|

Win $50!

|

|

There are two member numbers spelled out within the text of this eNewsletter. Find your number and give us a call at (888) 387-8632 to claim $50!

|

|

|

|

|

*Referred person must be 15 years of age or older, eligible for membership with 1st Northern California Credit Union, present a completed referral form when they apply, and become a member for referring member to receive the $25 deposit into their share account. Current members may refer up to 4 new members. Offer ends September 30, 2016.

|

|

Expanded Hours Coming Soon!

|

For your convenience,

beginning September 1, 2016

our new hours will be:

Monday - Wednesday: 9:00 am - 4:00 pm

Thursday: 9:00 am -

6:00 pm

Friday: 9:00 am - 5:00 pm

|

President's Corner President's Corner

|

Phenom rookie pitcher Nuke LaLoosh's first encounter with grizzled veteran catcher Crash Davis in the 1988 comedy "Bull Durham" was memorable. Nuke challenged Crash to a fight outside the local bar, and Crash challenged Nuke to hit Crash in the chest with a baseball. After thinking about it, Nuke threw the ball and missed Crash by several feet. Angry, Nuke charged at Crash who dropped Nuke with one punch. Crash responded, "I'm Crash Davis; I'm your new catcher, and you just got lesson number one. Don't think. You can only hurt the ball club."

To many investors, this is a difficult time to make money. Interest rates are at historical lows, the U.S. economy is increasingly tied into the rest of the world which is having their own set of problems, and government taxation and regulation partially explain decreasing manufacturing and increasing real unemployment.

Just before every recession short-term investors invested under the assumption stock prices and housing values would rise indefinitely. There are plenty of charts and graphs on the Internet clearly showing the cyclical nature of investing. The value of time is the greatest asset investors have. Over a long enough period of time, home equity will increase through monthly loan payments and appreciating market value, and stock values rise. Yes, there will be downturns, but as grizzled veteran stock broker Lou Mannheim told young buck Bud Fox in the 1987 film "Wall Street," "Quick buck artists come and go with every bull market, but the steady players make it through the bear market."

Today, smart investors don't have to think much. Instead of purchasing individual investments, anyone can invest in mutual funds which are baskets of stocks and bonds selected by professional money managers whose job it is to maximize yield based on the fund's investment objectives. Fund types include very conservative U.S. Treasury securities to highly risky international stocks. In the last few years, so-called "lifestyle" mutual funds have been created to target certain age groups, and target-date funds indexed to an individual's planned retirement date.

The keys to effective and efficient investing are diversity and cost. Mutual funds generally do a better job of diversification than purchasing individual stocks and bonds. Certain funds require less management and hence are less expensive to the investor. It saves on time and doesn't take much research and thought.

As Nuke LaLoosh matured, he began to understand the game within the game. A good friend of his used to say, "This is a very simple game. You throw the ball, you catch the ball, you hit the ball. Sometimes you win, sometimes you lose, sometimes it rains." Investing sounds a lot like baseball.

David M. Green

President/CEO

(925) 335-3802

|

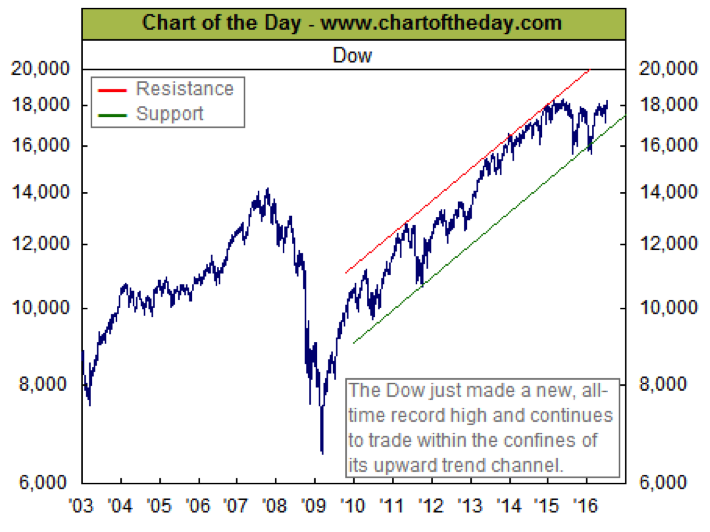

Stat-of-the-Month

|

The Dow Jones Industrial Average is at a new, all-time record high. For some perspective, this chart illustrates the overall trend of the Dow since 2003. As the chart illustrates, the Dow has rallied sharply since early 2009. Over the past six years the Dow has maintained a trend that remained well within the confines of an upward sloping trend channel (see green and red trend lines). Notice how the Dow struggled from early 2015 to early 2016 resulting in the Dow retesting support (see green line). Since early 2016, however, the Dow has rallied sharply and is now trading at a level never seen before.

|

Tips for Teens

|

Back to School Social Tips

You know school is not too far away when Walmart starts their back to school sales. Speaking of back to school sales, be sure to read the

Tips for Teens: Back to School shopping article in which Sierra discusses what items you should and should not buy.

