RETIREMENT SECURITY MATTERS

A forum for retirement innovation information sharing focused on

states, supporters, and service providers.

Vol 25 | February 25, 2021

|

|

Greetings! welcome! to Retirement Security Matters – where we talk about retirement readiness innovation by states, supporters, and service providers.

|

You, my friend, are making it through the wintry month of February. #Welldone! We have some distractions for you today. Enjoy away!

What’s on deck today? We think you’ll like these:

-

Treasurer Michael Frerichs talks Illinois Secure Choice

-

State programs serve more than 275,000 savers

-

Fresh news from Oregon, Colorado, Vermont, Connecticut, Illinois, Virginia and Idaho

-

Grant Sez: Let’s consider the Employer Mandate

-

Super Hot Sauce … new research from NBER and NIRS

-

And, you got it, Pix of the Week!

|

|

Illinois Secure Choice: Two Years Young

|

|

Treasurer Michael Frerichs,

State of Illinois

|

|

Mike Frerichs took office as Illinois State Treasurer in 2015 after a distinguished early career that includes study in the US and Taiwan, and roles as a state senator and county auditor. He first ran for public office just three years after graduation. As Treasurer, Frerichs has focused on getting money back into the hands of people to whom it belongs – by securing uncashed rebate checks and unpaid policyholder death benefits, and through the state’s unclaimed property program, I-Cash. He’s also helping Illinoisans get access to retirement savings opportunities at work through the groundbreaking Illinois Secure Choice program. Illinois Secure Choice opened up on a statewide basis in 2018. Join us as we talk about those exciting first two years. |

|

Treasurer Michael Frerichs, welcome! You've been an early leader in the retirement security space. Why is this so important to you?

I think we can all relate to the idea that financial worries cause stress and uncertainty. I know I feel great stress when I'm financially uncertain.

Secure Choice won't solve everything, but it gives people a chance to start saving for their future. It's easy for workers, and it's easy for employers. That's how government should work. For me, it's important to support something that can help relieve some of the anxiety that comes from financial insecurity and financial uncertainty. I think that's a no-brainer.

I was very excited that I got to support this legislation as a state Senator and then had opportunity to implement it as Treasurer -- and at the time, I thought that was unique. But then apparently there’s this guy from Oregon – we’re looking at your Treasurer Tobias Read -- who actually sponsored the legislation and then implemented the program, so I guess I’m in good company.

#welldone. Illinois Secure Choice is now two years young. What sort of impact are you seeing?

I'll start first with some numbers. In just a little over two years, we have roughly 82,000 savers who've put away approximately $50 million toward their retirement. We have over 6,000 registered employers based in every county in the state, and that number continues to grow. My team sees these employer and saver numbers, and they’re very encouraged. We've been told by some employers that, and this makes me very happy, “this is the best state program they've ever been a part of,” which means we're doing our job right.

We hear it from Illinois workers too. There’s a family-owned salon in central Illinois, not far from where I live and grew up. A worker there told us he didn't think that he would ever have access to a retirement plan … (Do not miss what happens next! - click, bookmark, read on here. )

We love it. Thank you so much Treasurer! We really appreciate the chance to talk to you.

If you’d like to connect directly with Treasurer Michael Frerichs, you can reach him here. You can connect with Illinois Secure Choice here and follow the Treasurer’s work and adventures here.

|

|

State Program Metrics - Auto IRAs |

|

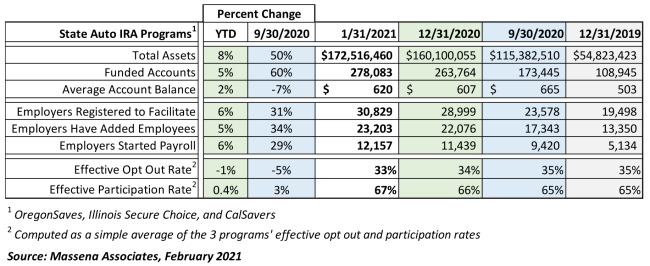

What’s interesting here – January figures are in and they show that funded accounts are up 60% over the last four months – to more than 278,000. Assets have grown by 8% in 2021 and 50% since September 30. Average account balances are rising, to $620. OregonSaves, the longest-running program, confirmed this week that its average account balance is now over $1,000. Auto-escalation took effect in Oregon and California this month for savers who’ve been in the programs six months or more. Both states saw nice boosts in their average deferral rates. California’s rate rose from 5% to 5.1%, and Oregon’s climbed from 5.3% to 5.6%.

