|

Mortgage Applications rise 2.3%, led by homebuyers

by CNBC

Buyers are returning to the housing market in ever growing numbers, as indicated by continued gains in loan applications to purchase a home.

Total mortgage application volume rose 2.3 percent week to week on a seasonally adjusted basis for the week ending April 17th, according to the Mortgage Bankers Association (MBA). The gain was driven largely by purchase applications, not refinances, even despite lower mortgage rates.

"Purchase applications increased for the fourth time in five weeks as we proceed further into the spring home buying season," said Mike Fratantoni, chief economist for the MBA. "Applications for FHA [government insured] purchase loans remained strong as well."

Mortgage applications to buy a home increased 5 percent from the previous week and are now 16 percent higher than the same week one year ago. Applications to refinance increased just one percent, but they are still up 41 percent from a year ago, when rates were considerably higher, around 4.25 percent.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($417,000 or less) last week decreased to 3.83 percent, its lowest level since January 2015, from 3.87 percent, with points decreasing to 0.32 from 0.38 (including the origination fee) for 80 percent loan-to-value ratio (LTV) loans, according to the MBA survey.

Rates haven't moved very much lately, which may be why homeowners have seen little incentive to refinance.

"In general, there's a pervasive air of dispassionate complacency," wrote Matthew Graham of Mortgage News Daily, regarding what he called the "flatness" of rates. "It would be easy to assume that the gorilla will reach the room when the Fed Announcement comes out next Wednesday, but then again, markets might be let down by a lack of 'clues' regarding the Fed's rate hike timeline."

While most analysts expect rates to rise through the course of this year, some now believe they could go even lower, given how little overseas bond markets have to offer investors. If investors continue to buy U.S. Treasury bonds, and if a still slow housing market means fewer-than-average mortgages and mortgage-backed securities are issued, rates in fact could move lower.

|

|

Why Higher Interest Rates Will Worsen the Housing Market

by DailyFinance.com

If you're looking to buy a home in the next year, you might want to do so before higher interest rates make financing such big-ticket purchases a lot more expensive. The Federal Reserve, which controls the supply of U.S. dollars and short-term interest rates, has indicated that it could start raising rates as soon as June.

Interest rates have been so low for so long that people might have forgotten what it's like to pay "normal" interest rates of 6 percent to 8 percent for a loan. But if rates rise, the impact will be felt by nearly everyone trying to buy a home and even those trying to sell their home.

Interest Rates and Borrowing Power

When you apply for a loan at a bank, they try to assess your ability to pay back the loan given your income and the loan's monthly payment. The higher your income, the larger the allowed payment, but interest rates play a big role in how large the payment will be. Even a slight rise in historically low interest rates could make it a lot more expensive.

Below, I've laid out the monthly payments for 15-year and 30-year $100,000 mortgages at different interest rates, not including any fees, like private mortgage insurance or property taxes. As you can see, a 1-percentage-point increase in interest rates from 4 percent to 5 percent on a 30-year mortgage results in a 13 percent jump in monthly payments. A 2-percentage-point increase results in an incredible 26 percent increase in monthly payments.

| Term |

4% Interest |

4.5% Interest |

5% Interest |

6% Interest |

| 15-Year Mortgage |

$740 |

$765 |

$791 |

$844 |

| 30-Year Mortgage |

$477 |

$507 |

$537 |

$600 |

Source data: Google mortgage calculator

The reason those higher payments are important is that they play into how much borrowing power you have. A bank is trying to figure out how much it can loan you and still expect you to pay it back on time, but the bank doesn't necessarily care how big the loan is. What it really cares about is whether you can make the monthly payment.

So, let's look at how a constant monthly payment impacts the size of home you may be able to buy. Below, I've calculated the maximum loan that could be taken out for the corresponding payments and interest rates.

| Monthly Payment |

4% Interest |

4.5% Interest |

5% Interest |

6% Interest |

| $1,000 |

$209,461 |

$197,361 |

$186,282 |

$166,792 |

| $2,000 |

$418,922 |

$394,722 |

$372,563 |

$333,583 |

| $3,000 |

$628,384 |

$592,083 |

$558,845 |

$500,375 |

Source data: Google mortgage calculator

Even with the same monthly payment, a 2-percentage-point increase in interest rate reduces borrowing power by 20 percent. As rates rise, that could have a major impact on not only your purchasing power but the entire housing industry.