With school so close, it's time to start seeking advice on how to survive the year. Lucky for you, I happen to have a few tips!

Incoming Freshmen: Freshman Friday is not a real thing. Chances are that if you end up in a trash can it's because you tripped over a backpack like I did. Or if you end up with a giant swollen eye, it's probably because you ran into a pole. I did that twice. Freshman year is full of new experiences and it's not anything like middle school. Don't be afraid to try new things. I joined my school's water polo team with no previous competitive swimming or water polo knowledge or experience. Literally, I had no idea that the sport existed. How did I get onto the team? They were short a few players. Yes, I was definitely the worst player on the team and almost drowned another player on our last game, but it was fun! I loved it, and if I could go back in time I would do it all again. While college may seem to be a lifetime away, don't put it off just because you're only in your first year of high school. You can start applying for scholarships and look around for possible colleges you would like to get into.

Sophomores:

This might be your hardest year. "Keep your friends close and your enemies closer." In this case, that's your homework! My advice, unless you maintained a 4.0 through freshman year and middle school, take only one AP/Honors/ROP class. There's no rush to finish college courses in high school or a college credit competition so don't do it unless if you are absolutely positive that is what you want. Also if you are going to be taking an advanced class, make sure it's a subject you're interested in.

Juniors: This was, by far, my favorite year. I found a group of friends who are all as crazy as I am. You'll find that you become more independent from your parents, and that's ok! It's called growing up. I was able to do things and go places with my friends that I might not have been allowed to back when I was a freshman. My favorite event that I attended as a Junior was Backroads Coffee House, an annual poetry reading event at my high school. It started at 9:00pm and lasted until midnight on a school night. It may sound like something a complete arts-nerd would attend, but it was amazing. If your school has something like this, I strongly recommend you going to it.

Seniors: If you aren't already feeling it, Senioritis might be setting in soon. I know it's your last year and you're anxious to move on to whatever you have planned after high school, but try to stay in the game. It's important that you continue to keep your grades up and stay focused. What better way to prepare you for the real world you're about to enter? Now that I've gotten the responsible stuff out of the way, let me add this: It's your last year of high school! Appreciate the time you have with your friends. Although we do have social media to stay in touch, life will change drastically after graduation and you may not see these friends as much. Take pictures! And last but not least, don't forget to have fun!

(EIGHT ZERO THREE FIVE)

May the grades be ever in your favor.

Luis Dominguez

Student Social Media Intern

1st Nor Cal Credit Union

|

Tips to Avoid Identity Theft

|

Identity theft continues to be a huge problem in the U.S. and gets worse every year. The damage caused can cost victims not only money but substantial time to repair. As you become wiser to the thieves' tricks, they are learning new ways to get access to your sensitive information. Follow these tips to avoid identity theft from damaging your financial security.

Always remember to:

- Safeguard your Social Security number. You should never carry your card with you.

- Shred all old financial and credit statements, including "junk mail" credit card offers and receipts containing important information. Cross-cut shredding is best, so that the strips can't be taped back together.

- Review charges on our credit card statements before paying them.

- Don't use your mailbox for outgoing mail of bill payments. If stolen from your mailbox, the payee's name can be erased with solvents.

- Check your computer for spyware or malware regularly.

- Report suspicious emails or phone calls asking for bank account or other identifying information.

- Make passwords that are difficult to replicate, and change them frequently.

- Shop on websites that you know you can trust.

- Check your account records regularly, as well as your credit reports, since these are the best methods of early detection.

Most experts agree that even if you take all of the right precautions, you may not be able to prevent identity theft fraud from happening, in part because your personal information is not always in your control. What you can do is protect yourself with coverage that helps you in the event that you are a victim. Most homeowners insurance offers an option to include Identity Theft coverage for about $25/year.

As an added benefit of your 1st Nor Cal membership

, we at Lou Aggetta Insurance will help you review the things that are important to you and provide you with

options for reducing risk in your life. We are an independent insurance agent and can provide you with home, auto, life, health, business and many other types of insurance coverage.

Contact me today to schedule your free review.

Denia Aggetta Shields

Lou Aggetta Insurance, Inc.

2637 Pleasant Hill Road

Pleasant Hill, CA 94523

(925) 945-6161

|

Retirement Solutions

|

Deciding when to retire may not

be as simple as it used to be.

By Jason Vitucci, CFP & Gene A. Schnabel

Today, retirees are facing a volatile economy and living longer than the generations before them. This brochure can help you understand some of the opportunities and challenges you may face in retirement, so you can take them into account as you determine your retirement age.

First Steps

Start by assessing where you are today - and addressing the concerns you may face tomorrow.

STEP 1:

Income Analysis

The first step in deciding when to retire is to estimate how much income you will need, and how much income you will have, in retirement.

