“Thank you for this series. I’m curious how the benchmark accounts for where the loan is in the cap structure? For example, recovery rates for unitranche, 1st lien and second lien are different. Any portfolio would have to match the composition to effectively compare against the benchmark. Otherwise, you would need different benchmarks for each.” – A Lead Left reader

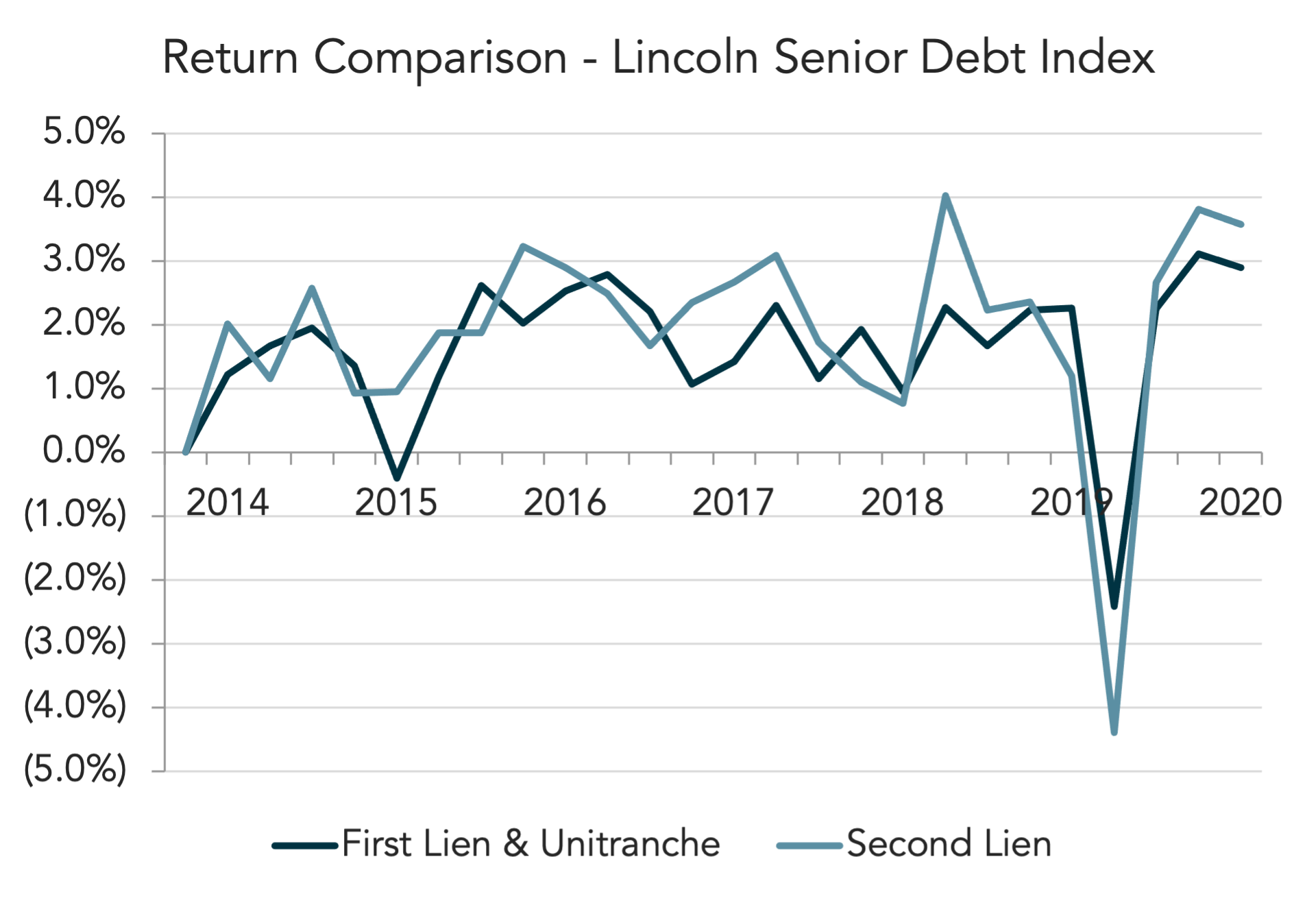

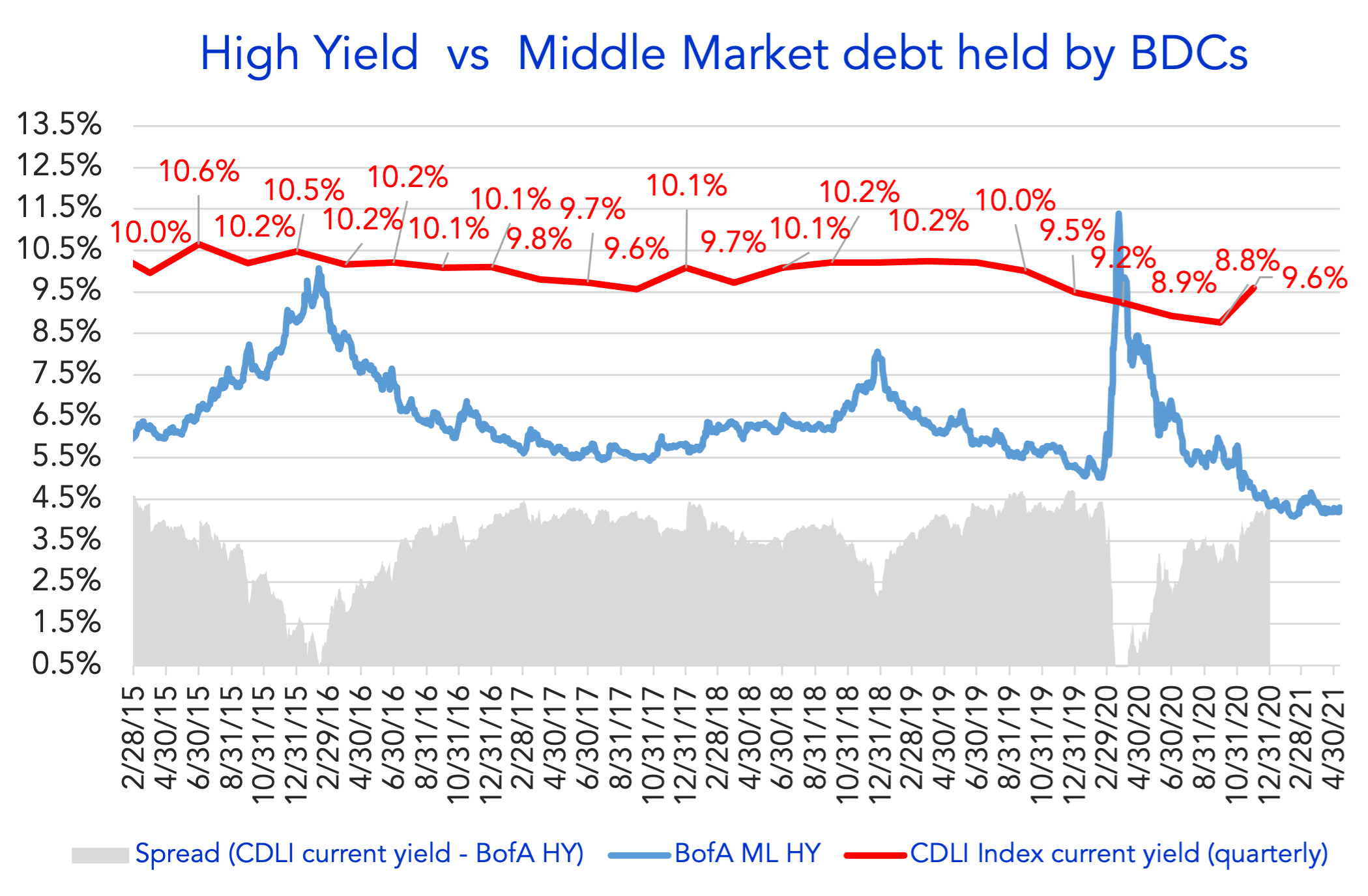

“We prepare various analyses of the Index. For example, looking at only first lien / unitranche, and separately, second lien. From a yield perspective, as one would expect, returns for second lien loans are higher but more volatile than first lien and unitranche. The latter shows average yields in our Index of 9.2%, while the former was 11.1%.

From a default viewpoint, Lincoln’s default rates and fair values of loans experiencing covenant defaults have been constructed two ways: equally weighted and size weighted. In certain periods, when there are meaningful differences between the two portfolios, we prefer size weighted data...