Why Interest Rates Would Hurt Housing

This dynamic among payments, interest rates and borrowing power could have a profound impact on a housing market that's still recovering from the recession.

When you get a mortgage, the amount you can borrow depends on how much money you make and how much the monthly payment of the mortgage will be. It's no secret that wages haven't risen much at all recently in the U.S., so recently the improving housing market has been driven by the borrowing power that low interest rates have provided rather than extra income from higher wages. If interest rates rise, even slightly, they could actually send home prices -- and home values -- lower, simply by reducing the ability of new buyers to pay for a home.

For millions of Americans, the impact of lower home values could be enormous because the home is the biggest asset a majority of Americans own. And since most people have a mortgage, it's a leveraged asset, meaning losses are magnified.

If you buy a home with 20 percent down and then sell it a few years later but can only get 90% percent of the price you paid, your loss is half of your down payment. That's a big loss on an asset that people don't usually expect to lose money on.

Higher Interest Rates Are Coming -- Someday

There's no doubt that higher interest rates are coming someday; the challenge is that no one knows quite when they'll arrive. With the economy and unemployment improving, the market is currently betting that the second half of 2015 will start to see higher interest rates, and consumers should know how it could impact them.

Higher interest rates mean lower borrowing power, so whether you're thinking about buying or selling a home, you might want to start thinking about how those changes will impact you in the future.

|

|

5 Reasons (Besides Money) Retirees Go Back to Work

by DailyFinance.com

Motivated, driven people who love their work -- and paycheck -- may find themselves back at a desk before they can make it to the golf course. According to a survey by CareerBuilder, 60 percent of workers age 60 and older will look for a new job after retiring. Here are some reasons you may head back to the office after you retire, even if you think you'll love being a pensioner.

1. Pursue an Encore Career

An encore career allows retirees to pursue a profession that may boost their financial stability while also providing personal fulfillment, and "the trend is catching on," says Erin Bramblett, senior human resources specialist at Insperity.

A recent Encore.org study revealed more than 4.5 million people between the ages of 50 and 70 are involved in encore careers. Popular sectors for these careers include public service, education or other opportunities that allow people to give back. "They want to do something different, stay inspired, stay informed, but they wont do their day job anymore," says Jason Ting, senior vice president of wealth management at Merrill Lynch.

"Many of them are going to use their skill set to do something for a nonprofit. They want to be able to talk to people, get to know people and learn something from another generation," he explains. "These people may not need to work, but they desperately want to stay up-to-date and feel challenged."

2. Have a Purpose

Some professionals can't imagine not working after many years of having a commitment to their career, Bramblett says. Many times, family and friends may pressure a person into retirement because they feel their loved one has "earned the right to stop working."

"They may not understand the desire to keep putting in the hours and have a purpose in life," she explains. "However, for reluctant retirees, work likely serves as a constant to fall back on and holds an individual accountable. Some simply don't know how not to work."

Many people have a large part of their identity and self-worth tied up in their jobs, Ting says. When they leave the industry or office they love, it's only natural to want to find a new challenge.

"Let's say you have a certain skill set and you've been at the same job for 20 years. When you take your skill set somewhere else, it can be a breath of fresh air. You have a new group of people appreciating your talent and it can actually be a boost your self-esteem. You feelings of self-worth increase when you see how much people value what you bring to the table."

3. Stay Physically Active

Very few people plan to retire and just do nothing, Ting says. But many people overestimate how much time their hobbies will consume.

"They say they are going to go golfing and travel, but you can't do that all the time. How many times are you really going to get out on the golf course? Maybe once per week? What is the rest of your schedule going to look like?"

Oftentimes people who leave the workforce find that they not only miss the routine of having somewhere to be every morning, but also crave the physical exercise associated with climbing stairs, walking around the office or traveling to meetings and conferences.

"A lot of our clients watched their parents retire at 50 or 60 and they saw them age quickly. They say, 'I don't want to be like that. I want to be active in my older years, and I have a lot of years remaining,'" Ting says.

