“I am seeing a lot of FOMU – fear of massively underperforming.”

– John McClain, portfolio manager, Diamond Hill Capital Management.

|

|

The New Healthcare (Second of a Series)

|

|

We continue our special series on how the coronavirus is affecting the healthcare industry. At the heart of this pandemic is the doctor/patient relationship.

Much has been written about heroic efforts by first-responders in the early days of the crisis. Information gleaned on the front-line by those experiences has contributed greatly to a better understanding of how this virus spreads. The importance of washing hands, wearing masks and social distancing has only been solidified as a result.

We spoke recently to our own primary physician in a Zoom interview about his experience in a COVID-19 world.

“Thank goodness for telemedicine,” he told us, speaking from his home. “I can be very effective each day and have meaningful discussions with my patients. A lot of these now involve testing for the virus antibodies, which is easy and quick. You can get the results next day. And our staff can do all the blood work for general physicals.”

How will this pandemic change patient behavior, and your practice? “I think patients are acutely aware now of how these viruses spread,” he said, “and how to protect themselves from infection. We’re still a ways from a vaccine. Even then, there’s a lot of uncertainty. What’s clear is that we’re in for a long haul with this virus.”

Even before COVID, telemedicine was an already emerging dimension of healthcare. “There’s been real innovation in the space,” one healthcare lender told us. “In home healthcare, if a patient has a medical episode, the facility can automatically wheel up a device that takes the patient’s vitals. The doctor instantly sees the data and can address with medication. Remote medicine will certainly change and improve.”

It needs to, according to one top healthcare M&A partner. “The state of telehealth is just ok. It needs to go through another evaluation and evolution. It needs to change from just a reactive substitute for COVID, to something that’s better.

“There’s so much we don’t know,” he continued. “Prescriptions for antibiotics are higher for virtual than office visits. Why? To guard against bad on-line patient reviews? We don’t know. Just like teachers had to adapt this spring to distance learning, doctors have to modify the way they operate. Training needs to start in medical school.”

How will the doctor/patient relationship evolve? “It’s the same batch-processing of treatment and individuals that’s always been there. It’s very inefficient. You used to sit in the waiting room. Now you sit in your car. The old models don’t work in this environment. We need some residual barriers in place.

“Social distancing may be with us for good. Think about how travel changed after 9/11. We had to accept screening and security precautions. There needs to be the same massive shift in infrastructure and healthcare delivery systems. Telemedicine is just the 21st century version of housecalls. It’ll take time, but the paradigm has to change.”

|

|

To make myself more productive working from home, I …

|

|

|

(*All responses are confidential.)

