Here's To Your Wealth

November, 2016

|

The Markets:

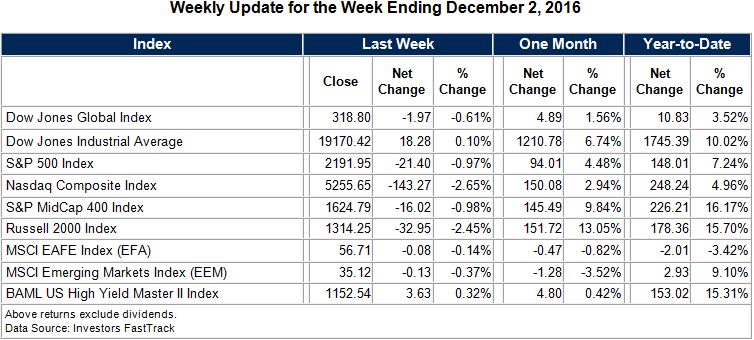

November, at least as far as the stock market is concerned, was the opposite of March: it came in like a lamb and went out like a lion. At the start of the month, there was caution and uncertainty about the election and its impact on the stock market. The conventional wisdom was that Wall Street and those in the know preferred a Clinton victory. During the campaign, when Clinton would fall in the polls, the stock market often dropped and when she would widen her lead, the markets would stabilize. Despite these moves, the net result was something of a 'wait and see' attitude.

When the results came in, after an initial drop in the futures on election night, the stock market celebrated the Donald Trump victory. In hindsight, the moves are clearly understood, but against a non-stop media onslaught about the pending catastrophe of a Trump victory, it was difficult to think unemotionally about a Trump victory and that is what led to the surprise rally.

With hindsight and a clearer vision, it's easy to visualize that a roll back of even some of the massive bank regulatory structure would be good for bank profits and a huge infrastructure spending bill would spur industrial stocks while being stimulative for the economy. When the markets also started factoring in the possibility of corporate tax reform and the return of up to $3 trillion dollars of corporate profits held overseas, there was exuberance about U.S. stocks. And few groups benefitted more than financials which are banking on less regulation and higher interest rates as a result of the assumed infrastructure spending, corporate tax reform and subsequent economic growth. Higher interest rates have a positive effect on bank profits.

To be sure, this run-up was not universal. Just look at the so called "FANG" stocks. Facebook, Apple or Amazon (take your pick), Netflix, and Google trailed the normally staid bank stocks which were on a tear. Overseas stocks also lagged, and bonds got hit hard. The growth script that the trilogy of less regulation, more infrastructure spending, and corporate tax reform brings to the market may mean higher interest rates which are generally not good for bonds. The 10 year Treasury note approached 2.40% by month end - almost back to the level we saw at the start of the year erasing much of 2016's appreciation.

Diversified investors might be looking at the headlines wondering why their balanced portfolios may not be following the Dow Jones Industrial Average into new highs. And the answer may be a result of their diversification notably the weakness in overseas stocks and U.S. bonds which had one of their worst months in recent memory. It might also be due to the somewhat concentrated nature of the rally. Take for example, the fact that only three Dow stocks are responsible for almost half of the

November gains

.

Looking forward, its important to recognize that none of the hoped for Trump policies have happened yet and stock markets always have the potential to disappoint - especially when exuberance is high. So the suggestion is to stay within your risk tolerance and stick with your long term plan. Changing investment strategy because of who is in the White House isn't a tried and true success formula. The stock market is mostly driven by corporate earnings and while things look rosy now, what will happen if interest rates - and oil prices - continue to rise? Will the rise in rates strengthen the dollar which will hurt our exports and the profits of multi-national corporations? What if there is an unforeseen overseas event that surprises Wall Street? Or what if Mr. Trump is surprised by deficit hawks in his own political party that don't go along with a massive infrastructure bill that raises the budget deficit? Nothing in politics is certain - and markets move in both directions. Usually when people least expect it.

Quote of the Day:

"Elections should be held on April 16th - the day after we pay our income taxes. That is one of the few things that might discourage politicians from being big spenders." - Thomas Sowell

Mark Avallone and the Potomac Wealth Advisors Team

P.S. Please feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, please reply to this e-mail with their e-mail address and we will ask for their permission to be added.

