|

RETIREMENT SECURITY MATTERS

A forum for retirement innovation information sharing focused on

states, supporters, and service providers.

Vol 58 | July 21, 2022

| | |

Greetings! Lisa, welcome to Retirement Security Matters – where we talk about retirement readiness innovation by the public sector, private sector, and policy organizations. | |

We love summer! In between work days and getting things done, we hope you’re enjoying the sun where you are. Grab a lemonade. We’re here to catch you up on the world of retirement security, and just a bit more:

-

Will Sandbrook on Nest UK, age ten.

- Frrreshhh state metrics

- Updates from California, Colorado, Illinois, Maine, New Mexico, and Hawaii.

- Can tuning your design lead to better user outcomes? Behavioral scientist Perry Wright opines.

-

Hot Sauce! … new research from our esteemed friends across the US.

- And, PIX of the Week! – we’re taking you outdoors and to the beach 🌅

| Comments or content suggestions? We welcome both. Have something about your program you’d like to share? We are all ears. | |

|

RSM wants your support! Be seen here.

Click for more information.

| |

When Ten is a “10”: Auto-enrollment

in the UK paves the way

| |

|

We’re excited to talk with our friend Will Sandbrook for several reasons. One, he’s been with Nest Corporation (UK) since it started. Ten years on, we want to know what he sees. Two, Will is Managing Director of Nest Insight, Nest’s in-house research and thought leadership unit focused on delivering cutting-edge research into how to improve retirement outcomes for the ‘DC generation.’ We always want to know what’s fresh news where he is. Among other initiatives, we touch on new results from the emergency savings space. Almost everything that’s going on in the UK is, or will soon be, very relevant to us in the US. You can see more of Will’s impressive credentials below, and join our conversation here.

| |

Will Sandbrook – we are now at the Nest ten-year mark. That was fast. What’s been the impact of Nest and its related legislation in the UK?

You’re right – the impact here is both the ten-year anniversary of Nest, and the ten-year anniversary of the auto enrollment mandate in the UK.

More savers. The UK's gone from hovering at under half of workers saving for their retirement to something like 80% of workers saving for their retirements.

Extended market reach. Now we have a low- and moderate-income mass market concept that makes auto enrollment work right down to the smallest employers, the lowest income workers, and the people who are shifting in and out of multiple jobs through the year.

Nest has really been the supply-side piece that has made the demand-side intervention of auto enrollment work for everybody. (Much more about Nest here).

To use a fun phrase, you’ve now got "universal workplace savings" in the UK.

Absolutely. I’d say universally available and almost universally participated in. There are 10 to 11 million more people saving for their retirement than there were before.

You're passionate about emergency savings. What are some of the most useful things you're seeing out of the work you've done so far?

Yes, there are two important stories that are emerging in our work:

At the macro level, we started out trialing voluntary opt-in emergency savings tools in various workplaces. At the micro level as we do more qualitative and quantitative research with the people in these pilots, we're getting a much clearer handle on different ways people are using their accounts.

(What! Tell us more – you’ll find the non-excerpted version of this piece here. You can also join the recorded version of Nest's May 15 2022 Emergency Savings Summit.)

Will, final question! What do you see as the next iteration of both automatic enrollment and savings in the UK?

Let’s start with auto enrollment. There are a couple of big debates at play in the UK. One is around our £10,000 threshold. Workers earning below this level are not automatically enrolled. Should the level be changed, removed, or lowered to bring more people in? The debate is occurring with a particular eye on part-time workers, who tend disproportionately to trend female. And therefore that £10,000 limit is seen as contributing to significant gender pensions gap in the UK. It also recognizes that people who have multiple sources of income where no single job pays them over £10,000 may be falling through the net multiple times, but actually maybe earning enough for it to be very sensible for them to be saving for retirement. So that's debate one. Debate two is contribution rates.

(Continued HERE! Don’t miss the rest of Will’s essential insights)

Thank you, Will.

Will Sandbrook is the Managing Director of Strategy, Analytics and Nest Insight at Nest. He has spent 20 years working in strategy, public policy, research and communications roles relating to personal finance and pensions, including working for the UK government on financial inclusion policy and the design and implementation of their landmark automatic enrolment programme.

