Access our research on the Bloomberg Terminal with ERH GXY <GO>

|

|

"Frog nation" leader Dani Sestagalli embroiled in drama following on-chain activity and the revelation that his partner is a felon with multiple convictions; Solana network outage shows design tradeoffs in action; OpenSea forced to reimburse users after UX issue leads to losses. |

|

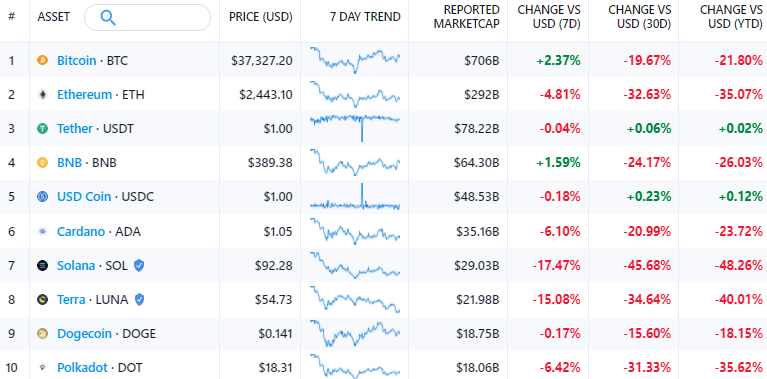

The total implied network value (market cap) of the digital assets market stands at $1.63tn, down 10% from last week (when it stood at $1.81tn). Bitcoin’s network value is 5.97% of gold’s market cap. Over the last 7 days, BTC is up 2.4%, ETH is down 4.2%, SOL is down 17.5%, and LUNA is down 15%. Bitcoin dominance is 43.29%, up 2 percentage points from last week. |

|

Data current as of 8:20am ET on January 28, 2022. Prices and Data via Messari.

|

|

The crypto bear market continued this week, and although the prices of majors appeared to stabilize a bit, the last 24 hours have felt like a rollercoaster. Here’s a quick summary of just some of the drama that went down:

-

A prominent DeFi founder named Daniele Sestagalli appeared to cash out some of his money surreptitiously before it was revealed that his anonymous partner on a major DeFi project was a felon with multiple convictions and former co-founder of fraudulent Canadian crypto exchange QuadriaCX (this is our top story below).

-

Facebook reportedly sold off the IP behind its controversial and stalled stablecoin project Libra/Diem to Silvergate Bank for $200m.

-

The SEC released a proposed change to the rules governing Alternative Trading Systems (ATS) that would expand the definition of an exchange to any “communication protocol system,” which some observers fear could ensnare decentralized finance protocols. (Read the proposal and SEC Commissioner Hester Peirce’s thoughtful dissent).

-

The US House released the text of its America COMPETES Act, a broad “must pass” bill put forth by Democratic committee chairs intended to promote American competitiveness in manufacturing, science, technology, and innovation. Buried on page 1482 of the bill, though, was a provision that would remove administrative procedures and safeguards (read: due process) from the Treasury Department’s ability to impose “special measures” prohibitions in the Bank Secrecy Act, allowing the Treasury Secretary “unchecked discretion to forbid financial institutions (including cryptocurrency exchanges) from offering their customers access to cryptocurrency networks,” according to CoinCenter.

-

Barons reported that the White House is preparing an executive order that would order federal agencies to analyze and “develop a set of policies that give coherency to what the government is trying to do” in the digital assets space, according to the report.

- The SEC denied Fidelity’s Wise Origin ETF (a spot Bitcoin ETF). While the outcome wasn’t unexpected, Fidelity is the most prominent firm now to have had their spot BTC ETF denied by the SEC.

- UX issues on OpenSea caused many users seeking to close out old NFT offers to be frontrun in the Ethereum mempool, resulting in at least one loss of over $1m.

