Weekly update from the National Housing Conference |

|

In this issue

March 26, 2023

Issue 92-11

· HUD restores discriminatory effects standard

· Housing leaders raise concerns about Build America, Buy America Act's impact on affordable housing

· FHFA seeks input about updating credit models

· FOMC raises target funds rate

· Housing funding support letters circulate through Congress

· New HMDA mortgage lending data available

· HUD publishes new equitable broadband access guidebook

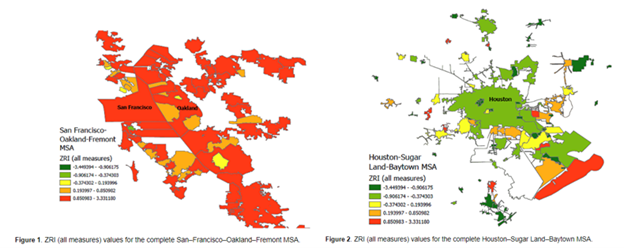

Chart of the week: Eviction Lab creates Zoning Restrictiveness Index

|

|

The Pitfalls of Cash-Out Refinancing in a Rising Interest Rate Environment

By Mike Calhoun, President, Center for Responsible Lending (CRL), and Edward Pinto, Director, American Enterprise Institute (AEI) Housing Center

Cash-strapped borrowers struggling to cope with high inflation and lagging wage growth are being enticed by cash-out refinance offers of easy access to their home equity, which increased dramatically during the pandemic. With today’s higher mortgage interest rates, taking out these first-lien loans will damage borrowers’ long-term financial health. Particularly concerning are trends and distributions for Federal Housing Administration (FHA) and Veterans Affairs (VA) programs, which typically serve minority, low-wealth, lower credit score, and veteran homeowners.

In a cash-out refinance, a homeowner with a mortgage takes out a new larger loan to pay off the outstanding principal on the existing mortgage and provide some amount of additional cash (the "cash out" in a cash-out refinance). Because the cash-out refinance interest rate is applied to that entire larger loan amount, cash-out refinances increase the amount of interest the homeowner pays on their existing loan balance whenever the cash-out refinance rate is above the original mortgage rate. In today’s environment, refinancing usually does mean taking on a higher interest rate—typically two to four percentage points above one’s existing rate. For example, the median interest rate on outstanding FHA and VA loans is 3.2% and 90% of these loans have an interest rate below 4.63%, while the rate on a cash-out refinance in late 2022 was close to 6.5%.

As a result, the typical FHA or VA borrower who completed a cash-out refinance in November 2022, obtaining about $36,000 in cash, saw their monthly principal and interest payment (P&I) on the balance of their old mortgage increase by $368 (37%). Assuming the borrower maintains the new mortgage for seven years, they will pay about $42,000 of additional interest on their existing loan balance – more than the amount of cash they obtained from the refinance. In addition, the borrower also takes on higher monthly payments because the new mortgage will be for a larger amount than the prior mortgage.

We are particularly concerned that the FHA and VA share of cash-out refinances increased from 16% in January 2022 to 42% in January 2023. At the recent rate of about 13,000 FHA and VA cash-out refinance loans per month, about 160,000 of these homeowners could become saddled with more costly mortgages this year. more...

|

|

News from Washington | By Brittany Webb

|

|

|

HUD restores discriminatory effects standard

Last Friday, HUD announced it rescinded the controversial 2020 Fair Housing Act rule and restored the 2013 Discriminatory Effects rule under a new Final Rule titled Restoring HUD's Discriminatory Effects Standard. The Final Rule says the 2013 rule "is more consistent" with how courts apply the Fair Housing Act and that the Final Rule "more effectively implements the Act's broad remedial purpose of eliminating unnecessary discriminatory practices from the housing market." The Final Rule goes into effect 30 days following its publication in the Federal Register. NHC was one of many organizations that advocated for maintaining the discriminatory effects standard, previously called disparate impact. "Similarly, HUD has an existential obligation to affirmatively further fair housing through its actions and policy. Yet the proposed rule all but renders the disparate impact standard moot by establishing a near-impossible standard for plaintiffs to make disparate impact claims," a 2019 letter from NHC to then Secretary Ben Carson stated.

The discriminatory effects doctrine serves as long-standing case law to the Fair Housing Act. The doctrine addresses discriminatory policies causing inequalities in housing, including zoning requirements, property insurance, lending policies, and criminal record policies. HUD published a fact sheet alongside the Final Rule, explaining its reasoning for taking this action. Housing community advocates celebrated the announcement.