Want more? You can connect directly with Will by email here. You can sign up here to receive updates from Nest Insight. Connect on Twitter @NESTInsight. You can also zip through the recent Nest Insight Conference on YouTube, here, and peruse some excellent Nest Insights research here.

| |

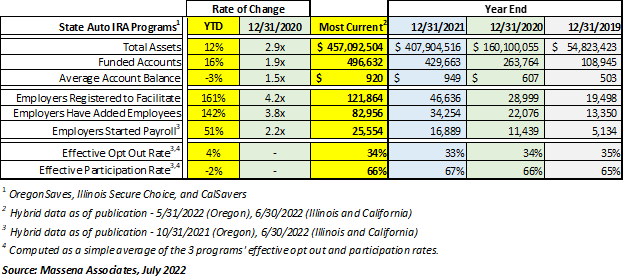

*Fresh!* State Auto IRA Program Metrics | |

|

What we see: June figures are rolling in. Year-to-date figures show strong growth across the board, with assets steady after cash flows as experts predict a choppy back half for the investment markets for the rest of 2022.

Highlights: Across the three programs, we now see over 496,000 funded accounts. For comparison, funded accounts are up 16% this year so far, up 1.9x since December 2020 and up about 4.6x since December 2019. Over 121,000 employers are now registered to facilitate a state Auto IRA program, and we foresee this to increase with CalSavers’ recent milestone, passing the mark of 100,000 employers registered.

Saver assets are up 12% year-to-date and 2.9x since December 2020. Average account balances declined a bit at $920, to be expected when new funded accounts surge. Note that these include the newest accounts for participants who have just begun saving. In Oregon, average account balances were over $1,300 as of the end of May. Finally, effective opt out rates are up slightly, to December 2020 levels.

| |

State Facilitated Retirement Programs - Fresh Highlights | |

|

California (workforce 19 million) – As expected, with CalSavers’ Wave 3 employer deadline recently passed, the program has reached a milestone with more than 100,00 employers registered, supporting over 275,000 savers. *Well done California!* Expect to see a significant uptick in funded accounts and assets between now and the end of the year as new participants come online and begin saving.

For more about the latest milestone, the effect the program has already had on workers and employers alike, and what may be ahead for the program in the coming months, check out PLANSPONSOR’s recent article. Payroll provider ADP commented recently as well.

| |

|

Colorado (workforce 3.2 million) – The Colorado Secure Savings Program Board held a rulemaking hearing on July 20, 2022 to review and accept public comment on the proposed rules governing the program. You can get your copy of the rules here.

| |

|

Illinois (workforce 6.2 million) - The Illinois Secure Choice Board re-awarded a contract to Marquette Associates, Inc. for investment consulting services for the program.

| |

|

Maine (workforce 677,000) – The Maine Retirement Savings Board met for the third time on July 20, 2022. The agenda included an update from Executive Director Search Subcommittee, and a presentation on common best practices and recommendations on program implementation. The agenda also included the potential for a number of motions including the election of Chair and Vice Chair, and permission to issue a set of RFIs/RFPs (private insurance; financial advisor; program administrator; investment manager; and investment consultant).

| |

|

New Mexico (workforce 1 million) – The New Mexico Work & $ave Board met on July 7, 2022. The agenda included a summary report from Executive Director Claudia Armijo on the status of New Mexico and Colorado interstate partnership, update on the Marketplace Consultant, as well as upcoming education and outreach efforts.

| |

|

Hawaii (workforce 647,000) – Ho'omaika'i 'ana! On July 12, 2022, Governor David Ige signed SB3289 establishing the Hawaii Retirement Savings Program. The program is intended to cover over 215,000 workers whose employers do not offer retirement savings plans.

As a refresher, the bill includes incentive funding of $25 million – intended to be used as a match of $500 to the first 50,000 contributing savers. This funding is a targeted effort on the part of the state to expand the level of retirement savings and financial security in the state, particularly amount populations that have not have access to work-based savings previously.

| |

|

C O M I N G U P

Join where you’d like, and count on us to follow these meetings for you:

-

California (workforce 19.0 million) –The next meeting of the CalSavers Board is scheduled for August 22, 2022.

