According to Refinitiv LPC, US unitranche volume came to almost $22 billion last quarter – the highest level they’ve tracked historically. That activity was comprised of records for both the middle and the larger corporate markets.

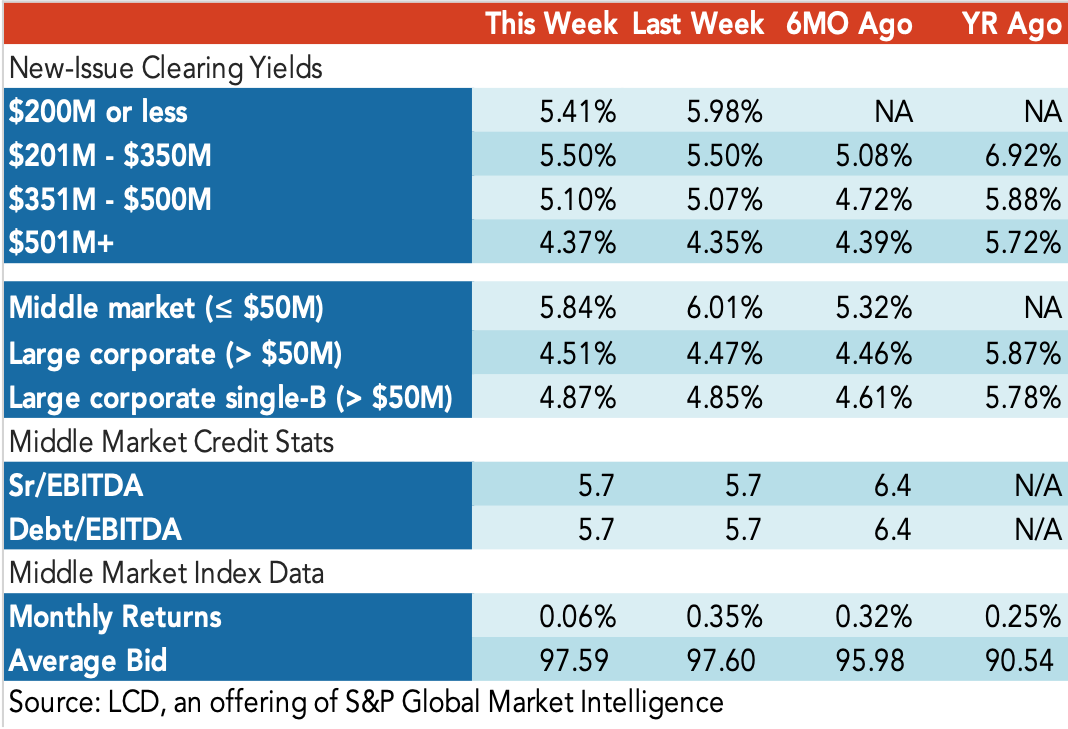

At the same time, one-stop risk/return dynamics have moved in favor of issuers. The average debt/ebitda is now at a record high 5.9x, with all-in Libor spreads hovering around 600 bps.

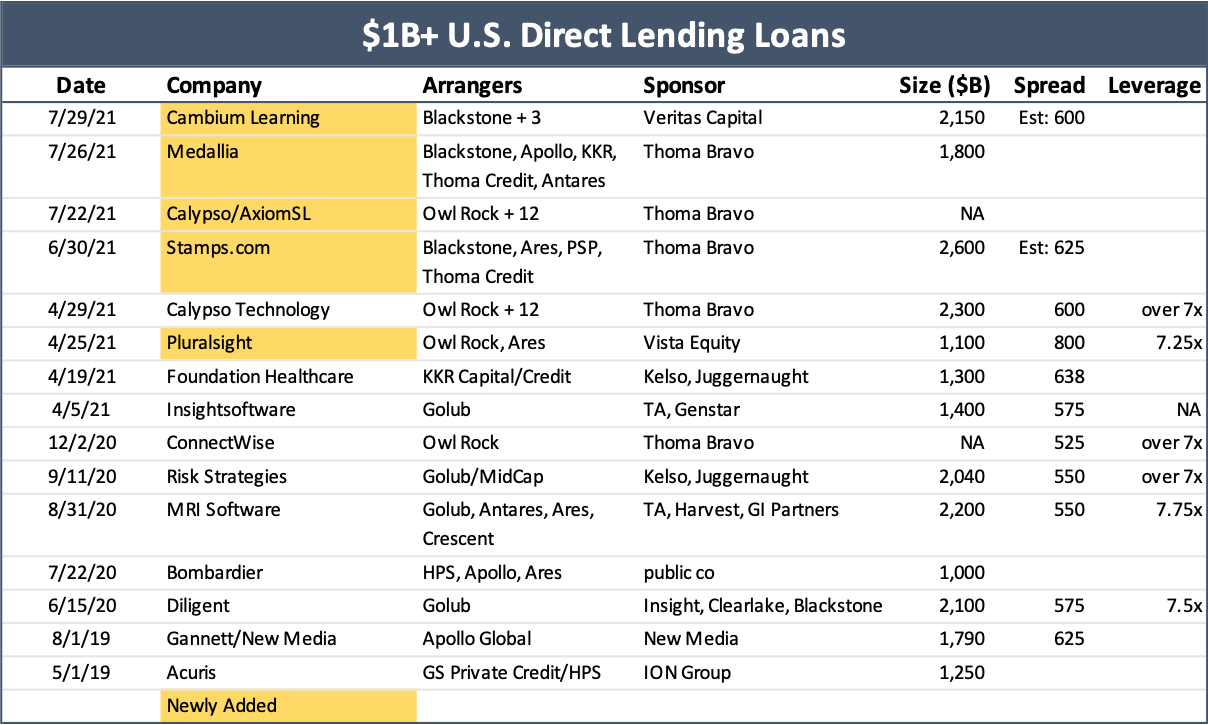

And as we mentioned last week, more $1 billion-plus unis are coming to market than ever. So what are the drivers behind the frothy market for this innovative financing?

Here’s what we told M&A magazine in a recent interview:

“The disintermediation away from the loan syndication market to private credit, particularly for the upper end of the middle market...