, and what we need to do to be sure that everyone is treated fairly when it comes to how much it costs to get a mortgage.

What was alleged

The Journal claimed that “under the rule, which goes into effect May 1, home buyers with a good credit score over 680 will pay about $40 more each month on a $400,000 loan. Those who make down payments of 20% on their homes will pay the highest fees. Those payments will then be used to subsidize higher-risk borrowers through lower fees.” Their conclusion was that this is a “socialization of risk” that “flies against every rational economic model, while encouraging housing market dysfunction and putting taxpayers at risk for higher default rates.” This is simply not true. The taxpayers are not at any higher risk, and neither are homebuyers, lenders, or anyone else. The allegations look at one aspect of a complex equation that charges more for some people with higher downpayments – which it shouldn’t – but it is wiped out by other parts of the equation.

Dave Stevens, a former president of the Mortgage Bankers Association and FHA Commissioner during the Obama Administration wrote about the new pricing grids in an op-ed in Housing Wire on February 6, just a couple of weeks after the new grids were made public. It’s pretty deep in the weeds, and not a lot of people noticed it (including me). He suggested that this was an effort to “push the GSEs to provide better execution for first-time homebuyers with lower [credit] scores, many of whom will be minority borrowers, [as] has been called for by civil rights and consumer activists for years.” The GSEs are the Government-Sponsored Enterprises Fannie Mae and Freddie Mac. The grids are Loan Level Price Adjustments (LLPAs) charged on some GSE loans as an extra fee to protect against credit risk traditionally covered by mortgage insurance, required on GSE loans with down payments under 20%.

The issue was picked up by the New York Post on April 16, with the headline “How the US is subsidizing high-risk homebuyers — at the cost of those with good credit.” It didn’t take long for FOX Business News to pick up the story a few days after that, where Stevens said he had just received an email from a lender who said, “so I guess we have to teach borrowers to worsen their credit before they apply for a loan.” It’s a clever talking point. It just happens to be completely wrong, but perfect for three news outlets owned by Rupert Murdoch. more...

|

|

News from Washington | By Brittany Webb

|

|

|

Senate hearing looks to address housing challenges

The Senate Committee on Banking, Housing, and Urban Affairs held a hearing on Wednesday titled “Building Consensus to Address Housing Challenges” that covered a wide range of housing industry issues that make housing unaffordable. The hearing featured testimony from Lou Tisler, Executive Director of the National NeighborWorks Association (NNA), Vanessa Brown Calder, Director of Opportunity and Family Policy Studies at the Cato Institute, and Diane Yentel, President and CEO of the National Low Income Housing Coalition. Each spoke to what Congress could do to help ease pressures in the housing market. Examples include increasing the affordable housing supply, limiting regulatory constraints, and passing bipartisan housing-focused legislation. The witnesses mentioned a slew of different housing proposals during the hearing, including the Choice in Affordable Housing Act, the Family Stability and Opportunity Vouchers Act, the Eviction Crisis Act, the HOME Investment Partnership Reauthorization and Improvement Act of 2023, the Affordable Housing Credit Improvement Act, and the Neighborhood Homes Investment Act. “There is not one silver bullet to address all the housing challenges faced across our nation,” said Tisler during his testimony. “NNA knows from experience that broad consensus works, whether here on Capitol Hill or between our partners at the Mortgage Bankers Association, the National Association of Realtors, and the National Home Builders Association. Between organizations like ours and NeighborWorks America and the National Housing Conference; between the Housing Assistance Counsel and Grounded Solutions Network or the Affordable Housing Tax Credit Coalition and a host of others, including my colleagues testifying beside me today. The urgency of consensus is now and will lead to success in addressing our housing challenges. A consensus in addressing our housing challenges will show taxpayers that there are achievable solutions that are good for them, our communities, and our country.” The hearing touched on zoning and land use regulation, Housing First strategies to ending homelessness, the Low-Income Housing Tax Credit, flood insurance, and other issues, many of which the witnesses supported. Sen. Tina Smith (D-Minn.) said during the hearing, “I think that I hear Mr. Chair, that there is a significant amount of bipartisan agreement on how we might approach this and a clear understanding that we have a supply problem.”

|

|

|

|

|

Congressional members update, introduce housing-focused legislation

Congress members updated two housing bills last week, leading up to the Senate Committee on Banking, Housing, and Urban Affairs hearing “Building Consensus to Address Housing Challenges.” First, Sen. Tim Scott (R-S.C.), the Committee’s Ranking Member, released a discussion draft of his previously announced ROAD to Housing Act. The Act focuses on six categories of improvements, broken down into a section-by-section fact sheet. Within those categories are various housing-related program changes, including reforms to housing counseling and financial literacy programs, reforms to the Rental Assistance Demonstration program, creating incentives for small-dollar loans, authorization of the Moving to Work program, incentivizing local solutions to homelessness, increasing housing in Opportunity Zones, and requiring annual testimony from various agencies working to address housing issues. “Homes and communities aren’t built without hard work. So, after making requests from everyone else in this room, I want to make a promise myself to consistently stay at the table, making sure that housing affordability is not a hearing, but a theme that permeates throughout the entire year,” Scott said during the Committee’s hearing. Also last week, Rep. Adam Schiff (D-Calif.), Sen. Tim Kaine (D-Va.), and Rep. Scott Peters (D-Calif.) reintroduced the Fair Housing Improvement Act of 2023. The legislation aims to protect veterans and low-income families from housing discrimination by adding veteran status and source of income as protected classes under the Fair Housing Act of 1968. “Access to safe, affordable housing provides individuals with stability and opportunity, but too often, individuals have been denied housing because of how they pay rent,” said Kaine. “I’m proud to reintroduce this bill to protect veterans and low-income families from discrimination and expand access to housing for all Americans.” |

|

|

|

|

HUD provides $5 million to address youth homelessness, $15 million for seniors

L ast week, HUD announced $5 million in funding for new Family Unification Program (FUP) voucher assistance. FUP is a program through which public child welfare agencies (PCWAs) and Continuums of Care (CoCs) provide Housing Choice Voucher assistance to two groups: Families who lack adequate housing for their children and people between 18-24 years old who left foster care or will be leaving foster care within 90 days. HUD said the funding would support coordination among public housing authorities, PCWAs, and CoCs. “At HUD, we know that housing is critical in ending homelessness, and this funding opportunity helps us continue our mission of getting people into more permanent and stable housing. In addition, this funding will allow PHAs to effectively administer the Family Unification Program for youth and families who need it,” said HUD Secretary Marcia Fudge.