Potomac Wealth Advisors, LLC

15245 Shady Grove Road, Suite 410

Rockville, MD 20850

Phone: 301-279-2221

Securities and Investment Advisory Services offered through H. Beck, Inc., Member FINRA/SIPC. 6600 Rockledge Drive, 6th Floor, Bethesda, MD 20817 301.468.0100. Potomac Wealth Advisors, LLC is not affiliated with H. Beck, Inc.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding any funds or stocks in particular, nor should it be construed as a recommendation to purchase or sell a security. Past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested.

Diversification and asset allocation do not guarantee against loss. They are methods used to manage risk.

This report has been derived from information considered reliable, but it cannot be guaranteed as to accuracy or completeness.

This report has been derived from information considered reliable, but it cannot be guaranteed as to accuracy or completeness.

|

|

|

The indexes are constructed and weighted using market value-weighted index. They provide 95 percent market capitalization coverage of developed markets and emerging markets. More than 3000 DJGI indexes provide data on more than 5500 companies around the world. Market capitalization is float-adjusted *The DJIA is a widely followed measurement of the stock market. The average is comprised of 30 stocks that represent leading companies in major industries. * The Standard & Poor's 500 (S&P 500) is an unmanaged group of securities considered to be representative of the stock market in general. *The NASDAQ Composite Index is a market-valued weighted index, which measures all securities listed on the NASDAQ stock market. *The S&P Mid Cap 400 Index This Standard & Poor's index serves as a barometer for the U.S. mid-cap equities sector and is the most widely followed mid-cap index in existence. To be included in the index, a stock must have a total market capitalization that ranges from roughly $750 million to $3 billion dollars. Stocks in this index represent household names from all major industries including energy, technology, healthcare, financial and manufacturing.

*The

Russell 2000 Index is a small-cap

stock market index of the bottom 2,000 stocks in the

.

* The

MSCI EAFE Index is a

stock market index that is designed to measure the equity market performance of

developed markets outside of the U.S. & Canada. It is maintained by

MSCI Barra,

[1]a provider of investment decision support tools; the EAFE acronym stands for

Europe, Australasia and Far East.

* The MSCI

Emerging Markets Indexs a float-adjusted market capitalization index that consists of indices in 21 emerging economies: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey.

* Opinions expressed are subject to change without notice and are not intended as investment advice or to predict future performance.

*The economic forecasts set forth in the presentation may not develop as predicted and there can be no guarantee that strategies promoted will be successful.

* Consult your financial professional before making any investment decision.

* To unsubscribe from the "Potomac Wealth Advisors, LLC newsletters" please reply to this email [email protected] with "Unsubscribe" in the subject line, or click below Safeunsubscribe. You may also write us at "15245 Shady Grove Road, Suite 410, Rockville, MD, 20850

|

|

|

Learn more about Mark Avallone's recently released book, Countdown to Financial Freedom

Recognized by:

The Washington Post

as a Greater Washington DC Region Five Star Wealth Manager (2015)

The Financial Times

as one of the country's Top 401 Retirement Plan Advisor (2015)

Private Wealth Magazine

as a member of their Inaugural All-Star Research Team (2012)

Washington Business Journal

as one of Washington's Premier Wealth Advisors (2011, 2012, 2013, 2014)

NABCAP

as one of the Top Wealth Managers in the Washington, DC Metropolitan Region (2011, 2012, 2013, 2014)

SmartCEO Magazine

Magazine Money Manager Award Recipient Finalist, Washington, D.C. Metropolitan Region

(2015)

Consumers' Research Council of America

as one of America's Top Financial Planners (2011, 2012, 2013, 2014)

DC Magazine

as a Five Star Wealth Manager, Washington, D.C. Metropolitan Region (2012)

SmartCEO Magazine

Magazine Top Wealth Manager, Washington, D.C. Metropolitan Region

(2012)

Financial Advisor Magazine

as an All-Star Research Manager (2012)

|

|

|

|