ISSUE 142, February 21, 2025 | |

| |

|

DURUM

Ryan Statz, Merchant

| |

|

- Durum is in a holding pattern waiting on a plethora of developments.

- The pending Mexico/Canada tariffs (slotted to take place March 1). Note, a few things here: the US is a large buyer of Canadian durum. If tariffs do occur, with limited north-south trade between the two markets, US millers will be forced to buy durum from ‘only’ US origin suppliers (BULLISH). However, Canada will lose a needed market and thus will get more aggressive on other pieces of business to continue to move durum (BEARISH)…will US prices tick lower in response to weakened global prices?

- You also have the Mexico drought situation that has not improved. Mexico buyers are starting to show interest in ‘other’ coverage to subsidize the potential lack of Mexico domestic production. Is this a play for the US with the tariff potential still in limbo? Or does Canada capture this business in lieu of the aggressive mindset scenario mentioned above? If Canada is successful to Mexico, US prices likely fall. If US is successful to Mexico, prices likely tick higher.

- All in all, markets will be affected by the 2 developments above. The degree and magnitude of which remains the million-dollar question.

- We will know a lot more of the course of the next few weeks.

|

| |

|

Joe Foley, Merchant

SOYBEANS

| |

|

|

Soybean futures hv been rangebound of late, following a 50cnt selloff over the last two weeks. Harvest in Brazil is well underway now, approaching 30pct complete, and slightly ahead of normal pace. Most observers are still estimating a record crop of 170-173mmt, with better-than-expected yields in the north offsetting some hot dry issues in the south. This is by far the largest soybean crop on record for any country and exceeds last year’s production by nearly 20mmt. Accordingly, we expect stiff competition from Brazil well into Q4. Managed money (funds) are maintaining a modest long, but nowhere near the size of their corn positions.

Export sales are seasonally slowing, with Brazil cash more than a 1.00/bu cheaper than U.S. PNW soybeans (landed in China) for March/April. Expect more choppy trade going forward with more attention focusing on U.S. acreage forecasts for the 2025 crop and of course the daily macro/tariff noise.

| |

Corn prices have been rocketing higher, trying to surpass 5.00 in March futures. Fund buying has been relentless, with managed money length now estimated at nearly 350,000 contracts (1.75bln bushels, well in excess of the projected carryout in the U.S.). The weather in S. America has improved markedly over the past few weeks with winter corn plantings now well ahead of normal pace @ 40pct complete, vs. 27pct average. The sooner the safrinha crop gets planted, the more likely pollination can occur prior to their seasonal hot/dry weather arriving. Nonetheless, U.S. PNW corn is the cheapest origin for Asian buyers (Japan, Korea, Taiwan) until at least June. Argentina corn Is getting cheaper for April/May however, and Brazil will take over starting in August, assuming normal weather going forward. Rail logistics in the northern plains have been awful this month due to the cold weather and crew issues. Columbia River exporters are struggling to get their trains spotted and interior locations can’t get empties. Hopefully this situation moderates along with the weather forecasts. S. America weather remains key as safrinha only getting planted now, so a long way from making their crop. The market still expects a slightly larger crop in Brazil than a year ago (126mmt vs. 122mmt last year). |

| |

|

WHITE WHEAT

Steve Yorke, Merchant

| |

|

We are finally starting to see some upward movement in the wheat markets. Cash prices for white wheat have surged to the highest levels since last October. Currently we are sitting at 6.30 per bushel which is up about .15 cents from our last newsletter. Much of this can be attributed to futures rallying due mainly to some weather issues in the US plains and more Black Sea unrest. Both situations will need to be monitored closely moving into the spring. Strictly on the white wheat side we are continuing to see steady export business and at this writing year to date exports sit at 192MBU which is up 43% from last year at this time. As I have mentioned before this is exactly what we need. Ending stocks are starting to get a touch tighter. In the past few weeks, we have not seen any more feed wheat being traded out of the PNW because Aussie and Black Sea values are cheaper, but we had our fair share earlier. We will keep a close eye on this as anymore will really start to chip away at our stocks. Club premium remains at .15 cents but stocks are tight so we could see some upward momentum in the months ahead. The past two weeks have provided some nice opportunities to place HTA’s and accumulators for next year’s crop. Please keep in touch with your local buyer to ensure your orders are in and working. We are always here to help explain all the tools available for you to market your grain. |

