|

Win $50!

|

|

There are two member numbers spelled out within the text of this eNewsletter. Find your number and give us a call at (888) 387-8632 to claim $50!

|

|

|

|

|

*Referred person must be 15 years of age or older, eligible for membership with 1st Northern California Credit Union, present a completed referral form when they apply, and become a member for referring member to receive the $25 deposit into their share account. Current members may refer up to 4 new members. Offer ends March 31, 2016.

*Referred person must be 15 years of age or older, eligible for membership with 1st Northern California Credit Union, present a completed referral form when they apply, and become a member for referring member to receive the $25 deposit into their share account. Current members may refer up to 4 new members. Offer ends March 31, 2016.

|

President's Corner President's Corner

|

If you liked ZIRP, you'll love NIRP. From the beginning of the Great Recession in 2007, interest rates decreased to almost zero. The Federal Reserve employed a strategy called ZIRP (Zero Interest Rate Policy), a method of stimulating economic growth while keeping interest rates close to zero. Even with the Fed raising rates 1/4% in December, ZIRP is still in effect.

How's that working out for you, Fed board members? The answer is, not much. Economic growth has been below historical growth since the most recent recession. Many economists think that lower growth is the "new normal" which we can expect in the future, regardless of which economic levers the central bank's "Gang of Nine" pulls.

Now, for the first time in American history, the Fed is considering NIRP (Negative Interest Rate Policy) which means Fed depositors, generally banks and some of the larger credit unions, will pay to keep their money on deposit instead of receiving any positive interest. The Fed is trying to incentivize banks and credit unions to lend more which will lead to hopefully stimulating the economy. Unfortunately, compliance regulations heaped on by state and federal governments are hampering loan growth. In particular, new mortgage loan documentation has made financing a home more complicated.

There is international precedent for NIRP. Switzerland implemented NIRP in the 1970s to counteract its currency's rapid appreciation. Sweden and Denmark used negative interest rates to slow down money flowing into their economy at the beginning of this century. More recently, the European Central Bank instituted NIRP to prevent the Eurozone from circling the deflationary drain.

It is doubtful that banks and credit unions will charge their customers and members for deposited funds. Some may increase loan rates and charge additional fees to make up the revenue shortfall. Money market funds may "break the buck" by returning less than $1.00 per share.

We've already seen significant volatility in the stock and bond markets and oil prices in the first month and a half of 2016. It's becoming clearer that a bear market and possible recession are in the near future. No one knows how ZIRP or NIRP factor into this volatility, or if the volatility factors into Fed decisions. One thing we do know is that it won't be boring.

David M. Green

President/CEO

(925) 335-3802

|

Stat-of-the-Month

|

In terms of the presidential cycle, the market is fast approaching what has historically been the most difficult leg of the four-year cycle. Early in a new presidential term and with the next election several years away, the powers that be tend to be more willing to address (or at least consider the possibility of negotiating about) such quaint topics as fiscal responsibility and budget deficits. The downside to this 'belt tightening' is that it can be a drag on the economy. This chart illustrates how the market has performed following a presidential election year high (plus or minus one quarter) until the following mid-term year low. In short, the market has tended to struggle significantly from an election-year peak to mid-term year low with a few exceptions (e.g. the run-up prior to the 1987 crash, the tail-end of the dot-com boom and during the post-financial crisis rally).

(EIGHT ZERO THREE TWO)

|

Tips for Teens - Buying vs Streaming

|

You might want to sit down for this one. Your Netflix and/or Spotify account is costing more than you think. You might want to sit down for this one. Your Netflix and/or Spotify account is costing more than you think.

Most of you have probably heard of Netflix or Spotify at some point in time. For Netflix, you pay anywhere from $7.99 to $11.99 a month and for Spotify you pay $4.99 (

for students

) to $9.99 a month. Both of these services sound like they're a great deal since they let you stream on demand any song or movie you can think of.

Almost

any song or movie you can think of.