"In taking this action, HUD heeded the feedback from technology experts; top mortgage lenders; and other industry leaders, including the Business Roundtable; as well as civil rights advocates, who asked the Trump administration to re-think and pause its plans to go forward with putting the 2020 Rule in place," said Lisa Rice, president and CEO of the National Fair Housing Alliance in a statement. She added, "The Trump administration's Disparate Impact Standard Rule would have made it effectively impossible for people to challenge housing and financial services policies that might seem neutral on their face but in fact have an unfair and discriminatory impact on certain groups, like people with disabilities, families with children, women, or Native Americans. HUD's action ensures that everyone has a fair shot at the opportunities we all need to live successful lives and carries us forward on the road to justice and fairness for all."

HUD also announced it's awarding more than $54 million to 182 fair housing organizations under the Fair Housing Initiatives Program (FHIP). HUD awarded $26.35 million of this funding to the agency's second- and third-year Private Enforcement Initiative grantees to continue fair housing enforcement. HUD said the money allows grantees to enforce fair housing standards by conducting investigations, identifying rental and sales markets, and filing fair housing complaints.

|

|

|

|

|

Housing leaders raise concerns about Build America, Buy America Act's impact on affordable housing

A diverse group of 24 housing industry representatives and housing advocacy organizations sent President Biden a letter expressing their concerns about implementing the Infrastructure Investment and Jobs Act's Build America, Buy America Act (BABA) provisions. The group, led by NHC, urged the Office of Management and Budget to clarify that affordable housing development and repair, including affordable homeownership repair and development programs and HUD-assisted and USDA-assisted multifamily housing, are exempt from the BABA's requirements.

"As currently written, the proposed guidance would increase the cost of building affordable housing, reducing the number of units that can be developed using existing federal funding," said David Dworkin, president and CEO of NHC. "OMB must ensure that the important work of the Biden administration addressing the nation's housing affordability crisis is not undercut."

Adding BABA requirements as a condition of funding for HUD's programs will place an enormous administrative burden on affordable housing builders and developers, restricting the supply of necessary construction materials and further exacerbating America's housing affordability crisis.

|

|

|

|

FHFA seeks input about updating credit models

FHFA announced it's beginning a public engagement process for Fannie Mae and Freddie Mac (the Enterprises) to transition away from using classic FICO credit scores. The transition would replace the Classic FICO model with FICO 10T and VantageScore 4.0 models and move from requiring three credit reports (tri-merge) to only two credit reports (bi-merge) for single-family loan acquisitions. FHFA estimates the move to bi-merge credit reports could occur during the first quarter of 2024, and anticipates implementing the new credit score models in two phases over 2024 and 2025. FHFA estimates Phase 1 will begin in the third quarter of 2024 and include delivery and disclosure of the additional credit scores. Phase 2 will occur around the fourth quarter of 2025 and include incorporating the new credit score models into pricing, capital, and other processes. "Today's announcement highlights FHFA's commitment to stakeholder engagement as the Enterprises implement the new credit score models and transition to a bi-merge reporting requirement," said FHFA Director Sandra Thompson. "Obtaining public input in a transparent manner and considering the feedback is critical to a successful transition."

FHFA said the Enterprises are soliciting public input on the implementation process and the agency and the Enterprises will work with stakeholders to ensure a smooth transition.

|

|

|

|

|

FOMC raises target funds rate

The Federal Reserve Board's Federal Open Market Committee (FOMC) announced it is raising the target federal funds range rate a quarter point to 4.75-5 percent. The move marks the ninth consecutive rate increase as the central bank tries to address inflation; it's thee rate range's highest level since Sep. 2007. However, Federal Reserve Chairman Jerome Powell indicated Silicon Valley Bank's recent failure would likely result in some tightening of credit conditions for households and businesses and it could lead to rate tightening due to new stresses in the banking sector. Powell highlighted the situation's uncertainty and the need for additional assessment. "We no longer state that we anticipate that ongoing rate increases will be appropriate to quell inflation; instead, we now anticipate that some additional policy firming may be appropriate," said Powell during a press conference. "We will closely monitor incoming data and carefully assess the actual and expected effects of tighter credit conditions on economic activity, the labor market, and inflation, and our policy decisions will reflect that assessment."

