|

ALTERNATIVE FINANCIAL SERVICE PROVIDERS ASSOCIATION

February 4, 2020

|

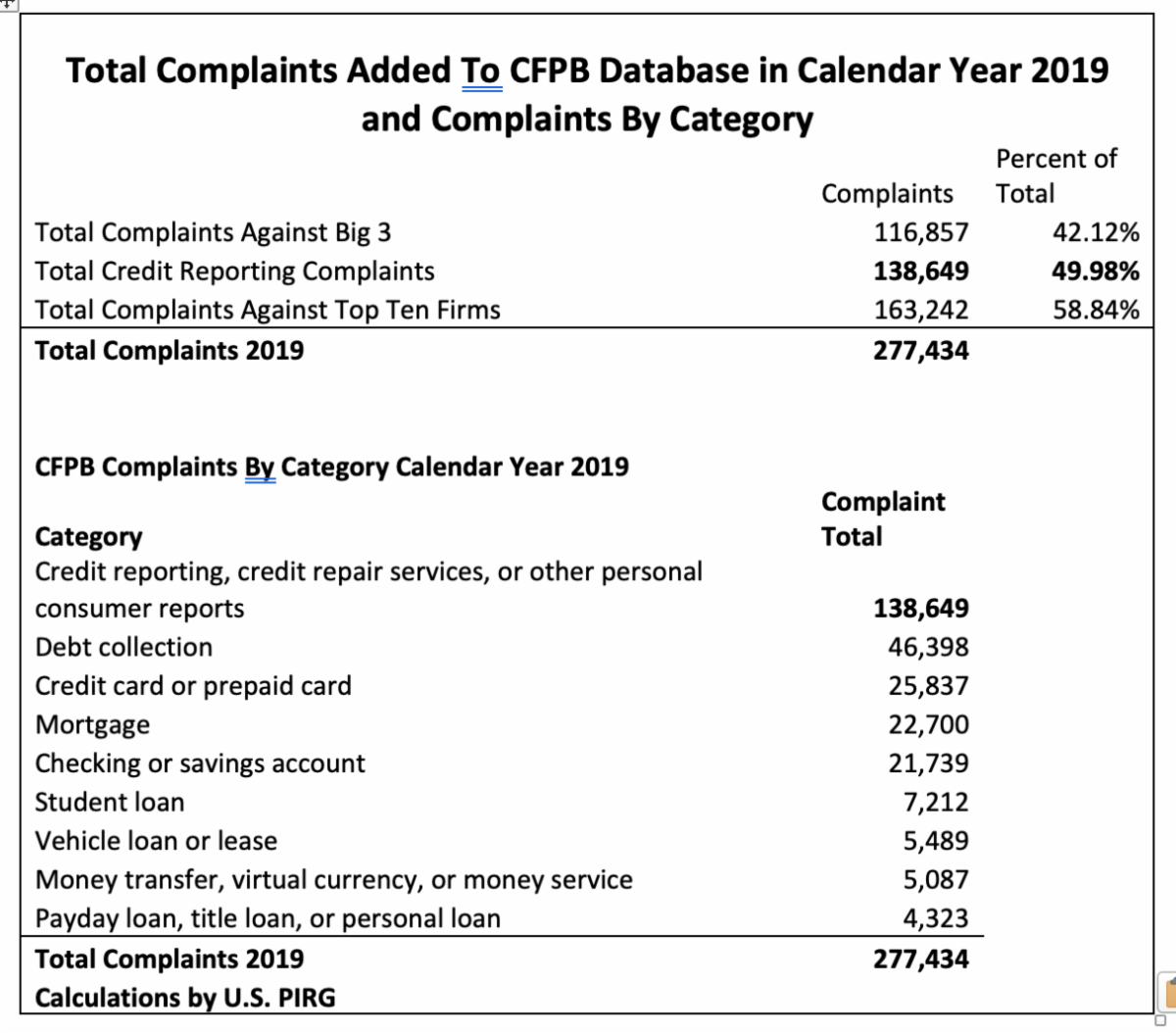

House passes legislation to overhaul consumer credit reporting

The House on Wednesday passed legislation aimed at overhauling consumer credit reporting and providing additional protections and opportunities to rebuild credit.

The legislation also includes provisions that would strengthen restrictions on credit checks for employment decisions unless necessary for positions that require background checks "by a federal, state or local law, or for a national security clearance" and would shorten the time negative credit information stays on a report down to four years and make changes to the credit report dispute process.

Proponents of the bill argued it is a necessary step to fight back against abusive or predatory practices and provide borrowers with options to gain financial stability.

Read more at THE HILL

|

When a small town loses its only bank

DUNCAN, Ariz. - If you squint into the desert sunlight, you can still read the faded letters on the white sign atop the former bank branch overlooking the Gila River.

