|

First Quarter 2019 Commentary & Market Outlook

Relief Rally

Financial markets rallied in the first quarter of 2019 in response to the Fed's revised interest rate outlook. While acknowledging weakness in economic growth here in the U.S. and internationally, Fed chair Jerome Powell notes no current plans to raise interest rates.

The government shutdown and uncertainty around trade deals were concerns this quarter, and reflected in corporate confidence. And while we are not expecting robust earnings for the first quarter, we await our management teams' outlook as regards the rest of the year.

Market Valuation

In our 2018 year end commentary, we reported market valuations at a forward price to earnings ratio for 2019 at 14.5x estimates. If you recall from past newsletters, price to earnings ratio is one of the ways we determine if the stock market is still in a good place to buy stocks, (whether or not it is at a fair price), or if it has gotten too expensive. The market rally and further decline in projected prices now has the market (S&P 500) trading at 16.9x estimates. In the past 3 months, estimates declined by 3.8%. At this point, we still believe that selective stocks should be bought. Interest rates have declined and when this happens, stocks are often a better purchase.

Where we end up for the year is still uncertain, but it is very possible we will see a rebound in profits for the 2nd quarter, now that the government shutdown is behind us. Any positive news on trade negotiations will also shift corporate confidence positively, which could lead the markets higher.

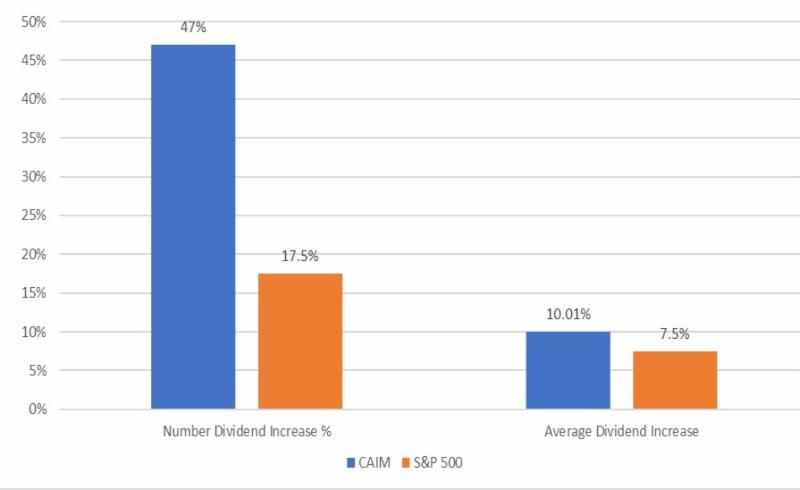

Dividends Still Robust for CAIM's Portfolio

Dividend growth continues to be strong for our portfolio. 47% of our companies have already announced dividend increases, with the average increase 10.1% so far. Dividend yield on CAIM portfolios is over 50 basis points above the 10-year Treasury bond. Meanwhile bond yields that had reached a high of 3.22% last October, have declined to 2.46%. Given this, dividend stocks, and in particular dividend growers, continue to be an attractive alternative to bonds for long-term investors.

Earnings Season Begins

While we do not expect robust earnings for the first quarter, we await direction from our portfolio companies management teams as to the outlook for earnings growth for the rest of the year. With management's typically conservative full year earnings outlook largely behind us, less currency headwinds and more benign commodity input costs, we foresee lower risk of further significant estimate reductions among our portfolios. It is management's guidance, more than past earnings, that tends to move these stocks, and here we think much of any bad news is behind us.

|