Dear CCIM Members,

We are in the beginning of the 4th quarter, crunch time! Let's all end the year strong. With that said, hope to see many of you at the CCIM Global Conference and Governance Meeting being held this week at the Westin Pittsburgh. Designees have a chance to attend some great networking and learning sessions. I'll also be attending the Pinning Ceremony for several candidates who are sitting for the exam along with a dinner with Region 11 on Friday.

With economic recovery heavily dependent on COVID, the length of this downturn remains uncertain. Adding to these worries, U.S. Congress must get it right with the 2022 budget unless the notion of the U.S. defaulting on its bond payments becomes a reality, which will clearly affect the stock markets.

CRE macro environment is being impacted similarly. But there is a dichotomy in operating fundamentals among property types—industrial real estate, health care, data centers, and cell towers have been positively disrupted, while offices, hotels, and retail have felt the negative effects. Multifamily and net leased investments remain steady and a reliable bright spot in primary and secondary markets due to demand.

Best,

-J.R.

(646) 481-3801

|

|

Join the New York Metro CCIM Chapter

|

|

Click HERE for RealtyZapp Onboarding/Training Recording.

|

|

Welcome to the Business of RE(Building). The CCIM Global Conference is designed to give you real-world solutions as the commercial real estate industry continues to reopen, recover, and rebuild. This year’s event will help you adapt and thrive in the new commercial real estate landscape.

With a combination of exclusive in-person events and virtual sessions, explore topics from across the renowned CCIM Institute curriculum as well as those affecting the industry in 2021 — all addressing the challenges facing CRE professionals amid the pandemic recovery and economic upheaval. The conference will also feature prominent industry leaders discussing the latest trends, the workforce of the future, decision-maker and growth strategies, and more.

Don't miss this year's CCIM Global Conference on in Pittsburgh on Oct. 9 and virtually on Oct. 19, 21, 26, and 28. Complete agenda and speaker details coming soon.

|

|

CHAPTER ANNOUNCEMENT

A PASSING OF A DEAR CCIM COLLEAGUE: JIM KINSEY, CCIM

|

|

Jim served as a Board of Director for the New York CCIM Chapter for many years and had hosted many leadership meetings at his Manhattan office.

It is with great sadness that I announce the passing of James Kinsey, a principal and COO at Avison Young’s New York City office who has died suddenly on Sept. 11, 2021, at the age of 44. Many of us personally know Jim and when I first came to New York City over 12 years ago, I had the fortune of meeting Jim who also invited me to grow his capital markets division within his firm.

Jim was a popular city broker who grew up in the real estate industry. He graduated from Boston College with a degree in music, but went to work with his late father, who ran a property management and development firm.

“After college, I realized that real estate was something I wanted to pursue too,” he told the New York Real Estate Journal in 2011. “Then a couple more years later, when my dad became ill, I stepped in and took responsibility for his property management and development firm.”

In 2000, Jim partnered with his late father to form Kinsey Capital Associates, a subsidiary of The Kinsey Corporation, that saw him add commercial real estate financing to the platform. In 2005, while simultaneously handling his responsibilities with The Kinsey Corporation, he formed Mason Real Estate LLC, a firm that handled residential sales and rental brokerage. Jim continued to manage its own and third-party properties across the city.

Jim also worked as a territory expert in the NoHo/NoLiTa market with Massey Knakal Realty before co-founding a new company, ERG Property Advisors, in 2009 with James and Richard Guarino. Believing that the market downturn presented an opportunity to combine forces with other industry veterans to build a more agile and diversified platform, Kinsey went on to work with industry leaders across various asset lines.

Bob Knakal, now chairman, NY Investment Sales with JLL Capital Markets, said, “Jim was a trusted and valued member of our old Massey Knakal family and we are deeply saddened by his passing. Jim was one of the good guys in the real estate industry.”

Kinsey joined Avison Young as a principal and director in 2018 and worked closely with veteran broker James Nelson to build the company’s investment sales and structured finance business in the tri-state area.

In a statement, Nelson said, “Jim was an incredible friend and business partner. He was loved by all and a truly remarkable individual. He did so much for those around him and we are grateful to have had him in our lives. Our hearts go out to his family during this incredibly difficult time.”

In an official statement, a spokesman for Avision Young said, “It is with great sadness that we mourn the loss of James (Jim) Kinsey, a beloved colleague, leader, mentor and friend. As Principal and Chief Operating Officer of Avison Young’s U.S. Capital Markets Group, Jim possessed invaluable wisdom, a strong work ethic and genuine love of both the real estate industry and wide variety of people in it. Our thoughts and prayers are with his wife Nicole, son Jim and daughter Noelle during this incredibly difficult time.”