-

Oregon (workforce 2.1 million) – The next meeting of the OregonSaves Board is scheduled for August 30, 2022.

-

Maryland (workforce 3.1 million) – The next meeting of the Maryland$aves Board is scheduled for September 12, 2022.

| |

Laying the Groundwork for More than a Nudge | |

|

Behavioral science is a popular topic. We want to know: can tuning our designs lead to better user outcomes?

In this edition we bring you the experts from Common Cents Lab sharing what they are observing about personal finance. We think this is news you can use.

| |

|

|

Here at Common Cents Lab we have the privilege of working with research and industry partners committed to improving the personal financial outcomes of their low- to moderate-income users, members, or clients using behavioral science. It’s challenging, rewarding work, and deeply affirming to partner with so many organizations dedicated to these material outcomes.

When a partner wants to improve financial health outcomes for their users, we collaborate with them to design an intervention, so that we can test what works best. A lot of times, partners arrive with a handful of competing ideas already in mind for improvements, and the results of an experiment give everyone confidence before a partner rolls out changes across their entire platform.

We most often begin designing an intervention by analyzing the current situation. Identifying the ways in which users are performing actions counter to your program assumptions, what we sometimes call misbehaviors, is one of the first steps in understanding how you can intervene to serve them more effectively.

Intention-action Gap. As you conduct this initial review, you may uncover what behavioral science calls an intention-action gap: users enter a decision-making environment or process with specific intentions and those outcomes are not fully realized due to an inability to follow through on those intentions. Large spans of time between steps or unclear expectations that require deep user attention can promote these intention-action gaps.

Here are some examples of what I mean:

| |

After Design Changes, What Next? We haven’t even begun to map out the constellation of cognitive and behavioral biases that influence user decision-making for retirement, but this lays the foundation to put additional insights from behavioral science to work.

Over the next few installments, we’ll cover a few of the most important of these biases, starting with the power of defaults and the influence of anchoring.

Stay tuned for more! / Perry

Perry Wright is a Senior Behavioral Researcher at Duke University's Common Cents Lab, using behavioral science to create solutions that aim to increase the financial well-being for low- to moderate-income people living in the United States and abroad. The Common Cents Lab is funded by the MetLife Foundation and supported by BlackRock as part of BlackRock's Emergency Savings Initiative. For more information and to connect directly, you can reach Perry by email here.

| |

|

Did you notice? We’ve gone tri-weekly. We’re still giving you the excellent content you love, just s-t-r-e-t-c-h-i-n-g things out a bit over these sultry summer months. By the way, do you love Retirement Security Matters? We’d love to see your firm as a sponsor. Our rates are excellent and you get yourself in front of the most important eyeballs in the space. Drop us a note to learn more. We won’t bug you. We will send you the rates.

It looks like men, as a group, are working a little longer than they used to. Is the Social Security full retirement age of 67+ a factor? Check out this new research from our esteemed friend Dr. Alicia Munnell, How to Think about Recent Trends in the Average Retirement Age. Short for time? Find the top line here.

The answer seems obvious, but we always like evidence. Are confident retirees happier than others? The work of DCIIA’s Retirement Research Center says “yes.” Does it matter whether you are married or single, male or female? These are Research Minutes so a quick peek will tell you what you need to know.

We agree. If you like work-based access to savings, you may want to check out AARP’s new fact sheet, Payroll Deduction Retirement Programs Build Economic Security. “Having access to a retirement plan at work is critical for building financial security later in life. And we know people are much more likely to save for retirement if they can do so automatically through their paycheck,” says Debra Whitman, AARP’s Executive Vice President and Chief Public Policy Officer.

As a transition between the last and the next item, you can also investigate how women are faring in retirement. Findings: “In this RRC study, gender disparities were substantial and persistent.”