When considering retirement you need to identify your potential retirement income sources, such as Social Security retirement benefits, pensions, income from savings, and your potential expenses - including health care costs, food, and housing.

For many, Social Security retirement benefits are often a main source of retirement income. Knowing when Social Security benefits are available to you and estimating what those benefits might be can help you make informed decisions on when to start taking benefits. You may be able to receive Social Security benefits as early as age 62 (if you qualify). But keep in mind that if you retire early, you'll receive at least 25% less Social Security income annually than if you wait until full retirement age (FRA). Also, postponing retirement past your FRA could mean an increased benefit of 8% more per year until age 70, when the maximum Social Security benefit is available. (Please refer to the Social Security Administration to discuss your specific situation.)

If you have an income gap - in other words, your projected expenses are greater than your projected retirement income - you may need to consider other available sources of income. Or you may also need to consider adjusting your overall retirement strategy, which could mean delaying your retirement age.

STEP 2:

Health Care Costs

Health care costs could be a big part of your retirement expenses. That's because, if you retire before age 65, you may need to pay for your own health insurance. The federal Consolidated Omnibus Budget Reconciliation Act (COBRA) does require that some employers offer medical insurance if you terminate employment before age 65, but usually only for 18 months - and the premiums may be higher than what they were when you were employed.

Also, it's important to consider that although the federal government's Medicare program may be available at age 65, it doesn't cover all health care costs. Plus, it also requires a monthly premium for Part B coverage, and deductibles for hospitalization.

STEP 3:

Other Employee-Sponsored Benefits

Retiring - at any age - may also mean giving up many other benefits such as employer-sponsored life insurance, employer contributions to health savings accounts (HSAs), disability income insurance, vision plans, and dental insurance.

Before deciding to retire, find out whether any of those employee benefits can continue into retirement, and at what cost to you. If those benefits are not covered after retirement, it's important to add them as a potential expense in your income analysis above.

STEP 4:

Phased Retirement

Some people prefer to ease into retirement, either through phased retirement with their current employer or part-time employment elsewhere. If you are considering either of these options, be sure the wages you receive from a phased retirement option will be enough to sustain your current living expenses.

Also be sure to ask whether the employer will provide health insurance, whether you may continue or begin contributing to the employer's 401(k) plan, and whether the employer matches your 401(k) contributions.

Finally, consider how many years you expect to be able to work, based on potential health issues you and your loved ones may be facing. It's possible you may be forced into retirement earlier than planned because of health or caregiver reasons.

STEP 5:

Personal Readiness to Retire

Many people overlook one final question as they decide when to retire: How will you spend your time in retirement? Though early retirement can sound attractive because it frees up time to travel, pursue hobbies, and be with your family, some early retirees find that they have excess time on their hands. Whether you decide to retire early or at normal retirement age, think about how you'll spend your time - and consider volunteering or part-time work if personal fulfillment might be an issue for you.

At Vitucci Integrated Planning, we are happy to take a look at your current retirement plan. As a valued credit union member, we invite you to contact us for a complimentary financial planning meeting. We also invite you to attend any of our Retirement Planning workshops that we hold. We have workshops coming up on Saturday, September 10th and Saturday, October 1st. For more information about our practice, our workshops, or to make an appointment, please call us at (925) 370-3750 or visit our website www.vitucciintegratedplanning.com.

Vitucci Integrated Planning

1330 Arnold Drive, Suite 249

Martinez, CA 94553

Securities through First Allied Securities, a registered broker dealer, member FINRA/SIPC. Advisory services offered through First Allied Advisory Services, Inc. Registered Investment Advisor. Investments not FDIC or NCUA/NCUSIF insured, not insured by Credit Union, may lose value. Products offered are not guarantees or obligations of the Credit Union, and may involve investment risk including possible loss of principal.

1st Nor Cal CU, Bay Area Retirement Solutions and First Allied are all separate entities.

Gene A. Schnabel CA Insurance Lic.: 0663016, Jason Vitucci CA Insurance Lic.: 0F59894

This article is designed to provide general information on the subjects covered. Please note that we do not give legal advice at all, for advice related to your Social Security benefits we would require meeting in person to begin the financial planning process. For more information, please visit your tax advisor, attorney, Social Security Administration office, or www.ssa.gov for your particular situation.

|

FREE Financial Counseling

|

Are you in need of financial counseling?

1st Nor Cal is here to help. Timely and honest debt advice is available to our members at no cost or obligation. Learn how to manage your finances.

(TWO FOUR ONE EIGHT TWO)

Make your appointment TODAY!

Just a reminder, you can annually request FREE Credit Reports from all 3 credit reporting agencies online by going to:

For FREE Financial Counseling, don't hesitate to contact:

Shelley Murphy

Senior Vice President of Lending & Collections

(925) 228-7550 Ext.824

|

Did you know we're on Social Media?

|

New Video - Oz

|

|

|