Despite the pandemic, employers and savers are hanging in there. In January, employer registration and facilitation rates went up by 6% across the three programs. California’s rate of increase is the highest, at 15%; Oregon’s rise was 5% and Illinois’ was also positive with a 2% increase year to date.

|

|

State Facilitated Retirement Programs in Rollout and Study Mode |

|

Oregon (workforce 1.9 million) – The OregonSaves Board met Tuesday, February 23 - agenda here. Sabra Purifoy, Operations Director for the Oregon Treasury Savings Network, gave an update on the plan to ensure a smooth transition of program administration and recordkeeping services from Ascensus to Sumday (Bank of New York Mellon). This will be the first time a state-facilitated Auto IRA program has undertaken such a transition. Questions about the extent to which a necessary blackout period might disrupt employer registration served to highlight the importance of communicating with employers and participants through the transition.

The meeting also included a brief presentation on OregonSaves’ recent audit, an update on program administration and implementation, and an investment performance report and market overview from Ryan Harvey of Sellwood Consulting.

|

|

Colorado (workforce 2.4 million) – The Colorado Secure Savings Program Board met February 22 to further its work on planned program and investment consulting RFPs.

|

|

Vermont (workforce 0.3 million) – The Green Mountain Secure Retirement Plan Board also met on February 22. Vermont is working with TAG Resources to launch its MEP plan later this year and has begun deliberating key characteristics such as plan types, default contribution levels, and more.

|

|

Connecticut (workforce 1.6 million) – the Connecticut Retirement Security Authority met on February 19. Its work included a review of program-related legislative proposals for the 2021 session, and to finalize its program administration agreement with BNY Mellon. Stay tuned for an announcement shortly.

|

|

Illinois (workforce 5.7 million) – The Illinois Secure Choice Board held its regular meeting on February 18. The agenda included program and legislative updates, a presentation on the environmental landscape by AKF Consulting and a 2020 Market Review and 2021 Outlook by Marquette Associates. Illinois shared intramonth program figures. The program now serves 83,234 funded accounts, supported by 6,098 facilitating employers. Assets have just crossed the $50 million mark.

The program has proposed legislation for the 2021 session. If passed as proposed, this bill: Amends the Illinois Secure Choice Savings Program Act. Provides that the Act applies to employers with at least one employee, rather than fewer than 25 employees. Provides for automatic increases in contributions. Makes changes regarding penalties for employers who fail, without reasonable cause, to enroll an employee in the Program. Provides that, for purposes of the penalties, the Department of Revenue shall determine total employee count for employers using the annual average from employer-reported quarterly data. Provides that the Department may provide notice regarding penalties in an electronic format to be determined by the Department. Removes a provision stating that penalty provisions shall become operative 9 months after the Illinois Secure Choice Savings Board notifies the Director of Revenue that the Program has been implemented. Makes other changes.

|

|

Virginia (workforce 3.8 million) – Following on the heels of its comprehensive report, Virginia has proposed legislation which is making its way through the legislative process. The bill passed the House by a vote of 56-44 last month and on February 5 by unanimous vote was continued to 2021 Senate Special Session 1 in Finance and Appropriations.

and …

|

|

Idaho (workforce 0.9 million) is the latest state with proposed retirement security legislation. House Bill 180 was introduced on February 16 relating to the Idaho Work and Save for Retirement Program; the bill would define terms, establish a Work and Save for Retirement Fund and administrative fund, establish provisions regarding a board, provide for program design and investment responsibility by the board, to provide for certain program components, and provide a program timeline. The program is described as voluntary for covered employers, employees, and self-employed persons.

|

|

Meetings on Deck.

-

California (workforce 17.9 million) –The next meeting of the CalSavers Board is scheduled for March 17, 2021.

-

Connecticut (workforce 1.6 million) – The next scheduled meeting of the Connecticut Retirement Security Authority is March 19, 2021.

-

New Mexico (workforce 1.0 million) – The meeting of the New Mexico Work & $ave Board originally scheduled for February 18 is now set for March 25, 2021 at 2p Mountain time. Register to join the meeting and watch for the agenda here.

|

|

Grant's Go-To's: Considering the Employer Mandate |

|

One of the key decisions in the development of a state-facilitated retirement savings program is whether to require employers to participate if they don’t already have some type of qualifying plan available for their employees. Because an employer mandate is not possible with an ERISA multiple employer plan, this is really only a decision for Auto IRA programs.

