|

ALTERNATIVE FINANCIAL SERVICE PROVIDERS ASSOCIATION

January 30, 2020

|

New rules are gutting consumer watchdog group from the inside, legal experts say

- The Consumer Financial Protection Bureau announced a new policy that some fear will weaken its policing of Wall Street.

- The agency, created a decade ago to rein in financial abuse against consumers, has recovered more than $12 billion to date.

- The Trump administration appears to have cut back significantly on enforcement activity.

The agency created in the wake of the 2008 financial crisis to protect consumers from abuse is being gutted from the inside, according to some consumer advocates and legal experts.

A new enforcement policy at the Consumer Financial Protection Bureau is the most recent example of an agency drifting away from its mission to police Wall Street's bad actors, these advocates say. Read more at CNBC

|

House bill to reshape credit reporting, help borrowers improve scores

The CREDIT Act, or HR 3621

A new bill is up for vote in the House of Representatives aimed at reforming credit reporting practices.

The bill would also direct the Consumer Finance Protection Bureau to study the impact of traditional credit reporting on minorities, people with limited credit history, immigrants, and those receiving government assistance.

According to the Federal Trade Commission, 1 in 5 Americans have found "potentially material" errors in their credit report. While 20% had modifications to their report, the FTC found, only 13% had a change in their score due to their dispute. The study also found that 5% had errors in their report that negatively impacted their ability to receive credit, or the terms of the credit received.

Read more at YAHOO FINANCE

|

|

Ex-Billionaire Scott Tucker Payday Loan Lender Finally Tells His Own Story. By Jer Ayles

Scott Tucker has been portrayed by Netflix, American Greed, The WSJ, The NYT... and on and on as a pure, 100% scum bag payday loan lender and loan shark for years. When I speak to investors, Wall Street, Family Offices, reporters, employees and peers, the name "Scott Tucker" is always part of the conversation.

Below, I give you your opportunity to hear directly from Scott. In his own words, you will gain insight into his side of his story. No matter your preconceived thoughts about Scott Tucker and his payday loan business escapades, the interview below will most likely change your mind in some respects and inform you as to the lengths our government will go should they choose to make an example of you! [NOTE: BOOKMARK THIS PAGE in order to listen to all 5 podcasts!]

No doubt about it, Scott employed some pretty outrageous business practices. Scott has a big ego and he pushes everything he participates in to the limit!

And, as we all now know, so do the FED's.

Scott did a 2.5-hour interview with a white-collar criminal consultancy group focused on helping defendants in criminal cases prepare for sentencing, prepare for prison, and prepare for the best possible outcomes.

Read more at The Business of Lending to the Masses

|

Final CFPB Payday Rule Expected in April

The Consumer Financial Protection Bureau (CFPB) said that it plans to issue its long-awaited final rule in April that would roll back underwriting requirements for payday lenders by eliminating a provision from 2017 mandating that lenders verify borrowers' repayment ability.

In 2019, the CFPB proposed reevaluating the rigid 2017 payday lending regulation issued under previous Bureau director Richard Cordray. According to American Banker, in the agency's fall rulemaking agenda, it said that the "comment period for the [proposal] closed in May 2019 and the Bureau is carefully reviewing the approximately 190,000 comments it received. The Bureau expects to take final action in April 2020 with respect to this proposal."

Under the current payday lender regulations, the CFPB restricts lenders from making multiple attempts to debit payments from consumer bank accounts. A pending lawsuit in Texas also seeks to eliminate the current regulation, to which the judge has postponed the rule's compliance date to November 2020.

An additional part of the bureau's agenda is to issue a proposal revising the remittance rule. It would confront the "temporary exception that allows institutions to estimate fees and exchange rates in some circumstances," the CFPB said.

Read more at Native American Financial Services Association

|

Our Bet on Alternative Data for Credit Scoring. By TRUST SCIENCE

Recently five federal regulators issued a joint statement advocating the use of alternative data in credit scoring. Ultimately, the statement was to expand access to credit and provide more favourable terms to borrowers.

At Trust Science we've been firm believers in the use of alternative data to not only serve the underbanked but also give lenders more accuracy in predicting good vs bad loans and the ability to serve more customers.

Trust Science was founded with the mission to for every single person to be able to get the credit they deserve. We knew the credit underwriting industry was in dire need for change, and it required innovation to take credit decisioning and credit scoring to the next level.

So we worked on a way to provide an online platform for lenders that gave them custom scores based on their business, loan types, geographies and consumers. Plus, we made our scores dynamic so that they could adapt based on new variables; variables that could include market conditions, interest rates, and regulatory changes. We powered the platform with machine learning and AI and considered all of the potential data sources that could provide the most accurate insights for lenders.

