Weekly update from the National Housing Conference |

|

In this issue,

May 7, 2023

Issue 92-16

· Bipartisan bill seeks to improve rural housing

· Housing Trust Fund allocates $382 million for affordable housing

· CFPB seeks to establish clean energy protections

· FOMC raises target funds rate by 25 basis points

· Casey introduces accessible living legislation

· Witnesses call for greater investment, focus on Native American housing

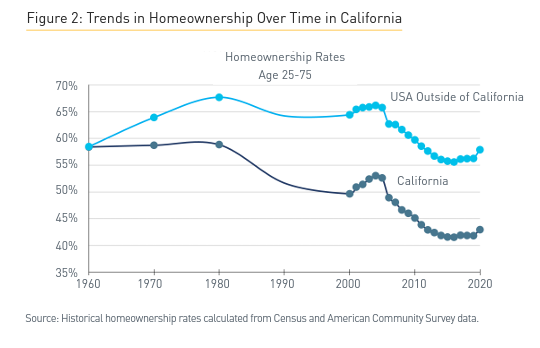

Chart of the week: California homeownership rate diverges from the rest of the country’s

|

|

It's time for a coherent policy on mortgage pricing

By David M. Dworkin

As I wrote about last month, housing policy has been thrust into the center of the culture wars. It's disheartening to witness bipartisan support for expanding homeownership, a cornerstone of the American Dream, devolve into a heated debate over “wokeness.” This unwarranted escalation detracts from the real issues at hand and should not continue. We need to have a serious, fact-based discussion of how we price government-sponsored mortgages, like those purchased by Fannie Mae and Freddie Mac, as well as those insured and guaranteed by the U.S. government, like those by the Federal Housing Administration (FHA)/Ginnie Mae.

Together, these two channels make over 70% of the mortgage market and present different types of risk to borrowers, investors and taxpayers. It’s worth getting right. The Federal Housing Finance Agency (FHFA) should lead this discussion among the broadest possible range of stakeholders and revise the pricing grid to maximize the fairness, safety, and soundness of government mortgages. The approach also needs to be transparent and easily understood.

One of the arguments made by opponents of the recent changes put in place by FHFA effective May 1 is that they penalize people who have better credit, or put more money down on a mortgage. Because the debate on this issue is dependent on the interpretation and comparison of highly complex mortgage pricing grids, it’s easy to mix fact and fiction without being intentionally untruthful.

Under the new pricing grid, the fact is that no one with the same downpayment and a higher credit score will be charged more than those with a lower credit score. It’s also true that under the new grid, no one who makes a higher downpayment will pay more than someone who makes a smaller downpayment, given the same credit profile. However, some of those who make a higher downpayment will be charged a slightly higher Loan Level Pricing Adjustment (LLPA) fee than those with the same credit profile who put less money down.

Wait a minute! Didn’t I just say the opposite? No. The difference is that when mandatory mortgage insurance is factored into the equation, the person with the higher downpayment won’t actually pay more than the one with the lower downpayment. This is why I have strongly defended FHFA’s effort to reduce fees on higher downpayment loans while also noting that critics are correct when they suggest that the charge is not risk-based pricing when higher-risk loans are charged less than lower-risk loans. Risk-based pricing like this is always going to treat someone unfairly because the current approach, instituted in 2009, is always going to be unfair to someone.

I believe the answer is to get rid of the LLPAs altogether. Many of my colleagues in the mortgage industry agree with me while others don’t. This is a discussion we should have with our nerdy charts at the ready, not in op-eds, soundbites, or talking points for lobbyists. more...

