“What you are witnessing is the early stages of a new credit cycle.”

– Victor Hjort, global head of credit strategy, BNP Paribas.

|

|

The New Healthcare (First of a Series)

|

|

Healthcare has been ground zero for COVID-19 since the virus took hold in early March. How the industry has reacted, and how lenders and equity investors are dealing with this new world order, is the subject of this special series.

To get started, we spoke to a friend who runs the healthcare capital markets desk at a leading senior credit provider. He gave us a front-line view of deals amid the worst pandemic of the modern era.

“Physician practice management (PPM) businesses were the first and worst hit,” he reported. “I’m skeptical anyway of projected practice productivity, but procedure volume dropped precipitously with COVID. We and other banks were approached by an anesthesia practice seeking a working capital line of credit. It serves surgery centers and hospitals, and Ebitda went from close to $100 million to zero.

“Most of these procedures were elective, ranging from orthopedic, cardio, and GI. It’s a great franchise. They haven’t lost a single doc. We offered a competitive ABL RC to fund receivables. There was real interest from other banks to finance this business. Procedures appear to be rebounding well. EBITDA has only begun to lift, but lenders are taking the view that a recovery in this business is inevitable.”

What was the valuation? “Interestingly this business was purchased in the teeth of COVID,” the banker replied. “The sponsor was opportunistic and able to buy it on the cheap. We have another portfolio company, a PPM in the orthopedic space, looking for liquidity and an amendment. There’s lot of support in the bank group for the deal.

“As ugly as things look right now,” he said, “investors are taking the long view of the sector. Despite procedures having gone to zero, expectations are they will come back. So there’s a willingness by lenders to stand behind these businesses.”

What about new auctions? M&A? “Private equity behavior is evolving. We’ve had mostly constructive conversations about new opportunities. Sector-wise, we’ve stayed away from urgent care facilities, for example. Nursing homes are also very challenged. We’re taking very much of a wait-and-see approach. A lot depends on the risks of secondary outbreaks, and the development of new safety protocols. It’s next to impossible to do a nursing home deal today.”

You’re a fan of home health care. “Home health and hospice haven’t seen much of a fall-off,” he told us. “It’s a nurse going to your house, pretty simple. Same with specialty infusion, a combination of pharma and nursing. That’s seen only a slight drop.”

Some media criticize private equity for overleveraging healthcare properties. “I’ve seen that. But those stories don’t include any metrics. Data comparing the clinical outcomes of sponsor-owned vs. non-sponsor-owned companies are absent. Sharing risks and rewards is a good thing, but it’s always subject to appropriate oversight and management.”

➢ Next week: How will the patient/doctor relationship role change, post-COVID?

|

|

- Covid-19 and the Leveraged Loan Market

- Covid-19 and Private Equity Activity

- The Role of Direct Lenders

- The Economic Outlook

- The Best and the Worst Industries

- The Great Stay-In vs. the Great Recession

- Direct Lending….After COVID-19

|

|

|

A vaccine for COVID-19 will be produced:

|

|

|

(*All responses are confidential.)

|

|

|

|

Direct Lenders: What’s been your primary source of investment opportunities so far in 2020?