|

|

Create an efficient home office

|

|

|

|

|

Stay in touch with my colleagues

|

|

|

|

|

|

|

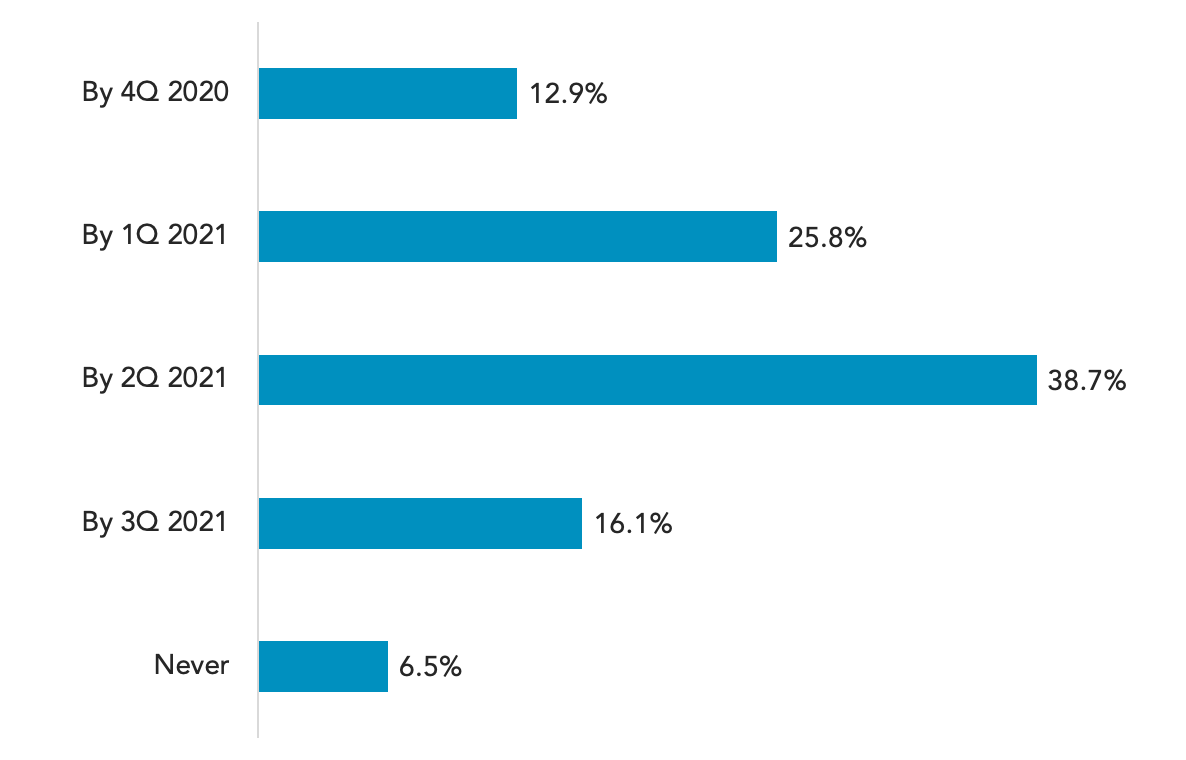

A vaccine for COVID-19 will be produced:

|

|

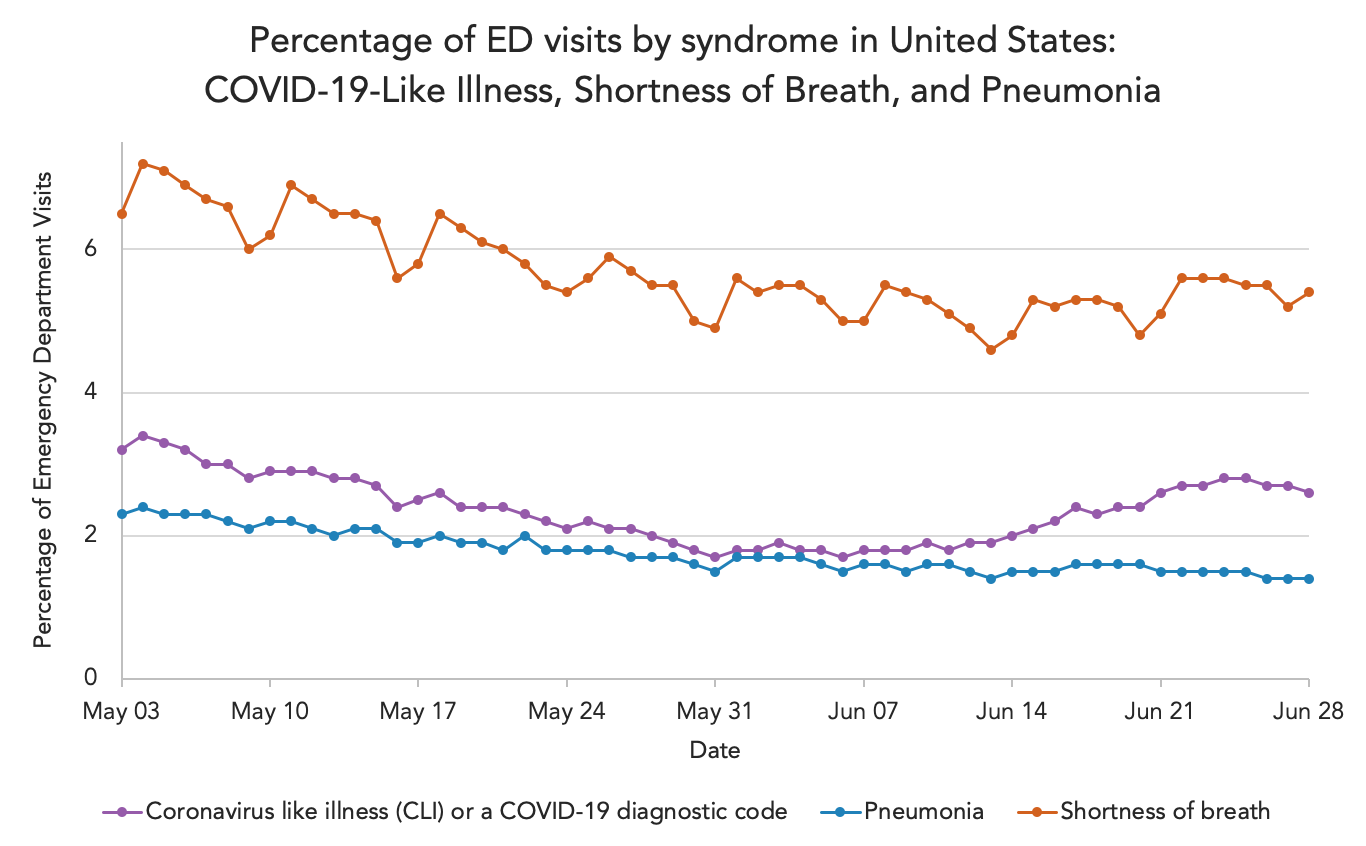

COVID-related emergency room visits are rising after bottoming out a month ago.

|

|

|

|

30-DAY FREE MEMBERSHIP

Join the leading voice of the middle market. Try us free for 30 days.

|

|

|

Something old, something new

|

|

A survey finds alternative asset firms embracing remote ways of working, but still seeing a future for office life.

|

|

The “new normal” is increasingly of a remote nature, whether you like it or not. In a recent cover story in

Private Debt Investor

, we examined the new generation of dislocation funds and questioned whether their short fundraising timeframes – which demand investors make quick decisions – really sat well with the difficulty of conducting deep due diligence in a world where face-to-face meetings are difficult or even impossible. It used to be that personal element – seeing the whites of the eyes – that was described as the key determinant for many investors.

