|

|

Your Investments |

August 2019

|

|

|

Today's newsletter is a mixed bag.

As we expected, the stock market continued its climb higher in July with the S&P 500 finishing the month 1.44% higher. I'm pleased to report that all of our models outperformed the S&P for the month.

Unfortunately, August, which is historically one of the worst months of the year for the stock market, is taking back the summer's gains. The cause: China trade war.

While we believe this is a war that must be faught to protect our workers and intellectual property over the long run, it is becoming increasingly clear that China will not go down without a fight.

|

The News is Driving the Market

The Federal Reserve and the China trade negotiations have figured prominently in the news over the last week and a half, and the market has reacted negatively.

First, to the surprise of no one, the Fed announced a 0.25% interest rate reduction on Wednesday, July 29. Some market participants, however, expected a 0.5% cut and were thus disappointed. Then, Chairman Powell acted a little defensively in his testimony to Congress, stating that the Fed was not necessarily entering into a "rate-cutting cycle." Further, he said the Fed always reserves the right to raise rates in the future as they see fit.

All in all, it was about as hawkish a rate cut as we've ever heard. The market did not sell off on the cut, but it did not break out to the upside either.

The very next day, President Trump tweeted about possible additional Chinese tariffs effective September 1. The S&P began to sell off late last week. What looked like a normal uptrend correction worsened over the weekend when China responded in kind to the US threatened tariffs and also immediately devalued its currency more than 10%. The effect is to make their goods cheaper than ours on a relative basis, leading to Monday's action where the S&P was down over 3% at one point during the day.

As discussed below, there has been significant technical damage done to the current uptrend, and we have decided to hedge our stock holdings as result of today's sell off. But we do not anticipate being hedged for a long period of time, or that this will become a protracted bear market. Corporate earnings drive the stock market in the long run, not the latest news headlines.

|

|

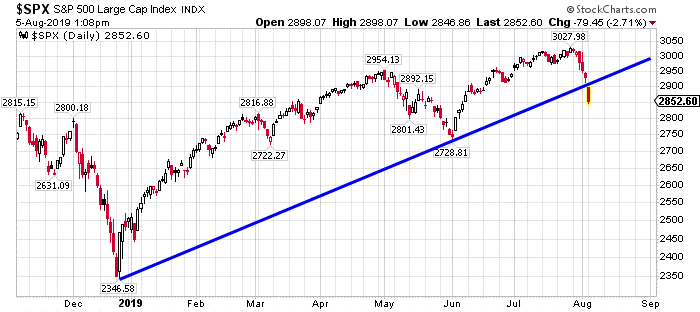

Technical Picture

Today, the S&P & Dow have sold off below their support line going back to the December low. As a result of the technical picture driven by the news of an escalation in the trade negotiations with China, we have hedged our portfolio for now.

The S&P currently trades at 2849 as of this writing. For the overall uptrend to remain intact (higher highs followed by higher lows), the S&P 500 needs to find support above the June low of 2729.

|

|

KCM Macro Trends - Classification Mistake

As you know, we use our mutual fund, the award-winning KCM Macro Trends Fund (KCMTX), in the management of our models and your money.*

Effective August 1, Morningstar reclassified KCMTX from its "multi-alternative" category to its "large-blend" category.** Do not be alarmed. Nothing has changed on our end.

Notwithstanding any third-party classification, you can rest assured that we remain an active manager focused on growing your wealth by striving to capture a majority of market uptrends; while at the same time doing our best to minimize bear-market losses that can have a catastrophic effect on your standard of living and retirement, e.g., 2001-2003 bear markets and the 2008-2009 financial crisis.

The unfortunate result of this reclassification is that our risk averse approach to investing is now being compared by Morningstar to "style box" funds, including some of which have zero risk management. A good thing in bear markets, but not always in bull markets. Apples and oranges.

The large-blend classification also gives the misleading impression that KCMTX invests only in large US company stocks. Not so. The fund invests in multiple asset classes including stocks, both domestic and foreign, bonds and commodities. It can also hedge market risk, like we did today, whereas many large-blend funds cannot.

Lipper, notably, continues to correctly classify the fund in the Alternative Global Macro category where it is a Lipper Leader achieving their highest rating of '5' in total returns and consistent returns for the 3-year, 5-year, and Overall periods out of 199, 173, and 199 funds respectively, as of 6/30/2019. The fund also won Lipper's 2018 and 2019 Awards for Best Alternative Global Macro Fund - 5 Years.***

We're doing our best to get Morningstar to correct its mistake and reinstate the fund's multi-alt classification, but are told, as crazy as it seems, we may have to wait a year.

|

In Closing

Nobody wins a trade war; everyone loses. While we don't necessarily agree, it's hard to see who the winner might be at this point. The stock market doesn't like uncertainty and for the moment that's what we've got. I even heard one pundit say we're in a new "Cold War." He may be right. Accordingly, we have taken steps to protect our portfolios from trade war volatility and seasonal weakness.