|

|

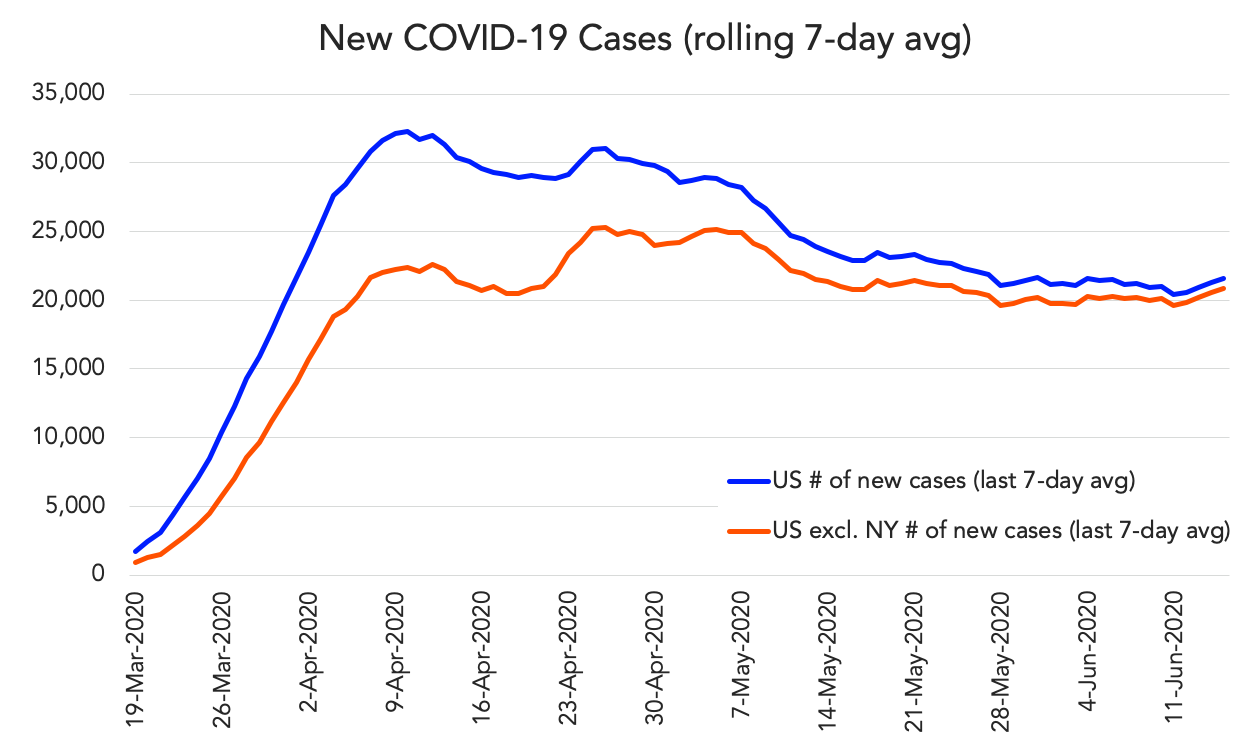

The number of new COVID-19 cases has leveled off, but outside NYC the trend is less favorable.

|

|

Source:

Refinitiv LPC, Washington Post, John Hopkins University

|

|

|

|

30-DAY FREE MEMBERSHIP

Join the leading voice of the middle market. Try us free for 30 days.

|

|

|

Is distressed best for LPs?

|

|

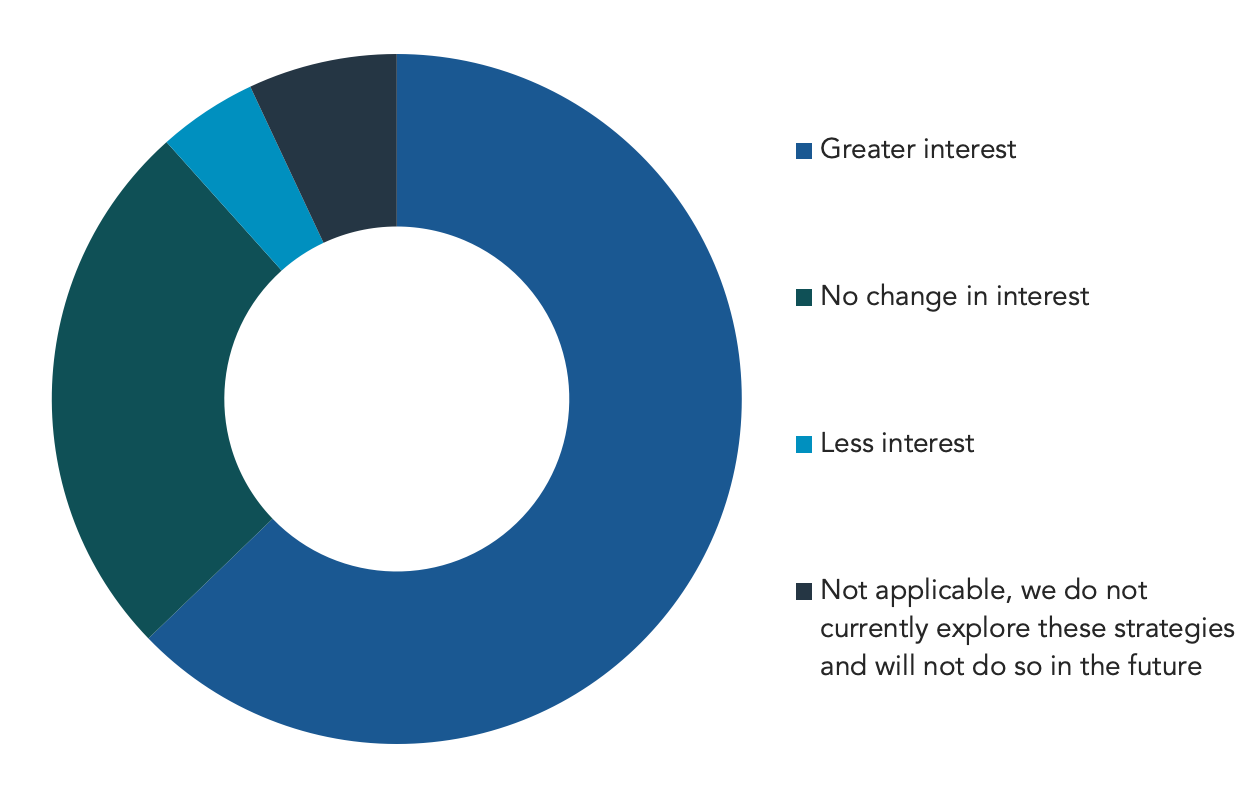

Fundraising targeting troubled companies is gathering pace, with surveys suggesting investors are keen to jump on board.

|

|

“We estimate that about half a trillion dollars across credit segments are trading at distressed levels,” said Karim Cherif and Jay Lee of UBS Global Wealth Management in a report published in mid-June.