You see, these services can only stream content they have a right to stream. Remember when Taylor Swift released 1982 and you couldn't hear Blank Space on Spotify? This is because she didn't want her music being streamed on Spotify, which is something all music artists and production companies have the right to decide. You might have also noticed by now that The Hunger Games is missing from the Netflix catalog. This is because Netflix did not renew their contract to stream STARZ content which resulted in Netflix being unable to stream The Hunger Games and Transformers: Age of Extinction, to name a couple titles. This is the first flaw streaming services have; they can lose or be denied the right to stream content. Let's say you're watching Grey's Anatomy on Netflix and one day it's gone and there is nothing you can do about it. Sounds pretty extreme right? Well it does happen. Not often, but it does happen.

The second and biggest flaw streaming services have is the cost. Like I said above, for Netflix, you pay anywhere from $7.99 to $11.99 a month and for Spotify you pay $4.99 (

for students

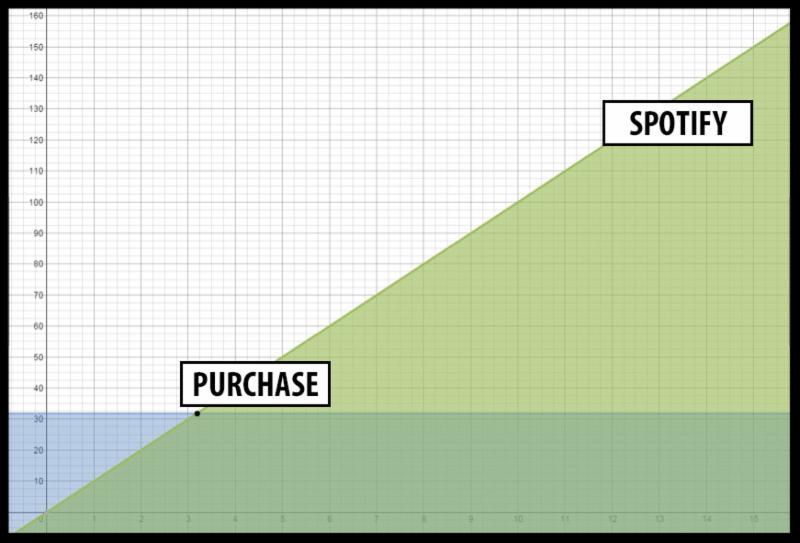

) to $9.99 a month. EVERY MONTH. It doesn't seem like a lot of money upfront, but in the long run, it adds up. Let me put this into perspective. In the past month, I have listened to the following albums: Dopamine by BØRNS, This is Acting and 1000 Forms of Fear by Sia; and to the following singles: New Americana by Halsey, Dreams by Brandi Carlile, and Rocketeer by Far East Movement. If I were to purchase everything I've heard in the past month on Google Play (my digital media store of choice), it would cost me $31.84 dollars or about 3 months and 6 days of a Spotify Premium ($9.99) subscription. You may be wondering why this is a big deal. I would only have to pay $31.84 dollars and the music would be mine forever, with no ads and the ability to download it onto my phone or as an MP3 file. With Spotify I would pay $9.99 every single month for the ability to play the music with no ads and the ability to download it only onto my phone. Now, let's say that I only listen to these songs for a year (which is very probable since I love them). I could pay $31.84 on Google Play OR $119.88 on Spotify, as illustrated below:

The green symbolizes the cost of a Spotify Premium account. As you can see, Spotify gets more and more expensive every month past the breakeven point. The breakeven point, shown in blue, is how much it would cost to own the music I would have listened to on Spotify this year.

The worst thing of all is that when you stop paying for your Spotify account, you lose access to the music on Spotify, thereafter.

Netflix is also guilty of this. I calculated how much my family and I have spent on my digital movies and TV library for the past 6 years, which totaled $562.61. Using the same concept as above, I present you the following graph:

The red symbolizes the cost of a Netflix account at $8.99 per month. The breakeven point, shown in blue, is how much we have spent on our digital library. One thing to note is that the breakeven point is after 62 months, which is about 5 years, making Netflix at least a little more cost effective than a Spotify account.

I encourage you to figure out how much it would cost to buy all the music you listen to and/or the movies and shows you view for the year, and compare it to your streaming costs. You will probably find that you're paying more than you need to by sticking to streaming services.