"

Patience and perseverance have a magical effect before which difficulties disappear and obstacles vanish."

John Quincy Adams

Sincerely,

Marty Kerns

President & Chief Executive Officer

|

Parker Binion

Chief Investment Officer

|

|

|

About Kerns Capital Management

Kerns Capital Management is a leading asset management firm with a focus on quantitative, liquid alternative investment strategies, including the KCM Macro Trends Fund. We are value-oriented investors in long/short equity, credit and volatility, and apply the same attention to risk in the deployment of capital that has guided us since our inception as a fiduciary investment manager to corporate pensions, trusts and high net worth individuals. Kerns was founded in 1996, and is based in Houston, Texas.

|

|

|

IMPORTANT DISCLOSURES

Performance data represents past performance and is not a guarantee of future results.

Performance current to the most recent month-end may be lower or higher, and can be obtained by calling 800-945-2125.

Marty Kerns, KC

M's Chief Compliance Officer, remains available to address any questions regarding this performance presentation, including its limitations. Mr. Kerns can be contacted via email at

[email protected]

or toll-free at 800.945.2125

.

The S&P TR 500 Index is an unmanaged composite of 500 common stocks. This index is widely used by professional investors as a performance benchmark. Total return includes reinvestment of dividends. You cannot invest directly in an index. The Dow Jones Industrial Average is a price-weighted average of 30 of the largest and most widely held stocks traded on the New York Stock Exchange and the Nasdaq. The Nasdaq Composite Index is a market-capitalization weighted index of the more than 3,000 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depository receipts, common stocks, real estate investment trusts (REITs) and tracking stocks.

*

KCM Macro Trends Fund. Investors should carefully consider the investment objectives, risks, charges and expenses of the KCM Macro Trends Fund. This and other important information about the Fund is contained in the prospectus, which can be obtained at kernscapital.com or by calling 800.945.2125. The prospectus should be read carefully before investing. The KCM Macro Trends Fund is distributed by Northern Lights Distributors, LLC. Member FINRA/SIPC. Kerns Capital Management, Inc. and Northern Lights Distributors, LLC are not affiliated.

** Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

Morningstar Multialternative Category includes funds that have a majority of their assets exposed to alternative asset strategies, including long/short, and can include funds with static allocations to alternative strategies and funds tactically allocating among alternative strategies and asset classes. The gross short exposure is greater than 20%.

Morningstar Large-Blend Category. Large-blend portfolios are fairly representative of the overall U.S. stock market in size, growth rates, and price. Stocks in the top 70% of the capitalization of the U.S. equity market are defined as large-cap. The blend style is assigned to portfolios where neither growth nor value characteristics predominate. These portfolios tend to invest across the spectrum of U.S. industries, and owing to their broad exposure, the portfolios' returns are often similar to those of the S&P 500 Index.

*** Source: Lipper, Inc. The Best Alternative Global Macro Fund award is granted to the fund in the Alternative Global Macro category with the highest Lipper Leader score for Consistent Return over the 5-year period as of 11.30 of the prior year. Lipper awards are granted annually to the funds in each Lipper classification that achieve the highest score for Consistent Return, a measure of funds' historical risk-adjusted returns, relative to peers.

Lipper ratings for Total Return reflect funds' historical total return performance relative to peers as of 12/31/18. The Lipper ratings are subject to change every month and are based on an equal-weighted average of percentile ranks for Total Return metric over 3-, 5-, and 10-year periods (if applicable). The highest 20% of funds in each peer group are named Lipper Leader or a score of 5, the next 20% receive a score of 4, the middle 20% are scored 3, the next 20% are scored 2, and the lowest 20% are scored 1. The Saratoga Large Cap Growth Fund, in Lipper's Large-Growth classification, received the following ratings for the 3-, 5- and 10-year periods (number of funds rated): Total Return: 3 (487), 5 (422) and 5 (311). Lipper ratings are not intended to predict future results, and Lipper does not guarantee the accuracy of this information. More information is available at lipperweb.com. Lipper Leader © 2019, Reuters, All Rights Reserved.

From Refinitive Lipper Awards, © 2019 Refinitive. All rights reserved. Used by permission and protected by the Copyright Laws of the United States. The printing, copying, redistribution, or retransmission of this Content without express written permission is prohibited. Lipper, a wholly owned subsidiary of Refinitive Reuters, is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

|

|

|

|

|