|

|

Your Investments |

April 2019

|

|

|

In March, the S&P 500 gained another 1.9%; the Nasdaq 2.7%. Year-to-date the indicies are up 13.51% and 17.97%, respectively.

If you're keeping score, the S&P now sits just 2.9% below its September 2018 high mark; while the Nasdaq is 4.4% short of its August peak.

An old Wall Street proverb says the stock market "climbs a wall of worry." This expression refers to a market uptrend that occurs when there is significant uncertainty about its sustainability. Today, uncertainty concerning slowing global growth, trade war with China and dysfunctional interest rate policy abound.

In our December newsletter we wrote about the inverted yield curve as a recessionary indicator. Turns out this time the inversion might be bullish! We'll explain.

In addition, we are pleased to announce that our mutual fund, the KCM Macro Trends Fund, has won its second consecutive

Lipper Fund Award

for Best Alternative Global Macro Fund over five years.

See

below.

|

|

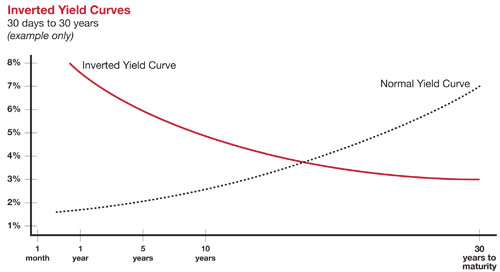

Inverted Yield Curve - A Head Fake?

In December, we wrote about a partial inversion of the yield curve (five-year yield below the three-year yield) as a potential canary in a coal mine.

Economists use an inverted yield curve to predict economic slowdowns and recessions. While there have been false positive inversions, an inverted yield curve has correctly predicted all ten recessions since 1953.

Typically, the 10-year yield is compared to the two-year (or shorter term) yield, and recessions usually occur 12-36 months after the inversion.

Back in December, the Fed was still planning to raise rates on the short end. Longer term US bond yields were falling because even at 3%, they were p

aying much more than foreign bonds. This drove foreign demand into US long-term treasuries.

Most inversions occur as a result of Fed tightening. However, on March 22:

1. just two days after the Fed signaled that there would be zero rate hikes in 2019 (as opposed to two), and

2. the day President Trump appointed dovish Stephen Moore to the Fed Board,

the 10-year yield fell below the three-month yield and the market sold off a bit in response, but then rebounded.

As a result, some pundits argue this will be a false positive inversion, citing the Summer 1998 false positive inversion as an example. In 1998, the 10-year yield plunged below the two-year yield after the Russian ruble crisis and the failure of Long Term Capital Management. The Fed turned dovish in response, and the market cruised to a banner year and all-time highs in 1999.

We tend to agree with these pundits. It's difficult to imagine a recession with the unemployment rate near a five decade low, wage growth above 3%, and an accommodative Fed.

As a result, with the economy at full employment, we are watching for any signs of inflation. In our view, the US economy will not experience a recession until inflation pressures force the Fed to start tightening again.

|

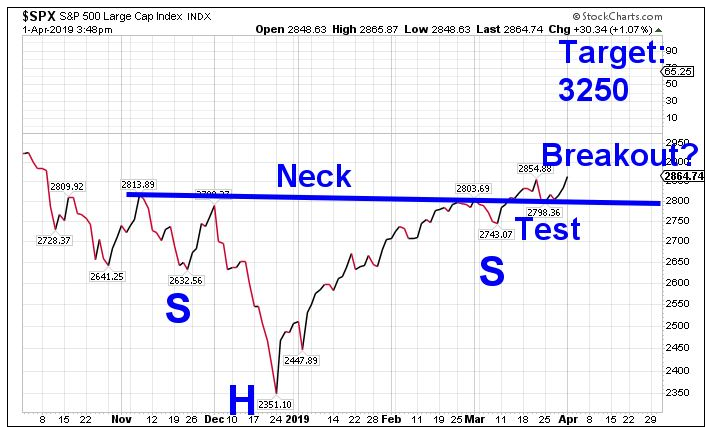

The Technical Picture - Bullish Breakout?

Technically, we may have just completed the formation of a bullish inverse head-and-shoulders pattern. The left shoulder formed at 2630 in November. The head formed at 2350 on Christmas Eve. The right shoulder formed at 2740 in early March. The neckline is in the 2800 region which we broke above in mid-March, and tested in late-March before bouncing. On April 1, we have now broken above the highs of March and made a new high for 2019.

If this pattern is in play, we would calculate the target by subtracting the head (2350) from the neckline (2800) and adding the difference (450) to the neckline. Thus, the target is 3250, which would be more than a 13% gain from current levels.

|

|

KCMTX Recognized by Refinitive (f.k.a. Thomson Reuters) & Morningstar

KCMTX Recognized by Refinitive (f.k.a. Thomson Reuters) & Morningstar

Refinitive, formerly Thomson Reuters, has once again awarded the KCM Macro Trends Fund (KCMTX) with the 2019 Lipper Fund Award for Best Alternative Global Macro Fund over five years. KCMTX also received the award in 2018.