And all this doesn’t even account for the FOMC meeting, after which Chair Powell refused to rule out raising rates at every upcoming meeting in 2022. It’s clear that the Fed is very concerned about inflation, with Powell saying they need to be “nimble” when it comes to monetary policy. The market viewed the press conference hawkishly, with expectations for the number of rate hikes between now and the end of the year reaching their highest levels (near 5). Bitcoin rallied into Powell's press conference to its weekly high near $39k before receding as low as $35.5k during and following the presser.

|

|

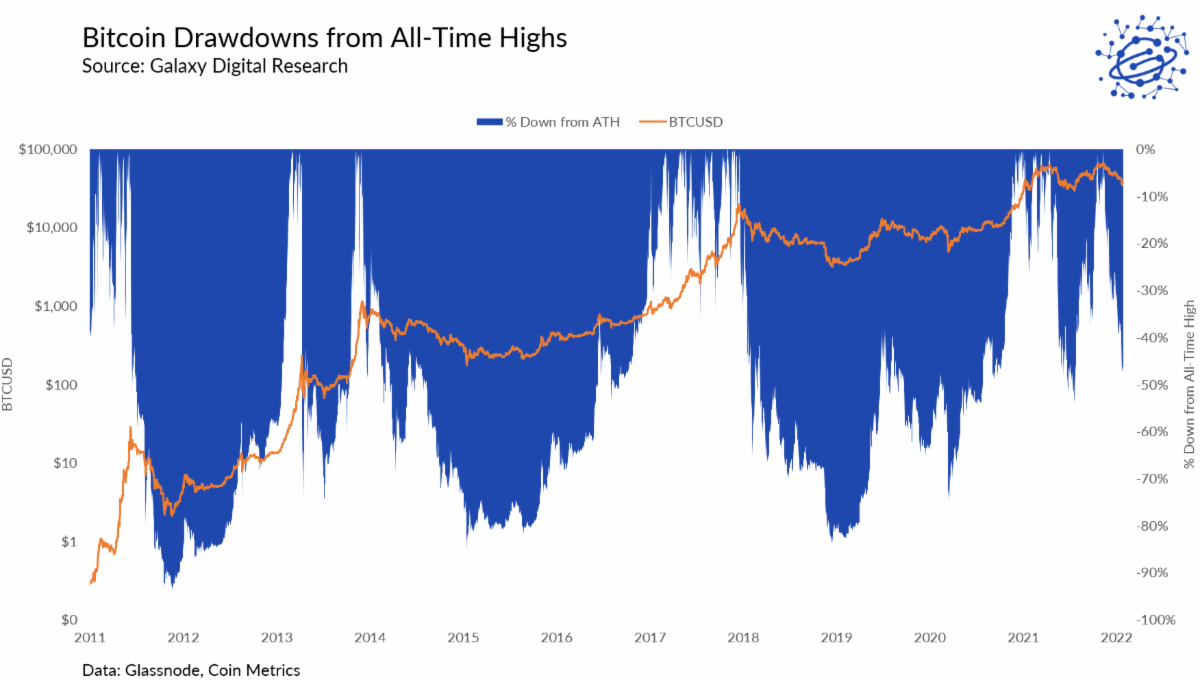

Ultimately, though, BTC and ETH mostly ranged sideways this week, with Bitcoin trading between $33k-39k and ETH between $2159 and $2742. ETHBTC swung pretty wildly, moving up and down as much as 9% in both direction throughout the week. Bitcoin is up 2.4% and ETH is down 4.2% WoW at the time of writing.

In a sign that a bear market has taken hold, almost 89.5% of the top 200 non-stablecoin cryptoassets by market capitalization are down more than 50% from their all-time highs (the average is –73% and the median is –77%). On a market-cap weighted basis, the top 200 non-stablecoin cryptoassets are -52% from their all-time highs (BTC is down 46% and ETH is down 50.5%).

|

|

BTC and ETH traded lower into and through the quarterly options expiry, but there was no dramatic sell pressure as a lot of in-the-money puts rolled off.