Jim is survived by his wife Nicole Blanchette Kinsey and children James David Kinsey III and Noelle Olivia Kinsey and remembered as a dedicated family man and well respected professional. He loved the outdoors, music, art, and was an avid camper.

-JRC

|

|

FEATURE ARTICLE – NEW CRE SUB-CLASSES

The Digital Revolution Is Creating New Real Estate Sectors. Here's How To Profit

|

|

A new Netflix film studio in London, a hunt for hundreds of locations to park takeaway food delivery scooters and e-bikes, and JLL launching a global short-term apartment rental business. These disparate transactions, all in the last month, might seem unrelated, but they are tied together by a broader trend upending commercial real estate.

All of these transactions or strategies stem from the worldwide digital revolution, which is creating entirely new real estate assets classes and opening up vast possibilities in traditional sectors. The fact that an ever-growing part of our lives happens in the online world is, ironically, reshaping the physical world.

The shift from physical retail to e-commerce has been happening for a couple of decades, but now entirely new types of real estate like food delivery hubs and dark kitchens have been thrown into the mix. Property that has existed for more than a century, like film studios, is now on the radar of investors, and data centers are also evolving and growing in popularity as a real estate asset class. Even the humble vacation rental is becoming an institutional real estate type because of the impact of digitization.

Whereas once a real estate investor’s portfolio might have been dominated by offices, retail, multifamily and industrial, asset classes that are tiny today are likely to play a bigger role as the world changes and real estate investment tries to keep up. Buying into them is not simple, but has the potential to put you on the right side of historical change.

“Many of us in real estate thought very little about what Apple was doing or what the iPhone was going to offer until Steve Jobs decided to break the glass ceiling and come up with an incredible product,” Real Corp Capital founder Chris Kanwei said.

“No one really took note of what companies like Amazon, Apple or Alibaba were setting out to achieve, and the amount of disruption that they were going to bring into the space," he added. "But fast forward to where we are today, that needs to be ingrained in our thinking as part of our investment processes. Because we're still looking at incremental changes, but the current world we're in is a world of complete disruption, where things change incredibly fast.”

Below is a tour through four real estate sectors that could not exist in the non-digital world and some of the key trends shaping them right now:

Source: Bisnow

|

|

NATIONAL DEMOGRAPHIC TREND

Why Secondary Cities Are Pulling Ahead

|

|

Just two states account for half the top-performing metros, according to the National Association of Realtors.

Half of the strongest office markets were in Florida and Texas during the third quarter, with several secondary markets making the list, according to the National Association of Realtors’ latest Commercial Market Insights report.

NAR identified 10 metros with the best market conditions as of the third quarter. The secondary markets, with relatively affordable commercial and residential prices, are benefiting from in-migration, while large urban markets continue to struggle and many of their offices are still largely unoccupied due to the pandemic.

In alphabetical order, the top markets are: Austin, Texas; Boise, Idaho; Chattanooga, Tenn.; Daytona Beach, Fla.; Miami; Myrtle Beach, S.C.; Omaha, Neb.; Palm Beach, Fla.; Provo, Utah; and San Antonio, Texas.

NAR compared 10 local indicators to national figures in 390 commercial real estate markets including vacancy rate, 12-month net absorption, year-over-year rent growth, leasing volume, cap rate and sales transactions in both square feet and dollars. The report notes several small- and medium-sized metropolitan areas are seeing increases in office occupancy rates that are outperforming most large cities and the national average.

NAR Chief Economist Lawrence Yun said in a prepared statement the office market is the one real estate sector that is still lagging behind, even as the economy continues to make a steady recovery. Yun said work-from-home flexibility could be the defining shift of the post-pandemic economy. However, Yun pointed to some markets that are seeing more office occupancy and rising rents. He said a combination of strong in-migration and a relatively lower cost of doing business is driving the growth in those markets.

The NAR third-quarter report found the primary office markets are beginning a slow recovery with New York, Atlanta, Dallas and Seattle experiencing positive net absorption of office space in the third quarter. Due to the huge losses in office occupancy, office vacancy rates will likely remain above 10 percent for the next two years. The report stated 144.4 million square feet of office space has lost occupancy since the second quarter of 2020. The office vacancy rate increased from 9.8 percent in the first quarter of 2020 to 12.4 percent as of Aug. 22.