The Lipper Fund Awards USA recognize funds and fund managers for their consistently strong risk-adjusted three-, five-, and ten-year performance, relative to their peers, based on Lipper's proprietary performance based methodology.*

K

CMTX also continues to hold Morningstar's highest overall rating of 5-Stars as of March 31, 2019. The Morningstar Rating is a measurement of a fund's risk-adjusted return, relative to similar funds. Fund

s are rated from 1 to 5 stars, with the best performing receiving 5 stars. KCMTX is also the Top-Ranked Multi-Alternative Fund for the five-year period ending March 31, 2019 out of 178 funds based on total return.**

To learn more about the Fund, please visit

KernsCapital.com

or contact Martin Kerns at 713.993.0949, ext. 107.

|

|

In Closing

Bull markets "climb the wall of worry." Bear markets "slide down the slope of hope". In our opinion, we're in in the sweet spot. The economy is growing, jobs are abundant, wages are growing, inflation is in check and interest rates are low. A "Goldilocks" market some say. Yet, slowing growth outside of the US has many pulling on the reins. Until inflation and interest rates start rising, we believe the waters are safe and that pullbacks should be seen as a buying opportunity.

Sincerely,

Marty Kerns

President & Chief Executive Officer

|

Parker Binion

Chief Investment Officer

|

|

|

About Kerns Capital Management

Kerns Capital Management is a leading asset management firm with a focus on quantitative, liquid alternative investment strategies, including the KCM Macro Trends Fund. We are value-oriented investors in long/short equity, credit and volatility, and apply the same attention to risk in the deployment of capital that has guided us since our inception as a fiduciary investment manager to corporate pensions, trusts and high net worth individuals. Kerns was founded in 1996, and is based in Houston, Texas.

|

|

|

IMPORTANT DISCLOSURES

Performance data represents past performance and is not a guarantee of future results.

Performance current to the most recent month-end may be lower or higher, and can be obtained by calling 800-945-2125.

Marty Kerns, KC

M's Chief Compliance Officer, remains available to address any questions regarding this performance presentation, including its limitations. Mr. Kerns can be contacted via email at

marty@kernscapital.com

or toll-free at 800.945.2125

.

* KCM Macro Trends Fund. Investors should carefully consider the investment objectives, risks, charges and expenses of the KCM Macro Trends Fund. This and other important information about the Fund is contained in the prospectus, which can be obtained at kernscapital.com or by calling 800.945.2125. The prospectus should be read carefully before investing.

The KCM Macro Trends Fund is distributed by Northern Lights Distributors, LLC. Member FINRA/SIPC. Kerns Capital Management, Inc. and Northern Lights Distributors, LLC are not affiliated.

** Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

Morningstar Ratings. The Morningstar RatingTM for funds, or "star rating", is calculated for managed products (including mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product's monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The Morningstar Rating does not include any adjustment for sales loads. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics.

The KCM Macro Trends Fund (KCMTX) received 5 stars from Morningstar in the Multi-alternative category for the 3-year and 5-year periods ending March 31, 2019 based on risk-adjusted returns out of 276 and 178 funds, respectively. The Fund received 4 stars out of 63 funds for the 10- year period.

Morningstar Rankings.

The KCM Macro Trends Fund (KCMTX) ranks in the top 1% of Multi-alternative funds by Morningstar, Inc., for the five-year period ending March 31, 2019 out of 178 funds based on total return. The fund ranks in the top 2% for the three-year period and top 8% for the ten-year period out of 276 and 63 funds respectively. Rankings are just one form of performance measurement.

Morningstar Percentile Rankings are based on the average annual total returns of the funds in the category for the periods stated and do not include any sales charges or redemption fees. The highest (or most favorable) percentile rank is 1 and the lowest (or least favorable) percentile rank is 100. Rankings for each share class will vary due to different expenses.

Morningstar Multialternative Category

includes funds that have a majority of their assets exposed to alternative asset strategies, including long/short, and can include funds with static allocations to alternative strategies and funds tactically allocating among alternative strategies and asset classes.

*** Source: Lipper, Inc.

The Best Alternative Global Macro Fund award is granted to the fund in the Alternative Global Macro category with the highest Lipper Leader score for Consistent Return over the 5-year period as of 11.30 of the prior year. Lipper awards are granted annually to the funds in each Lipper classification that achieve the highest score for Consistent Return, a measure of funds' historical risk-adjusted returns, relative to peers.

From Refinitive Lipper Awards, © 2019 Refinitive. All rights reserved. Used by permission and protected by the Copyright Laws of the United States. The printing, copying, redistribution, or retransmission of this Content without express written permission is prohibited.

Lipper, a wholly owned subsidiary of Refinitive Reuters, is a leading global provider of mutual fund information and analysis to fund companies, financial intermediaries and media organizations.

© Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information.

The S&P TR 500 Index is an unmanaged composite of 500 common stocks. This index is widely used by professional investors as a performance benchmark. Total return includes reinvestment of dividends. You cannot invest directly in an index. The Dow Jones Industrial Average is a price-weighted average of 30 of the largest and most widely held stocks traded on the New York Stock Exchange and the Nasdaq. The Nasdaq Composite Index is a market-capitalization weighted index of the more than 3,000 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depository receipts, common stocks, real estate investment trusts (REITs) and tracking stocks. The iShares Core U.S. Aggregate Bond Index is an ETF (AGG) that seeks to track the investment results of an index composed of the total U.S. investment-grade bond market. The Morningstar Moderate Target Risk Index is based on a well-established asset allocation methodology from Ibbotson Associates, a Morningstar company and a leader in the field of asset allocation theory. The securities selected for the asset allocation indexes are driven by the rules-based indexing methodologies that power Morningstar's comprehensive index family. Morningstar indexes are specifically designed to be seamless, investable building blocks that deliver pure asset-class exposure. Morningstar indexes cover a global set of stocks, bonds, and commodities.

3230-NLD-4/2/2019

|

|

|

|

|