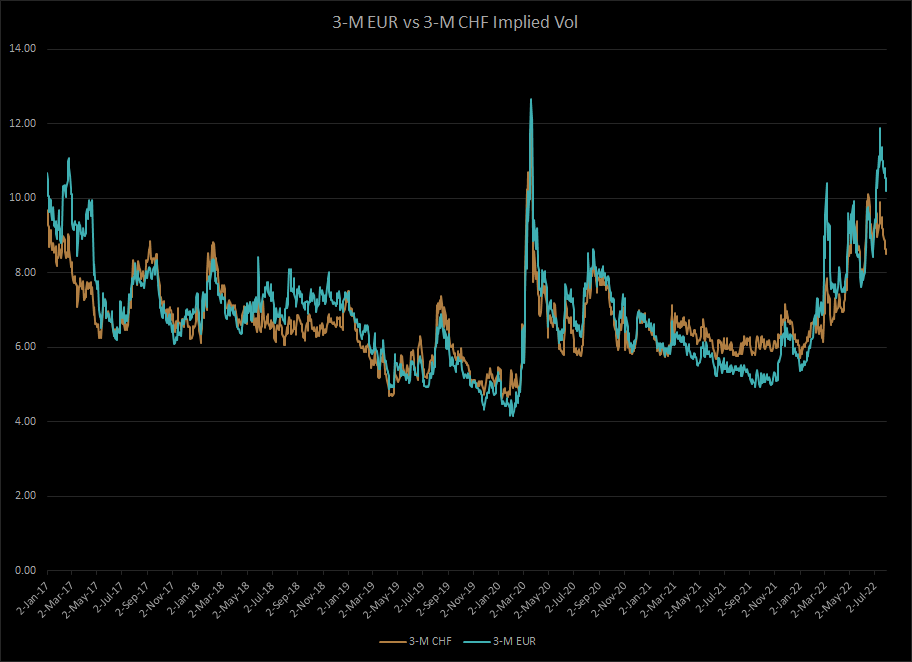

The chart above is 3-month CHF vol less 3-month EUR implied vol. A bit more than half the time the spread from 2017 has been negative with CHF trading at a discount to the EUR. As you can see the current spread is close to the previous cyclical low. One obvious trade would be to short EUR vol and buy CHF vol which in our view is really largely a bet that EURCHF has come down too far. But it also may not be a bad trade to consider just owning CHF vol on its own, but not in the form of strangles but rather in the form of straddles, taking on less of a break-out view and more of a gamma trading view. Given the discount, this trade makes more sense but it would be re-balanced more actively or until a clear range break has occurred.