|

Exposure Draft No. 1: CPA Competency-Based Experience Pathway

The first proposal is aimed at helping CPA candidates meet initial licensure requirements. This additional option would not replace existing pathways, but instead respond to market changes and expand opportunities for the next generation of accountants.

The Uniform Accountancy Act (UAA) provides state legislatures and boards of accountancy with a national model that can be adopted in full or in part to meet the specific needs of each state and jurisdiction. The UAA provides a national framework for regulating CPAs, promoting consistent standards, and protecting the public.

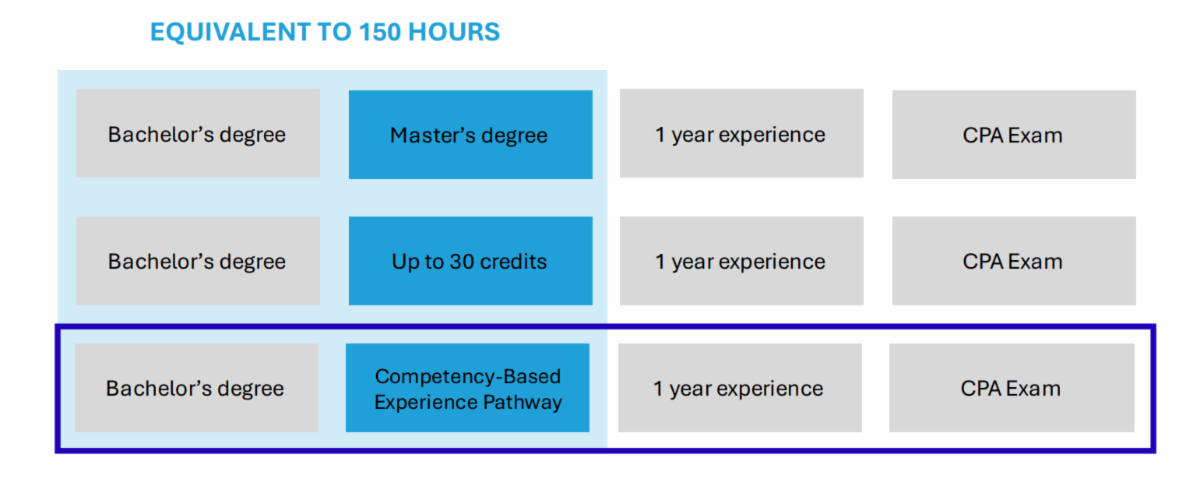

The proposed changes to the UAA would allow states to potentially adopt the CPA Competency-Based Experience Pathway, an additional option for CPA candidates to demonstrate professional and technical skills in the workplace after earning a bachelor’s degree and meeting their state’s requirements for accounting and business courses.

Under the UAA currently, after candidates obtain a bachelor's degree, they must pass the CPA Exam, complete one year of professional general experience, and either earn a master's degree or take college courses that bring them to 150 total credit hours—most bachelor’s degrees require 120 hours. (NOTE: In Nebraska presently, two years of public accounting experience or three years of experience in business, government, or academia are required to obtain a permit to practice.)

The competency framework at the heart of the proposal includes seven professional and three technical competencies. Candidates would be required to exhibit all seven professional competencies and at least one of the three technical competencies. The proposed professional competencies are ethical behavior; critical thinking and professional skepticism; communication; collaboration, teamwork, and leadership; self-management and continuous learning; business acumen; and technology mindset. The proposed technical competencies are audit and assurance; tax; and business and financial reporting.

The competencies, which would be verified in the workplace by licensed CPAs, are expected to take most candidates a year, but there is flexibility in the timing for completion.

Comments on the Competency-Based Experience Pathway Exposure Draft are due Dec. 6.

|