Luis Dominguez

Student Social Media Intern

1st Nor Cal Credit Union

|

Retirement Planning Can Start with an IRA

|

|

These accounts make a good "first step" in retirement saving.

By Jason Vitucci, CFP & Gene A Schnabel

Sooner or later, people decide to start saving and investing for retirement. When that starting point arrives, taking that "first step" can seem like a big deal. Opening an Individual Retirement Account (IRA) amounts to an easy "first step" in retirement saving for many.

When you invest through a traditional or Roth IRA, you give those invested assets the potential to grow with compounding and you also position yourself for present or future tax savings.

How does an IRA work?

An IRA is not an investment in itself, but an account into which various investments can be placed. It is yours; you control it. In that way, it differs from an employer-sponsored retirement account that you lose immediate control over when you leave a job.2

IRAs are tax-advantaged. In both Roth and traditional IRAs, account earnings compound with tax deferral until withdrawn - that is, they grow without being taxed.

With a traditional IRA, contributions are usually tax-deductible, based on your income, but withdrawals are taxed as ordinary income after age 59 1/2 (a 10% penalty often applies to withdrawals made before that). With a Roth IRA, tax-deductible contributions are not permitted, but your earnings can be withdrawn tax-free. (Contributions will not be taxed when you withdraw them either, as long as you are the original IRA owner and have had the Roth IRA for more than five years.)2

So there you have the main difference between a traditional IRA and Roth IRA: while both give you a chance to build retirement savings with tax advantages, the traditional IRA offers you a sizable tax break today while the Roth IRA offers you a big tax break tomorrow. Or to put it another way (as some have), a traditional IRA lets you amass tax-deferred savings while a Roth IRA lets you amass tax-exempt savings.2,3

Should you open a traditional IRA or Roth IRA?

Several variables should be considered as you make your choice, and a chat with a financial professional can help you weigh them. One key question to consider: do you think you will be in a lower tax bracket when you retire? If you do, a traditional IRA might be the better choice. If you have decades to go until retirement and think you will retire to a higher tax bracket than you are in today, the Roth IRA may be the better choice. Some savers "hedge their bets" and open Roth and traditional IRAs.4

Given compounding, the future tax break offered by a Roth IRA may be profound indeed. Roth IRAs also have two other compelling features. One, you never have to make mandatory withdrawals from them starting in your seventies (as with traditional IRAs). Two, you can keep contributing to them all your life, whereas contributions to a traditional IRA are prohibited after the year in which you turn 70 1/2. Certain couples and individuals cannot have Roth IRAs, however, as they have incomes well over $100,000 (the precise thresholds are periodically adjusted upward for inflation).2

Some traditional IRA owners convert their accounts to Roth IRAs. That is a taxable event, and if the traditional IRA is large, a Roth conversion may not be worth the effort: the resulting income tax bill may be too large to handle and even offset the potential long-range benefits.4

How do you open an IRA?

Just about any financial professional can help you do that; we are certainly happy to help. Quite often, opening an IRA is just a matter of filling out an application (and a beneficiary form) and writing a check. Alternately, you may be able to transfer money from a bank account to start an IRA.5

What are the drawbacks of IRAs?

First, their annual contribution limits. Right now, you can only contribute a maximum of $5,500 a year to a traditional or Roth IRA ($6,500 if you are 50 or older). If you have multiple IRAs, your total yearly contributions to all of them must not exceed that limit or you will incur an IRS penalty. This annual contribution ceiling is low compared to common workplace retirement plans such as 401(k)s and 403(b)s.6

Many Americans would like a retirement account that never loses money. A Roth or traditional IRA is not that account. IRA assets are not usually allocated to riskless investments, and when you have investment risk, you have potential for investment losses. IRAs are not insured by the FDIC or any other federal agency.2

At Bay Area Retirement Solutions, we are happy to take a look at your current financial plan. As a valued credit union member, we invite you to contact us for a complimentary financial plan review. We also invite you to attend any of our Retirement Planning workshops that we hold. For more information about our practice, our workshops, or to make an appointment, please call us at (925) 370-3750 or visit our website www.bayarearetirementsolutions.com.