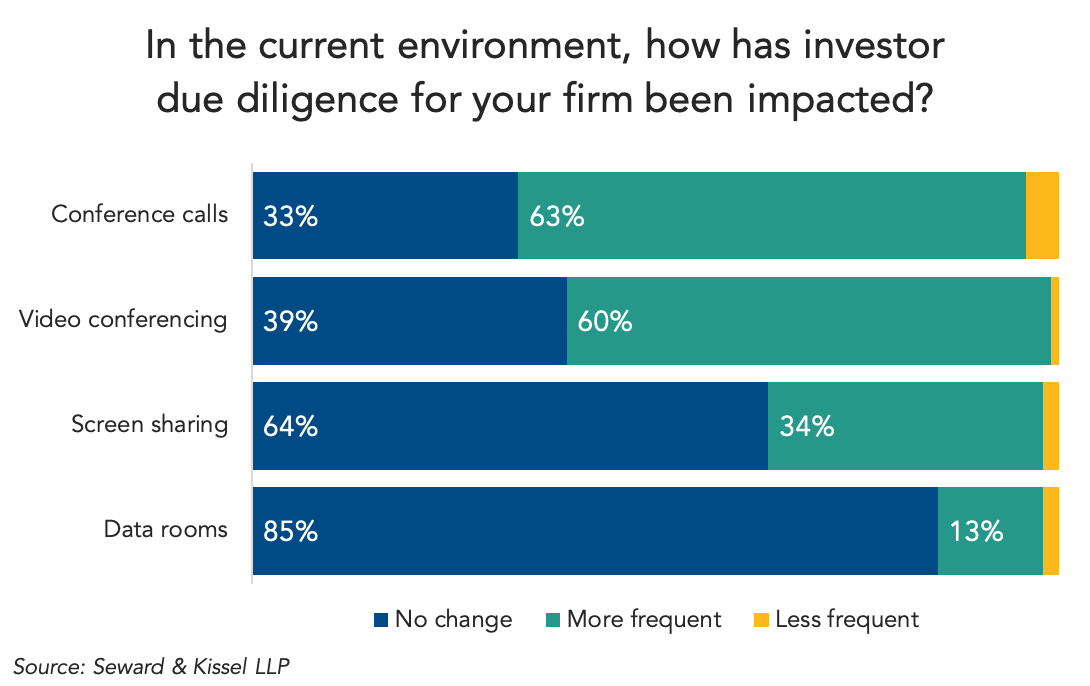

But it may be futile trying to hold back the tide, with the world is changing in ways that are perhaps irreversible as a result of the changes wrought by the global pandemic. A recent survey from law firm Seward & Kissel of US-based alternative asset firms found that, when it came to investor due diligence, 63 percent were making greater use of conference calls, 60 percent video conferencing and 34 percent screen sharing (see chart above).

The survey underlines that the remote working phenomenon has become more

|

|

widely accepted, with 40 percent of respondents saying their firm is likely to consider hiring remote operations, accounting or IT personnel; and 34 percent saying their firm was likely to consider hiring remote investment professionals. The expectation of remote hiring was more common for firms based in New York, where the pandemic bit particularly hard, than elsewhere in the US.

In some ways, however, it may come as a surprise how much of the “old normal” is seeking to re-establish itself. They may be more open to remote hiring but – counterintuitively perhaps – New York firms are also the most optimistic in terms of getting staff back into their offices. Some 90 percent of New York-based respondents said they anticipated that at least 50 percent of employees would be back in the office by the end of this year (compared with 75 percent of respondents based elsewhere).

Moreover, some things never change: only 10 percent of firms said they had offered concessions to investors on fees, liquidity or reporting terms during the pandemic.

|

|

Refinitiv LPC’s Quarterly Lender Survey:

One fifth of lenders have not heard any plans to return to the office

|

|

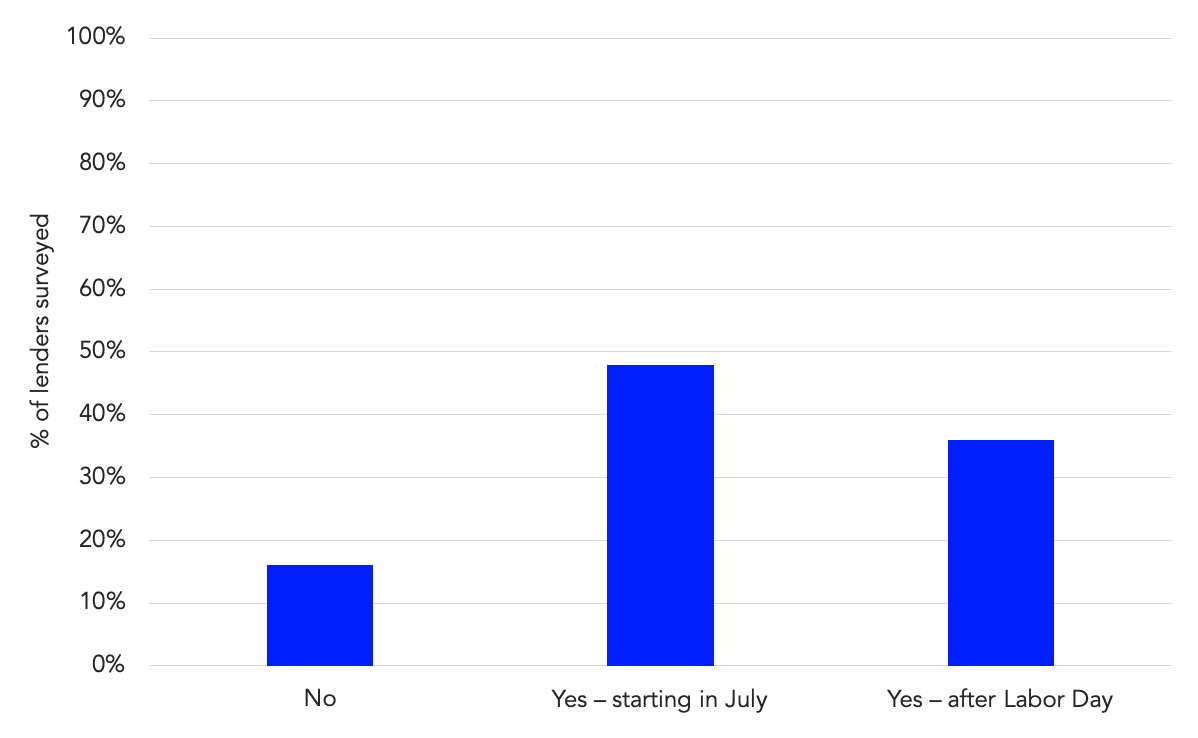

When asked if plans are being announced for segmented re-opening of your office, 16% of lenders said no while 36% reported that plans had been announced to start after Labor Day. “We were given a questionnaire internally in cities across our footprint asking for feedback on how comfortable would you be going back to work and what types of concerns are on your minds,” commented one lender. Another added, “our institution has taken a serious view to assessing comfort levels and how productive we are and how comfortable we are working in this setting. We have not gotten an outside date because there is public transportation and overall safety of moving around in this

|

|

area (midown Manhattan),” echoed another. However, nearly half of large corporate buyside and sellside lenders surveyed between June 18th and June 28th said there are plans to return some personnel representing a small share of total capacity in July. “We are hearing you’ll get advance notice and it will be optional as no one wants to force people back. Phase one started middle of June, but we still have 95% of staff working remotely which hasn’t impacted our ability to transact. There are people that can’t wait to come back into the office but also a lot of us got settled in. We have hunkered down at home and are expecting this to drag out for a while,” said a third sellside lender.