Read more at TRUST SCIENCE

|

CFPB defines 'abusiveness' but draws advocates' fire

The Consumer Financial Protection Bureau (CFPB) clarified the definition of an "abusive" act or practice as one in which "the harm to consumers outweighs the benefit," according to an agency statement Friday.

The bureau also said it would generally avoid "dual pleading" - that is, if the agency penalizes a company under the unfairness or deception standards, it won't use the same set of facts to also find the company abusive unless it can provide a legal rationale for bringing a separate abusiveness claim.

The Dodd-Frank Act gave the bureau the power to punish organizations over unfair or deceptive acts and added the abusiveness standard. But the CFPB let actions speak louder than words, issuing enforcement actions under the standard - in essence, establishing a precedent - without necessarily defining it.

Banks have sought a narrow definition of abusiveness for some time. But the CFPB's clarification - and particularly the "dual pleading" clause - drew criticism from consumer advocates because the bureau's enforcement history doesn't seem to back it up.

Read more at BANKING DIVE

|

Least Cost Routing: How to Minimize the Cost of Debit Payment Processing. By Payliance

Controlling costs and operating efficiently are critical to success in business. One method of reducing operating costs in the lending space is to leverage payment solutions that incorporate least cost routing. With least cost routing, a processor uses a proprietary algorithm in combination with identifying information embedded within the card number to process debit card transactions through the lowest cost network available.

The Cost of Debit Card Processing for Lenders

In 2010, the Durbin amendment to the Dodd-Frank law was passed, limiting interchange charges with the intent of passing savings from merchant to consumer. It also disallowed exclusive deals between network and a single card issuer, requiring that at least two networks be available for transaction routing.

The Federal Reserve found that the average cost per debit card transaction was 1.15 percent of the total transaction value in 2017. However, the interchange fee makes up 85-90 percent of the total fee. These interchange rates are set by the networks and are formulated based on several different factors, including the merchant industry, type of card, and compliance standards. Those rates are also reviewed two times each year.

Read more at PAYLIANCE

|

24 state attorneys general step up to defend CFPB

A coalition of two dozen state attorneys general has filed a brief with the Supreme Court arguing that the Consumer Financial Protection Bureau's regulatory powers should be protected.

The coalition, led by New York Attorney General Letitia James, filed an amicus brief in Seila Law, LLC v. Consumer Financial Protection Bureau. The case stems from a 2017 investigation by the CFPB into Seila Law, a California law firm, for its debt-relief practices. Seila Law sued to block the investigation entirely, arguing that the CFPB's structure was unconstitutional because its director could only be removed for cause. Seila Law maintained that this for-cause provision violated the Constitution's separation of powers clause.

Both the US District Court for the Central District of California and the Court of Appeals for the Ninth Circuit rejected Seila Law's argument, and the firm has now appealed the case to the Supreme Court. The law firm is arguing that Title X of the Dodd-Frank Act - which includes the provisions that created the CFPB - must be struck down as unconstitutional.

Read more at MORTGAGE PROFESSIONAL AMERICA

|

What Does the Truth in Lending Act Mean for Consumers and Businesses? by MicroBilt News

The Truth in Lending Act (TILA) is one designed to protect consumers from predatory lending practices and ensure fair treatment for all consumers. The original law was passed in 1968 though it has been amended multiple times in the 50+ years since.

How does TILA Protect Consumers Shopping for Loans?

The Truth in Lending Act prevents lenders and creditors from engaging in deceptive practices to convince consumers to apply for the following:

- Mortgage loans

- Credit cards

- Auto loans

- Home equity loans

- Other types of credit and loans

It works by requiring lenders to reveal specific information to borrowers that include vital information such as annual percentage rates for the loan, the term of the loan (how long the loan will last), and the total costs borrowers will pay for the loan.

Read more at MICROBILT

|

Smaller Companies Need to Step Up Their Cyber Security Efforts

Whenever we hear about major cyber security attacks such as data breaches, it's typically larger enterprises that are the victims. That makes sense, considering those events can potentially impact a lot of people and therefore are more likely to grab headlines and garner attention.

But that doesn't mean small and mid-sized companies (SMBs) are immune to such attacks. In fact, smaller organizations are frequent targets of cyber incidents, and they generally have far fewer resources with which to defend themselves.

A recent study by the Ponemon Institute, which conducts research on a variety of security-related topics, presents a clear picture of the cyber security challenges SMBs are facing. The report, "The 2019 Global State of Cybersecurity in SMBs," states that for the third consecutive year small and medium-sized companies reported a significant increase in targeted cyber security breaches.

For its report, Ponemon conducted an online survey of 2,391 IT and IT security practitioners worldwide in August and September 2019, and found that attacks against U.S., U.K., and European businesses are growing in both frequency and sophistication.