Industrial strength

The NAR third-quarter report said positive net absorption of industrial space more than offset the negative net absorption of office space during the same period. In the industrial market, 518.8 million square feet of space has been absorbed since the second quarter of 2020. The industrial vacancy rate has fallen from 5.3 percent in the first quarter of 2020 to 4.6 percent as of Sept. 19.

The report states the industrial market absorbed 113 million square feet in the second quarter of 2021—the most space ever absorbed in a single quarter. Still, demand continues to outpace supply, NAR noted, even with new supply totaling 190.1 million square feet delivering since the beginning of the year.

Markets with positive net absorption for the past 12 months included Dallas-Fort Worth; Chicago; Atlanta; Phoenix; Houston; Los Angeles; Indianapolis; Memphis, Tenn.; Columbus, Ohio, and the Inland Empire in California.

The industrial sector also saw rising rents while office rates fell. The average asking rent per square foot for the industrial market rose 6.9 percent, higher than the 5 percent increase seen prior to the pandemic. The average asking rent in the office sector was down by 0.4 percent year-over-year, compared to 2.8 percent before the pandemic. However, the NAR report states that office rents are up on a year-over-year basis in 365 of 380 metro areas.

Secondary and tertiary office markets that are seeing rent increases include Tucson, Ariz. (6.2 percent), Providence, R.I., (6 percent), Naples, Fla. (5.6 percent), Fort Myers, Fla. (5.3 percent) and Las Vegas (4.9 percent). Decreases in large markets like San Francisco (down 4.4 percent) and New York (down 2.8 percent) continue to pull down the national average rent rates.

Source: National Association of Realtors

|

|

GLOBAL CRE TREND: GREEN BUILDINGS

Buildings account for 39% of global greenhouse emissions — that could be an opportunity for investors

|

|

KEY POINTS

· Investing in sustainable buildings could offer a real solution to reducing emissions, ESG investment firm Taronga Ventures said.

· Green solutions can be found across the value chain, from design to construction and operations, Avi Naidu told CNBC.

· Buildings currently represent 39% of global greenhouse emissions, according to U.N. data.

· Investing in sustainable buildings could offer a real solution to reducing emissions in one of the world’s most polluting sectors, said Taronga Ventures, an investment firm focused on sustainable innovation and tech.

Buildings currently represent 39% of global greenhouse emissions, according to U.N. data. Almost one-third (28%) of the global total is the result of running buildings — referred to as operational emissions, while 11% comes from building materials and construction.

“It is a widely unknown fact,” Avi Naidu, co-founder and managing director of Taronga Ventures told CNBC’s “Squawk Box Asia” Friday.

“Many people think that it’s transport, it’s methane, it’s food that is a big driver, but actually it’s the built environment,” said Naidu, whose company invests in innovation within real estate and construction.

Dispelling misconceptions

That lack of awareness, however, presents a “huge opportunity” for investors, said Naidu, noting that the technology and appetite for sustainable building solutions are already there.

“There is a misconception in markets and particularly from landlords [that] it will cost more. Absolutely, as technology is first introduced it sits higher on the cost curve, [but] as it gets more widely adopted we see it go further and further down the cost curve,” he said.

“We’re also starting to see consumers and investors pay a premium for products and assets that are ESG aligned and much more sustainable,” he continued.

Environmental, social and governance — or ESG — investing has grown increasingly popular in recent years, mainly in the wake of the Covid-19 pandemic.

“So a lot of the cost is being increasingly mitigated by the ability to command greater rents, greater asset values, and that’s really how landlords should be thinking about it,” he said.

Decarbonizing the economy

Decarbonizing the economy could be a market opportunity worth up to $30 trillion within the next two decades, according to Goldman Sachs.

For its part, Taronga Ventures is investing in green building solutions “across the value chain,” said Naidu. That includes design, construction, and operations, but also the repurposing and ultimate destruction of buildings.

As we build new stock, “we have an opportunity to think about different materials, different kinds of concrete, different methodologies that make the process safer, smarter and obviously, from a carbon perspective, more efficient,” he said.

Naidu’s comments come ahead of the 26th U.N. Climate Change Conference of the Parties, known as COP26, in Glasgow in November, where world leaders will discuss efforts to combat the climate crisis.

Source: CNBC

|

|

AFFORDABLE HOUSING - POLICY

Treasury suspends investment property restrictions to boost housing supply

|

|

Rules had limited the volume of loans Fannie, Freddie could buy

Good news for second-home buyers: Certain loan restrictions at the federal level have been lifted, which will make it easier to get a mortgage for those properties.