Bay Area Retirement Solutions

1330 Arnold Drive, Suite 249

Martinez, CA 94553

Securities through First Allied Securities, a registered broker dealer, member FINRA/SIPC. Advisory services offered through First Allied Advisory Services, Inc. Registered Investment Advisor. Investments not FDIC or NCUA/NCUSIF insured, not insured by Credit Union, may lose value. Products offered are not guarantees or obligations of the Credit Union, and may involve investment risk including possible loss of principal.

1st Northern California Credit Union, Bay Area Retirement Solutions and First Allied are all separate entities.

Gene A. Schnabel CA Insurance Lic.: 0663016, Jason Vitucci CA Insurance Lic.: 0F59894

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note - investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Citations.

2: us.hsbc.com/1/2/home/invest-retire/retirement/ira [2/16/15]

3: fool.com/money/allaboutiras/allaboutiras03.htm [2/16/15]

4: schwab.com/public/schwab/nn/articles/Roth-IRA-Conversion-Look-Before-You-Leap [5/1/14]

5: fool.com/money/allaboutiras/allaboutiras14.htm [2/16/15]

6: fool.com/retirement/iras/2015/01/11/ira-contribution-limits-in-2014-and-2015-and-how-t.aspx [1/11/15]

7: money.usnews.com/money/retirement/articles/2014/11/24/how-retirement-benefits-will-change-in-2015 [11/24/14]

8: myra.treasury.gov/about/ [11/24/14]

|

11% cash back on all purchases when using a 1st Northern California Visa Credit Card. Excludes cash advances and balance transfers. Rebate applied monthly to Visa Credit Card account balance. Rebate cannot exceed $10 per month and/or $120 per year. Terms are subject to change without notice.

11% cash back on all purchases when using a 1st Northern California Visa Credit Card. Excludes cash advances and balance transfers. Rebate applied monthly to Visa Credit Card account balance. Rebate cannot exceed $10 per month and/or $120 per year. Terms are subject to change without notice.

|

New & Innovative Earthquake Program

|

An Earthquake can be financially devastating to a homeowner, yet in California less than 10% currently have EQ coverage. Certainly part of the reason is the cost, since the premium can easily exceed what your Homeowners premium is. The other reason is that in the past the lowest deductible you could find was 10%. We now have a now have an Earthquake policy that can be tailored to your individual needs. Some of the highlights of this program are:

- Deductibles as low as 2.5%

- Choose your limits for Other Structures, Contents & Additional Living Expenses

- Rates apply separately for each coverage, so you only pay for the coverage you need

- No age restrictions

Serious earthquakes in CA will happen, often with disastrous results. Even if you currently have coverage through the CEA or another insurer, it is worth your time to have us requote your coverage. If you do not have earthquake coverage, get a quote so you may make an educated decision about your coverage needs. Preparing for the next big one is not always enough... insurance provides security & peace of mind.

As an added benefit of your 1st Nor Cal membership

, we at Lou Aggetta Insurance will help you review the things that are important to you and provide you with

options for reducing risk in your life. We are an independent insurance agent and can provide you with home, auto, life, health, business and many other types of insurance coverage.

Contact me today to schedule your free review.

Denia Aggetta Shields

Lou Aggetta Insurance

2637 Pleasant Hill Road

Pleasant Hill, CA 94523

(925) 945-6161

|

FREE Financial Counseling

|

Are you in need of financial counseling?

1st Nor Cal is here to help. Timely and honest debt advice is available to our members at no cost or obligation. Learn how to manage your finances.

(THREE SIX NINE EIGHT SIX)

Make your appointment TODAY!

Just a reminder, you can annually request FREE Credit Reports from all 3 credit reporting agencies online by going to:

For FREE Financial Counseling, don't hesitate to contact:

Shelley Murphy

Senior Vice President of Lending & Collections

(925) 228-7550 Ext.824

|

Did you know we're on Social Media?

|

Game of Zombies

|

|

|