Powell's comments caused many to predict this may be the last rate increase for some time. |

|

|

|

|

Housing funding support letters circulate through Congress

Three "Dear Colleague" letters urging support for funding affordable housing and community development programs are circulating the House of Representatives as negotiations for 2024 fiscal year spending begin. U.S. Rep. Mark DeSaulnier (D-Calif.) circulated a letter asking for a minimum of $50 million in funding for HUD's Section 4 Capacity Building Program. The letter included a request to sign on to support the funding by March 24. U.S. Rep. Joyce Beatty (D-Ohio) is circulating a letter asking for at least $2.5 billion in funding for the HOME Investment Partnership Program with a March 30 deadline to sign on to support. And U.S. Reps. Ann McLane Kuster (D-NH), Ayanna Pressley (D-Mass.), and Dwight Evans (D-Penn.) are circulating a letter requesting $150 million for the Family Self-Sufficiency program with a March 28 deadline to sign on to support. |

|

|

|

New HMDA mortgage lending data available

The 2022 Home Mortgage Disclosure Act (HMDA) data on Modified Loan Application Register (LAR) is now available for approximately 4,394 data filers, according to the CFPB. Previously, you had to request the data from specific institutions. However, the data is now available online, and users can download one combined file containing all institutions' modified LAR data. The announcement further notes that, later this year, 2022 HMDA data will be available in other forms to help provide users with further insights, including a nationwide loan-level dataset with all public data for all HMDA reporters, aggregate and disclosure reports with summarized information by geography and lender, and access to the 2022 data through the HMDA Data Browser that allows users to create custom datasets, reports, and maps. |

|

|

|

|

HUD publishes new equitable broadband access guidebook

HUD released a new guidebook to help public housing authorities, multifamily owners and operators, and indigenous tribes better understand the Broadband Equity, Access, and Deployment Program (BEAD) and the Digital Equity Act programs. The Department of Commerce's National Telecommunication and Information Administration manages both programs. BEAD will provide $42.45 billion to connect underserved communities across the U.S., and the Digital Equity programs will make available an additional $2.75 billion to provide technology devices, digital skills training, and support underserved communities nationwide. "We are committed to making sure every home has access to high-speed internet, through initiatives like HUD's ConnectHome and the Bipartisan Infrastructure Law's Affordable Connectivity Program. We are so grateful to the NTIA for their support in developing this useful resource and we look forward to the continued partnership between our agencies," said HUD Secretary Marcia Fudge.

|

|

|

|

Eviction Lab creates Zoning Restrictiveness Index

A new paper by Matthew Desmond and Matthew Mleczko from Princeton University's Eviction Lab introduces a Zoning Restrictiveness Index (ZRI) and National Zoning and Land Use Database (NZLUD). Using publicly available data, the NZLUD collects key zoning elements, including minimum lot sizes, permitted density, parking requirements, and more, to produce the ZRI, a single measure of exclusionary zoning. The ZRI ranks municipalities on a 1 to 5 scale, with 1 equaling the least restrictive area and 5 the most. The ZRI shows the metropolitan statistical areas with more permissive zoning and showcases exclusionary suburbs within otherwise permissive areas, like those around Houston. |

|

A BuzzFeed News article examines how companies market credit cards to Gen Z by promoting paying rent with credit cards. Credit cards such as Bilt and Plastiq allow consumers to charge their rent payments and earn rewards while waiving the standard fees associated with credit card payments. Some Gen Z adults say the system helps them reap the benefits of credit card rewards, while others are skeptical about adding to their existing debt.

An article by The New York Times tells the story of a Black landlord who experienced discrimination when an appraiser evaluated his property, occupied by tenants who are also Black, as worth $359,000 while the landlord's lender said the property was worth $500,000. In addition, the article points out that 97 percent of appraisers are white, highlighting ongoing appraisal bias that impacts property owners of color.

A USA Today article examines how the Federal Reserve's rate increases over the past year have impacted the housing market. The analysis begins with the pandemic-era competitive housing market when home prices rose 40 percent over two years. It continues through the ensuing rising mortgage interest rates as the Fed looks to battle inflation. |

|

Monday, March 27

Tuesday, March 28

Wednesday, March 29

Thursday, March 30

Friday, March 31

|

|

The National Housing Conference is a diverse continuum of affordable housing stakeholders that convene and collaborate through dialogue, advocacy, research, and education, to develop equitable solutions that serve our common interest. |

|

Defending Our American Home since 1931 |

|

Copyright © 2022. All Rights Reserved. |

|

|

|

|

|

|