Stablecoin supplies have been growing, likely a result of demand for cash as traders exit long positions, and on the positive side balances on exchanges have remained consistent, suggesting that money is waiting on the sidelines rather than exiting the crypto economy entirely. A decline in stablecoin demand or even just significant reduction in supply held on exchanges would be a bearish indicator for the broader market.

|

|

Crypto markets are clearly in a wait-and-see pattern regarding regulatory and macroeconomic developments. With so many institutions considering or investing in digital assets, it’s clear that cryptoassets are more a part of the broader investment ecosystem than ever before, but that attention subjects the asset class to extrinsic factors not relevant to the nascent industry during prior cycles. But this also serves as an important point: the drawdown was the result of larger non-crypto market moves and sentiment, not a blowoff top like prior cycles. Indeed, 40% of NASDAQ-listed stocks are also down more than 50% from their 52w highs.

Nothing has changed in the long-term outlook for bitcoin or digital assets since all-time highs in November, and while some are on the sidelines waiting to see how things develop, others are taking the opportunity to add to their positions at lower entry points. The number of Bitcoin “accumulation addresses” (those that have received 2 or more non-dust inbound transfers but never sent) is spiking to all-time highs, while the balance held in those addresses also has seen a noticeable rise since December.

|

|

🐸 'Frog Nation' Croaks for Wonderland |

|

The criminal past of Wonderland’s treasury manager revealed. Wonderland was launched as a fork of Olympus, the original DeFi 2.0. Protocol-owned liquidity, on Avalanche by Daniele Sestagalli (@danielesesta), who had founded Abracadabra & Popsicle Finance. Wonderland’s treasury was managed by a pseudonymous individual (@0xSifu), whose identity was revealed on Wednesday to be Michael Patryn, former co-founder of QuadrigaCX, the Canadian crypto exchange that lost hundreds of millions of user funds through unsanctioned trading of customer funds. Patryn also has several criminal convictions in the past, including for taking part in operating an identity theft ring between 2005-07 (for which he served time in prison) and operating a ponzi scheme called Midas Gold.

Before the news of 0xSifu’s identity surfaced, some accounts on Twitter identified on-chain activity from Sestagalli that appeared to show he borrowed against his illiquid TIME holdings, swapped the resulting stablecoin (MIM) for USDT, and then allowed his on-chain position to be liquidated, apparently part of a strategy to cash out some gains while maintaining some plausible deniability. Then, following the identification of 0xSifu as Michael Patryn, Sestagalli issued a statement apologizing to the community and stating that he only discovered the identity and criminal-ridden history of 0xSifu after his appointment to treasury manager, although that was before Sestagalli had appeared to cash out. For the time being, 0xSifu has stepped down from his role while a governance proposal to confirm him to his role is currently open (currently ~80% voting in favor to reject him).

|

|

OUR TAKE: Sestagalli had been sitting on this compromising information for "about 1 month." Frog Nation, the passionate community behind Daniele Sestagalli’s projects, is angry and looking for answers. Outside of Wonderland, Abracadabra's SPELL token and Popsicle Finance's ICE token also saw steep drops in prices despite being separate projects run by separate teams.

|

|

Upon the public’s discovery of 0xSifu’s identity, rather than singlehandedly removing him from his role, Sestagalli decided to put it up to a community vote. Often times, founding teams are unfairly blamed for problems or flaws in the project - if the project is actually decentralized, the project teams cannot unilaterally push changes to the projects. The open-source nature of such projects allows anyone to propose an improvement or upgrade to the protocol for the community to vote on; the responsibility of the project team may be limited to just executing the code behind the approved proposals. That said, Sestagalli deserves some of the blame for his failure to do proper due diligence on his project’s treasury manager and for not acting or notifying the community of the information of 0xSifu’s criminal past sooner.