Women Working in Retirement Savings. This is so important. We joined this WIPN event (We Inspire. Promote. Network, fka Women in Pensions Network) to learn more about the 2022 perspective on trends facing women in the retirement savings industry. We’re sneaking you in to the recorded replay. Don’t miss it. Link here. Access passcode: b^19JYj0

| |

From WIPN: On June 23, WIPN released the highlights from its 2022 research findings on women in the retirement workplace. Hosted by members of the project team – Jen Mulrooney, WIPN’s Vice President, Lindsey Dickman of Escalent and WIPN’s Atlanta co-chair, Theresa Conti, WIPN’s Head of Programming & Research, and Daniella Moiseyev, WIPN’s Washington DC co-chair, we discussed the overall progress, trends and research process that we will dive deeper into throughout the year. Learn how the research project came to life and the study highlights for members, sponsors, and advocates of WIPN. The groundbreaking study was supported by our research partner, Escalent, and our research sponsors, CUNA Mutual Group, Columbia Threadneedle, Paychex, Fidelity Investments, and OneDigital and our collaborating sponsor, DCIIA. | | |

|

Fees matter. When leaving their employer, many people choose to roll 401(k) savings to an IRA in the same mutual fund. Wouldn’t you know it, retirement plan fee differentials add up. Yipes! A recent brief by The Pew Charitable Trusts examines the difference between institutional and retail class annual expenses across mutual funds that offered at least one institutional and one retail share class. Their headline says it all: Small Differences in Mutual Fund Fees Can Cut Billions From Americans' Retirement Savings.

Also on Our Minds 💡.

What do you think of Carbon Savings Accounts – like HSAs, only different? We think it’s an intriguing idea and one whose time should come! Check out the great thinking of our friends Lizzy Kolar and Kaitlyn Highstreet at Scope Zero. Wouldn’t it be great if there were a tax break for this sort of forward thinking savings?

When we’re not reading our friends’ websites we are following the history of American Presidents. This season it’s Teddy Roosevelt. We’ve gone for the long form, three book biography. Stephen Floyd has the best blog about presidential biographies and steered us to Edmund Morris. We’re cruising our way through The Rise of Theodore Roosevelt. To be honest, the book’s prologue focuses on 1907, at which point he had risen pretty far. We’re looking forward to digging into the details of this curious, energetic guy. Danger, high likelihood of pithy quotes ahead.

| |

... We're patient, but give us some PIX! | |

Will Sandbrook, thank you for bringing us in! The world must be growing more normal if we can catch up in Paris for selfies without masks. Here’s Will joining a former colleague for a few minutes of catch-up time on the continent. | |

Below, at left: “Enjoying the British heat wave with an evening picnic with my kids.” And at right: “Pondering the work to be done serving on the food stand at my son’s school fair.” ♥️ You’ve got this, Will! Looks delicious. | |

Across the pond, where in the world are we? Just a hint, in traversing to here from Oregon we were able to log time in three states we’d never visited before: Louisiana, Mississippi, and Alabama. | OK, you’re right. It’s Florida. Did we eat all of that food? Yes, yes we did. And then we sucked in our belly for this great golden hour family photo. Our kids are growing up! | |

|

That’s it for this edition. ❤️ Hug your people and change the world.

If you like this piece, please stick with us. We’ll be back in about two weeks. If you don’t like it, please unsubscribe below. Comments for us? Please let us know. Want your own subscription? Request one here. All information shared is from public sources or used with express permission.

| |

Massena Associates provides process, policy, and implementation consulting on retirement savings programs and products.

Our clientele includes public entities, policy organizations, and private sector providers. Our specialty – efficient, targeted results. We are an active speaker on retirement security topics, including state-facilitated programs, MEPs and more.

If you’d like to explore working together, we welcome the conversation. Connect with us here, and at 339-236-0684.

| |

|

Looking for a great retirement savings innovation resource? Led by Dr. Alicia Munnell, the Center for Retirement Research at Boston College develops and hosts terrific content and proprietary research related to states, financial security, social security, and more.

The Georgetown Center for Retirement Initiatives, Exec Angela Antonelli, provides excellent information on state-based and other retirement security innovation and policy.

Pew’s Retirement Savings Project studies the challenges and opportunities for increasing retirement savings and is another great resource - check out the work of John Scott and his terrific team.

If you want a great source of broad-based, consumer-focused retirement news, Jeffrey H. Snyder’s The Morning Pulse is your ticket. You can subscribe here.

| | | | | |