|

|

News from Washington | By Brittany Webb

|

|

|

Bipartisan bill seeks to improve rural housing

Sens. Tina Smith (D-Minn.) and Mike Rounds (R-S.D.) introduced bipartisan legislation for improving federal rural housing programs, titled “Rural Housing Service Reform Act of 2023.” The bill considered feedback from public hearings and stakeholder input to modernize and update rural housing services and programs. If passed, the legislation will make it easier for nonprofits to acquire Sec. 515 properties with maturing mortgages, decouple rental assistance from sites so the aid can remain after mortgages mature, make permanent a pilot program that makes mortgages available in Native communities through local community development financial institutions, bring USDA’s income measurements in line with HUD’s, and make other updates to cut through red tape and speed up processing. “Homeownership is part of the American dream and a key to building wealth,” said Rounds. “Over the past year, Senator Smith and I have held hearings, met with stakeholders and visited with constituents in our states about the hurdles within the U.S. Department of Agriculture’s Rural Housing Service. This legislation makes important improvements and updates to the Rural Housing Service that will create and preserve affordable housing opportunities in South Dakota. As we face an affordable housing crisis across the nation, I look forward to working with my colleagues to get these important, bipartisan updates signed into law.” The Senate Committee on Banking, Housing, and Urban Affairs also held a hearing discussing the bill. The hearing, titled “Rural Housing Legislation,” included as witnesses Natalie Maxwell, managing attorney at the National Housing Law Project, Christopher Potterpin, president at the Council for Affordable and Rural Housing, David Lipsetz, president and CEO at the Housing Assistance Council, Dianne Hunt, president at Syringa Property Management, and Anne Manity, executive director at Minnesota Housing Partnership. “Given this policy landscape, HAC is very pleased to see the bipartisan effort that has gone into the Rural Housing Service Reform Act of 2023. This bill makes commonsense improvements to critical RHS programs, authorizes and builds on the success of pilot programs and demonstrations, and offers a host of provisions that are ripe for inclusion in cross-Committee collaboration in the 2023 Farm Bill,” said Lipsetz in his testimony. The bill includes many of the Housing Assistance Council’s recommendations. |

|

|

|

|

Housing Trust Fund allocates $382 million for affordable housing

HUD announced the allocation of $382 million through the Housing Trust Fund (HTF), an affordable housing production program for extremely low- and very low-income households. The formula-based program allocates $3 million per state. State affordable housing planners can apply the money to eligible activities, including administrative and planning costs, site improvements and development hard costs, demolition, relocation assistance, and more. “The Biden-Harris Administration is committed to improving the nation’s housing affordability crisis and the Housing Trust Fund provides communities resources they need to produce more safe, sustainable, and affordable housing,” said HUD Secretary Marcia Fudge.

|

|

|

|

|

CFPB seeks to establish clean energy protections

The CFPB proposed a new rule that would create a congressional mandate to establish consumer protections for residential Property Assessed Clean Energy (PACE) loans that are offered to finance clean energy improvements on homes. Typical enhancements include adding solar panels or energy and water efficiency upgrades. Homeowners pay the loans back through increased property tax payments over time. The proposed rule would require assessing a borrower’s ability to repay and provide a framework for how loans will be treated under the Truth in Lending Act. CFPB also published a new report finding that PACE loans caused some increases in borrower mortgage delinquency. “When unscrupulous companies bait homeowners into unaffordable loans with exaggerated promises of energy bill savings, this can lead to serious financial distress,” said CFPB Director Rohit Chopra. “We are proposing new rules that would require sensible safeguards on these clean energy loans.”

|

|

|

|

FOMC raises target funds rate by 25 basis points

The Federal Reserve Board’s Federal Open Market Committee (FOMC) increased interest rates by 25 basis points, bringing the target range to 5 to 5.25%. It’s the FOMC’s tenth straight rate increase as it attempts to curb inflation, bringing the target range to its highest level since 2007.

NHC President and CEO David Dworkin called for the FOMC to stop raising rates. “Raising interest rates further to control inflation is no longer the answer and is instead contributing to an increase in the cost of shelter. The FOMC needs to let the economy absorb the previous rate increases while we focus on increasing housing supply to address skyrocketing shelter costs,” Dworkin said. In a statement to National Mortgage News, Dworkin said, “The FOMC’s indication it may step back from taking further action will not address the affordable housing shortage in the country that has been exacerbated by inflation. We need the Administration and Congress to address the critical need for affordable housing in this country and move forward with actions and policies that will increase our nation’s housing supply.” The article noted NHC’s call on Congress to pass both the Neighborhood Homes Investment Act and the Affordable Housing Credit Improvement Act. |

|

|

|

|

Casey introduces accessible living legislation

Sen. Bob Casey (D-Penn.), chairman of the U.S. Senate Special Committee on Aging, introduced a bill titled “ Visitable Inclusive Tax Credits for Accessible Living (VITAL) Act” that seeks to address housing affordability and accessibility issues for people with disabilities. The announcement notes that by 2060, one in four Americans will be over the age of 65 and that two in five adults over 65 have a disability. The bill would increase funding for the Low-Income Housing Tax Credit (Housing Credit) program and further ensure that developers are building accessible housing units by requiring at least 40% of units to be adaptable or accessible for people with disabilities or require only 20% of the units if they are in walkable or rollable areas. The bill’s cosponsors include Sens. Tammy Duckworth (D-Ill.), Kirsten Gillibrand (D-N.Y.), Amy Klobuchar (D-Minn.), and Peter Welch (D-Vt.). “Anyone living with a disability deserves equal access to housing that accommodates their needs, is affordable and provides a safe environment for them to thrive,” said Duckworth. “We must do more to make sure Veterans, seniors and people with disabilities can live the full, independent lives they deserve, which is why I’m proud to help Senator Casey introduce this bill to help make that a reality.” |