Read more at SECURITY BOULEVARD

|

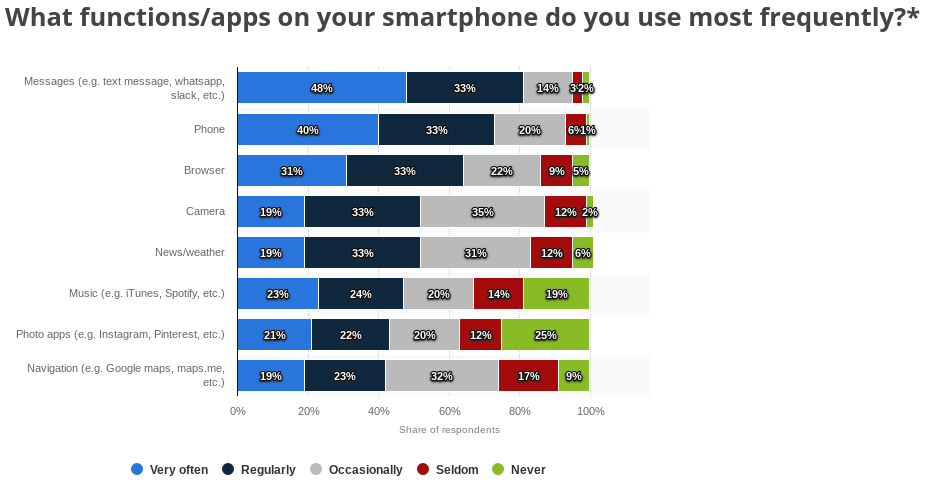

Launch Your Own Mobile Payment App. by Kristen Hoyman

Make it easy for customers to pay and stay with your very own mobile payment app.

People use their smartphones for so many things other than making actual calls. In a late 2017 Statista survey, almost one-third of smartphone owners reported that they use their phones to make calls either occasionally, seldom, or never.

Yet, almost two-thirds of smartphone users use their mobile browsers regularly and more than 70% use the messaging functionality regularly or very often. Aside from texting, there are many mobile apps in the Messages category, including Slack, WhatsApp, Asana, Basecamp, Telegram, Discord and more.

The bottom line: people are on mobile apps. A LOT. This includes your customers. In fact, eMarketer conducted a fascinating study in late 2017. The study concluded that people are on their mobile phones for longer periods each day (no surprise there). The surprise, however, was that the time spent in mobile browsers is declining and time spent using mobile apps is increasing. At the same time, the number of apps people are using is dropping. People all over the country, including your customers, are on their phones more, browsing less, and using fewer apps more frequently.

Read more at REPAY

|

The Supreme Court could upend consumer financial protection as we know it

The Supreme Court is hearing a case in March about the Consumer Financial Protection Bureau and could ultimately rule the agency to be unconstitutional.

That would dissolve the CFPB, which was created in 2010 as a response to the financial crisis, and may reduce states' power to police financial laws, as well.

The CFPB has recovered more than $12 billion for consumers since its creation.

A case before the Supreme Court has the power to dramatically reshape how the U.S. government polices financial fraud and other misdeeds against consumers - which many experts fear would weaken existing protections and expose the public to more harm.

The case, which concerns the Consumer Financial Protection Bureau, could ultimately lead to the dissolution of the agency, which lawmakers created in the wake of the 2008 financial crisis and was bestowed with broad powers to issue and enforce consumer protection rules in areas such as banking, student loans, credit reporting, mortgages, payday loans and debt collection.

Read more at CNBC

|

States charge feds of giving payday lenders a loophole around usury laws

A proposed rule change would allow small loan lenders to affiliate with banks that are exempt

A coalition of 18 states and the District of Columbia is asking the Office of the Comptroller of the Currency (OCC) to reconsider a proposal that the states say would give payday lenders a loophole to get around state usury laws.

A number of states have enacted laws to limit the interest rate on small-dollar loans to no more than 36 percent APR. Since payday lenders charge fees that often amount to as much as 400 percent APR, they can't operate within those jurisdictions.

The state officials contend that, if finalized, the new OCC rule would enable predatory lenders to circumvent these interest rate caps through "rent-a-bank" schemes, in which banks act as lenders in name only and pass along their state law exemptions to non-bank payday lenders.

Read more at CONSUMERAFFAIRS

|

|

ALTERNATIVE FINANCIAL SERVICE PROVIDERS ASSOCIATION

|

| Alternative Financial Service Providers Association

757.737.4088 315 Tuscarora St., Lewiston, NY 14092

[email protected]

www.afspassociation.com |

|

|

Copyright © 2020. All Rights Reserved.

|

|

|

|

|