If this quote doesn’t grab the attention of investors, it’s hard to know what will. There’s every sign that they are indeed sitting up and taking notice. A recent survey conducted by our colleagues on

Private Equity International

found that almost two-thirds of limited partners were expecting their interest in distressed debt to increase over the next six months (see chart above).

With LPs’ focus turning to distressed, there is no shortage of new funds seeking to take advantage. We have seen many examples of dislocation funds, such as a $4 billion vehicle raised by KKR and $1.75 billion by Apollo. In recent weeks, Bain Capital closed a $3.2 billion global distressed and special situations fund and Balbec Capital raised $1.2 billion for a niche non-performing loan strategy. There are many other examples.

The UBS report indicates that distressed

|

|

may be a long-lasting opportunity, which was not necessarily assumed in the early days of the covid-19 outbreak when some economists were predicting a rapid v-shaped recovery. The downturn in the debt markets and pick-up in default rates still have some way to run and there are plenty of troubled companies to be helped.

There is a hint in the report that the opportunity set could be even bigger had the monetary and fiscal policy response not been quite as dramatic. This intervention has succeeded in bringing the number of distressed credits down from the high point seen in March. However, the report also indicates that these actions are unlikely to save economies from long-term damage.

The ‘next phase’ of the opportunity – after the initial shocks felt mainly on public markets – relates to the longer-term issues that companies are facing and is where distressed specialists come in with their understanding of company fundamentals, capital structures, operating models and legal frameworks. There is much to be done.

