|

3. Stay Alive to Thrive: Portfolio excellence sustains investment activity/playing offense.

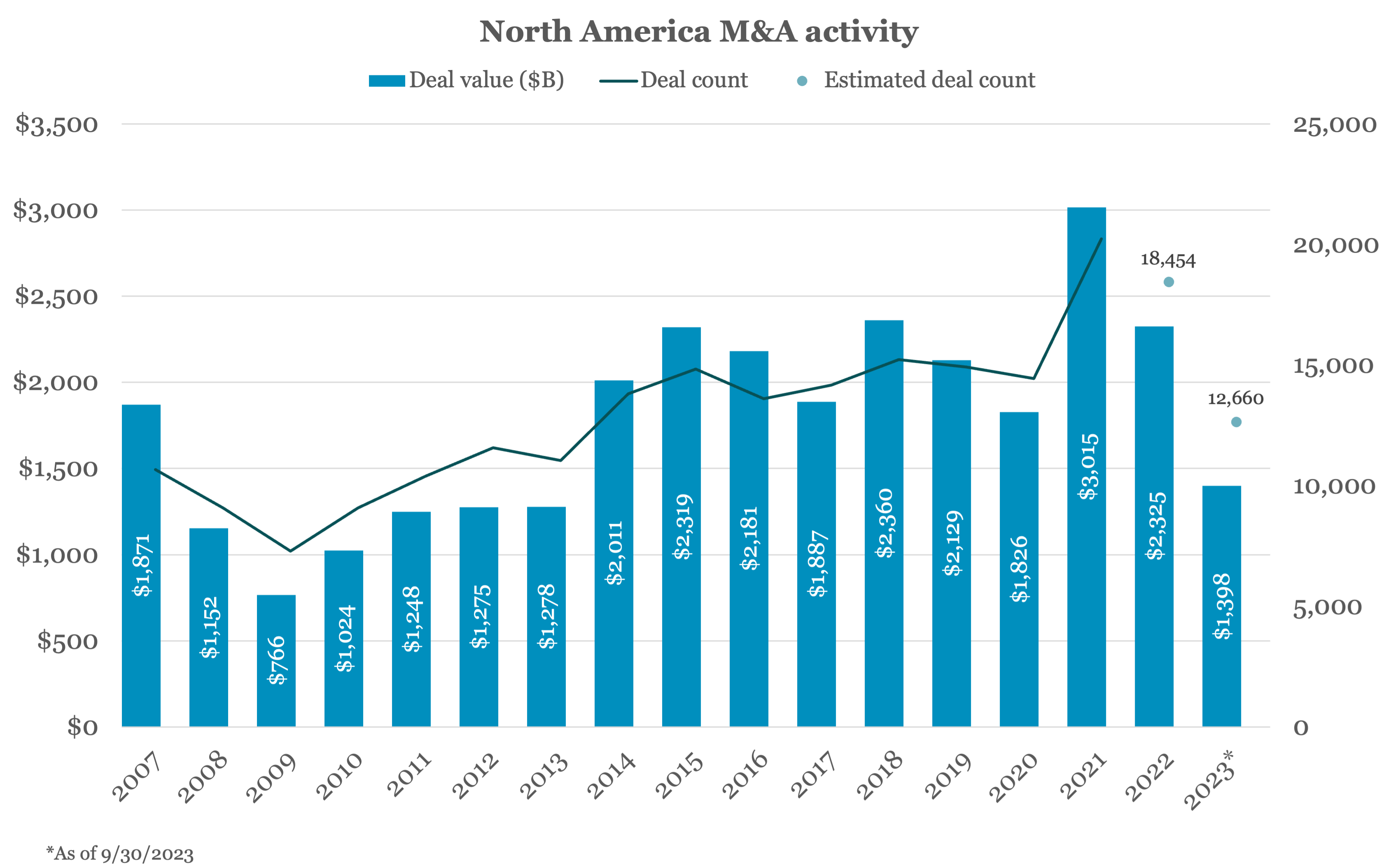

Last week we wrote about the growing gap between private capital winners and losers. That will only accelerate as today’s winners emerge from the higher rate market. Experienced managers with healthy, high-quality portfolios can and will continue to play offense and take market share. Our own portfolio expanded nicely despite a marked decline in overall middle market M&A volume.

What goes into creating portfolio excellence? We put it into three operating principles:

First, diversification as a shield. It’s easy to talk about portfolio diversification (everyone does), but what does “diversified” really mean? Diversification must be evaluated across multiple dimensions: sector, deal structure, leverage profile, sponsor relationships, company model, and so on.

Absolutely fundamental is having no outsized loan commitments relative to the size of the portfolio. As one example, our average position size is well below 1%. This intense focus on diversification minimizes the impact of any challenged investment. So, while we have certainly seen headwinds in certain areas such as multi-unit healthcare, third-party logistics and digital marketing, the platform continues to play offense with deployment up smartly.

“Flight to quality” was a key theme for investors in 2023 given overall market uncertainty. Prioritizing high quality assets should always be a focus, irrespective of economic conditions. By consistently backing strong businesses (in bull and bear markets), investors can have a durable portfolio with sustained growth despite a tough environment with minimal watch-list names. Quality businesses are those that 1) have strong cash flows and margins; 2) offer non-discretionary products or services and (3) operate in service-oriented, B2B end markets.

Finally, investing behind sponsor-backed portfolio companies has been crucial to mitigating risk. GPs not only bring deep experience creating value through market cycles, but also have meaningful skin in the game, typically through a significant cash equity investment. In today’s portfolios, it’s not unusual for buyers to contribute 60% equity or more.

This dynamic creates real alignment between lenders and PE firms, helping to drive positive outcomes when things go sideways. By focusing on sponsor-backed financings, private capital investors can efficiently allocate resources to the best opportunities.

By maintaining a diversified portfolio, focusing on resilient sectors, and mitigating risk through strong alignment, private capital investors will not only survive challenges but can also thrive amidst uncertainty. In 2024, if overall market M&A volume picks up as expected, these winners should be very well-positioned for another strong year.

|