In an effort to boost housing supply, the Treasury Department and Federal Housing Finance Agency are removing some rules that limited the number of loans that Fannie Mae and Freddie Mac could buy, HousingWire reported.

The restrictions, which were added to the Preferred Stock Purchase Agreements in January, prevented Fannie Mae from acquiring loans secured by second homes and investment properties. Lenders are more hesitant to make loans that cannot be sold to Fannie and Freddie, and loans that are off limits to the government-sponsored entities are typically more expensive for borrowers.

Under the January change, only 7 percent of the agency’s total single-family acquisitions could be from loans secured by second homes and investment properties. Other restrictions included those on higher-risk loans and small lender cash window access.

With home prices on the rise and few homes on the market, dropping these restrictions is a way to promote sustainable homeownership, the Treasury Department said in a statement.

“The administration is focused on promoting housing stability, which includes advancing housing policies that can sustainably increase the stock of affordable housing units for rent and ownership,” the statement continued.

When the restrictions were implemented, they were met with outcry from lenders and trade groups, who complained that the limits on the cash window would force lenders to send mortgage-backed securities to the private market, the publication reported. By spring, demand for those properties had risen by 84 percent over the past year, according to a report from Redfin.

The rollback was met with positive reactions from groups including the Community Home Lenders Association, which commended FHFA director Sandra Thompson for the reversal.

Source: The Real Deal

|

|

AFFORDABLE HOUSING - LEGISLATION

Chuck Schumer calls for $80B in public housing funding

|

|

Senate Majority Leader pens op-ed to double American Jobs Plan allocation

Senate Majority Leader Chuck Schumer says the $40 billion allocated by the American Jobs Plan for public housing isn’t nearly enough to address a national “humanitarian crisis” unfolding in developments in New York City.

About 400,000 people live in a NYCHA development in the city, operated by the city’s housing authority. In an op-ed for City & State, Schumer called for boosting resources for public housing residents in New York CIty and across the country by doubling the allocation in the bill to $80 billion.

“I have pledged to use all of my power as majority leader, alongside my New York colleagues in the House of Representatives, to secure a funding package that can restore and transform NYCHA,” Schumer wrote.

Schumer cited examples of various problems in NYCHA buildings, from lead exposure to children to residents lacking gas and units missing either air conditioning or heat. The senator called for fixes to all these problems, as well as more “sustainable and efficient infrastructure,” better drainage and more working elevators.

In calling for the increase in funding, Schumer cited the ballooning cost of NYCHA’s capital needs. Those needs were estimated to be about $17 billion back in 2011, but now stand in excess of $40 billion.

Schumer’s op-ed echoes a demand the New York lawmaker announced in May with Rep. Richie Torres — a former New York City Council member who chaired its Committee on Public Housing — highlighting NYCHA facilities as a key example of dire need for increased federal investment.

In addition to a lack of resources, the management of NYCHA, one of the biggest housing authorities in the country, has been criticized by local politicians. Last year, Public Advocate Jumaane Williams called out Bill de Blasio’s administration for its management of the agency, which landed the administration at the top of a list of the city’s worst landlords.

Earlier this year, NYCHA announced a plan to overhaul the agency’s management system in conjunction with federal prosecutors and the U.S. Department of Housing and Urban Development. That could still be a ways away, however, as the first part of an implementation plan is due this month and the second due in June, before implementation can actually occur.

Source: The Real Deal

|

|

LOCAL NYC - REZONING NEWS

CPC approves rezoning to turn Blood Center into life science hub

|

|

The City Planning Commission today approved by vote of 8 to 2 the New York Blood Center’s ULURP application for an applied life sciences hub called Center East on the Upper East Side that will serve as a key driver of the city’s life science innovation ecosystem and a key part of its pandemic response infrastructure.

The Blood Center’s project is one of the key re-zonings left under Mayor de Blasio’s administration. Per the city’s land use process, the City Council will now consider a project that will see the New York Blood Center is partner with Longfellow Real Estate to transform its East 67th Street headquarters into a 600,000 s/f life science campus.

Called Center East, the hub will replace NYBC’s existing facility with a state-of-the-art center anchored by NYBC, which supplies life-saving blood products and services to nearly every hospital across the five boroughs and delivers stem cell products to over 45 countries worldwide.