|

|

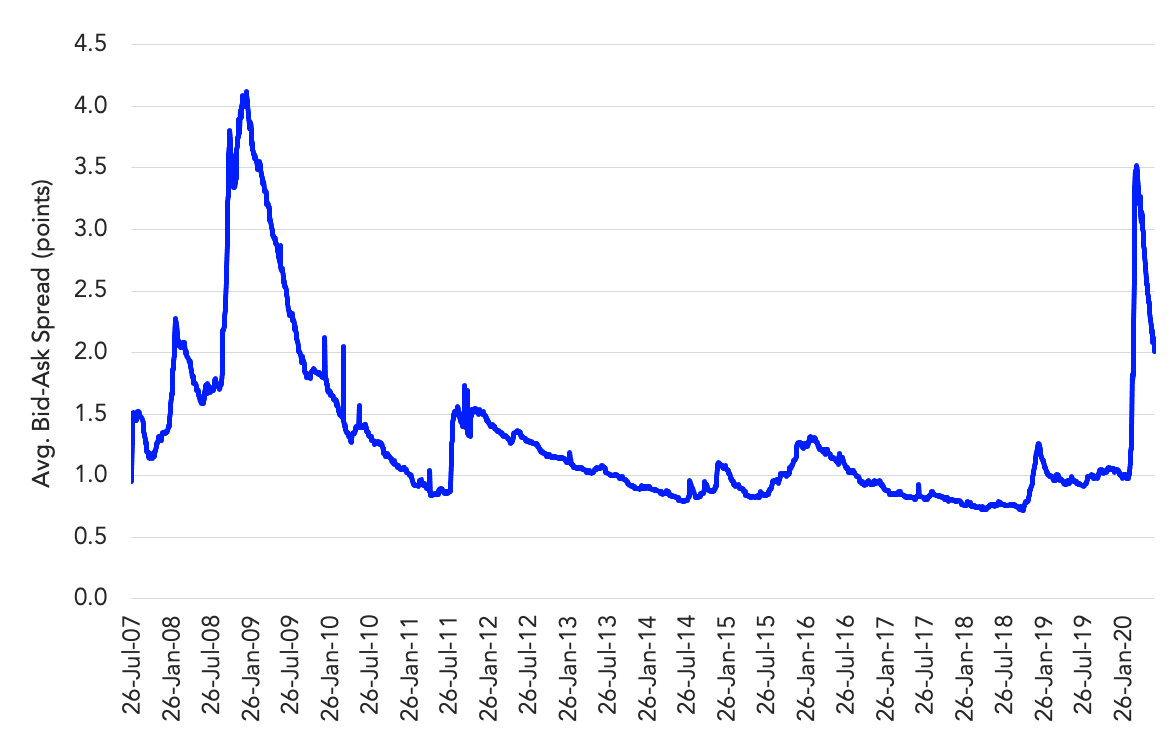

Bid/Ask spread finally narrows to 2 points

but still historically high

|

|

The average bid/ask spread in the overall US secondary market finally narrowed to 2.01 points yesterday after peaking at 3.52 points on March 27 and hovering above 2 points for 3 months. Previously, the bid/ask spread fell below 3-point mark on April 27 after hovering above 3 for a month and it’s been on a slow but constant narrowing trend ever since. However, it still remains persistently high compared to its historical norm of 1.21 points. The only other time the bid/ask spread widened to more than 2 points was during the Great Financial Crisis (GFC) peaking at

|

|

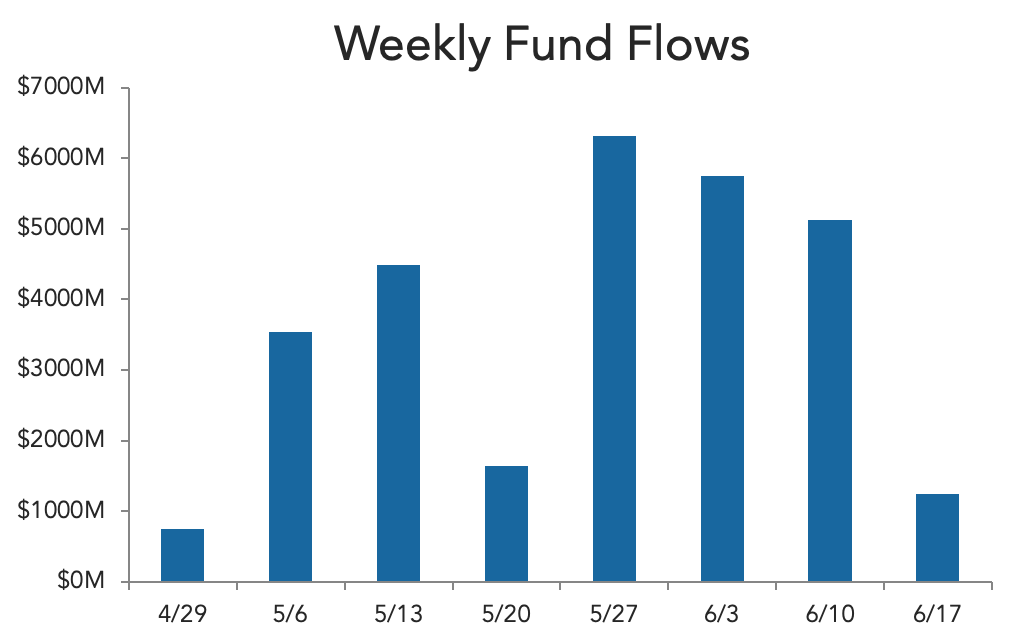

4.12 points on January 6, 2009. Back then, it took 8 months for bid/ask spread to narrow to less than 3 points and almost 2 years to recover to its historical norm. Secondary bids have been recovering with some week of inflows more recently. However, for the year, there has been US$20.2bn of outflows from loan funds through June 17 after US$37.7bn was pulled in 2019, according to Refinitiv Lipper. In contrast US$31.8bn has flowed into high-yield bond funds this year on top of the US$18.9bn past year.

