(Editor's Note: Rarely do we come across an article that takes such an in depth and critical look at the antics of the Class One railroads, while exposing their behavior and the lies of Precision Scheduled Railroading so plainly for all to see. Please read this article. We commend the author and the magazine!) |

|

This magazine - The American Prospect - devoted the entire February issue to the subject of the broken supply chains. Check out the entire issue and all of the articles below...

|

|

Featured Article:

How America’s Supply Chains Got Railroaded

|

|

Rail deregulation led to consolidation, price-gouging, and a variant of just-in-time unloading that left no slack in the system.

|

|

When the Union Pacific Railroad closed its Global 3 Intermodal Ramp outside of Chicago in 2019, Union Pacific marketing executive Kenny Rocker promised that closing the facility would bring “more consistent, reliable and predictable service” to shippers who depend on rail. Union Pacific was cutting costs by consolidating its unloading facilities in Chicago, a national center of transshipment for goods that come by rail from ports.

Two years later, as the supply chain crisis gripped the country, the railroad had to abruptly reopen Global 3. In the meantime, Union Pacific stopped service between the all-important shipping hubs of Los Angeles and Chicago for one week last July while the company reconfigured its operations. Union Pacific’s remaining facilities in Chicago couldn’t keep up with the volume, nor could Union Pacific find enough workers or equipment to handle the goods. Industry analyst Larry Gross told Trains.com that Union Pacific “sacrificed surge capacity” when it closed Global 3. “If you don’t have any additional capacity in your hip pocket, even moderate disruptions put you in a world of hurt.” Gross estimated that Union Pacific’s weeklong suspension of service would keep roughly 40,000 containers stranded on the West Coast.

Every other major railroad suffered from supply chain snags in 2021. Another overwhelmed rail company, BNSF, ordered a slowdown of shipments into its Chicago facility. Two other remaining large rail companies, Norfolk Southern and CSX, received sharply worded letters from the head of their primary regulator, Surface Transportation Board Chairman Martin Oberman. In his letters, Chairman Oberman asked each railroad to respond to complaints from shippers—across different types of goods—of worsened service delays and higher costs.

But the freight railroads’ poor operational performance has not impaired their spectacular financial performance. If anything, the bottlenecks create more pricing power. Less than a week after his company reversed its 2019 decision and reopened Global 3, Union Pacific executive Rocker optimistically predicted on an earnings call that Union Pacific would be able to “take some pretty robust pricing on the market”—in other words, keep its prices high. The stock market shared Rocker’s optimism for all Class I railroads, whose stock prices rose in 2021, many by 20 percent or more. The last year was one more of a decade of financial prosperity for the industry as the stock price and total return of every publicly traded Class I railroad from the end of 2011 to the end of 2021, except for Canadian National, grew faster than the S&P 500. Union Pacific earned the second-highest total return in that period, getting investors an almost sixfold return on their money and beating the S&P 500 by over 100 points.

