|

A recent survey found that 28% of workers are very confident about having enough money to live comfortably through their retirement years. At the same time, 27% are not confident.1

In 2001 congress passed a law that can help older workers make up for lost time. But few may understand how this generous offer can add up over time.2

The “catch-up” provision allows workers who are over age 50 to make contributions to their qualified retirement plans in excess of the limits imposed on younger workers.

How It Works

Contributions to a traditional 401(k) plan are limited to $20,500 in 2022. Those who are over age 50 – or who reach age 50 before the end of the year – may be eligible to set aside up to $27,000 in 2022.3

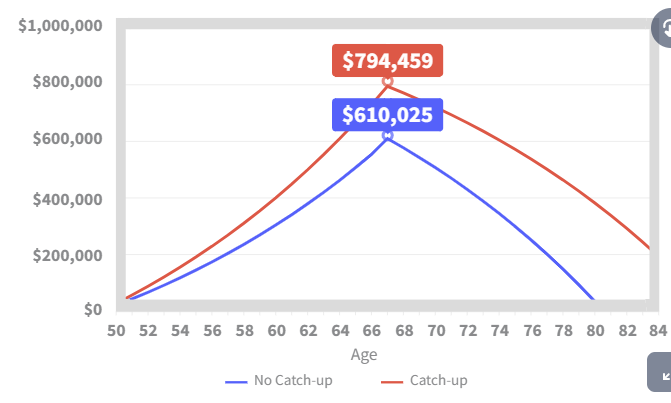

Setting aside an extra $6,500 each year into a tax-deferred retirement account has the potential to make a big difference in the eventual balance of the account. And by extension, in the eventual income the account may generate. (See accompanying chart.)

Catch-Up Contributions and the Bottom Line

This chart traces the hypothetical balances of two 401(k) plans. The blue line traces a 401(k) account into which $20,500 annual contributions are made each year. The green line traces a 401(k) account into which an additional $6,500 in contributions are made each year, for a total of $27,000 in contributions a year.

Upon reaching retirement at age 67, both accounts begin making withdrawals of $6,000 a month.

The hypothetical account without catch-up contributions will be exhausted by the time its beneficiary reaches age 81. Keep in mind, the IRS regularly updates these maximum contribution limits.

|