4. Keep the Mind Sharp

Doctors recommend that retirees keep their minds active to avoid premature memory loss, Bramblett says. The earlier a professional retires, the sooner mental capacity can begin to decrease. According to the Center on Longevity at Stanford University, work plays a key role in keeping the mind functioning optimally.

"Retirement often ushers in a slower pace, but it could prove too slow for some," she cautions. "After many years of work, most individuals look forward to a shorter to-do list, less stress and more relaxation time. However, after the initial excitement of retirement wears off, some retirees, especially those without regular social or educational activities, could find themselves bored or lonely after having an empty schedule week after week. Going back to work in some capacity will allow retirees to once again feel challenged and socially engaged."

5. Earn Cash -- Maybe for the Family

Today's retirees are both concerned about and excited by their "longevity bonus," Ting says. "Fifty or 60 years ago, you went to school, you worked, you lived a few extra years and you died," he says. Now people are living comfortably to age 90, so you have this whole extra life after you retire. People are asking themselves, 'What are we going to do with our longevity bonus?' Yes, you can travel and spend time with the grandkids, but you're also going to need money to live comfortably during that time."

Some retirees may not need additional funds for themselves, but may go back to work due to unexpected family expenses, Bramblett says. According to a Merrill Lynch retirement study, 62 percent of people 50 and older are providing financial support to family members. "Whether it is because of a layoff, health issues or other factors, money can suddenly become tight for a close relative or friend," she said. |

|

U.S. Economy Still on Track for Best Year Since 2005

by CNN Money

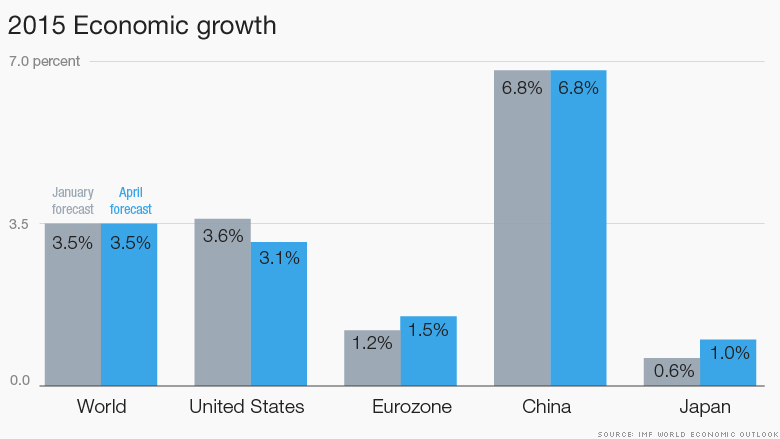

The U.S. economy should manage growth of 3% or more in 2015 despite a poor start to the year, the International Monetary Fund said Tuesday. Official data for the first quarter will be released April 29, and forecasters are marking down their numbers due to weak spending by consumers and businesses. The IMF cut its forecast for U.S. GDP growth in 2015 to 3.1%, from 3.6% in January. But that's still much better than 2014, when the economy grew by 2.4%. Low oil prices should begin to feed through to consumer spending, the IMF said, and even a gradual rise in interest rates and the strong dollar shouldn't prevent the U.S. from turning in its best performance since 2005. "For the U.S. the strong dollar is good but it slows down spending," said Olivier Blanchard, chief economist at the IMF. "But the U.S. has the tools to respond to it if the economy were to slow down. They could ... increase interest rates later, or may be able to use fiscal [stimulus]." The flip side of a strong dollar is a weak euro and yen, which have lost about 25% and 10% of their value respectively since the start of 2014. That should support the tentative recoveries in Europe and Japan. The IMF raised its forecast for eurozone growth to 1.5%, compared with 1.2% in January, and for Japan to 1%. Central banks in both economies are pumping vast quantities of cheap money into their banking systems to stimulate demand. At 3.5%, the IMF's global growth projection is unchanged since its last update and just a shade stronger than 2014. High levels of debt -- public, household, or corporate -- continue to act as a brake on the world economy. "Financial crises leave long scars," said Blanchard. "In most countries there is one of these things that is not right, there is a level of debt that is too high." Advanced economies will make up for slower growth in most of the major emerging markets. China's growth will slow to 6.8% from 7.4% last year. But India should power ahead with growth of 7.5% in 2015, according to the IMF.

|

|