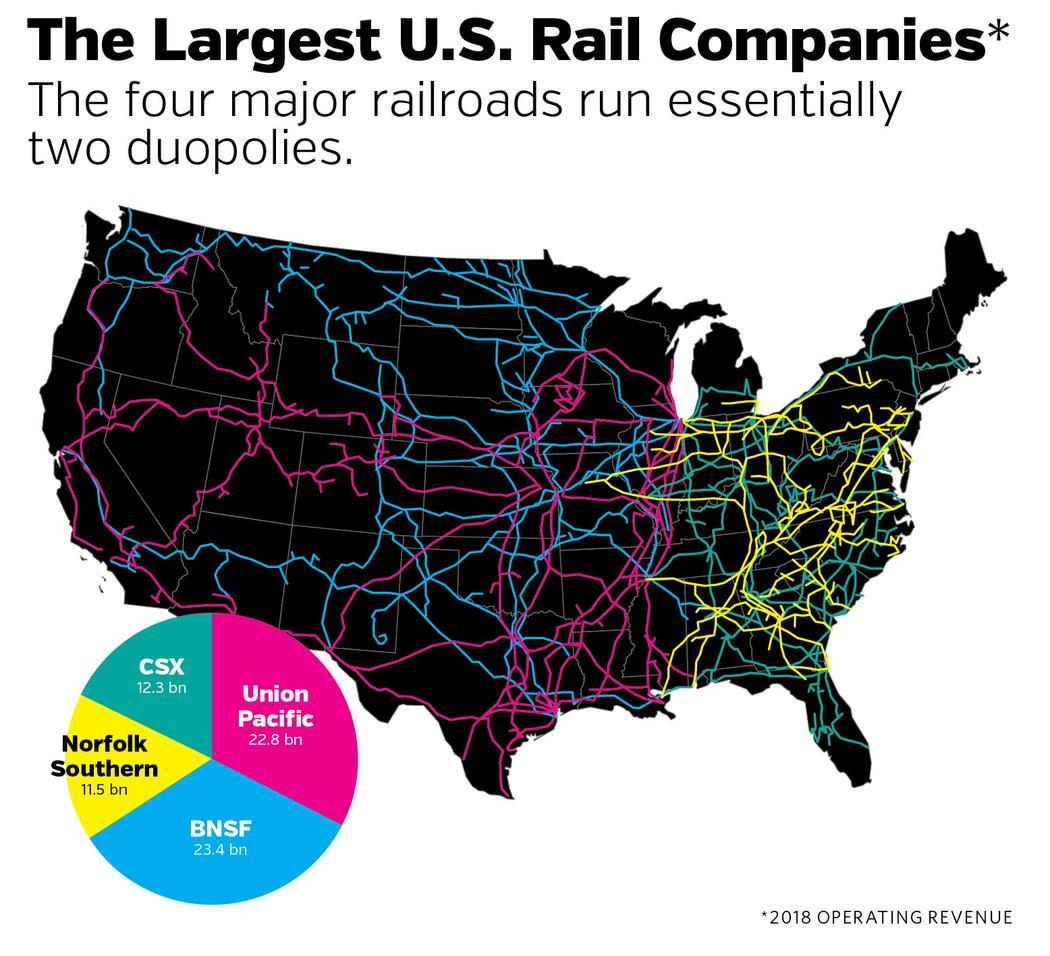

THE RAIL SUPPLY CHAIN CRISIS was decades in the making, based on two fundamental sources—excessive consolidation and the railroads’ version of just-in-time, called precision scheduled railroading (PSR). In 1980, at the dawn of rail deregulation, there were 40 Class I railroads. Today, there are just seven. Of those seven, four have 83 percent to 90 percent of the freight railroading market. Wall Street took notice of railroads’ growing market power and pushed them to implement PSR, which meant running faster, longer trains, and skimping on service, spare capacity, systemwide resilience, and safety. When Union Pacific closed Global 3, the railroad was implementing PSR.

|

|

Today, using PSR, railroad management’s job is to drive down the “operating ratio,” or operating expenses as a percentage of revenue. In other words, Wall Street judges railroads’ success based in part on spending less money running the railroad and more on stock buybacks or dividends. Theoretically, focusing on lowering operating ratios pushes railroads to be more efficient, to do more with less. But when railroads have the market power they have today, they can instead “do less with less,” as shippers and workers put it.

In a September speech, STB Chairman Martin Oberman criticized railroads for their “pursuit of the almighty OR” and estimated that U.S. railroads have paid out $196 billion in stock buybacks or dividends to shareholders since 2010. In comparison, over that same period according to Oberman, railroads spent $150 billion actually maintaining the physical rail and equipment they need to run their railroad.

The driving force behind PSR’s widespread adoption was railroad executive E. Hunter Harrison and investor Bill Ackman, a notorious hedge fund manager. After the two pushed through PSR at the Canadian Pacific railroad, Ackman’s colleague Paul Hilal opened an investment fund called Mantle Ridge, which invested $1.2 billion in CSX and successfully pushed CSX to appoint Harrison CEO. Under Harrison, and with the backing of CSX’s board, who saw larger bottom lines in sight, CSX pushed through PSR despite complaints from shippers who reported long delays or lost shipments. Every other railroad has adopted PSR or PSR equivalents; industry watchers say the one holdout yet to officially adopt PSR, BNSF, has adopted PSR-like measures ...

|

|

Railroad Workers United

Solidarity -- Unity -- Democracy

|

|

|

|

|

|

|