|

|

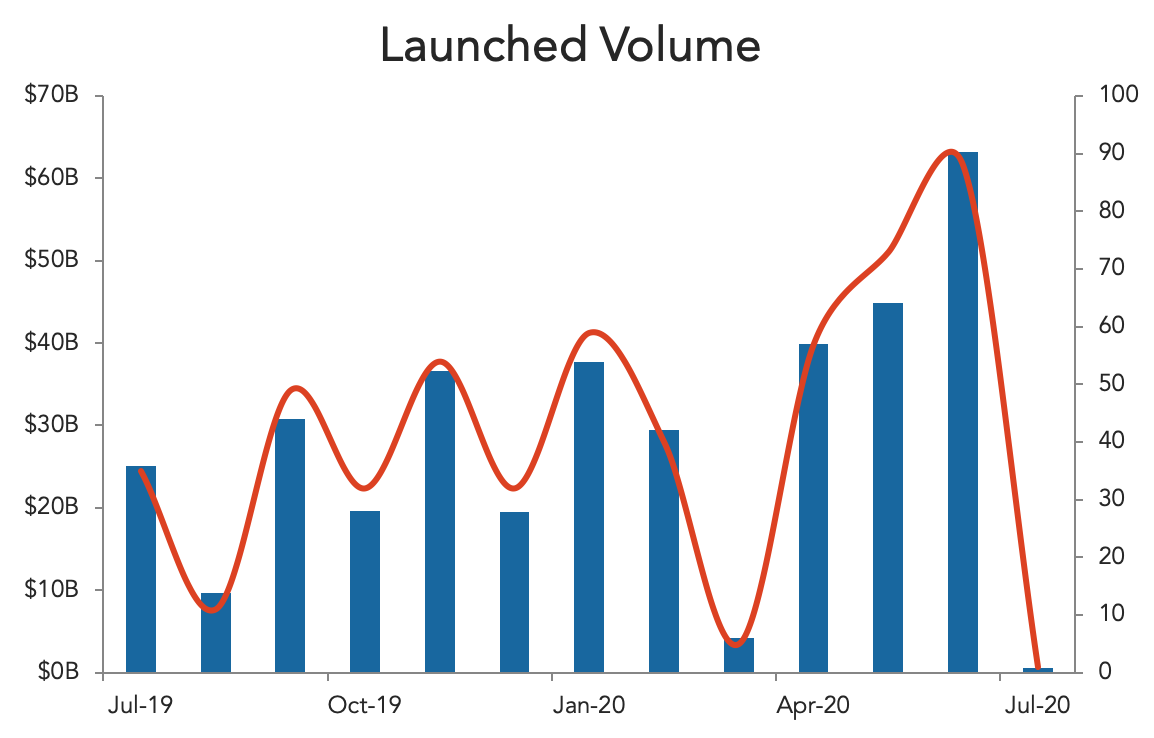

Fundraising sped up in Q1

|

|

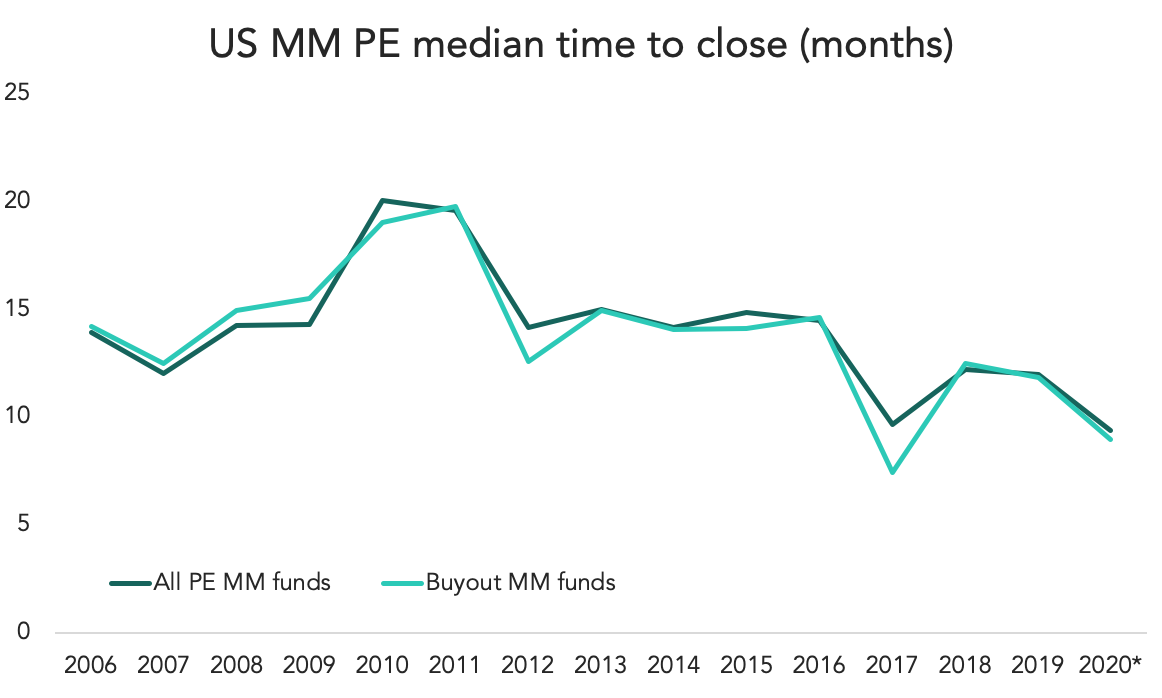

Somewhat expected, we found a quirk in Q1 fundraising data that should reverse soon. Funds that closed in the first three months of 2020 were wrapped up relatively quickly compared to 2019, according to PitchBook’s latest US Middle Market Report. As a whole, middle market funds that closed in Q1 took only 9.4 months to do so, which was visibly faster than the 12.0 months it took similar funds to close in 2019. It continued a downward trend that dates back to 2010, when it took upwards of 20 months to close the typical MM fund.

The quirk is partially explained by the pandemic and stay-at-home orders. By the end of February and into March, it was becoming apparent the world was looking at a substantial healthcare crisis and potential economic fallout. Quarantines began in mid-March, putting a crimp in fundraising logistics, among other things. If they hadn’t closed their funds already, investors were under sudden pressure to do so. Travel restrictions were being put in

|

|

place in California, New York and other states that made it impossible to meet with LPs and do in-person due diligence. For many investors, if they were close enough to their targets or were trying to eek out a few more commitments before wrapping up, their window to do so was rapidly closing.