Whether Sestagalli was well-intentioned or not, the event is a reminder for all to exert caution and not to blindly put their trust in others, particularly with large sums of money. The saga also highlights the propensity of crypto natives to “ape” into new, promising projects, often without conducting sufficient diligence on the parties involved or the control they exert. Indeed, Sestagalli tweeted on January 9 that “doxed teams tokens will outperform anons ones.” But while we can't always know the people transacting on-chain, we can track their flows, and the flows of assets in their projects. That transparency allows users to judge for themselves the state of credit and leverage in the system, and act accordingly. Incidents like these are a reminder of both the nascency and power of decentralized finance and those who hunt for alpha and yield on-chain.

|

|

❌ Solana Endures Network Outage |

|

Solana’s ninth network outage this month underscores its growing pains as it chases scale above all else. This partial network outage is second in severity only to its 18-hour outage last September, which the Solana team described as a denial-of-service attack exacerbated by Grape Protocol’s IDO on Raydium. This most recent outage started on Friday, January 21st and lasted approximately 30 hours before being patched. According to this tweet, endorsed by Solana founder Anatoly Yakovenko, the recent outage was driven by volatile crypto markets coupled with Solana DeFi activity that has grown faster than the Solana network itself has evolved. In this case, a large number of open DeFi positions were underwater and targeted by liquidation bounty hunters, leading bots to race to close eligible positions (to capture liquidation bounties). Solana’s network subsequently saw a spike in the number of duplicate transactions on the network. Since Solana’s network fees are consistently kept cheap by design, bots were able to keep spamming the network, hoping to capture arbitrage opportunities visible on decentralized lending protocol Solend. And because Solana has no mempool (transaction queue) for transactions users to wait, regular users were crowded out by high frequency bot transactions and unable to get their transactions broadcasted on the network. In many cases, this meant that the users whose positions were undercollateralized were unable to recapitalize them, even if they wanted to do so. At the height of this outage, two-thirds of all transactions in Solana’s blocks were attempted Solend liquidations that failed.

Since the outage, there have been multiple remedies implemented in production by both the Solana and Solend teams. The Solana team started by rolling out the v1.8.14 update which primarily improves the performance of deduplication measures to prevent these types of spam transactions from accumulating on the network. The Solana team also plans to roll out additional improvements once they implement v1.9 in the next 2-3 months. The Solend team has also pushed a number of updates designed to give end-users a better chance of seeing their transactions confirm during these times of high network congestion. Their updates are described in the following blog post and boil down to 1) disabling pre-flight checks, 2) increasing staleness tolerance, 3) removing dependencies on pricing oracles for deposits/repays, and 4) creating a liquidator whitelist toggle for the core team. The Solend team is hopeful that their updates will substantially reduce the number of liquidations its users, particularly those who were willing but unable to post collateral, face during times of high network congestion.

|

|

OUR TAKE: Some have criticized Solana for its multiple network outages at seemingly the worst times. Others claim that Solana’s massive demand for block space at high throughputs is evidence that the technology, bursting at the seams in terms of adoption, is actually working pretty well. In other words, they see Solana’s outages as a “good problem” that will get solved over time. The truth is perhaps somewhere in the middle. Regardless, Solana’s congestion issues can serve as a real-world case-study on the challenges of scaling blockchains through a monolithic architecture. Going back as far as March 17th, 2021 (which is the earliest date with available data), Solana has had either a partial or full network outage for 106.27 hours. The network itself has been operating for 7,608 hours during this same exact timeframe, implying that the network is down (either partially or fully) 1.4% of the time. The question now is...is a 1.4% downtime a decent enough trade-off for a network with consistently high speeds and low fees? There isn’t a cut-and-dry answer to this. In some centralized industries, such as gaming, it is the norm to see servers go down for days at a time. The fact that Solana has already leaned heavily into the gaming industry might suggest that this trade-off is worth it for the performance guarantees it otherwise can offer its end-users. Said differently, Solana’s design decisions highlight a trade-off between robustness of the blockchain itself (zero downtime) vs usability of the blockchain (fast/cheap). It seems naïve to think that only one of these two extremes is the “correct” answer. Clearly, Solana prefers a mostly-on (99% uptime) and always-cheap approach instead of always-on (100% uptime) and sometimes prohibitively expensive approach. Those who disagree with the tradeoff can use different platforms—there are now many of them taking different design approaches. Different strokes for different folks?