National Bank of Arizona, the last in a series of out-of-town banks to operate a branch in this small, geographically isolated community, closed its doors in July 2016. Today the beige-colored building is vacant, except for an ATM operated by another company, which charges $2.75 for a cash withdrawal.

Posted on the glass front door is a notice that invites visitors to patronize the bank's branch in Safford, Ariz. The trouble is, that location is 40 miles away. "We apologize for any inconvenience," the notice reads.

The local branch's closing has been a major blow to residents of Duncan, which is near the New Mexico border and was once a popular stop along the road connecting Phoenix and El Paso, Texas. Local business owners no longer have a place to deposit cash each night, nor anywhere nearby to apply for a loan. Many senior citizens, especially those uncomfortable with digital banking, have felt an outsize impact.

Read more at AMERICAN BANKER

|

|

The Supreme Court could upend consumer financial protection as we know it

The Supreme Court is hearing a case in March about the Consumer Financial Protection Bureau and could ultimately rule the agency to be unconstitutional.

That would dissolve the CFPB, which was created in 2010 as a response to the financial crisis, and may reduce states' power to police financial laws, as well.

The CFPB has recovered more than $12 billion for consumers since its creation.

A case before the Supreme Court has the power to dramatically reshape how the U.S. government polices financial fraud and other misdeeds against consumers - which many experts fear would weaken existing protections and expose the public to more harm.

The case, which concerns the Consumer Financial Protection Bureau, could ultimately lead to the dissolution of the agency, which lawmakers created in the wake of the 2008 financial crisis and was bestowed with broad powers to issue and enforce consumer protection rules in areas such as banking, student loans, credit reporting, mortgages, payday loans and debt collection.

Read more at CNBC

|

|

LoanPaymentPro Highlights

- Multiple Exclusive Domestic Acquiring Banks and ODFI Banks

- State-by-State License and FI Chartered Lenders supported

- Brick and Mortar, Online Lenders, Marketplace Lenders

- Installment, Line of Credit, Title Loans, Lease to Own, Marketplace etc...

- 350+ Plus Active Merchant Lenders currently using LoanPaymentPro

- Average Clients' Monthly Bankcard Processing Volume - $750K

- Single source Bankcard, ACH, and RCC/Check21 processing platform

Read more at LoanPaymentPro

|

2020 list of Consumer Reporting Companies

This list includes the three nationwide consumer reporting companies as well as other companies that focus on certain market areas and consumer segments.

Use this list to help you take advantage of your right to review the information in your consumer reports, and dispute possible inaccuracies with companies as needed.

The list includes the three nationwide consumer reporting companies-Equifax, TransUnion, and Experian-and several other reporting companies that focus on creating consumer reports for certain industries.

View the REPORT

|

Alchemy FinTech Infrastructure Platform enables FinTech, Banks and Financial Services to launch with ease.

Alchemy was founded on the belief that technology, analytics and operations should be executed in concert, flawlessly. We founded this company to take away the back office pain points from our clients and enable to the focus on their story.

We deliver our core solution and customized workflow for a variety of financial verticals. Our personal loan, line-of-credit, mechanics financing, construction loans and student loan installations are state of the art. We have developed point-of-sales portals for student aids office and construction offices to qualify and finance customers in real time.

Out of the box and customized lending software

We spent the past 4 years crafting customer and point of sale experiences in a variety of industries. Based on the foundation of our deep lending experience and real-world implementations, we continuously refine industry-specific underwriting algorithms, workflows, user experience and loan management functionalities.

Our vertical solution in mechanics financing, construction loans and student lending space have the most up to date customer experience and regulatory compliance already built into our software.

Read more at ALCHEMY

|

Federal Reserve Board announces series of "fintech innovation office hours" across the country to meet with banks and companies engaged in emerging financial technologies

The Federal Reserve Board on Tuesday announced that it will hold a series of "fintech innovation office hours" across the country to meet with banks and companies engaged in emerging financial technologies, popularly known as fintech.

The sessions will serve as a resource for banks and fintech firms to meet one-on-one with Federal Reserve staff members with relevant expertise to discuss fintech developments and ask questions. They may be particularly helpful to community banks and their potential fintech partners. Sessions will be co-hosted with Reserve Banks, with the first session at the Federal Reserve Bank of Atlanta on February 26. Firms interested in participating can sign up here.

Also on Tuesday, the Board launched a new section of its website specifically focused on fintech innovation. It will serve as a central hub of information for stakeholders interested in learning about and engaging with the Board on innovation-related matters. The section features the latest Federal Reserve Consumer Compliance Supervision Bulletin, which summarizes supervisory observations regarding fintech and practical steps institutions can consider when engaging in fintech activity.

Read more at The Federal Reserve Board

|

Dreher Tomkies LLP: SERVICE PROVIDERS' DATA SAFEGUARDS SUBJECT TO SUPERVISION

Financial institutions are not the only entities that must implement reasonable data security programs. The consumer data safeguard practices of third party service providers to such financial institutions are also subject to supervision by various federal regulatory agencies, including the Federal Trade Commission ("FTC") and the Consumer Financial Protection Bureau ("CFPB").