| |

|

HARD RED SPRING WHEAT

Justin Beach, Merchant

| |

|

What an interesting 2-week period. Export business remains quiet off the PNW. FOB Vancouver is offered 95MWK which is considerably cheaper than PNW basis levels and importers of spring wheat continue to buy Canadian. BNSF performance has been horrible the last 2 weeks with the cold snap across the Northern Tier of the US. This has caused secondary rails freight to explode higher and remain elevated through the freight curve. Meanwhile, PNW bids have moved lower which has caused basis to retreat aggressively in the interior in Montana. However, domestic mill coverage is strong and most business is May forward and premiums in the Eastern Milling Market remain stagnant. The ND farmer has been much less engaged selling HRS than in Montana and business remains flat. Price targets have moved higher and a lower move in the board would turn off farmer selling for the time being, so basis seems to have reached an inflection point. The weaker dollar over the past 2 weeks has aided Minneapolis futures and funds have moved to reduce short positions. Many believe policy from the Trump administration is inflationary therefore we will see more fund money entering the wheat market and supporting cash prices. |

| |

|

HARD RED

WINTER WHEAT

Ryan Statz, Merchant

| |

|

- A rallying futures market and exploding rail freight values continues to be the name of the game in HRW cash markets.

- Psychological flat price benchmarks are being hit to the grower and the rally is being rewarded. This is leading to a lot of grower selling which is far out pacing overall demand in all markets – domestic, gulf, and PNW. Basis levels continue to tick lower in response.

- One interesting development with nearby basis softening are the cash carries from old to new crop that are arising.

- This has been met with solid grower sales in deferred / new crop windows to take advantage.

- Simply put, in the upfront windows, the market is receiving more grain than it can sell out.

- The market needs to see demand pick up. The concern is that at these flat price levels, most incremental business for US demand is not in the question as US values are at a significant premium to ‘other’ world values. US buyers are backing off in response as they don’t want to get caught trying to catch a falling knife. Additionally, the US market is now priced out of any HRW going to feed channels….

- The market knows we started the marketing year off in an impressive way…but stated previously, this has tallied off significantly the last 90 days.

- HRW Routine demand alone won’t push supply tightness quick enough to firm premiums in a big way before summer programs.

- The market needs to get back to some incremental (S. America/Cent. America/Indo/China/feed) demand for this to happen. These destinations are what drove the big pace to start the year. Again, this business has tallied off the last 3 months.

- In addition to futures action, the market continues to watch:

- Rail Freight / Transportation

- Global crop conditions/turmoil – particularly Russia/Black Sea

- World ‘feed’ markets.

- USD currency firmness

- Tariffs

|

| |

|

Feed the rally, don’t let the greedy bird get you…Remember don’t get analysis paralysis, place Good ‘til Cancelled orders to take advantage of knee jerk reactions in the futures markets when it rears its head up.

I will be visiting the below charts on a regular basis over the next few months as we turn the page to really focus on new crop opportunities. It’s never too early to look at new crop opportunities and by new crop I mean as far out as we can physically go in the futures markets to help offset some of the price risk, looking out to the ’25 crop year along with the ’26 crop year or even the ’27 crop year.

Utilizing the cost of production approach is and always will be the best approach to planning your marketing decisions. Knowing your cost of production and adding your desired rate of return early in the marketing year campaign does help alleviate some of the emotions behind pulling the trigger on your grain sales.

We have had a nice rally over the last few weeks in corn wheat(s) and soybeans and we have seen the producer rewarding the rally and taking advantage of some of these most recent price moves. On the charts below I have some pricing targets that I will be addressing over the next few months – but the levels that I am looking at are purely from a chart perspective and do not take into account any desired rates of return or your cost of production.

