|

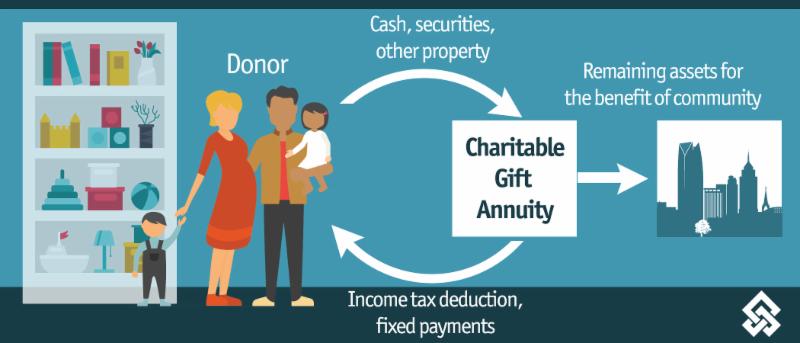

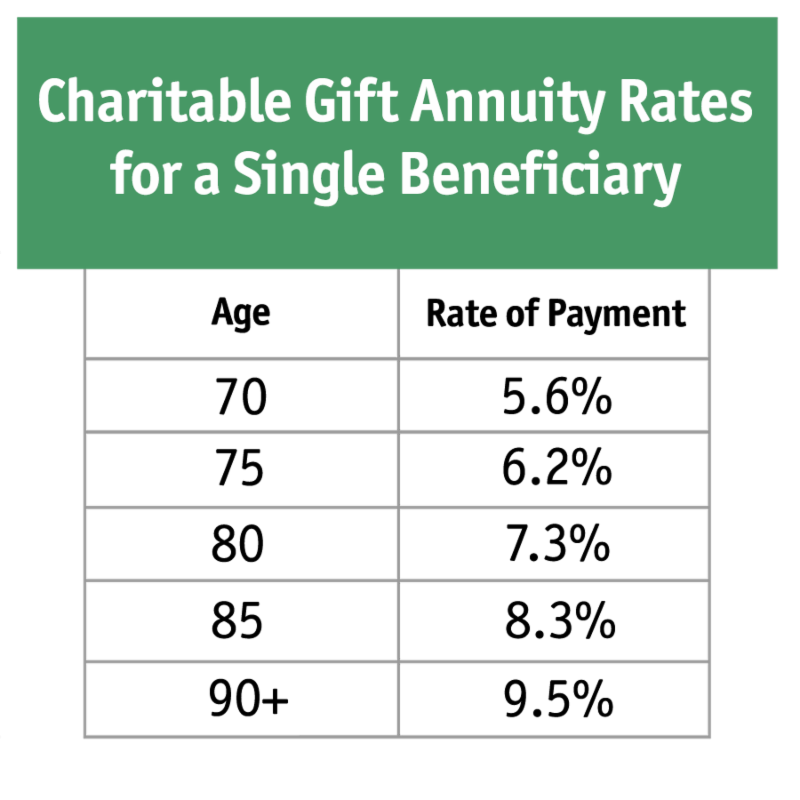

The donor transfers an asset (typically cash, securities or real estate) to charity in exchange for a lifetime income stream for themselves and/or a loved one, and receive an immediate charitable income tax deduction. At the end of life or termination of the contract, the charity receives the remaining balance in the annuity. For example, a 75-year-old can expect to receive a 6.2 percent rate of return and an approximate charitable deduction of 45 percent of the face value of the contract.

We have many donors that like to use highly-appreciated stock to fund a CGA, because they can avoid the immediate capital gains tax while allowing full use of the gift to provide an income stream. Other donors prefer using cash, because a larger portion of the income will be considered tax-free for a period of years. In some cases, donors will use CGAs as a portion of their fixed-income portfolio, knowing this is a gift and the principal can never be returned. However, given the favorable returns are typically higher than those of CDs and money markets, CGAs are very attractive for donors who wish to support charitable causes.

Another benefit of CGAs is they have no age limitations compared to commercial annuities.

We've executed several CGAs for donors well above the age of 90.

Why? A 9.5 percent return is what they would tell you!

By funding a CGA at the Oklahoma City Community Foundation, a donor can name a donor advised fund as the beneficiary. Rather than supporting just one charity, this allows them to support a number of charities while also creating a lasting charitable legacy. For a calculation of how a CGA might benefit your clients, visit our online

deduction calculator and the schedule of

gift annuity rates. Please feel free to

contact me to help you create a personalized proposal for your clients at 405/606-2914.

|

Do you want to increase your professional knowledge and skills and better serve your clients? Do you want insight that will benefit your clients immediately? This free luncheon through the Oklahoma City Community Foundation and the Cannon Financial Institute helps you make it happen!

Do you want to increase your professional knowledge and skills and better serve your clients? Do you want insight that will benefit your clients immediately? This free luncheon through the Oklahoma City Community Foundation and the Cannon Financial Institute helps you make it happen!