|

|

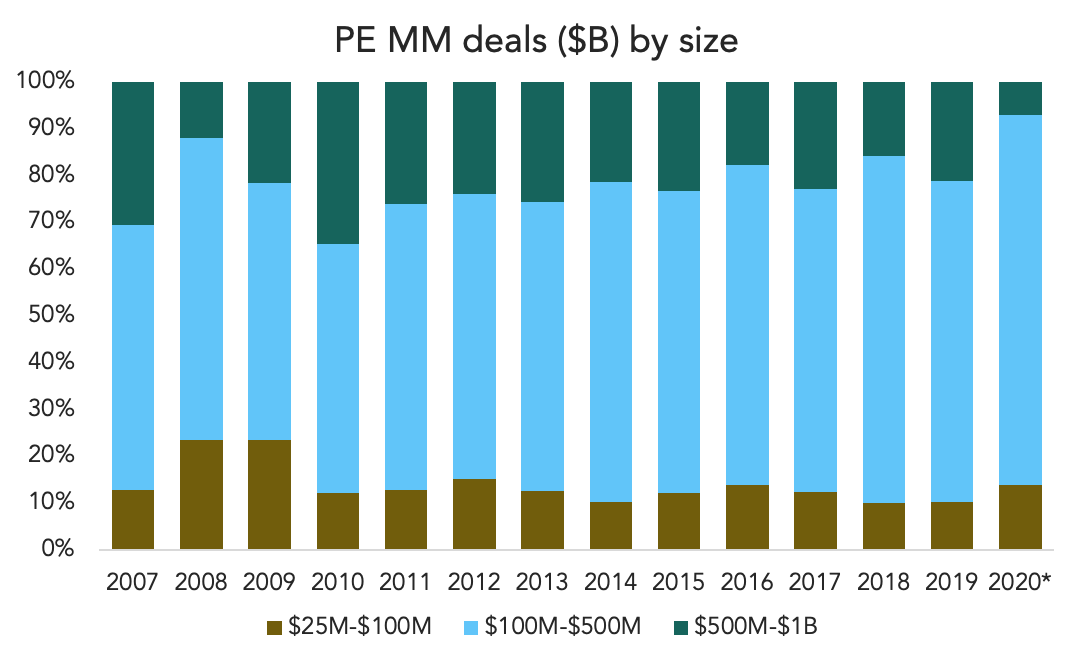

The US middle market only saw about $7 billion worth of deals valued in the $500M-$1B transaction range in Q1. That translated into 7% of total dollars invested in the middle market, a very small ratio by historical standards, according to PitchBook’s latest US Middle Market Report. Last year upper middle market deals accounted for 21% of total value, so the first quarter pivot is probably not an accident. As a whole, 2019 UMM deals were worth a combined $101 billion. It’s unlikely another $94 billion worth of transactions is in the works as 2020 progresses.

The lower middle market fared much better. 268 LMM deals were done in Q1 totaling $13.6 billion. Both numbers lined up well with 2019’s pace of 1,207 transactions valued at $48.3 billion. Like every corner of private equity, it’s unlikely that 2020 will keep up the pace this year, particularly once we know how soft Q2 numbers turn out to be. The quarantines are disproportionately impacting smaller businesses, so much so that large corporations that took federal stimulus money were shamed into returning it. The

|

|

LMM took the brunt of the initial impact, according to

RSM’s US Middle Market Business Index

. Over half of companies with annual sales between $10 million and $50 million sought immediate federal relief, while another 43% planned to apply within six months. Larger MM companies filed far fewer applications: 34% sought immediate relief with an additional 25% indicating future interest. Social distancing hurdles disproportionately impact LMM companies, too. Not every small business has the resources to effectively work from home.

In the same vein, LMM deals are often done for personal reasons. They’re less transactional and more event-driven—retirement, divorce and medical reasons are common catalysts to sell. The headache that is 2020 is another event to add to the list. One hopes this won’t happen, but it’s possible many small business owners will grow more exhausted as time passes and decide to move on to something else. Seeing their companies survive under PE ownership presents a happier ending compared to other options.

