|

|

|

|

Coronavirus Alters Tax Season

|

Coronavirus resources

Coronavirus has impacted how and when the Department collects taxes. As the crisis continues to evolve, so does the Department's response. We have been working closely with the legislature and office of Gov. Phil Scott to the lessen the economic impact to Vermont's businesses and individual taxpayers. Our

Coronavirus page contains up-to-date information to guide Vermont taxpayers as the situation changes. We encourage taxpayers to check that page and the associated

FAQs page for updates before contacting us with questions.

Late penalty waivers

Personal Income Tax

Federal and state taxes originally due April 15, 2020, are automatically extended to July 15. The Vermont taxes extended are:

- Personal income tax

- Homestead Declaration and Property Tax Credit Claims

- Corporate income tax

- Fiduciary income tax.

Anyone ready to file before then is encouraged to do so.

Stimulus Payment scams

While many Americans are waiting to receive the federal Economic Impact (Stimulus) Payments, scammers are hard at work targeting individuals and preparers to get to the money first. We caution everyone to be alert to attempts by scammers to get bank account information. Government agencies of any kind, such as the IRS, the Vermont Department of Taxes, and the Social Security Administration, never contact people for their account numbers. If you receive a phone call like this, hang up. Email? Delete. Do not engage or respond in any way. The

IRS has information on these newest scams.

|

|

|

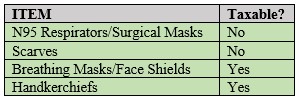

Face Coverings

|

Taxable or not?

Because of heightened awareness about the use of face coverings, below is a quick summary of Sales and Use Tax as it relates to the various types of coverings.

- N95 respirators and surgical masks are exempt from sales and use tax under 32 V.S.A. § 9741(2) because these items are therapeutic in nature, not normally used by people who aren't ill or injured, and are not capable of repeated usage. Although in these unusual times these items are becoming more routinely used by the general population, they are still exempt from tax.

- Scarves are exempt because they qualify as clothing under the law.

- Breathing masks and face shields are taxable under 32 V.S.A. § 9741(45). Although clothing is exempt from sales tax, protective equipment is taxable, because it is typically used in nonmedical settings, such as manufacturing and cleaning.

- Handkerchiefs are also taxable because they qualify as taxable "clothing accessories or equipment" under Vermont law.

See our fact sheet, General Guidelines on Sales Tax: What is Taxable and Exempt?

|

|

|

Seasonal Reminders

|

Purchasing ice

Food, when purchased from a retail store, is exempt from Vermont Sales and Use Tax. However, ice has no taste nor nutritional value, therefore it isn't food. Purchased ice is always taxable, even when the ice is intended to keep food cold or will be incorporated into beverages for sale. A business buying ice to be sold in beverages is the actual end user, and must pay sales tax. Similarly, the business pays sales tax for napkins, cups, and straws, even when Vermont Meals tax will be be charged to the consumer. See Reg. § 1.9741(13) of the

Vermont Sales and Use Tax Regulations.

Propane in containers

Propane sold in a free-standing container is subject to 6% Vermont Sales and Use Tax. The tax applies when a consumer buys a new container prefilled or exchanges an empty container for a full one. However sales tax should not be charged when a consumer has their own container for refilled.

Propane is subject to the Fuel Tax of $0.02 per gallon of fuel sold at retail only when delivered to the consumer.

Campgrounds

Campground operators are reminded of their obligations to collect and remit Vermont Meals and Rooms Tax, and if applicable, Sales and Use Tax. Technical Bulletin 50 (

TB-50) addresses the unique tax situations that campground operators may encounter in their day-to-day operations.

|

|

|

Tips for Taxpayers

|

The Compliance Corner

The Compliance Corner on the Department's website is intended to help businesses and individuals avoid making errors that can cost them time and money. The guidance in the "Tips & News" section is compiled from data gathered during audits. There have been several updates in recent months on Sales and Use Tax exemptions for the agriculture industry. Check the "Current Work" section to see what initiatives we are working on now.

New resource for young workers

A new

Tax Learning Center page on the Department website gives background information and links to resources for anyone who pays taxes. It includes a new resource, "

First Job? First Taxes!" centered around young workers. Though it's designed for classroom teachers, high-schoolers and parents may also find it helpful.

|

|

|

Proposed Regulation Updates

|

Comments requested

The Department has drafted updated Property Transfer Tax Regulations and Meals and Rooms Tax Regulations. The regulations, short descriptions, and a place to send comments is located at tax.vermont.gov/public-comments.

|

|

|

IRS Ruling: Paycheck Protection Program

|

Businesses may not deduct wages from PPP money

The IRS has ruled that a company that receives Paycheck Protection Program relief money cannot also deduct wages paid with those funds. The IRS and the Treasury Department both note that the payment is not taxable income, so also taking a deduction for the wages paid directly with federal funds would amount to a double tax benefit.

See more about the Payment Protection Program at the

IRS website.

|

|

|

To Be Perfectly Clear: Fuel Deliveries

|

Further clarification: fuel deliveries

In our January 23, 2020, e-newsletter, we wrote that the Legislature had clarified the tax on fuel deliveries in Vermont to state that deliveries to nonprofits are not exempt from the "2% Fuel Tax." This is not correct. The Fuel Tax rate is

$0.02 per gallon of fuel sold at retail, not 2% of the sale amount.

We apologize for any confusion this may have caused.

Also to note: in addition to nonprofits, the Fuel Tax applies to deliveries made to governmental entities.

|

|

|

Education Property Tax Estimator

|

New online tool

The Department has created an

Education Property Tax Estimator tool for the 2020-21 property tax year. The tool is designed to help taxpayers and school district officials understand the relationship and impact of school budgets to property taxes. The tool requires Microsoft Excel.

|

|

|

We're on Social Media

|

Looking for the latest Vermont tax tips and news?

Follow us on Facebook and Twitter!

|

|

|

When You Have a Question

|

Businesses and nonprofits with questions may reach the Department at 802-828-2505 (option 2). This phone number is answered Monday, Tuesday, Thursday, Friday 7:45AM-4:30PM. We do not take calls on Wednesdays.

For questions about Sales and Use Tax, Meals and Rooms Tax, Local Option Tax, Withholding, or for support with myVTax, email

tax.business@vermont.gov.

We are here to help.

_____________________________________________________________________________________

|

|

|

|

|

|

|

|

|

|