Making a program voluntary for employers can look like the easier path to legislative success. It’s not uncommon for interested parties to express concern about possible administrative complexities for employers. And everyone is sensitive to the impact of the COVID-19 pandemic on both employers and employees.

On the other hand, employer-voluntary approaches have so far shown limited uptake and use.

From a public policy perspective, a key question is whether. …

|

|

Mandates encourage employer facilitation, which is the gateway to access for employees, but what about workers themselves? How do states encourage employees to participate and save for retirement? In the next edition of this column, I’ll explore the “soft paternalism” of features such as automatic enrollment and automatic escalation of contributions.

Stay tuned! / Grant

|

|

Check this one out: Earlier this month, the National Bureau of Economic Research published a working paper titled Auto-Enrollment Plans for the People: Choices and Outcomes in OregonSaves, researched and written by professors and research experts John Chalmers, Olivia S. Mitchell, Jonathan Reuter, and Mingli Zhong. The paper analyzes participation choices (including the choice to opt out), account balances and inflow/outflow. The authors conclude that overall, “OregonSaves has meaningfully increased employee savings.” We love that conclusion!

Another Oregon tidbit: we like to follow the Oregon Employment Department’s workforce and economic research. This piece addresses employment trends in transportation and warehousing, two sectors that have been both buffeted and buoyed by the pandemic. Why we care: we’re interested in understanding employment shifts that may impact benefits like access to retirement accounts.

New from NIRS: Retirement Insecurity 2021 | Americans’ Views of Retirement by Dan Doonan, Kelly Kenneally and Tyler Bond. “More than half of Americans (51 percent) say that the COVID-19 pandemic has increased concerns about achieving financial security in retirement. And the COVID-19 concern is high across party lines: 57 percent among Democrats; 50 percent for Independents; and at 44 percent for Republicans.” In this report, Americans emphasize the appeal of solutions that provide secure, annuity-like retirement income. Read: Social Security, and defined benefit pension plans, and a concern about ability to manage their own money in retirement.

What We’re Reading: This week it’s Rutherford B. Hayes by Hans Trefousse. We’re not sure if we should recommend this one. It reads a bit like a book report, despite the fact that “Ruddy” was a very interesting person! The book we really wanted to read wasn’t available on Kindle so we are suffering through. We make our selections using the advice of Steve from BestPresidentialBios.com, who’s invested some serious time into presidential biographies.

If you want a much more spicy view of the Presidents, try the podcast Very Presidential with Ashley Flowers. This short series focuses on the bad behavior of fifteen of our former leaders. She manages to get George Washington onto the list – must listen soon!

|

|

... and now for Pix of the Week! |

|

There’s a lot of cuteness and outdoorsy fun going on here. Beautiful Ella and Dad know how to have a good time! It may be winter where we are but these pix have us looking forward to spring. Thank you for sharing, Frerichs Family! |

|

Meanwhile in the Northwest, winter weather is having its way with us. In western Oregon we get storms where warm moist air from one direction meets cold air from another, creating freezing rain. Icy rain sticks to the trees, bringing down limbs and even splitting trees to their roots. We’re still cleaning up from the Valentine’s Day storm that had 300,000 people without power and left a big mess behind. Neighbors said the sound of trees coming down was so unnerving that they left their homes to stay elsewhere.

Looks like we’ll be planting some new trees ourselves in a month or two! 🌳

|

|

OK, that’s a wrap. ❤ Hug your people and change the world.

If you like this piece, please stick with us. We’ll be back in about two weeks. If you don’t like it, please unsubscribe below. Comments for us? Please let us know. Want your own subscription? Request one here. All information shared is from public sources or used with express permission.

|

|

Massena Associates provides process, policy, and implementation consulting on retirement savings programs and products. Our clientele includes states, governments, policy organizations, and private sector providers. Our specialty – efficient, targeted results. We are an active speaker on retirement security topics, including state-facilitated programs, MEPs and more.

“We would not be where we are without Lisa’s great leadership and direction.”

If you’d like to explore working together, we welcome the conversation. Connect with us here, and at 339-236-0684. |

|

Looking for a great retirement savings innovation resource? Led by Dr. Alicia Munnell, the Center for Retirement Research at Boston College develops and hosts terrific content and proprietary research related to states, financial security, social security, and more.

Pew’s Retirement Savings Project studies the challenges and opportunities for increasing retirement savings and is another great resource - check out the work of John Scott and his terrific team.

|

|

|

|

|

|

|