|

Life During COVID 19

Well, its certainly different this time. The shock that the economy, and our lives, have endured is unlike anything we have seen before. And at CAIM we're Boomers, so we've been around awhile!

Let's focus on what the current situation means for your portfolio.

At CAIM our job is to try and maximize returns while controlling risk and (here's the tricky part) investing in the US equity market. And doing so while sticking to our long-term discipline of seeking the best cash flow based returns.

The last sentence begs the question: has the long term changed? We think not. This is not the stock market's first shock, even if it was the quickest, giving most of us little time to react.

Companies currently suffering are doing so through no fault of their own. Earlier this year saw solid fundamental growth and cash flow generation in the companies we chose to own. And looking ahead we do expect these strong fundamentals to return, at some point, for the vast majority of these companies.

The current recession began in March, and experts agree is likely to last through the second quarter. The question remains how quickly we come out of the recession in the second half. Given

current circumstances it is unlikely we can flip a switch on a shut-down economy. This means sales and earnings will likely see a long climb back. And the question remains, when will the market discount such recovery and by how much. And to what the extent has it already done such discounting.

Why Active Management Provides an Advantage

In periods of high volatility and/or market declines, as we are seeing currently, active management has been shown to outperform passive strategies (i.e. ETFs), according to a recent study by StyleAnalytics. In this difficult first quarter, more than half of active managers have outperformed

their benchmarks. The reason? Active managers can be more nimble in focusing on individually mis-priced companies. Lower prices mean more buying opportunities. And we still believe it is a 'market of stocks,' more than a 'stock market'. This is evident in the out performance of our portfolios versus our benchmarks.

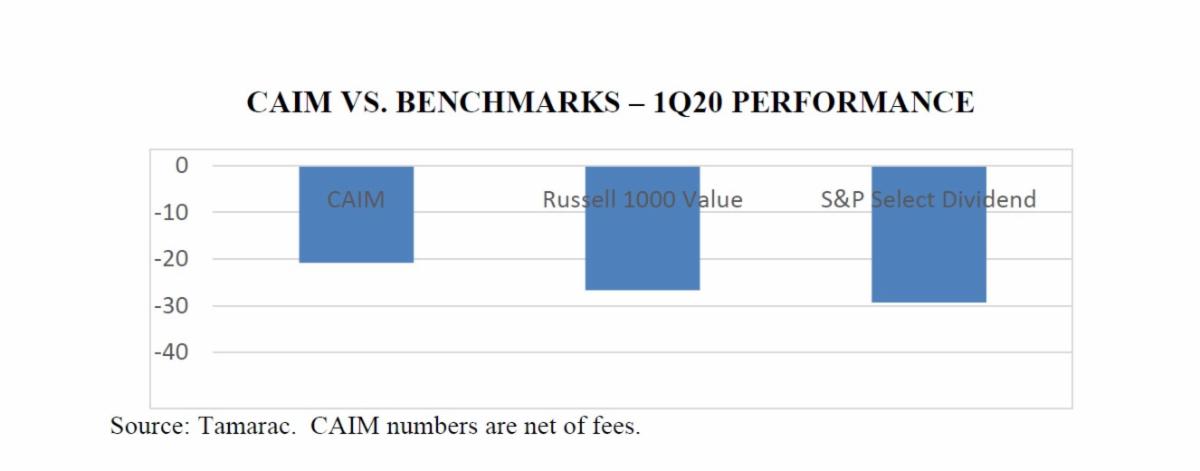

For the first quarter, the CAIM portfolio strategy saw a total return of (-20%), including dividend yields about 100 bps ahead of the market, while our benchmarks declined notably more, as shown in the graph (below). Our dividend focus was 600 basis points ahead of the Dow Jones Select Dividend index and the Russell 1000 Value index. Our strategy continues to rank in the Top Quartile of our Morningstar peer group with a 4-star ranking on a 1-, 3- and 5-year basis (please call or email us for more specific data).

Moving Forward

Even as we write this letter, we are seeing stocks rebound from their March 23rd lows. And while trying to analyze and/or estimate data for companies between now and year end with any accuracy is difficult, what we do know is that the economy will slowly move back to normal during the course of 2020.

It will be different by industry and region and we will also be somewhat subject to how the recovery progresses on a global level.

Interest rates will continue to remain low for an extended period of time. One year Treasury notes are yielding 0.168%. High quality dividend paying stocks are slightly over 3.5%.

Which brings us back to the dilemma of how to allocate our investments for both safety and growth. We lived through this scenario post the 2008 financial crisis and it never really improved. Our advice is to keep a minimum of 2 years cash flow in money market, CD's, short-term treasuries for capital preservation and buy high quality stocks with the remainder of your investable assets.

For anyone with questions, please call or email us to set up a ZOOM call.

We wish you and your family's good health!

|