“This is exactly the project our city needs right now. Center East will position New York to be a life science innovation hub, create jobs, stimulate billions in economic output annually, and open career opportunities for local students and young professionals. Our vision for a state-of-the-art life science facility will not only ensure the nonprofit Blood Center continues to provide safe, affordable blood services to the region’s hospitals, but enable the center to significantly expand its life-saving research on COVID-19 and blood-related diseases in collaboration with institutions and biotechnology partners all under the same roof,” said Rob Purvis, Executive Vice President and Chief of Staff, New York Blood Center.

However, the project has seen opposition from the local community which has criticized its height and residential to commercial zoning it requires.

Among the loudest voices against the plan is Council member Kallos, who told the City Planning Commission over the summer, “The New York Blood Center has been seeking to build a tall tower for as long as I can remember, for my entire career in politics, back to when I first started in 2006 on Community Board 8, and again in 2016. At every stage, their aggressive proposals have been rejected by elected officials and the local community.”

Kallos said that the community doesn’t have a problem with expansion within current zoning, which would permit expanding the current three-story building to seven stories.

However, earlier this month, a grassroots coalition representing thousands of New Yorkers endorsed the Blood Center’s proposal. Its members—including Laborers’ Local 79; Greater New York LECET (Laborers-Employers Cooperation and Education Trust); Building & Construction Trades Council of Greater New York; Urban Upbound; Community Voices Heard, Baruch Computing and Technology Center; and The Knowledge House—all signed a letter urging local Council Member Ben Kallos and the City Council to advance the project.

Gary LaBarbera, President of the Building and Construction Trades Council, said, “The New York construction industry lost 74,000 jobs and $9.8 billion in economic activity last year during the shutdowns triggered by the pandemic. Projects like Center East are critical to the future of New York City as we look to rebound, and build back stronger than ever.

“The building and construction trade industry represents 20 percent of the city’s economy, 10 percent of jobs and 5 percent of wages. While it is disheartening to hear that the NIMBY voices are once again putting themselves and their own personal interests ahead of the greater good, it’s certainly not surprising or new. Center East will generate more than 1,500 full-time construction jobs and $1.1 billion in economic output annually. Our city needs this project now.”

Carlo Scissura, New York Building Congress President and CEO, added, “The New York Blood Center is a crucial hub for New York’s life science industry, and given the heightened need following the COVID-19 pandemic, now is the time to create a purpose-built center that will help the Blood Center’s important mission. New York City boasts industry-leading life science institutions, but we have yet to reach our full potential as one of the country’s leading life sciences hubs.”

Source: Real Estate Weekly

|

|

NEW CRE TREND: "BTR" OR BUILT-TO-RENT

How Tech is Driving the Growth of Built-to-Rent Communities

|

|

One of the first things you learn in economics is the concept of economies of scale. The principle is simple, as you make more of something, the per unit cost goes down.

In the property industry, this plays out when it comes to multifamily buildings. The larger a building gets, each of its units are able to share more services, which makes them cheaper to manage and own. Due to labor costs, the economies of scale in a building are not perfectly linear. Instead, the form is more of a stair step. A few hundred units might need only one maintenance person or leasing agent, a few more might need two. But, for the most part, the bigger the building is, the cheaper it is to run and the more shared amenities it can afford to offer.

The operating efficiencies that come with having all of your customers under one roof is what has traditionally pushed larger investment groups into the multifamily housing sector. Now, though, investors are looking at built to rent communities as a way to tap into the growing market for single-family rentals. As Brad Hunter, president and owner of Hunter Housing Economics said, “Demand for rental homes is growing faster than supply.”

Luckily, advancements in technology are helping to make built to rent communities just as efficient to manage and amenitize as their multifamily counterparts. Scalability is being noticed by large companies as landlords of single-family rentals can host premiums up to 15 percent higher than comparable multifamily projects. “Part of the appeal of multifamily buildings is the amenities that they provide and the community that they can create,” said Lucas Haldeman, CEO of smart home technology platform SmartRent. “Now, we are seeing large single-family rental communities rolling out the same kinds of amenities. They are basically a multifamily building spread out over an entire development.”

For tenants, that means that they can have the benefits of living in a house, like adjacent parking, ample storage, and a yard, while still benefiting from communal spaces like pools, gyms, and clubhouses. Booking these can be done easily thanks to mobile apps, and access can be granted via smart locks. Single-family rentals generally have less turnover than rental apartments, and the addition of these types of leisure facilities can even further increase the average length of stay.

