|

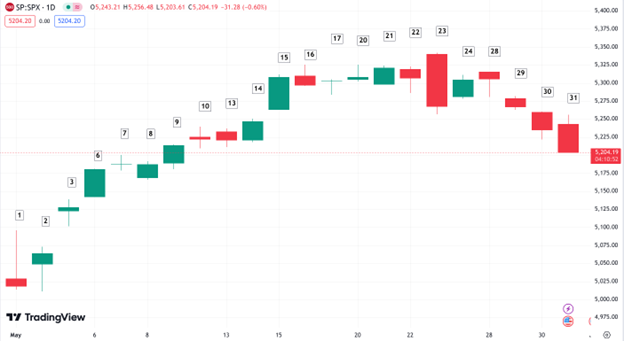

S&P 500 Index - Daily Chart - May 1 - 31, 2024 (Source: Tradingview)

May 1

The major averages rebounded from a miserable April but fell into the close, ending mixed for the day. Dow stocks increased by 87 points, while the S&P lost 0.34% and the Nasdaq fell 0.70%. The Federal Reserve left rates unchanged, with Fed Chair J. Powell believing that interest rates are high enough to suppress inflation despite the current lack of progress.

May 2

Bond yields retreated as investors absorbed the Federal Reserve’s news, lifting the market. The Dow jumped by 322 points, with the S&P and Nasdaq gaining 0.91% and 1.29%, respectively. Consumer sentiment was bolstered by both the receding bond yields and the Federal Reserve's implication of a potential rate cut in the coming months.

May 3

A jobs report came out weaker than expected, heightening expectations for future rate cuts. The Dow surged another 450 points, with the S&P gaining 1.26% and the Nasdaq finishing up 2%. The April non-farm payrolls were below expectations, unemployment rates were higher than estimates, and job growth came in beneath projections.

May 6

Stocks received a boost during midday, with relatively good news about the Israel-Palestine conflict helping the market close at highs. Dow stocks climbed 176 points, the S&P rose 1.03%, and the Nasdaq increased by 1.13%. A well-received jobs report eased inflationary fears, continuing the market's upward momentum.

May 7

The Dow continued its winning streak with a 32-point increase, the S&P rising by 0.13%, while the Nasdaq flattened out with a 0.01% loss. Bond yields decreased slightly as earnings season continued, with Disney dragging on the Dow with a decline of 9.51%. Revenue misses beat Disney’s stock down as streaming services caused the company to lose money.

May 8

After the momentum from the previous week’s job report faded, stocks were mixed and indeterminate. The Dow, with help from Goldman Sachs, Boeing, and JP Morgan, rose 172 points while the S&P was virtually unmoved, and the Nasdaq fell a meager 0.04%. With a lack of market-moving data, the market began to stagnate.

May 9

The market bounced back with leadership from industrial and bank stocks, while technology took a step back. Dow stocks continued to escalate, climbing 331 points, while the S&P rose 0.51% and the Nasdaq drifted 0.16% higher. The market rebound was favorable, but consumer fatigue remained apparent.

May 10

Stocks steadily moved upward after making up April losses, awaiting crucial economic data in the upcoming week. The Dow rose by 125 points, the S&P gained 0.17%, and the Nasdaq ended 0.26% higher. The University of Michigan consumer sentiment gauge came in well below estimates, pulling stocks from session highs.

May 13

Main stocks flatlined for the day, whereas meme stocks suddenly rose, with Gamestop surging 74%. Dow stocks fell by 0.21% (-81 points), the S&P remained flat with a 0.02% loss, and the Nasdaq rose 0.21%. There was a noticeable broad increase in the market, even forcing underperforming stocks upward.

May 14

Inflationary data lifted stocks, causing the S&P to near record highs and the Nasdaq to break them. The Dow rose 126 points, with the S&P gaining 0.48% and the Nasdaq climbing 0.68%. The PPI for April was higher than expected, but revisions to March inflationary data pacified consumer sentiment.

May 15

The April Consumer Price Index rose less than expected, pushing the S&P past record highs. The Dow jumped 349 points while the S&P increased by 1.17% and the Nasdaq by 1.49%. The low CPI report was interpreted by investors as a sign of slowing inflation.

May 16

After reaching record highs, Wall Street underwent a period of adjustment. Both the S&P and Nasdaq declined by 0.21%, and the Dow lost 38 points for the day. With help from the CPI report and the rally following it, the market had overall recovered from the 5% deficit in April.

May 17

With moderate persistence, the Dow managed to end the week above 40,000 points. The Dow rose 134 points, the S&P increased by 0.12%, and the Nasdaq drifted 0.06% lower. The bounce back from April was facilitated by corporate growth, easing inflation indicators, and a drop in bond yields.

May 20

Nvidia boosted the S&P to record highs while JP Morgan pushed the Dow into red territory. Dow stocks ended down 196 points while the S&P eked out a 0.09% gain and the tech-heavy Nasdaq climbed 0.69%. JP Morgan's CEO, Jamie Dimon, revealed his retirement timetable, stating that succession plans are in the works.

May 21

The market held steady as the S&P awaited Nvidia’s profit report while investors remained patient regarding inflation. Dow stocks rose 66 points, with the S&P increasing by 0.25% and the Nasdaq by 0.21%. The S&P rose thanks to Microsoft releasing information about its AI offerings to software developers.

May 22

The major averages dropped as Federal Reserve officials revealed their misgivings about cutting rates too soon. The Dow fell by 201 points, the S&P declined by 0.27%, and the Nasdaq decreased by 0.05%. Nvidia announced a 10-1 stock split and reported adjusted earnings of $6.12, greatly exceeding expectations.

May 23

Despite Nvidia’s support for the major averages, a declining semiconductor rally and stronger-than-expected servicing and manufacturing data dragged stocks down. Dow stocks plummeted 600 points, the S&P lost 0.77%, and the Nasdaq fell by 0.44%. Boeing lost 6.7% for the day, becoming the largest contributor to the Dow’s 600-point fall.

May 24

Wall Street regained a portion of its previous day’s losses, avoiding an otherwise losing week. The Dow barely moved with a 4-point gain while the S&P rose 0.70% and the Nasdaq climbed 0.99%.

May 27

The U.S. stock market was closed for Memorial Day, so there were no significant trading activities or economic reports scheduled for this day.

May 28

On Tuesday, the Dow lost 220 points, the S&P 500 fell by 0.35%, and the Nasdaq decreased by 0.45%. The S&P CoreLogic Case-Shiller Home Price Index showed a continued rise in home prices, while the Conference Board's Consumer Confidence Survey for May indicated improved sentiment despite economic uncertainties.

May 29

Wednesday saw the Dow drop 305 points, the S&P 500 decline by 0.50%, and the Nasdaq decrease by 0.65%. The Richmond Manufacturing Index showed mixed manufacturing activity, while the Federal Reserve's Beige Book provided regional economic insights. Salesforce's Q1 earnings showed strong revenue growth but a significant stock drop due to guidance concerns.

May 30

On Thursday, the Dow plunged 450 points, the S&P 500 fell by 0.75%, and the Nasdaq decreased by 0.80%. The Q1 GDP growth rate was revised down to 1.3%, reflecting slower consumer spending. Weekly jobless claims and April's pending home sales data contributed to a subdued market atmosphere. Dell Technologies reported strong revenue growth but saw a stock price drop due to future performance concerns.

|