|

3rd Quarter 2018 Market Outlook

3Q Gives Us Springboard

Financial markets perked up in the 3rd quarter. Despite the headlines on trade wars and interest rates moving up again, the markets moved higher. As we discussed in last quarter's newsletter, the market's valuation at the end of the 2nd quarter was more compelling than at the beginning of the year. We used that as an opportunity to add to stocks that had been lagging in the market, especially in the Financial and Industrial sectors.

3Q 2018 YTD 2018

Dow Jones Select Dividend 3.08% 4.14%

SP 500 7.71% 10.56%

Russell 1000 Value 5.71% 3.92%

Economic Support Strong, With Some Caution

It's no surprise that economic growth has been strong due to corporate and individual tax reform. Gross Domestic Product (GDP) grew at 2.2% in the 1Q and 4.2% in the 2Q and growth in the 3Q is estimated to be in the 3-4% range. According to the Institute of Supply Management (ISM), economic activity in the manufacturing sector expanded in September and the overall economy grew for the 113th consecutive month. However, we note that many of the respondents discussed some pent-up buying in advance of the tariffs and voiced their concerns that the tariffs could slow near term growth. We also note that Consumer Confidence has surged to historically high levels, despite the fact that auto and housing sales have weakened.

Valuation - Higher But More Room

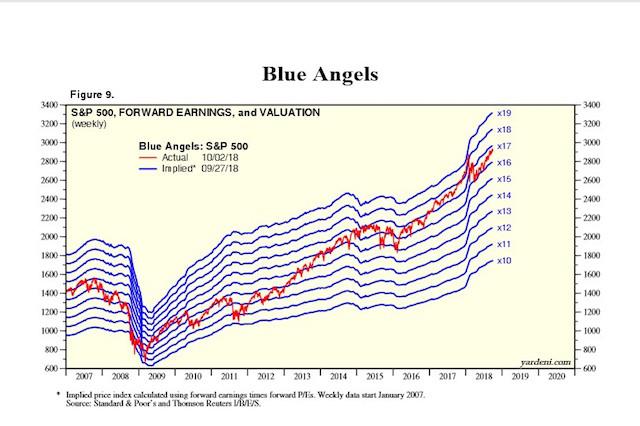

The strength of the markets in the third quarter has increased valuations. The SP 500 Index as of September 30, 2018 was trading at a Price-to-Earnings multiple (P/E) of 18.1x 2018 estimates and 16.4x 2019 estimates. According to consensus FactSet data, Earnings are expected to grow at a roughly 10% rate for both 2019 and 2020. This gives us confidence that markets can continue to rise into next year.

So we expect earnings growth can drive the market higher, but there is also potential for further multiple expansion. The chart below from economist Ed Yardeni's Strategist Handbook October 2018 implies that forward earnings on the S&P 500 have an implied value of 3400, suggesting a 16% increase from where we are today (2923.43 as of October 3, 2018.)

Dividend Strategy Driving Our Performance

We continue to focus on Dividend Growth as our primary investment strategy. This was very strong for our companies in the 3Q. Seven of our companies increased dividends an average of 13%. This brings our year to date average dividend increase to nearly 12%, compared with less than 8% for the SP 500. A full 82% of our companies have announced dividend increases.

And Earnings Could Surprise Further

Clearly, 2018 has been an exceptionally good year for corporate profits, in one of the longest expansions in history, albeit from a low base from the bottom of the financial crisis. There appear to be little traditional warning signs of recession. Rather, we see a number of reasons earnings growth could be a bit better than consensus expectations, including:

- Continued benefits of tax reform

- Trade reform to benefit domestic companies

- Low unemployment driving higher consumer income

- Consumer confidence driving increased spending

- Gradual rate increases giving companies pricing power

- Higher capacity utilization expanding corporate margins

- Growing free cash flow driving aggressive stock buybacks

Finally, we note that such higher free cash flow can drive dividend increases for companies in our portfolio at continued strong double digit rates

|