What ultimately caused this outage to happen is a feature of Solana’s blockchain that optimizes for usability at the expense of robustness. Unlike many other blockchains, Solana does not use a traditional mempool for including transactions into the blockchain. Instead, it uses Gulf Stream, which predetermines block leaders to order transactions in a manner that can achieve incredibly high throughputs with low fees. Blockchains like Bitcoin and Ethereum with traditional mempools have transaction fees that incorporate free-markets, so the fees themselves can scale up or down depending on block demand. In other words, users with high priority transactions can pay higher transaction fees to skip the transaction queue—but Solana has fixed low fees and no transaction queue. On the other hand, Solana is architected in such a manner that fees are always low. Most of the time, this approach is good for users since they will always be able to make transactions at a low cost. During times of incredibly high block space demand, however, this fixed fee approach is a double-edged sword. Block demand can eventually outpace block space. In the absence of market forces to balance supply and demand, the network can screech to a halt. To make a crude analogy, imagine using Uber during a massive snow storm in a densely-packed city. To help balance supply and demand, Uber institutes surge pricing. This both incentivizes new drivers to drive (increasing supply) while disincentivizing end-users from calling a ride in favor of cheaper alternatives (decreasing demand). But during the covid pandemic, some cities (like Boston) banned surge pricing in hopes of keeping rides cheap... the reality was that drivers vanished entirely, making it almost impossible to find a ride. Bitcoin and Ethereum embody this concept of “surge pricing” with their fee structures while Solana does not. Using this same analogy for Solana, the end-result is that a bunch of users may open up the Uber app during a snowstorm, but the app keeps crashing, or there are no cars available. Instead of some people getting a ride (assuming they’re willing to pay more), zero people get a ride.

|

|

😮 Over $1mm Stolen Due to OpenSea Issue |

|

Savvy users of the NFT marketplace OpenSea have profited over $1 million this week by exploiting a loophole in the platform’s user interface. The loophole enables hackers to buy expensive and rare NFTs for a fraction of their value by purchasing the asset at previously listed price. Normally, if a user on OpenSea wants to delist their NFT and relist it at a higher price, they have to pay a fee for the removal. In order to avoid the removal charge, users on OpenSea have been relisting their NFTs without canceling previous list prices by transferring the assets over to a new wallet. While this workaround does update the listing price for NFTs on the OpenSea website, it does not always update the information stored on-chain which can be accessed through alternative NFT marketplace websites such as Rarible or through the OpenSea API directly.

Recent market volatility has caused ETH price to decline by close to 50% from its all-time high. Given that NFT listings on OpenSea are denominated in ETH as opposed to USD, but the NFT market has mostly priced rare NFTs in dollar terms (and the best projects have held up well in USD terms during the ETH downturn), there has been an influx of users updating the prices of their listings. As such, while the existence of this loophole has been publicly known since as early as Dec.31, 2021, it had not yet been exploited to a large extent until this week. One pseudonymous attacker by the name of “jpegdegenlove” bought a Bored Ape NFT at an old listing price of 0.77 ETH or $133,000 and was able to resell the asset for $934,000 in ETH. The OpenSea team has announced that it is actively reaching out to NFT owners who were caught unaware of the discrepancy in the platform’s UI and reimbursing lost funds.

|

|

OUR TAKE: Though OpenSea as a centralized company can make reparations for users in the form of a financial reimbursement, it has no way to restore NFT ownership after a trade has been executed. All trades on OpenSea are final by nature of these transactions being recorded on the Ethereum blockchain, an immutable ledger. While the finality of a blockchain can be an advantageous feature for businesses, it is a double-edged sword that comes with disadvantages as well. As highlighted by the exploit on OpenSea, the irreversibility of transactions means that the web interface explaining what exactly is being executed to the user must be crystal clear. To this end, OpenSea has recently launched a new NFT listing manager and dashboard for explicitly showing all of a user’s inactive listings and how to properly cancel each one.