There is also an added benefit of bringing a community of built to rent homes together: better wifi. In order for smart rentals to function, they must be equipped with their own wifi. This is the case for standalone rental homes but the advantage that rental communities have is that they are able to create a network by meshing every house’s signal. That means that if any one router stops working, devices can instantly and securely be connected to a neighbor’s signal, which avoids the dreaded signal outages that derail Zoom meetings and interrupt someone’s favorite show.

Community-wide wifi is an amenity that people care about. It doesn’t just make work or play easier, it makes communities safer and consistently connects property managers with residents.

This community wifi hub’s capabilities are not restricted to new builds. It can also be done as a retrofit to existing built to rent communities. With the trend of remote working, residents can take their work to the park or to the office-like space at the community center without having to switch to a new wifi network. “Community-wide wifi is an amenity that people care about. It doesn’t just make work or play easier, it makes communities safer and consistently connects property managers with residents,” explained Haldeman.

Connections among community homes go beyond wifi; they include integrating technologies like Ring doorbells and smart thermostats. For example, SmartRent’s integration with Ring lets users add their front door devices to their smart home app for a live view of what’s happening around their home even when they’re not nearby. “Every smart home vendor should be thinking about an “occupied” vs “vacant” mode. In vacancy mode, owners have access but once it is occupied, their abilities go away except for things like leak sensors,” stated Demetrios Barnes, COO of SmartRent. The smart thermostats allow residents to remotely activate different modes, keeping their home comfortable while saving energy and reducing costs.

The integration doesn’t reduce the capabilities of these devices, it just brings everything together in one app so residents can easily access what they need. Plus, with the community hub wifi, it is always online and accessible. One app, one community.

And, when something goes wrong, the same app that brings everything together doubles as a work order platform. “If you need to put in a maintenance request, you already know how to do it. Residents don’t need to search for where to go,” added Haldeman.

As much as smart home tech can make a community better for built to rent occupiers, it is an even bigger benefit for management and staff. Leasing is one of the most labor intensive parts of any rental building. Since many prospective tenants want to tour homes after work and on weekends, it can be difficult and expensive to staff a full-time leasing office.

Now landlords are able to effortlessly grant access to prospects thanks to one-time smart lock codes. “It’s interesting that it took the pandemic to wake up the industry to self-guided tours; we’ve been doing those since 2011 as it was necessary for us to manage homes across states,” added Barnes. Monitoring and maintaining the amenity spaces are also much easier. Smart locks record who was the last person to use any area and closed-circuit cameras allow security to monitor even a multi-acre complex from one central command center.

For vacant residencies, tech enables the built to rent community with control and monitoring without having boots on the ground. “When you send someone over to do work on a place, the first thing they do is adjust the temperature to make it comfortable. Nine times out of ten, they don’t turn it back up,” said Barnes. With remote control, spaces that are unoccupied are kept within an acceptable range of comfort even when human error is taken into account.

Technology has allowed managers of large rental communities to tap into the economies of scale much like multifamily buildings do. Earlier this year the country’s largest homebuilder, Lennar, announced its plans to both build and manage built to rent communities. This new business model will help Lennar branch out past the low margin, high risk business of building houses and tap into the stable, recurring revenue and economies of scale that come with being a landlord.

From the resident’s angle, it’s all the community aspects and perks without all of the responsibilities and downsides of home ownership. It’s not just a go-between from renting to owning; to many, these homes are the perfect mix and the absolute end goal. This can lead to high retention rates, and also a unique attraction to future residents. And it is all made possible thanks to the devices and software that are now widely available in all of our homes.

Source: Propmodo

|

|

CAPITAL MARKETS - BTR SECTOR

Capital Is Pivoting from Multifamily Into the BTR Space

|

|

The increased demand for single-family rental product is pulling players from the apartment market into the build-to-rent arena.

Build-to-rent communities are quickly becoming the most sought-after new asset class. According to Noam Franklin, a founder of Berkadia’s JV Equity & Structured Capital group, investment capital is pivoting from multifamily to build-to-rent investments in response to surging demand.

“Capital sources such as private equity funds have recognized the increased demand for rental product across the country and are pivoting dollars away from other asset classes in real estate and doubling down on the residential space,” Franklin tells GlobeSt.com. “While traditional multifamily remains attractive to these investors, our team has noticed a significant increase in interest in purpose-built build-to-rent single-family product since early 2020.”