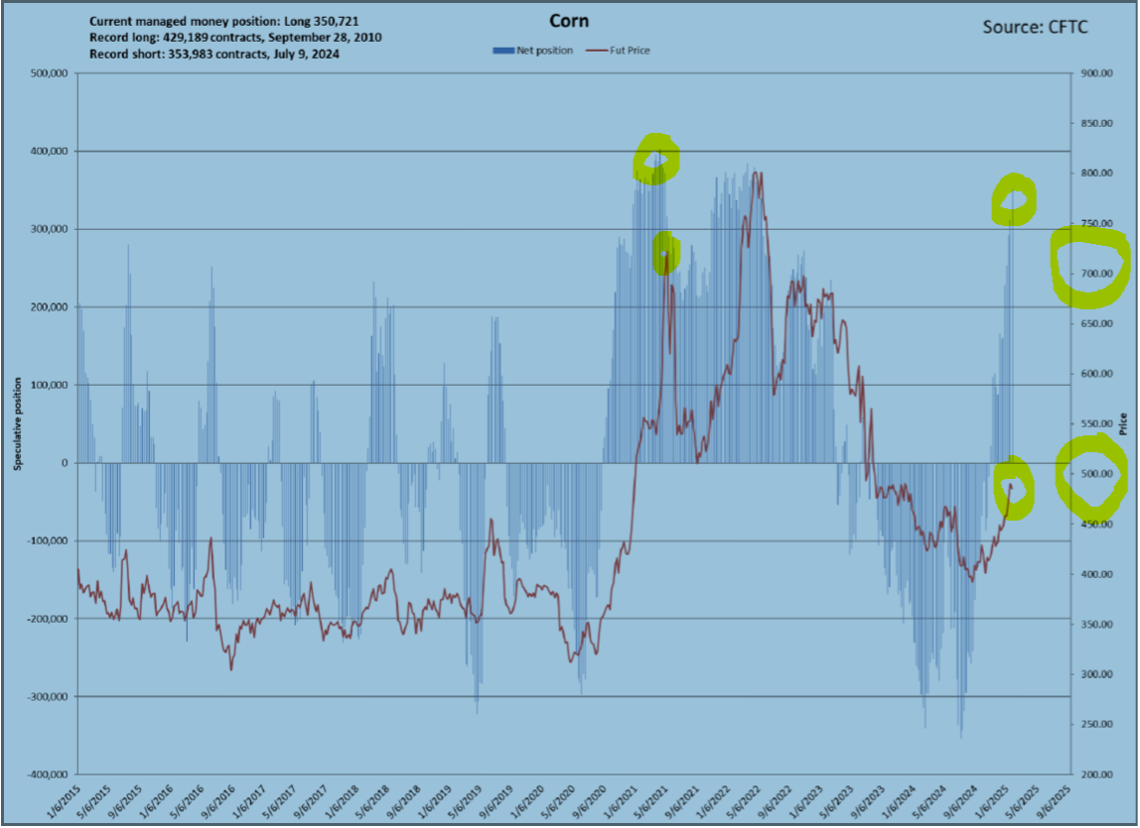

| Kansas September futures have hit the first two pricing points that we have listed on the charts with the first target established at $6.25 KWU5 – this price was first hit in early February and the markets pulled back slightly but then rallied further giving us some additional selling opportunities at $6.60 KWU5 just this week (February 18th). Kansas September has eased a bit since hitting that price earlier this week, but I would have some additional sell orders sitting up at $6.80 and then again at $7.00 KWU5 if we have the opportunity to sell $7.50 KWU5 I would be selling rather aggressive and more importantly I would also be looking out the ’26 crop year to see if the same opportunities exist going to next year as well. | I would have a similar approach to the Chicago Wheat September futures market as well, we have had the opportunity to sell WU5 at $6.30 a few times in February starting in early February. We have not hit the next selling target on the chart below at $6.60 WU5 BUT if we were looking at accumulator contracts, we have would have been able to get that price a few times over this most recent rally. If we can sell $7.00 WU5 I would be selling this price rather aggressively as well and again, more importantly I would be looking to see what opportunities exist going to the ’26 crop year. | Switching gears to look at corn – corn has had a very nice / aggressive run higher over the last two months now – we had what could be viewed as a ‘double bottom’ back in December of last year. With the ‘funds’ building a long futures position this has resulted in December corn rallying over 50 cents a bushel and trading on the chart below at $4.80 for the most recent high. This rally has occurred with eh funds building a significant long futures position giving us some wonderful pricing opportunities that we REALLY need to be taking advantage of. The funds have recently come very close to creating a new record long position in corn, which does create some concerns that this position as we could be getting overdone and due for some ‘profit taking’. The danger we are faced with now is in the event the funds get ‘spooked’ by something in the marketplace and they decide to unwind their position we could see some rather dramatic moves. | |

The below chart shows the historical funds position in the corn market and the corresponding corn futures price at the same time. The area of concern that I see now is if / when they decide to unwind the position. The last time the funds held a position of this length in May of ’22 the corn market was trading around $8.00 on the futures board when they began to sell this position out taking it from long 380,000 contracts to long 100,000 contract the futures markets moved from $8.00 to $6.00 rather aggressively. Today we see nearby corn futures trading around $5.00, now it is important to remember that no two marketing years are the same and there are different aspects in play today than there was in ’22. But if we do see something spook the funds and they decide to unwind their long position quickly they could have a rather dramatic negative impact on the futures price going forward.