Still, a centralized company using the blockchain as its primary ledger for transactions does beg the question why the centralized company needs to be the intermediary at all for executing user trades. Since the launch of OpenSea in 2017, the capabilities of smart contracts, autonomous self-executing code on Ethereum, has become increasingly sophisticated and complex. Smart contracts designed to mimic financial services such as trading, lending, derivatives, and more (“DeFi”) have accumulated nearly $80 bn in assets under management. As such, the need for a centralized NFT marketplace like OpenSea that conducts most of its core trading operations on-chain anyways is contestable, which is why alternative decentralized NFT marketplaces such as LooksRare are growing in popularity.

That said, a fully decentralized model for blockchain services such as an NFT marketplace does come with its own unique challenges and tradeoffs. For example, most decentralized applications on Ethereum operate today in a grey area as it relates to regulation, which also restricts avenues for fundraising and incentivizing user adoption. In addition, though the technology around coding applications for blockchains has improved significantly over the last few years, there is still a significant amount of research and development needed to overcome the operational challenges of creating a non-centralized approach to managing on-chain trades, as evidenced by the millions lost in DeFi hacks over the course of 2021. Even so, by straddling the line between having centralized and decentralized components to its business, OpenSea is forced the juggle the challenges of both models, without fully realizing the benefits of either.

|

|

-

Blockchain security firm Dedaub claims bug on cross-chain protocol Multichain put billions at risk

-

Facebook-backed cryptocurrency project Diem reportedly selling assets and intellectual property for $200mn

-

IMF urges El Salvador to reverse its decision to make bitcoin legal tender

-

Valkyrie files for a bitcoin mining ETF in the U.S.

-

The President of Russia Vladimir Putin calls for new laws to encourage bitcoin mining in the country

|

|

Access our research on the Bloomberg Terminal with ERH GXY <GO>

|

|

|

|

US Govt Report Offers Glimpse of Digital Dollar |

Read this November report from GDR's Head of Research Alex Thorn analyzing the Presidential Working Group on Financial Markets' report on stablecoins.

|

|

|

|

2021: Bitcoin Mining's Big Year |

In this report, GDR's Karim Helmy and Galaxy Digital Mining's Brandon Bailey give a detailed overview of the major events and trends that made 2021 Bitcoin mining's most important year. They also share detailed predictions for 2022.

|

|

|

|

MEV: How Flashboys Became Flashbots |

In this major report, GDR's Christine Kim does a deep dive on miner or maximal extractable value, how miners and bots frontrun users on Ethereum.

|

|

|

|

2021: Crypto VC's Biggest Year Ever |

In this report, GDR's Head of Research Alex Thorn summarizes the epic year in VC investing that saw more than $33bn invested in crypto/blockchain startups.