A recent deal with Capstone Communities is among the most recent examples. Franklin, along with Chinmay Bhatt and Cody Kirkpatrick, secured a programmatic capital partner for Capstone Communities’ BTR pipeline. The team sourced $37 million of equity for the first two projects in Port St. Lucie and Myrtle Beach. The deal is one of many that the team has worked on in the last year. “To give you a sense of that demand, our team has capitalized over $500 million of opportunities within the BTR space – most of it programmatic in nature—over the past 12 months. We also have a robust pipeline of deals slated to close in the next quarter,” says Franklin.

Capital is responding to the sudden increase of demand for BTR product, a trend that has been bubbling for years but was accelerated by the pandemic. “The surge of interest in BTR is the result of a convergence of demand drivers. COVID-19, of course, had a profound impact in terms of fostering people’s desire for more space and creating the possibility of being able to work from anywhere,” says Franklin, adding that the residential rental sector has myriad benefits. “Other factors include the fact that BTR product appeals to families who want a single-family home type experience with on-site amenities; pet parents who want private outdoor space for their pets; and empty nesters seeking the conveniences of greater mobility and no down payment,” he says.

Franklin is also seeing the move to BTR investment all over. Franklin explains, “Even among our own friends and peers, we’ve seen an increase in the “renter by choice” tenant who wants all the benefits associated with single-family home living without the responsibilities.”

Source: Globe St.

|

|

OFFICE POLL: COVID ERA

5 Findings From New Study About the Value of the Office

|

|

One of the biggest remote work studies ever conducted recently released findings that show the office isn’t going anywhere.

The study, conducted by UC Berkley scientists, looks at over 61,000 Microsoft employees. Microsoft’s rapid shift to a work-from-model presented a unique opportunity for researchers, a natural experiment that can help shed light on the value of company-wide remote work policies. What the researchers found was that remote workers engage in fewer real-time conversations, work more siloed, and spend less time in meetings.

The study, published Sept. 9 in the journal Nature Human Behaviour and co-authored by Berkeley Haas Asst. Professor David Holtz, builds on assumptions around previous research showing the value of networks and personal connections for organizations. It also has positive effects for the individuals in the organization. Being connected to different parts of organizations through personal connections outside of a team provides new information that individuals can leverage to fill structural holes in the organization. ‘Knowledge transfer,’ whereby information and experiences from one team are passed to another, is critical to high-quality output and culture. The efficacy of that type of transfer and the benefits of networks to an organization depends on the strength of the ties between individuals, that’s where the value of the office is anchored.

“Measuring the causal effects of remote work has historically been difficult because only certain types of workers were allowed to work away from the office,” said Holtz, who conducted the research as an MIT Sloan doctoral intern at Microsoft, and co-wrote the paper with Microsoft colleagues Longqi Yang, Sonia Jaffe, Siddharth Suri, and seven others. “That changed during the pandemic, when almost everyone who could work from home was required to do so. The work-from-home mandate created a unique opportunity to identify the effects of company-wide remote work on how information workers communicate and collaborate.”

Here are some of the most shocking findings of the study:

1. Remote workers spend about 25 percent less of their time collaborating with colleagues across groups

The study found firm-wide remote work policies caused Microsoft teams to become less interconnected, reducing the number of informal bridges and ties filling structural holes in the company’s collaborative process. Employees spend less time building bridges and ties, and less time collaborating with what connections remain. Less time collaborating across teams slows down critical knowledge transfer necessary for innovation and synergy.

2. Company-wide remote work caused workers’ collaboration networks to become less interconnected and more siloed

Interestingly, with fewer ties to maintain outside of their teams, individuals lean more heavily on their stronger ties within the team. This had the positive benefit of creating more dense connections between teams, but the negative externality of more siloed work. Without in-person interactions networks become more static, with fewer members being added or removed. Changes in collaboration patterns like those detailed in the study impede knowledge transfer and reduce the quality of employee output.

3. Remote work led workers to communicate more frequently with people in their inner network, less frequently with those outside of it

Remote workers spend more time collaborating with stronger ties, and less time with weak ties, which provide novel information. Those changes make it more difficult for workers to capture the benefits of forming new bridges, reconnect with previous connections, or change their own status within a network.

4. Remote work caused workers to spend more time using asynchronous forms of communication

Remote connections like Zooms meetings, phone calls, and Slack messages aren’t necessarily replacing in-person interaction, it may be eliminating some of it altogether. Often synchronous communication, like in-person conversation and phone calls, are being replaced by asynchronous communications, like email and IMs. This affords more flexibility for the communicators but makes it more difficult to convey complex information.