|

|

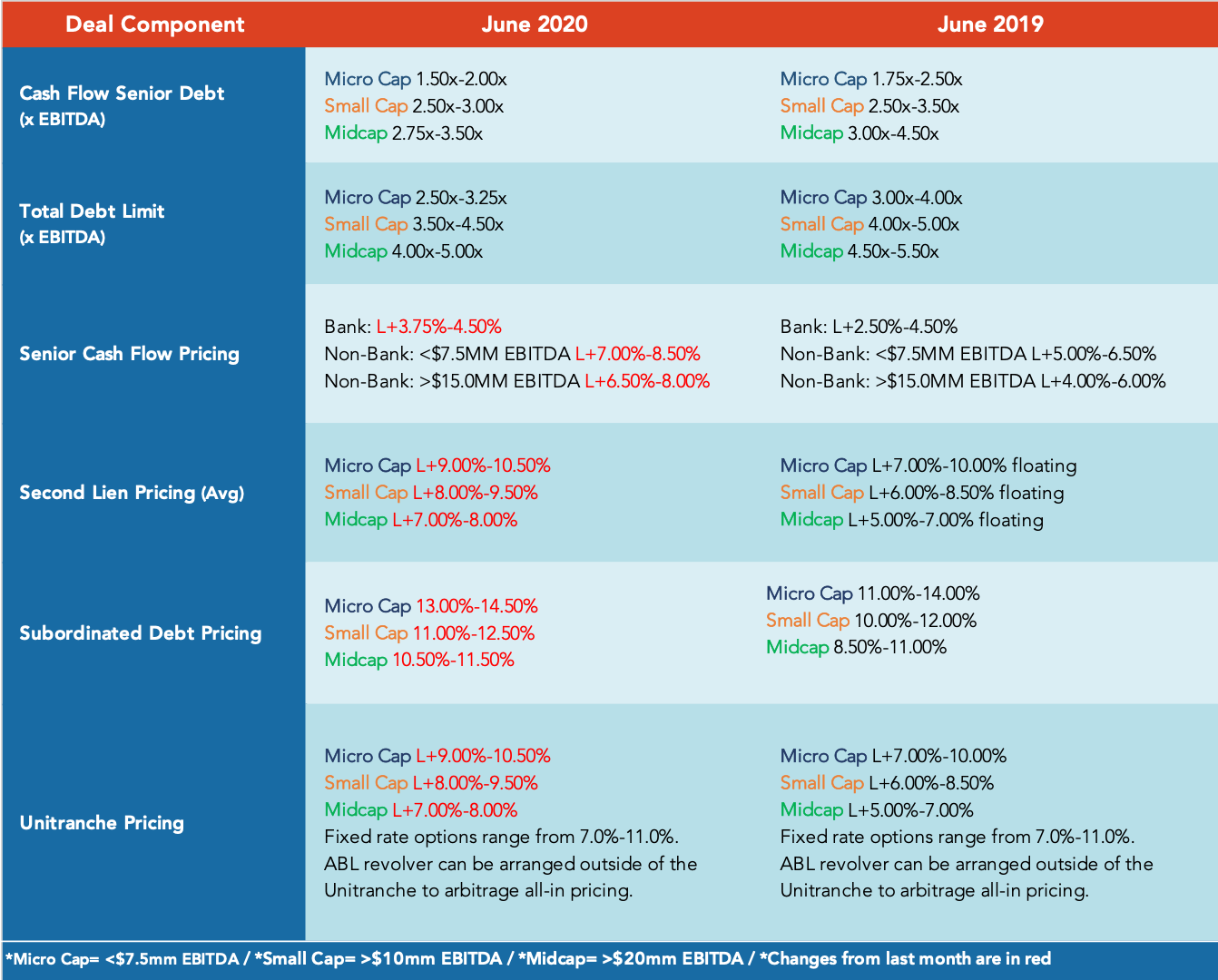

Percentage of Loans with F&C Tranche / Pro Forma EBITDA >0.9x (All Deals)

|

|

Weekly fund flows source:

Lipper

|

|

Ardonagh highlights viability

for large unitranches

|

|

It’s not a buyout, but

Ardonagh Group

’s record unitranche loan of £1.575 billion highlights the viability of jumbo ‘unis’ in a cautious direct lending market.

Ares Management’s direct lending platform in Europe is lead arranger on the financing, while Caisse de depot et placement du Quebec, HPS Investment Partners and KKR are significant lenders, according to Ares. The lender group is tight, sources said, and includes Oaktree Capital and Owl Rock Capital.

Hold levels across direct lenders have retreated anywhere from 25% to 50% since the pandemic hit, sources say, but they note jumbo unis can still get done if anchored by underwriters that will take north of $100 million— as shown by Ardonagh’s roster. Without big anchor tickets, it’s much

|

|

harder to piece together a unitranche of more than $400 million, they said.

While a U.K. deal, U.S. sources said that pricing and other terms would be similar here. The opening spread is L+750, tied to a grid and subject to a floor, according to sources. The non-call period runs for two years, then flips to 102/101 in years three and four.

There are few Covid-era comps on pricing for large direct lending deals. Sources say L+750 is about 100 bps to 150 bps above averages from a year ago.