|

|

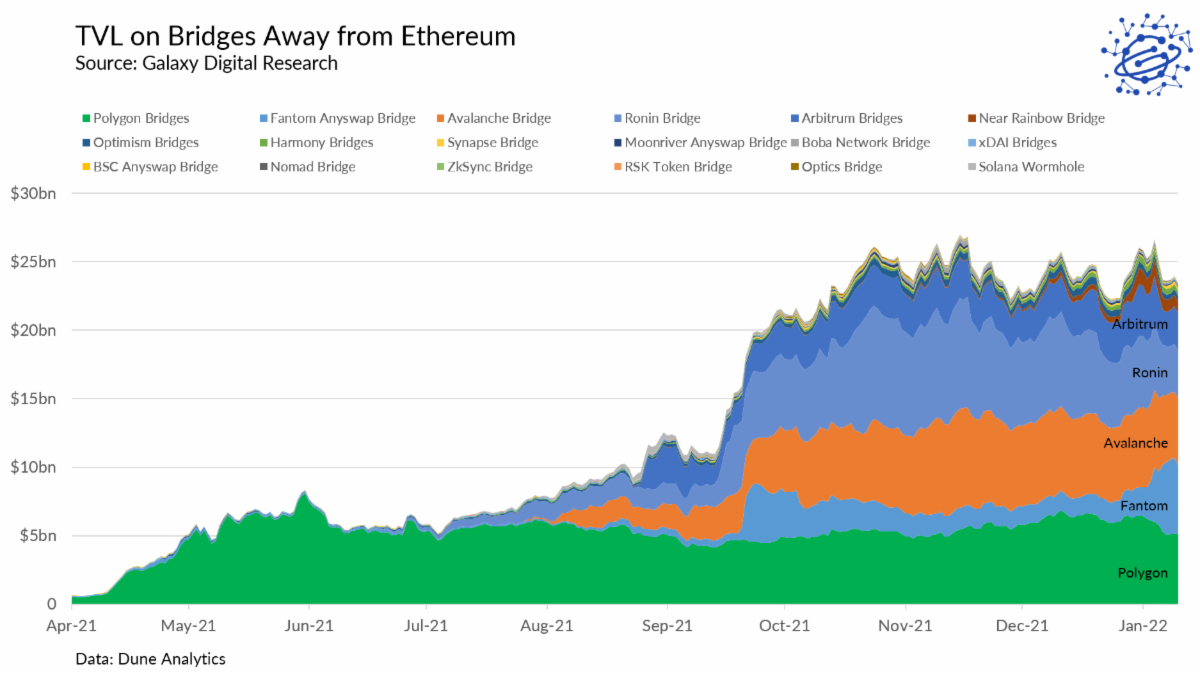

Bridges to other networks from Ethereum have mostly held their TVLs over the last few months, with growth having stalled. Fantom has grown its share. |

|

Despite bridge TVLs remaining mostly unchanged, the number of new daily depositors onto these bridges has collapsed over the last month. |