In November 2019, the FTC issued a complaint and proposed settlement with a Utah-based technology company ("TechCo") that provides back-end operation services to direct sale companies. The FTC complaint provides that the TechCo provides products and services to manage all aspects of their client's business operations, including compensation, inventory, orders, accounting, training, communication and data security, among other things. In the course of providing these business operations, the TechCo received significant amounts of consumer personal information, including full names, dates of birth, physical and email addresses, telephone numbers, Social Security numbers or other government identification numbers, payment card information including credit or debit card numbers, Card Verification Values and expiration dates, bank account information including bank account and routing numbers and account user IDs and passwords.

Read more at Dreher Tomkies LLP

|

Gen Z has more card debt than millennials - and higher credit scores

Credit cards are more common among Generation Z Americans than they were with the preceding generation of millennials, who came of age during the Great Recession, according to a study released last week by credit bureau TransUnion. About 41% of people age 18 to 24 in 2019 had them, compared with 34% in the same age range in 2012.

About 50% of Gen Z reported prime credit scores (661 and above), compared with 39% of millennials in 2012.

A greater percentage of millennials in 2012 reported having student loans (44%) than their Gen Z counterparts in 2019 (37%). That could be because higher unemployment rates led more millennials to continue their education before entering the workforce, TransUnion said.

Gen Z's higher credit scores may make lenders more comfortable extending credit. However, underwriting standards in the auto and credit card industries have also become more favorable toward nonprime borrowers since 2012. About 23% of subprime Gen Z consumers have a credit card. That's nearly double the 12% of millennials that had one or more at the same age. Additionally, 10% more credit-active Gen Z consumers have an auto loan, compared with millennials at the same age.

Read more at BANKING DIVE

|

Banking-As-A-Service's Secret Sauce

Remember that old term "banker's hours?"

That term, which fairly or unfairly suggested that banks were centers of slow-moving progress and relatively easy professional work, is long gone. Indeed, banks represent a significant and necessarily vital part of the massive changes taking place all around the world in financial services and payments - moves that are happening at increasing, even real-time, speeds. They are more often bound together with their business clients, as well as other consumers and players, via the world of FinTech. Banks are now at the center of some of the world's most exciting and vital innovations and disruptions - new ecosystems are being created as technology progresses and consumer habits evolve.

Banking As A Service

Those changes have given rise to the banking as a service (BaaS) concept, which - as Anabel Perez, NovoPayment CEO and co-founder, told Karen Webster - is finally coming of age. Banking as a service, as Perez defines it, serves as a software platform that connects financial institutions (FIs) to a variety of innovators with value-added services that help them acquire and retain new customers via new and evolving use cases. Application programming interfaces (APIs) simplify that access for banks and for FinTechs that want their innovations to reach their customers.

Read more at PYMNTS.COM

|

Better Money Habits® Millennial Report - Winter 2020

Our 2020 Better Money Habits Millennial Report explored the money mindset of today's young adults (ages 24-41), revealing their financial priorities, trade-offs and stressors and how they're balancing it all along the way. We found that nearly one in four millennials that are saving have at least $100,000, up from 16 percent in 2018 and 8 percent in 2015. Despite this good news, millennials still feel behind financially compared to peers and are juggling substantial debt levels with near and long-term financial priorities.

- Nearly three-quarters (73 percent) of millennials are saving for life milestones and future goals, a 10 percentage point increase compared to 2018. Three-quarters are saving for retirement, while 51 percent are building an emergency fund.

- Over the past year, 39 percent of millennials boosted their credit score, 29 percent secured a raise and 24 percent put away more toward retirement.

- Millennials saving for retirement started building their nest egg at 24 years old, on average - earlier than Gen X (30) and baby boomers (33).

- Despite financial progress, 51 percent of millennials feel behind in their overall financial situation and 33 percent believe their peers are better off financially. Seventy-three percent are not optimistic about their financial future.

- Still, 90 percent of millennials are willing to make sacrifices to achieve a financial goal, including cutting back on dining out (70 percent) and eliminating vacations (35 percent).

Read more at Bank of America

|

- CENTRAL TEXAS: 5 Financial Services

- TEXAS: 15+ Payday, ATL and Installment Lender Operations

- MICHIGAN: 20+ Location PDL Operation

- CHICAGO area: Small Dollar Installment Lender

- SOUTHERN CALIFORNIA: 1 Payday Loan Store

|

|

ALTERNATIVE FINANCIAL SERVICE PROVIDERS ASSOCIATION

|

| Alternative Financial Service Providers Association

757.737.4088 315 Tuscarora St., Lewiston, NY 14092

[email protected]

www.afspassociation.com |

|

|

Copyright © 2020. All Rights Reserved.

|

|

|

|

|