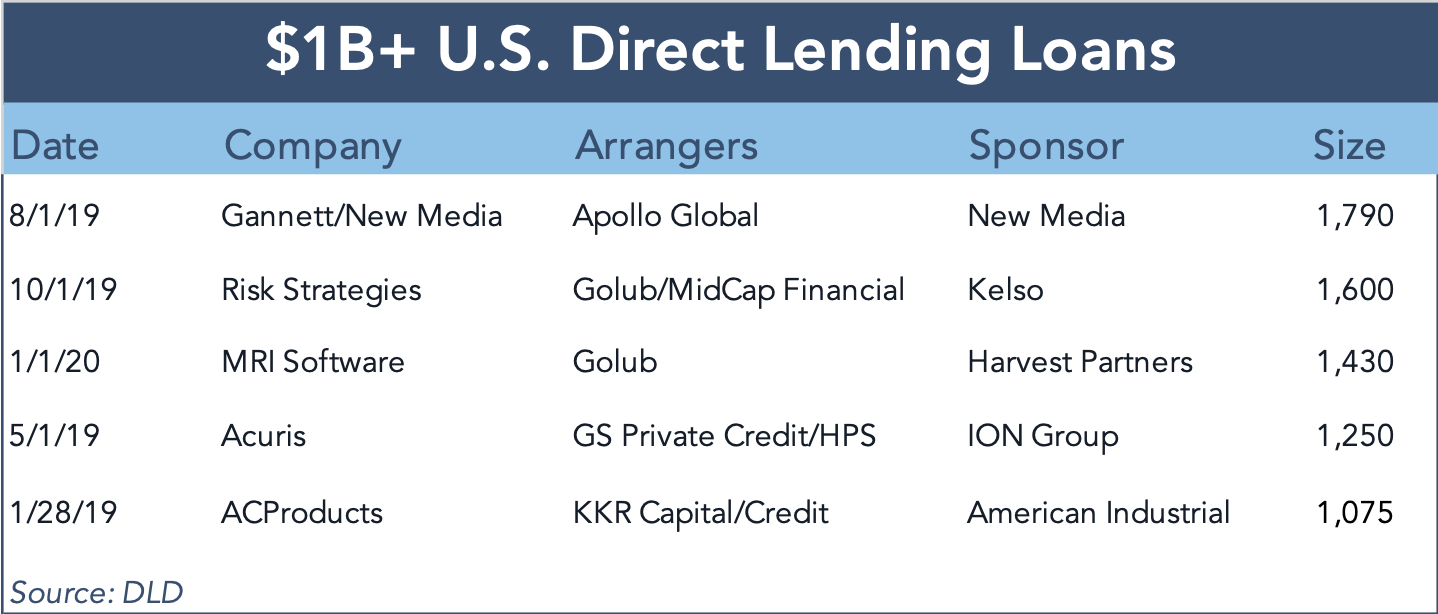

The £1.575 billion is equivalent to $1.96 billion and eclipses the $1.79 billion unitranche financing arranged by Apollo Global for Gannett/New Media last year, which up until now was believed to be the largest unitranche ever underwritten.

|

|

Distressed Debt Funds are on the Raise

|

|

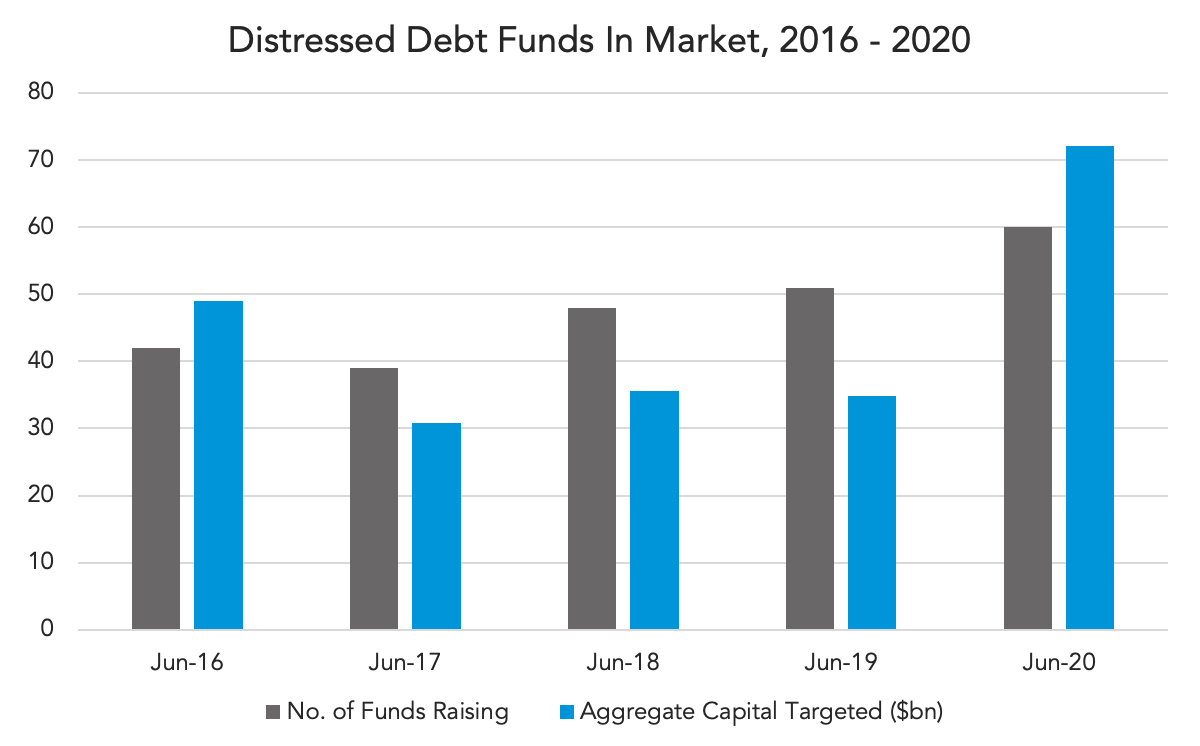

The private debt market is very crowded and, although direct lending funds represent the largest proportion, distressed debt funds have reached new records. There are currently 60 distressed debt funds in market looking to raise capital, seeking for a combined $72bn in capital. This represents more than double the amount of capital targeted by distressed

|

|

debt funds during 2019, and the highest total in the past five years. North American companies constitute 74% of capital targeted by distressed debt funds on the road, followed by a 20% of funds looking towards European firms. The largest distressed debt fund in history is now in the market: the Oaktree Opportunities Fund XI, which is targeting $15bn.