|

|

|

|

Witnesses call for greater investment, focus on Native American housing

The House Appropriations Subcommittee on Transportation, Housing and Urban Development, and Related Agencies, held a hearing titled “Tribal Perspectives on Housing and Transportation” to discuss the unique challenges and opportunities in tribal housing and transportation. In his opening remarks, Subcommittee Chairman U.S. Rep. Tom Cole (R-Okla.), an enrolled member of the Chickasaw Nation and whose state has 39 sovereign tribes, stated that “in some ways this is a somewhat historic hearing…even though HUD and DOT have important long and important relationships with us and tribes, we’ve never had a hearing here with that portion of our budget.” Witnesses included Gary Bohnee, special assistant in the office of congressional and legislative affairs for the Salt River Pima-Maricopa Indian Community, Barbara Little Owl, executive director of the Standing Rock Housing Authority, Tonya Plummer, director of Native American housing programs for Enterprise Community Partners, Leo Sisco, chairman of Santa Rosa Indian Community of the Santa Rosa Rancheria Tachi-Yokut Tribe, Russell Sossamon, executive director of Comanche Nation Housing Authority, and Alex Wesaw, treasurer of the Pokagon Band of Potawatomi Indians. All witnesses underscored the need for increased investment and focus on Native housing, saying Native Americans experience a shortage of affordable homes and higher rates of substandard homes and overcrowding. Plummer told the committee, “Our Tribal structure is focused on the family, which is built around the home. A stable home is a cornerstone of social, emotional, spiritual, and economic stability. Housing is economic development.” |

|

|

|

California homeownership rate diverges from the rest of the country’s

The Terner Center for Housing Innovation at UC Berkeley published new research examining California's homeownership erosion. The report explores why homeownership is increasingly out-of-reach for California residents compared to the greater U.S. Before 1960, California’s homeownership rate nearly matched the rest of the country’s but has been diverging since. The paper notes that in 2021 the share of adults who own a home in California was 43.5%, nearly 15 percentage points lower than the U.S. homeownership rate and the largest gap in history for the metric. |

|

NHC President and CEO David Dworkin was a guest on the podcast On the Hill hosted by Tim Rood, where he spoke about policy solutions and regulatory reforms needed to address the housing affordability crisis. Dworkin touched on simplifying the structures of housing programs, streamlining the mortgage financing system, and addressing exclusionary zoning at local levels. He noted the importance of being thoughtful about our new policies and learning from our past mistakes.

Politico published an article examining creation of the modern unemployment rate and suggests that the U.S. should establish and track a “National Housing Loss Rate.” The article says you cannot fix something you can’t measure. And it argues that if the country wants to tackle homelessness, it must start tracking the number of people who lose their homes each year, especially as the housing supply continues to fall short of demand and contributes to high housing costs.

An NPR article tells the story of Cook Medical, a company in Indiana that built homes to sell to their employees at below-market prices a year ago. The article describes a form of employer-assisted housing, an increasingly interesting topic for employers who want to ensure their employees can afford to live near their work. Cook Medical is creating a subdivision of 99 homes priced between $188,000 and $212,000. Doing so should help Cook Medical employees attain homeownership, which is difficult to do where the company operates due to a lack of affordable housing supply. A Forbes article interviews leaders of four key housing agencies, HUD Secretary Marcia Fudge, FHFA Director Sandra Thompson, Ginnie Mae President Alanna McCargo, and FHA Commissioner Julia Gordon. The article highlights that for the first time in U.S. history, women hold each of these positions, which oversee the country’s housing markets. Each was interviewed to understand how they plan to navigate the difficult housing market and the challenges ahead. |

|

Saturday, May 6

Sunday, May 7

Monday, May 8

Tuesday, May 9

Wednesday, May 10

Thursday, May 11

Friday, May 12

|

|

The National Housing Conference is a diverse continuum of affordable housing stakeholders that convene and collaborate through dialogue, advocacy, research, and education, to develop equitable solutions that serve our common interest. |

|

Defending Our American Home since 1931 |

|

Copyright © 2023. All Rights Reserved. |

|

|

|

|

|

|