HUD also announced $15 million in awards to 13 nonprofits supporting low-income seniors. Through the Older Adults Home Modification Program (OAHMP), elderly homeowners can remain in their homes and make home modifications to improve their overall health and safety of their homes. This funding will deliver more than 1,900 seniors’ home modification services. See the full project summaries here

|

|

|

|

HUD updating criminal record guidance

HUD announced steps to ensure that housing opportunities are not denied to qualified people due to a criminal record. The department will issue a Notice of Proposed Rule Making in the upcoming weeks and develop updated regulations for public housing agencies and HUD-subsidized housing providers to apply principles of the Fair Housing Act better and address discrimination concerns. In addition, PHAs and HUD-affiliated owners will receive assistance to determine convictions relevant to health and safety and how to conduct individualized assessments when reviewing criminal records. HUD will also provide technical assistance to encourage grantees, PHAs, and housing owners to use HUD programs to provide housing and services that support people’s successful reentry into the community. This announcement follows a comprehensive review of HUD regulations to increase opportunities for qualified individuals, including not automatically denying an applicant due to a prior criminal conviction.

“This Fair Housing Month and Second Chance Month, HUD recognizes that current criminal justice and housing policies have denied those seeking rehabilitation a chance to lead better lives,” said HUD Secretary Fudge. “As we execute our action plan, I invite state and local housing agencies, owners, and property managers to partner with HUD to remove barriers to housing to people with criminal records and support people’s successful reentry to the community. Research shows that providing safe and affordable housing and supportive services so that people succeed during reentry makes our communities stronger and safer.”

|

|

|

|

|

HUD seeks comments on revisions to accessibility regulations

“Modern standards for accessible program design must reflect advances in building practices and technology. Hearing from the public, particularly stakeholders most directly impacted, is an integral part of HUD’s rulemaking process,” said Demetria McCain, HUD Principal Deputy Assistant Secretary for Fair Housing and Equal Opportunity. HUD is accepting comments through July 24.

|

|

|

|

|

CFPB issues zombie mortgage advisory opinion

The CFPB issued new guidance on silent second mortgages, also called zombie mortgages. The guidance clarifies that debt collectors threatening to bring a state court foreclosure action to collect a time-barred mortgage debt may violate the Fair Debt Collection Practices Act. In addition, the opinion notes that some debt collectors are demanding mortgage balances along, with interest and fees, for mortgages that are past the statute of limitations and may not be enforceable in court.

“Some debt collectors, who sat silent for a decade, are now pursuing homeowners on zombie mortgages inflated with interest and fees,” said CFPB Director Rohit Chopra. “We are making clear that threatening to sue to collect on expired zombie mortgage debt is illegal.” |

|

|

|

Zoning changes slow rent growth in some cities

New research from Pew Charitable Trusts examines zoning policy changes in four jurisdictions, Minneapolis, New Rochelle, N.Y., Portland, Ore., and Tysons, Va. The research finds that updating restrictive zoning policies can help improve housing affordability. According to the findings, the number of households in these four jurisdictions grew 7-22% between 2017 and 2021. But rent growth was minimal in these locations relative to the U.S. overall during that period. New Rochelle is a remarkably insightful example. The city permitted an average of 37 new homes annually in 2017 and 2018. After downtown rezoning allowed apartments, the average jumped to 989 for 2019 to 2021. Rent costs rose 12% from January 2017 to January 2020 and then declined 5% from January 2020 to February 2023 as the new apartments became available. |

|

An article in Yahoo Finance reports that a Boston University Initiative on Cities’ 2022 Menino Study of Mayors poll finds housing costs at the forefront of cities’ challenges. The poll asked 118 mayors from U.S. cities of 75,000 residents or more, with 81% saying housing costs are an issue. The survey’s authors noted they were surprised by how much housing costs stood out as a concern for mayors compared to inflation.

Harvard’s Joint Center for Housing Studies published a blog post examining the sociology of housing and how homes shape our social lives. It introduces a working paper that discusses the extent and consequences of urban decline and how to address housing in neighborhoods that have experienced such decline. The paper notes that urban decline has shaped racial inequities in neighborhoods. It is an ongoing reality for disinvested cities, but the paper highlights promising areas of study for responding to these issues.

The National Low Income Housing Coalition released a new Eviction Record Sealing and Expungement Toolkit. The toolkit provides information on eviction record-sealing protections nationwide. The toolkit also includes eviction-related legislation currently in place and recommendations for lawmakers developing new protections in their jurisdictions. |

|

Monday, May 1

Tuesday, May 2

Wednesday, May 3

Thursday, May 4

Saturday, May 6

|

|

The National Housing Conference is a diverse continuum of affordable housing stakeholders that convene and collaborate through dialogue, advocacy, research, and education, to develop equitable solutions that serve our common interest. |

|

Defending Our American Home since 1931 |

|

Copyright © 2022. All Rights Reserved. |

|

|

|

|

|

|