5. Remote work also caused the number of hours people spent in meetings to decrease by about 5 percent

The initial rush to work from home policies at the start of the pandemic caused a spike in meetings as teams attempted to overcome the lack of in-person interaction with more numerous formal meetings. Since then, the number of overall meetings has declined significantly, now below pre-pandemic levels. The decrease in synchronous scheduled meetings is related to the increased prevalence of asynchronous communication.

What it all means

“The fact that your colleagues’ remote work status affects your own work habits has major implications for companies that are considering hybrid or mixed-mode work policies,” Holtz said. “It’s important to be thoughtful about how these policies are implemented.”

The study is not necessarily an endorsement of the office or an indictment of remote work. The pro-office team looking for definitive evidence that going into work is better should keep looking, but in the same vein, the anti-office crowd must accept that remote work does come with some negative consequences. The key is studying both remote work and in-office work as viable options, delineating the advantages and disadvantages of each so managers can make the best decision for their teams on an individual level, rather than through a company-wide mandate. Valuing bridges, ties, connections, and collaboration to a company’s bottom line is notoriously difficult.

What is missing from the study is weighing changes in work against Microsoft’s performance. If remote work is holding back Microsoft, you would hardly know it. The company’s stock price is approaching record territory after the tech firm revealed its quarterly net income was up 47 percent annually. The success has set Microsoft up to raise its quarterly dividend by 6 cents and announce a plan to buy back $60 billion in stock. Microsoft’s financial future is clearly not strongly tied to its workflow policies. Microsoft’s 365 and Teams platform have allowed the company to profit handsomely off the massive shift to remote work. The company is now sitting on nearly $130 billion in cash.

Clearly, there’s still much about remote work and the value of offices we don’t fully understand. People are complicated, groups of people even more so. The study of Microsoft’s 61,000 employees moves our understanding of the value of the office forward but is far from conclusive. Many teams take the office for granted, tied to the status quo. Research like the Microsoft study provides a real basis for defending in-person work rather than just being adverse to change. Before any conclusive evidence can be produced, a return to normal to establish a baseline will be required. Maintaining control groups and assumptions is nearly impossible during a global pandemic. We are getting close to understanding the effect of remote work but every answer seems to bring up even more questions about one of the biggest changes to the American workforce in decades.

Source: Propmodo

|

|

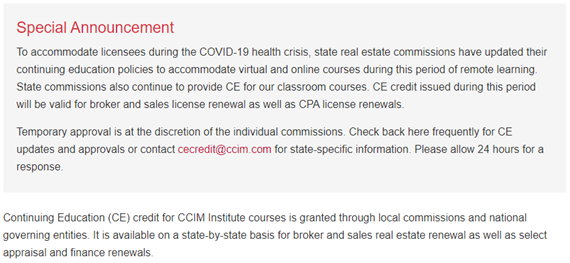

CCIM Continuing Education |

|

(Sample of courses only; go to CCIM’s website for more offerings!) |

|

2021 NEW YORK METRO CCIM CHAPTER

LEADERSHIP

|

|

President- JR Chantengco, MBA CCIM, Black Pearl Investments

|

|

Vice President- Tom Attivissimmo, CCIM, Greiner-Maltz of Long Island LLC

|

|

Treasurer- Robin Humble, CCIM, Nelson & Nielson

|

|

Assistant Treasurer- Matt Annibale, CCIM, First National Realty Partners

|

|

Secretary- Samuel Weiner, Langdon Title

|

|

Director - Ian Grusd, SIOR CCIM, Ten-X

|

|

Director - Al Holloman, CCIM, RMFriedland

|

|

Director - Chris Cervelli, CCIM, Cervelli Real Estate

|

|

Director - Camille Renshaw, CCIM, B+E

|

|

Director - Scott Perkins, SIOR CCIM MCR MRICS, NAI James E. Hanson

|

|

Director - Lee Barnes, CCIM, Woodman Group LLC

|

|

Director - Brian Whitmer, CCIM, Cushman & Wakefield

|

|

Institutional Real Estate

Northern New Jersey

Mixer

Social Media

Newsletter

Virtual DealShare

|

|

Copyright © 2021 NY Metro CCIM Chapter of the CCIM Institute, All rights reserved.

You are receiving this email as a current or past Member of the CCIM Institute or through the local chapter in proximity to your primary place of business.

NY Metro CCIM Chapter of the CCIM Institute

|

|

|

|

|

|

|