From this point forward, we suspect the time-to-close metric will go up from here. Q2 statistics will more fully reflect those stay-at-home orders, and will partially reflect the hesitation LPs were having in committing to new funds in a wildly uncertain environment. The bigger question is how much that metric will rise in the year or two ahead. It took a median of 14.3 months to close for 2009 vintages; 2010 vintages took 20.1 months to close, a slowdown that extended to 2011 vintages, as well. It wasn’t until 2012 that fundraising speed reverted to their historical norms, despite the deal flow opportunity for PE following the crash.

|

|

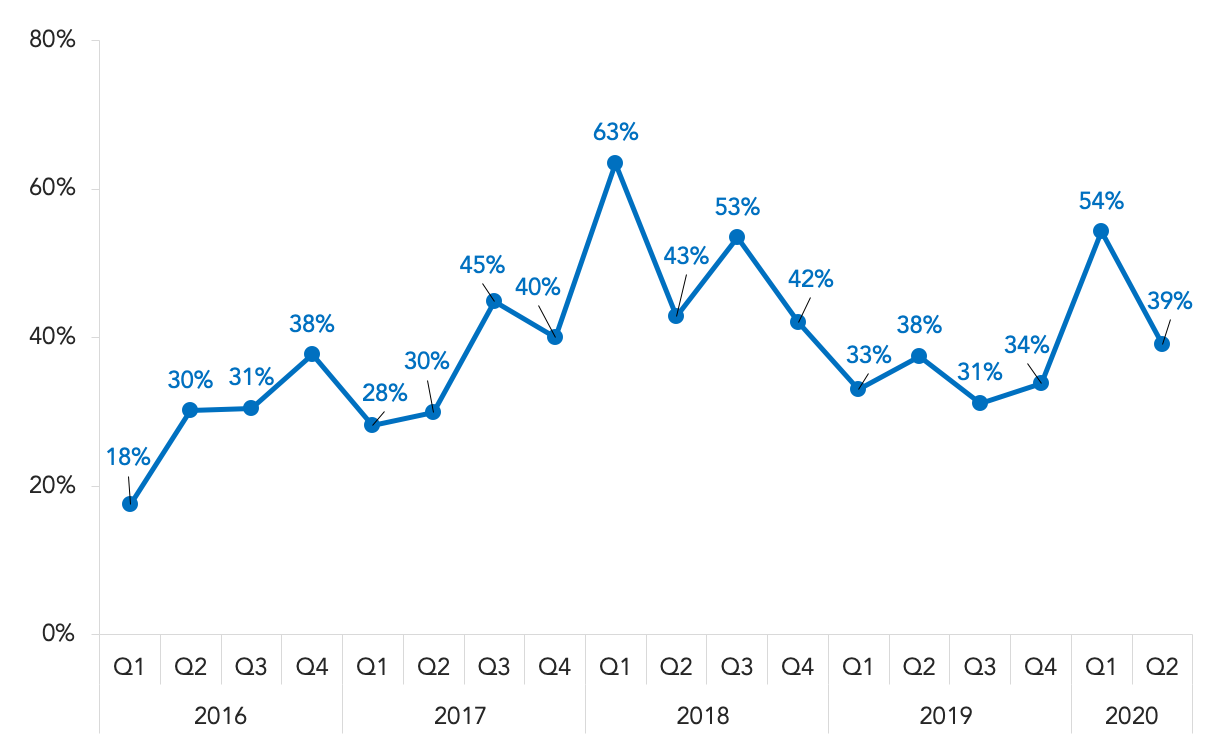

Percentage of Loans with Uncapped Synergies &

Cost Savings EBITDA Addbacks

|

|

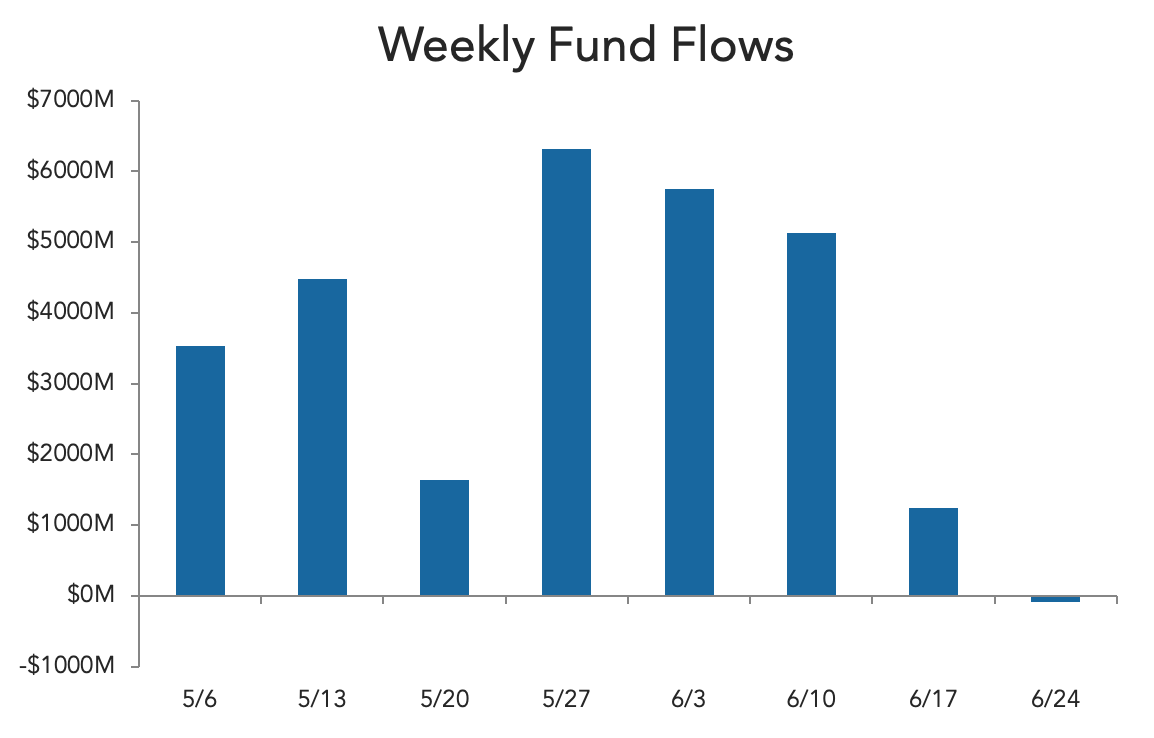

Weekly fund flows source:

Lipper

|

|

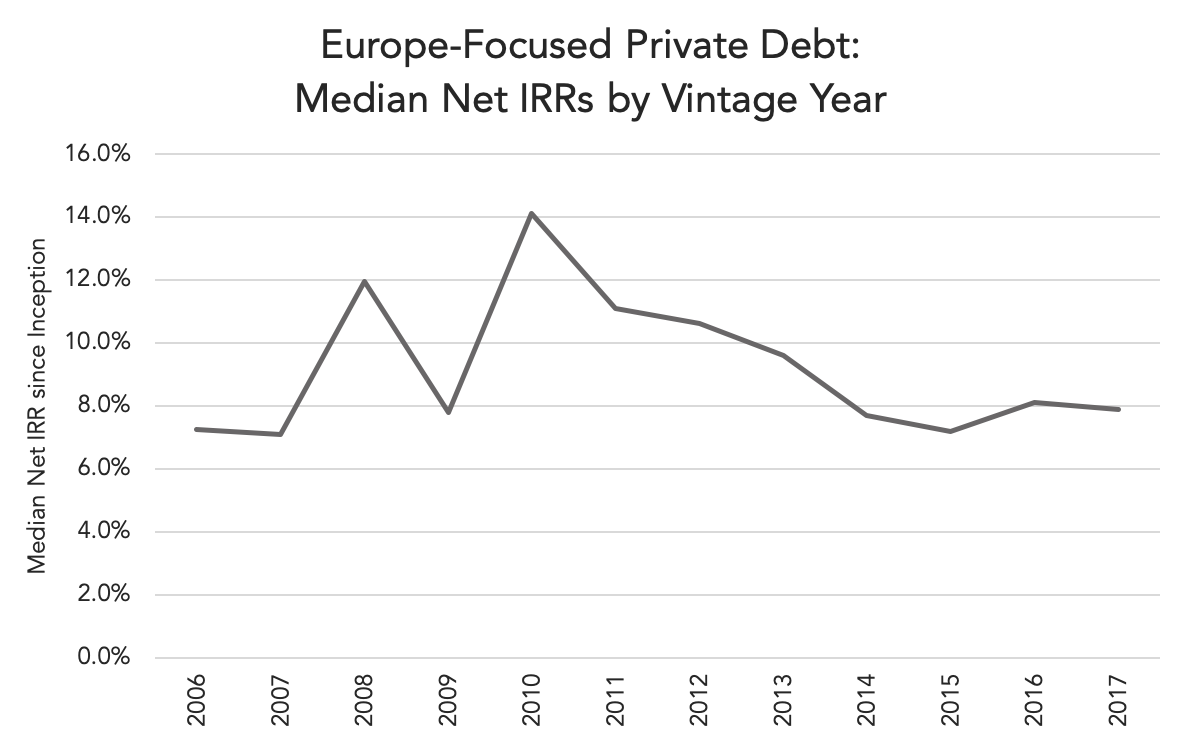

Crisis-vintage Funds Outperform in Europe

|

|

European private debt is facing its first major test due to COVID-19. In the middle of a new crisis it’s inevitable to look back and see how it might evolve in future. The private debt industry in Europe emerged following the 2008-2009 Global Financial Crisis (GFC) and funds with vintages from this time-period have now given the answer to the performance of the industry in a crisis-era.