For now, it is important to get your orders working and look at all the opportunities and tools that we can offer through Columbia Producer Solutions to help enhance your selling price and help to reduce some of the emotion behind pulling the trigger on your grain sales.

| | |

|

Sean Ferguson, Merchant

CANOLA

| |

|

|

ICE canola futures have sustained higher prices the past few weeks off the heels of firmer global vegetable oil prices. In their most recent report, the North American Oilseed Processors Association lowered both the soy crush as well as soy oil stocks in the states. The slower soy crush combined with the tightening of US soy oil stocks have provided recent price buoyancy for soy oil on the CME. Palm oil values have also exhibited strength following the Indonesian government’s announcement of more stringent biofuel mandates, meaning more palm oil will flow into the biofuel realm as an admixture. The past few weeks have seen managed money aggressively flop their ICE canola position from short to long. The mix of bullish global vegetable oil fundamentals as well as StatsCan’s recently published lower Canadian canola stocks value have contributed to the change of bias on the managed money front and subsequently, stronger futures. Basis has remained steady to firmer at US crush facilities as oil buyers eagerly buy from US manufacturers in efforts of circumventing potential tariffs from product coming from Canada.

CGI is excited to announce a non-GMO canola Act of God contract. Contract specs include 20 bu/acre AOG on dryland and 40 bu/acre AOG on irrigated land. Experience the yields of commodity canola with the benefit of a healthy non-GMO price premium.

Planting seed is available for purchase. Please contact your local CGI representative for more information.

| |

|

The flax market has remained flat the past few weeks as the shine of a potential trade war between the US and Canada has begun to wear off. Many buyers in the US have gotten their fill out of Canada and are now stepping back to see what unfolds in the next few weeks. Buyers in the EU and China continue to buy flax in style out of Russia and Kazakhstan. As long as stocks remain ample in Eastern Europe, prices will be hard pressed to exhibit serious strength.

CGI’s flax AOG pricing has now been released. Contact your local CGI elevator for up-to-date pricing.

|

| |

|

BARLEY

Matthew Schorn, Merchant

| |

|

|

Tariffs Update

Tariffs continue to keep buyers and sellers on the sidelines as they wait for more clarity around the proposed March 1st deadline.

- Malt barley traditionally moves between Canada, Mexico, and the US, but the risk of tariffs is pausing demand decisions.

- The potential for US feed barley imports to Canada facing a tariff could lead to a drop in feed barley prices in Montana, as suppliers seek to offset the additional costs and other demand markets are bid lower.

- Both buyers and suppliers are hopeful that a long-term resolution to these tariff discussions will be reached.

Malt Demand and Price Trends

Malt demand remains limited with no participation from buyers in both the old and new crop positions.

- Prices continue to decline as the market adjusts to this sluggish demand, and in many cases, there are no bids for nearby delivery periods.

- Consumer preferences continue to shift away from beer, with increasing interest in wine, seltzers, and cannabis products.

Canadian Domestic Feed Market

Domestic feed values in Canada are flat, with the Canadian feedlot well covered for March and April requirements.

- Feeders have been cautious in placing new cattle orders, with many uncertainties arising from ongoing tariff discussions.

- There is demand for barley May forward, but there is the grower is reluctant to sell and there is hesitation on the seller side on what will happen with tariffs creating a wide bid-offer spread.

- Barley continues to be the most economical feed grain in the ration, as rising corn futures push the corn-barley spread closer to 50USc per bushel.

- When the US dollar strengthens against the Canadian dollar, Canadian buyers lose import purchasing power, making US corn and barley more expensive compared to locally the inverse is also true, as we have seen the Canadian dollar come off the lows in recent sessions.

|

| | | |