Early last year, as SPACs began their rise in popularity, the WSJ reported of those that IPO’ed in 2015 and 2016, over 50% “were trading below their IPO price.” Performance of SPACs in the 2010-2017 period, the analysis showed, was 3% worse than the overall market, measured annually for the first three years after the IPO.

In the article, a University of Florida finance professor was quoted as saying “I’ve been surprised by the staying power of SPACs, given that they haven’t been producing big returns for investors.”

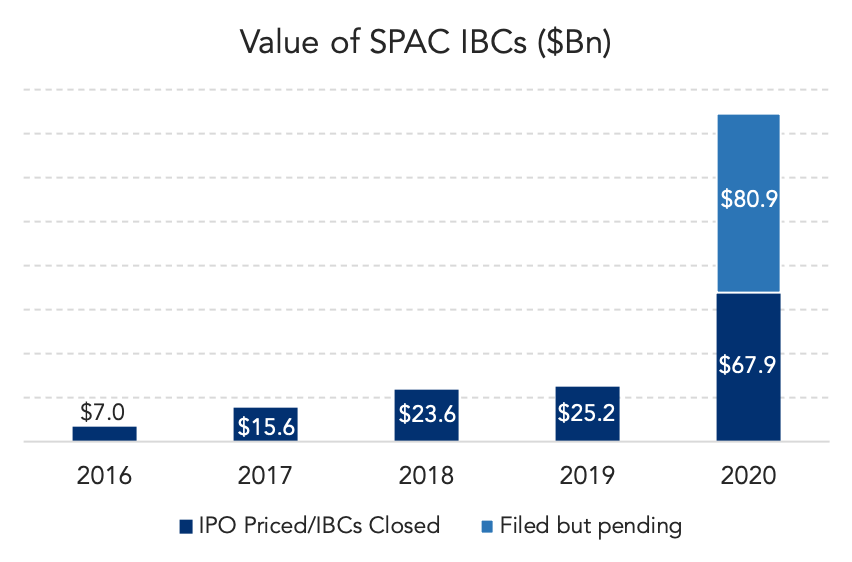

According to Renaissance Capital, an IPO research specialist, of the 200-plus SPACs launched during the last five years, 107 have completed mergers and gone public...

✒︎ From the Editor: The Lead Left will be on break until January 4th. To all of our readers, best wishes for a safe, healthy and restful holiday season.