On a median net IRR basis, Europe-focused

|

|

funds from crisis-era vintages tend to outperform other vintages, specifically two vintage years – 2008, when the GFC was ongoing, and 2010, a year after the crisis ended. Vintage 2008 funds recorded a median net IRR of 12% and, vintage 2010 funds had higher median net IRR of 14.1%. But also, worth mentioning that 2009 vintage funds’ performance registered a 7.8% net IRR, a significant down tick in comparison with the previous and later year.

|

|

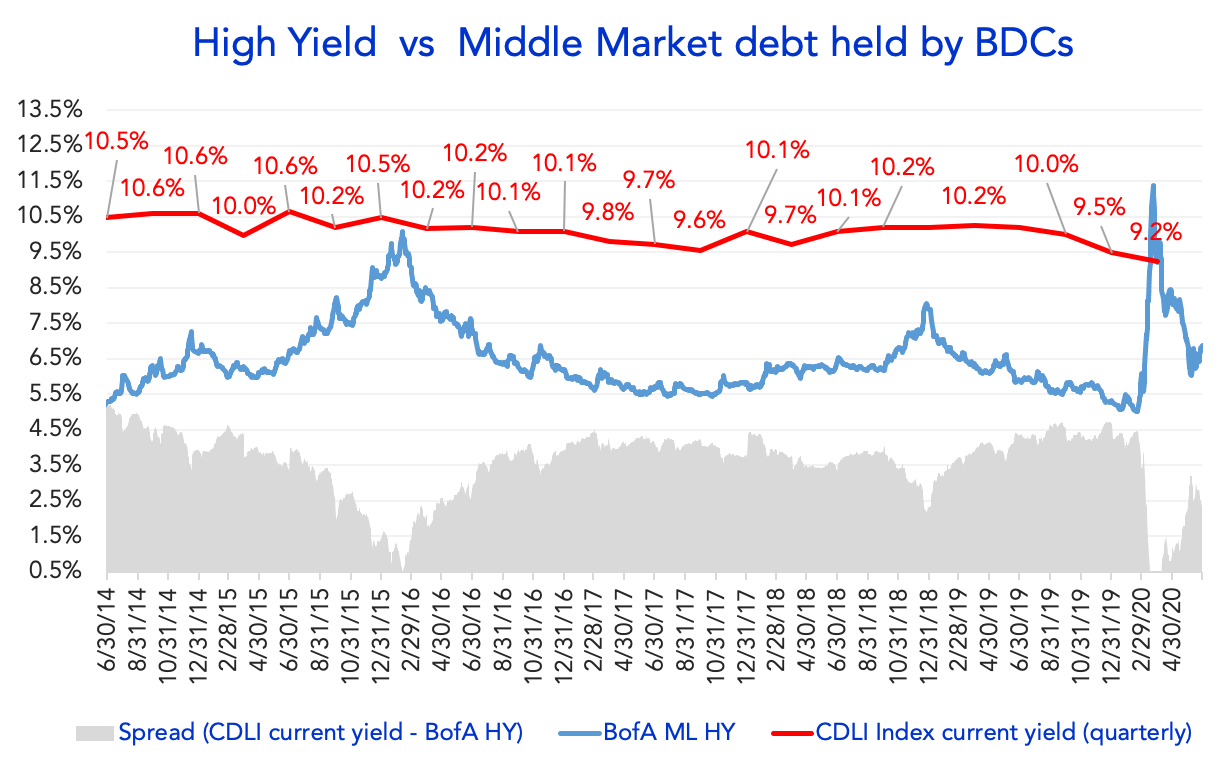

The red line in the chart is the *Cliffwater Direct Lending Index (CDLI) current yield, which is based on the investment income of the underlying assets held by public and private BDCs. BDCs invest in middle market companies, and the Index comprises of more than 6000 middle market loans – with 61% senior debt, 26% subordinate debt and 8% equity. The blue line displays the BofA Merrill Lynch US High Yield, which tracks the performance of USD denominated below investment grade corporate debt publically issued in the US. Increase in high yield depicts dislocations in market, pricing in higher risk. The spread of CDLI current yield minus BofA ML HY (shaded area in grey) shows the premium of middle-market loans over traditional High Yield, gauging attractiveness of the asset class. The higher premium for middle-market, to some extent, depicts the illiquidity for private loans and credit risk associated with smaller companies. After stabilized in 2018 and 2019, it surges steadily in the beginning of 2020 and remains at

236-basis points differential, as of 29 June 2020.

* As of 31 March 2020,

the CDLI index

includes USD 113.5bn in assets, with more than 6000 loans – approximately 71.4% senior debt, 17.3% subordinate debt, 6.8% equity and 4.5% other. BDC eligibility to be included in the Index is at least 75% of total assets represented by direct loans as of the Index valuation date. All the yields are unlevered. CDLI Index yield is total interest income of all BDCs covered, divided by their total assets, reported quarterly (9.24% as of 31 March 2020).

CDLI

data is quarterly while

BofA Merrill Lynch HY Effective Yield

is daily.

|

|

This publication is a service to our clients and friends. It is designed only to give general information on the market developments actually covered. It is not intended to be a comprehensive summary of recent developments or to suggest parameters for any prospective financing opportunity.

|

|

|

|

|

|

|