|

|

Primary issuance picks up the pace

as loan deal flow rebounds

|

|

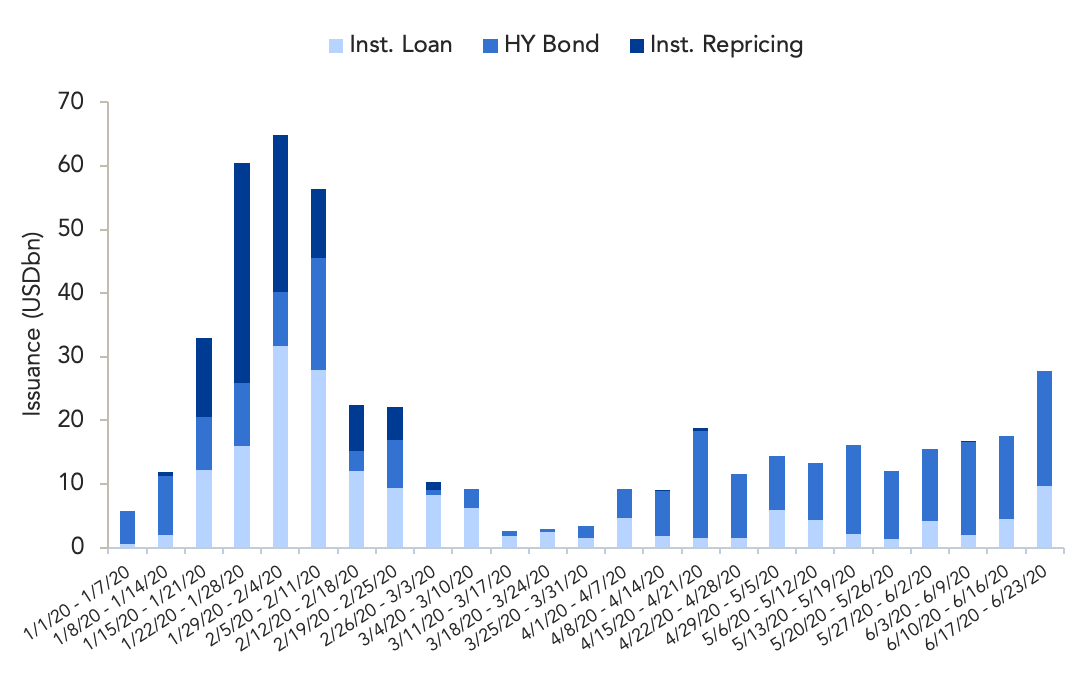

Weekly primary market activity has reached its highest level since the onset of the pandemic as issuers continue to tap the leveraged debt markets to address financing needs. The most recent week of 17 June to 23 June saw roughly USD 27.8bn of deals priced, marking the largest single-week total since well before the coronavirus (COVID-19) pandemic shut down much of the leveraged debt markets in March.

The recent milestone noticeably trails the roughly USD 65bn leveraged deal flow seen back in late January, however a significant portion of issuance at the time, roughly USD 24.6bn, was attributed to loan repricings which have all but vanished from the current market landscape.

Also of note is the recent uptick in loan issuance, though it continues to lag high yield bond volume. The latest week saw USD 9.7bn of institutional loans price, the

|

|

highest weekly figure since early February. Institutional loans have similarly made up a greater proportion of combined issuance in recent weeks, increasing to 36% from 11% at the end of May.

High yield bonds still dominate the narrative however, making up the lion’s share of the market and posting the highest weekly issuance figure year-to-date, at USD 18.1bn. Month-to-date activity in June totals USD 51bn, already surpassing the full-month totals of USD 41bn and USD 46bn achieved in April and May when the markets reopened.

Notable deals to price in the last week include

Ultimate Software

’s USD 3.545bn loan refinancing package,

Eldorado Resorts

and

Caesars Resort Collection

’s USD 1.8bn term loan and USD 6.2bn notes supporting their merger and

PG&E

’s USD 2bn dual-tranche note offering to support its exit from bankruptcy.

|

|

This publication is a service to our clients and friends. It is designed only to give general information on the market developments actually covered. It is not intended to be a comprehensive summary of recent developments or to suggest parameters for any prospective financing opportunity.

|

|

|

|

|

|

|