|

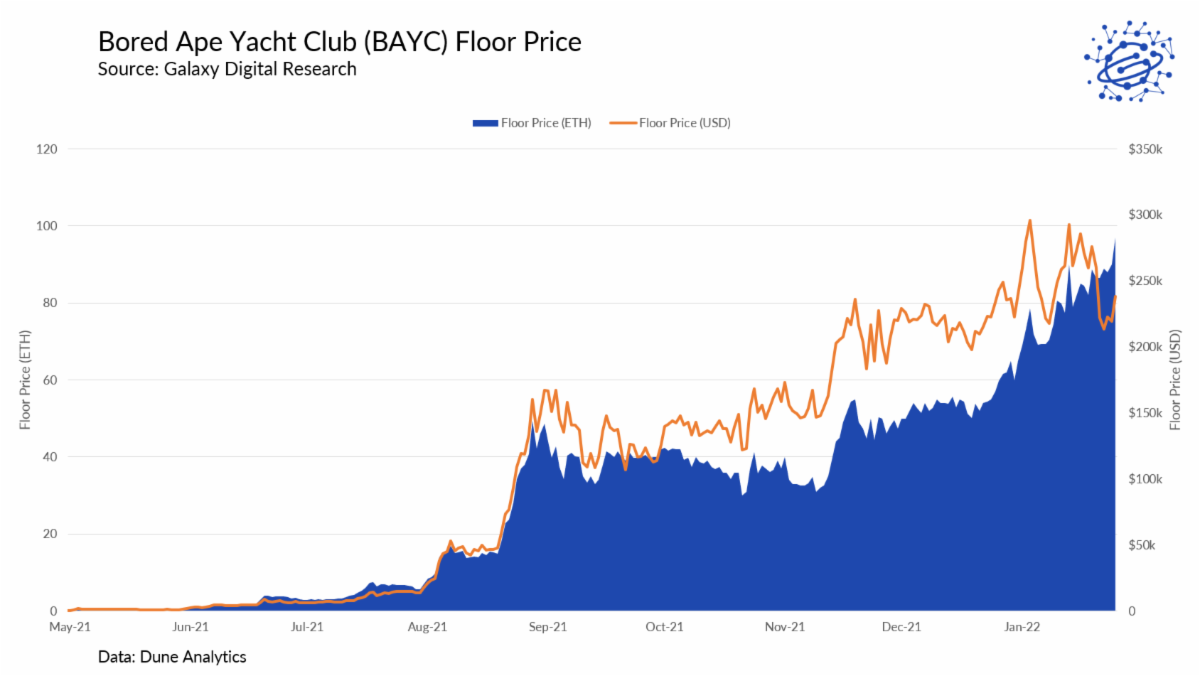

The market appears to be pricing top-tier NFTs in dollars rather than crypto, leading the "floor prices" of popular projects to rise as ETHUSD has declined. This decoupling between top-tier NFT project value and ETH price shows the strength of the NFT market outside of crypto circles. |

|

Thanks for reading this week. Have a great weekend.

|

|

Alex Thorn

Head of Firmwide Research

|

|

|

Legal Disclosure:

This document provides links to other websites that we think might be of interest to you. Please note that when you click on one of these links, you may be moving to a provider's website that is not associated with Galaxy Digital. These linked sites and their providers are not controlled by us, and we are not responsible for the contents or the proper operation of any linked site. The inclusion of any link does not imply our endorsement or our adoption of the statements therein. We encourage you to read the terms of use and privacy statements of these linked sites as their policies may differ from ours. This document, and the information contained herein, has been provided to you by Galaxy Digital Holdings LP and its affiliates (“Galaxy Digital”) solely for informational purposes. This document may not be reproduced or redistributed in whole or in part, in any format, without the express written approval of Galaxy Digital. Neither the information, nor any opinion contained in this document, constitutes an offer to buy or sell, or a solicitation of an offer to buy or sell, any advisory services, securities, futures, options or other financial instruments or to participate in any advisory services or trading strategy. Nothing contained in this document constitutes investment, legal or tax advice. You should make your own investigations and evaluations of the information herein. Any decisions based on information contained in this document are the sole responsibility of the reader. Certain statements in this document reflect Galaxy Digital’s views, estimates, opinions or predictions (which may be based on proprietary models and assumptions, including, in particular, Galaxy Digital’s views on the current and future market for certain digital assets), and there is no guarantee that these views, estimates, opinions or predictions are currently accurate or that they will be ultimately realized. To the extent these assumptions or models are not correct or circumstances change, the actual performance may vary substantially from, and be less than, the estimates included herein. None of Galaxy Digital nor any of its affiliates, shareholders, partners, members, directors, officers, management, employees or representatives makes any representation or warranty, express or implied, as to the accuracy or completeness of any of the information or any other information (whether communicated in written or oral form) transmitted or made available to you. Each of the aforementioned parties expressly disclaims any and all liability relating to or resulting from the use of this information. Certain information contained herein (including financial information) has been obtained from published and non-published sources. Such information has not been independently verified by Galaxy Digital and, Galaxy Digital, does not assume responsibility for the accuracy of such information. Affiliates of Galaxy Digital own investments in some of the digital assets and protocols discussed in this document. Except where otherwise indicated, the information in this document is based on matters as they exist as of the date of preparation and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available, or circumstances existing or changes occurring after the date hereof. The foregoing does not constitute a "research report" as defined by FINRA Rule 2241 or a "debt research report" as defined by FINRA Rule 2242 and was not prepared by Galaxy Digital Partners LLC. For all inquiries, please email contact@galaxydigital.io. ©Copyright Galaxy Digital Holdings LP 2021. All rights reserved.

|

|

|

|

|

|

|