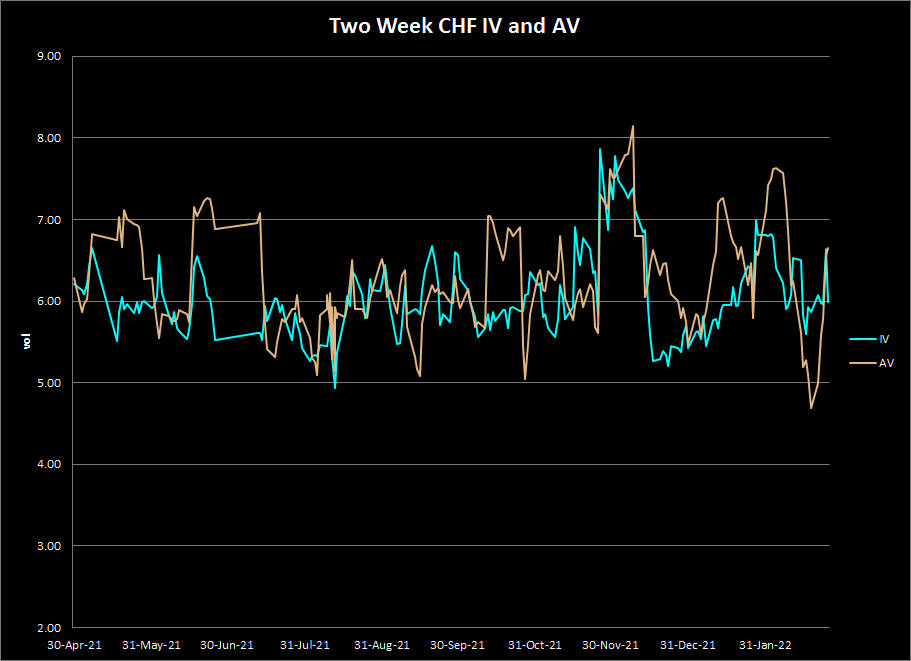

While not showing up as a "buy" on our percentile rank model, the short-dated CHF implied vols do look attractive both on a relative value basis (compared to other FX pairs in our database) but also on the basis of IV-AV spreads. The market is assuming that USDCHF vol will be damped down by movements in EURCHF and this may well be true on further EURCHF sell-offs but it is unlikely to be the case should EURCHF find a meaningful bottom. This has two implications. First, if you are a good to confident delta hedger the short dates look attractive, and second, if we do start to see a credible bottom in EURCHF then USDCHF should start to move higher. The other opportunity we will look for (at the moment we do not have enough evidence to support this) would be to structure a longer-dated EURCHF Condor structured to the upside. This is a trade for another day in our view but now, it is an idea that should be noted and filed for review once we get confirmation from other signals.